Reports >

Technology And Media

>

Food Robotics Market Report

Food Robotics Market Report

First published: 24 September 2024 | Last updated: 31 January 2026 | Report Code: food-robotics

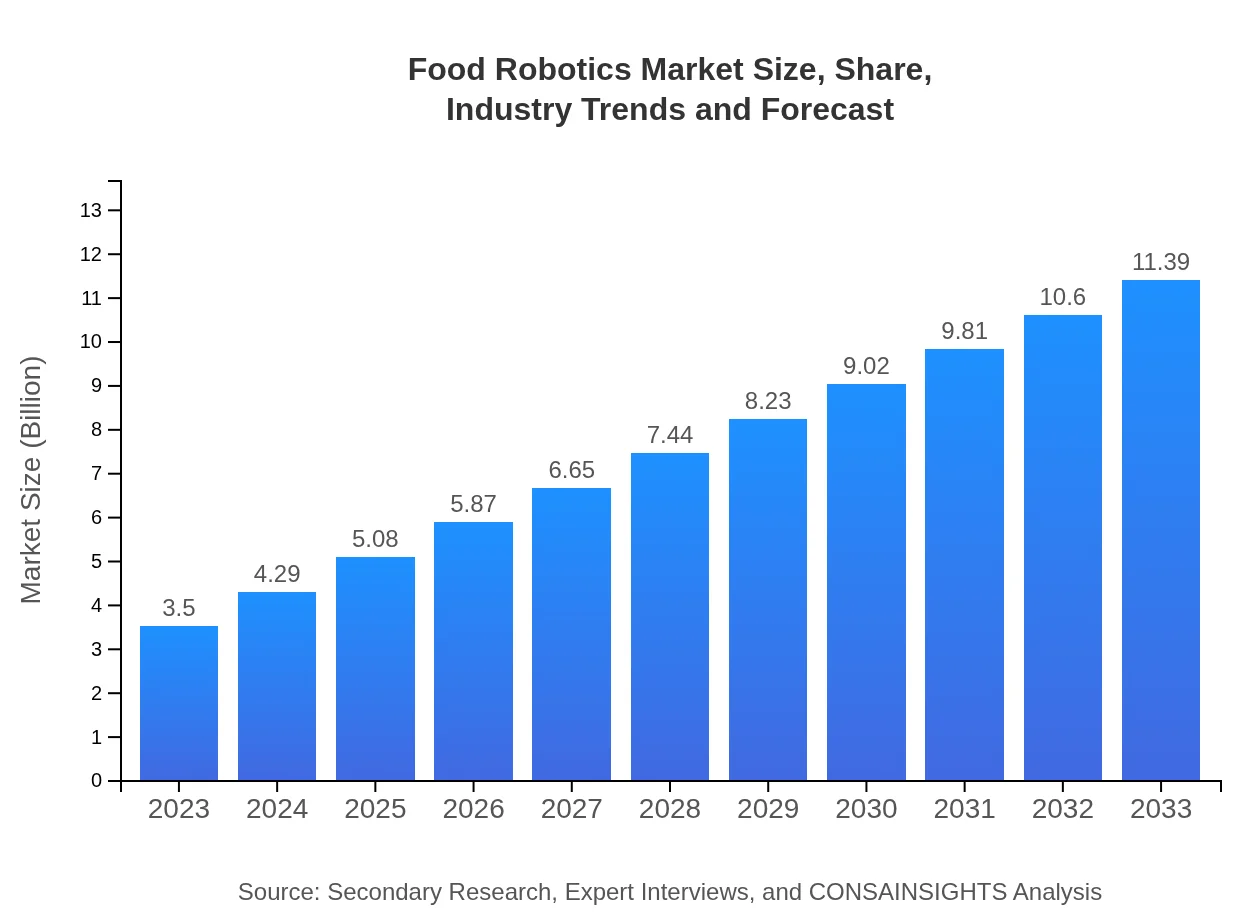

Food Robotics Market — USD 3.5 billion in 2023, Growing to USD 11.39B by 2033 at 12% CAGR

This report provides an in-depth analysis of the Food Robotics market, covering key insights, market size, trends, and forecasts from 2023 to 2033. It evaluates regional dynamics, product types, and technological advancements impacting the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $3.50 Billion |

| CAGR (2023-2033) | 12% |

| 2033 Market Size | $11.39 Billion |

| Top Companies | ABB Robotics, KUKA AG, Fanuc Corporation, Yaskawa Electric Corporation, Robot Coupe |

| Published Date | 24 September 2024 |

| Last Modified Date | 31 January 2026 |

Food Robotics Market Overview

Customize Food Robotics Market Report market research report

- ✔ Get in-depth analysis of Food Robotics market size, growth, and forecasts.

- ✔ Understand Food Robotics's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Food Robotics

What is the Market Size & CAGR of Food Robotics market in 2023?

Food Robotics Industry Analysis

Food Robotics Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Food Robotics Market Analysis Report by Region

Europe Food Robotics Market Report:

In Europe, the market for Food Robotics stands at $0.86 billion in 2023 and is projected to grow to $2.78 billion by 2033. Strong regulations regarding food safety and quality are driving the adoption of robotics, particularly in food processing and packaging.Asia Pacific Food Robotics Market Report:

In 2023, the Food Robotics market in the Asia Pacific region is valued at $0.73 billion and is projected to reach $2.37 billion by 2033. The growth is largely driven by the rapid urbanization and increasing demand for automation in food services and manufacturing sectors.North America Food Robotics Market Report:

North America, with a market size of $1.19 billion in 2023, is expected to grow to $3.86 billion by 2033. High adoption rates of robotic systems in restaurants and food distribution significantly contribute to this growth, supported by technological innovation and consumer trends.South America Food Robotics Market Report:

The South American Food Robotics market, valued at $0.32 billion in 2023, is forecasted to reach $1.03 billion by 2033. The market growth in this region is propelled by increasing investments in enhancing food processing infrastructure.Middle East & Africa Food Robotics Market Report:

The Middle East and Africa market is estimated at $0.41 billion in 2023, expanding to $1.34 billion by 2033. This growth is attributed to the rising demand for automation to enhance food production processes and improve efficiency.Tell us your focus area and get a customized research report.

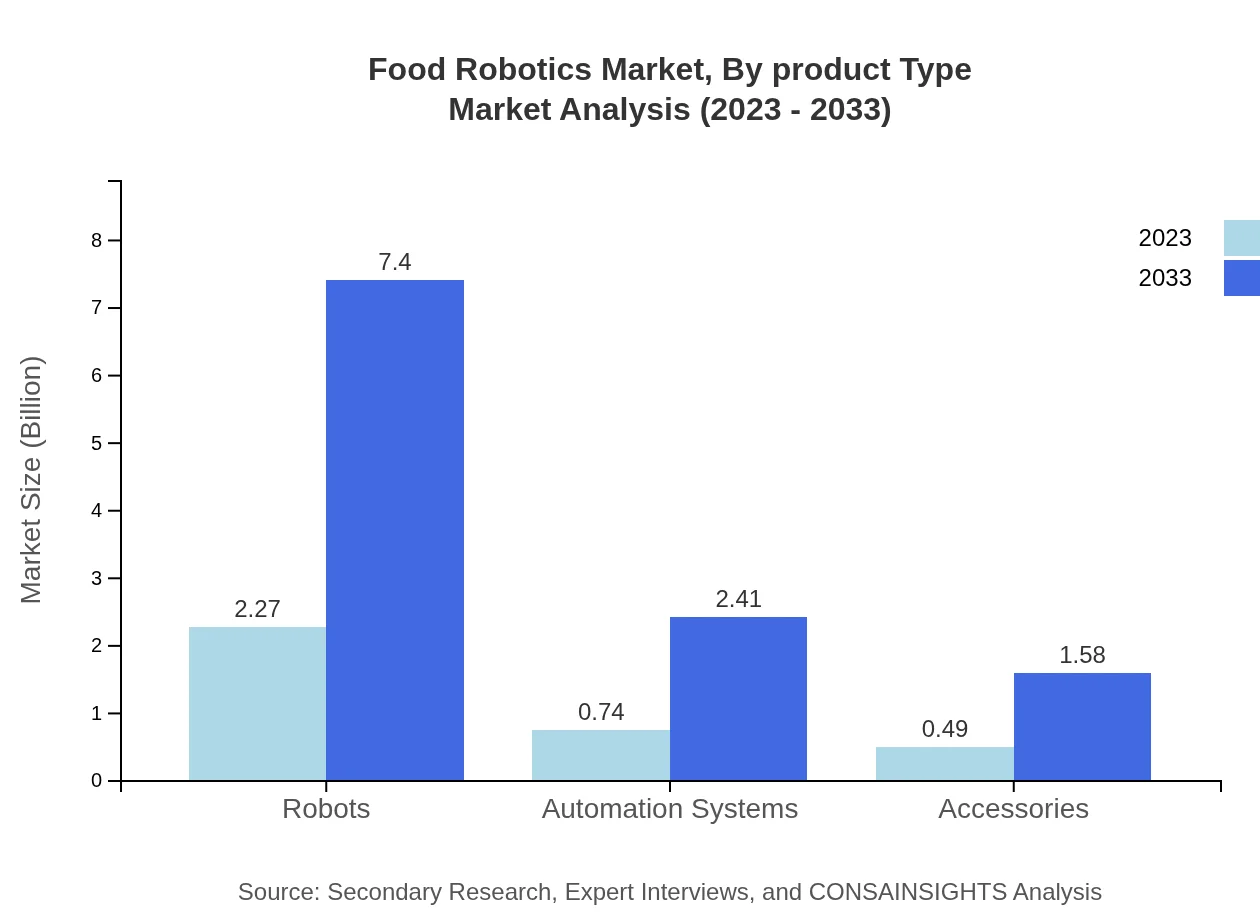

Food Robotics Market Analysis By Product Type

In the Food Robotics market, the product types include robots, automation systems, and accessories. Robots are predicted to dominate the market with a value of $2.27 billion in 2023, growing to $7.40 billion by 2033, making up 64.96% market share. Automation systems, valued at $0.74 billion in 2023, are also expected to show significant growth.

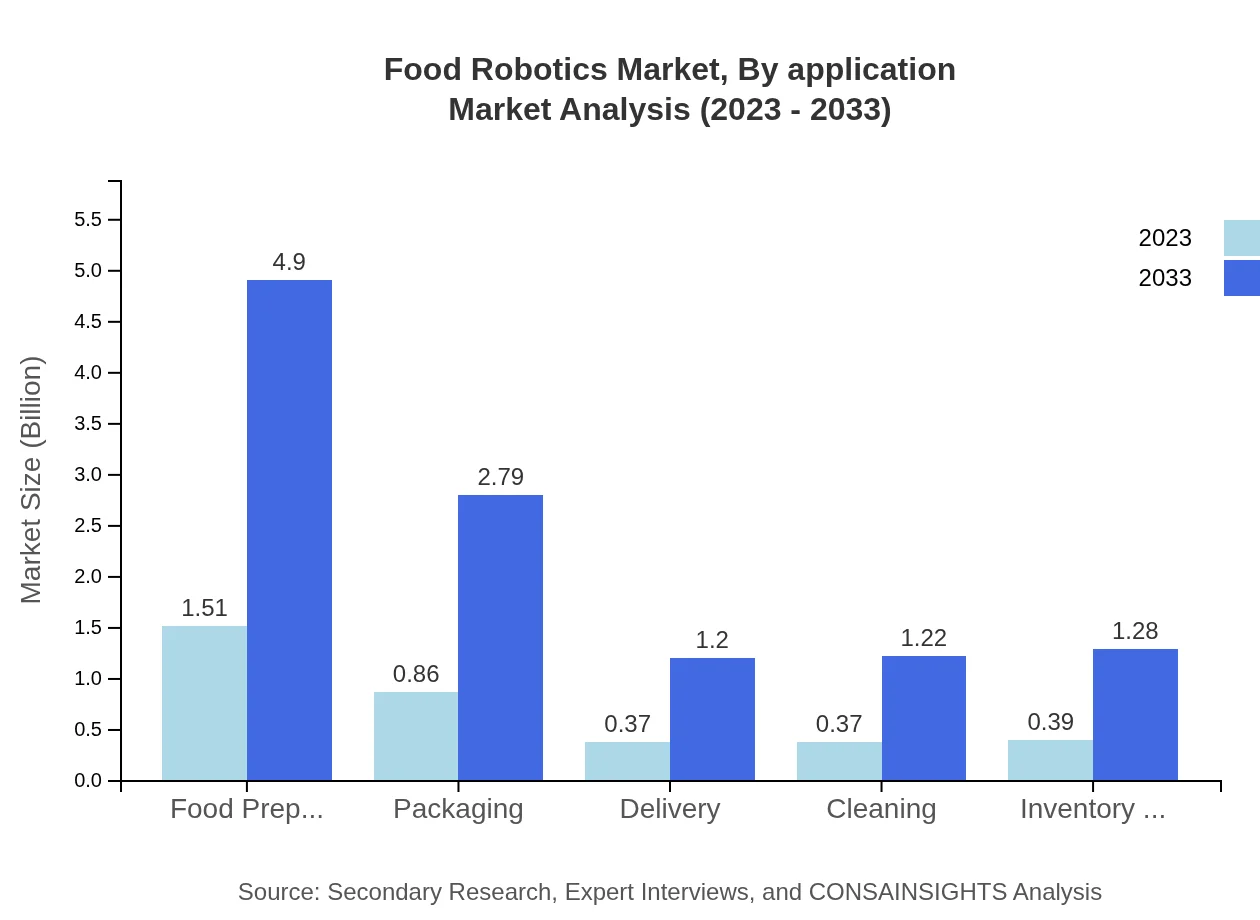

Food Robotics Market Analysis By Application

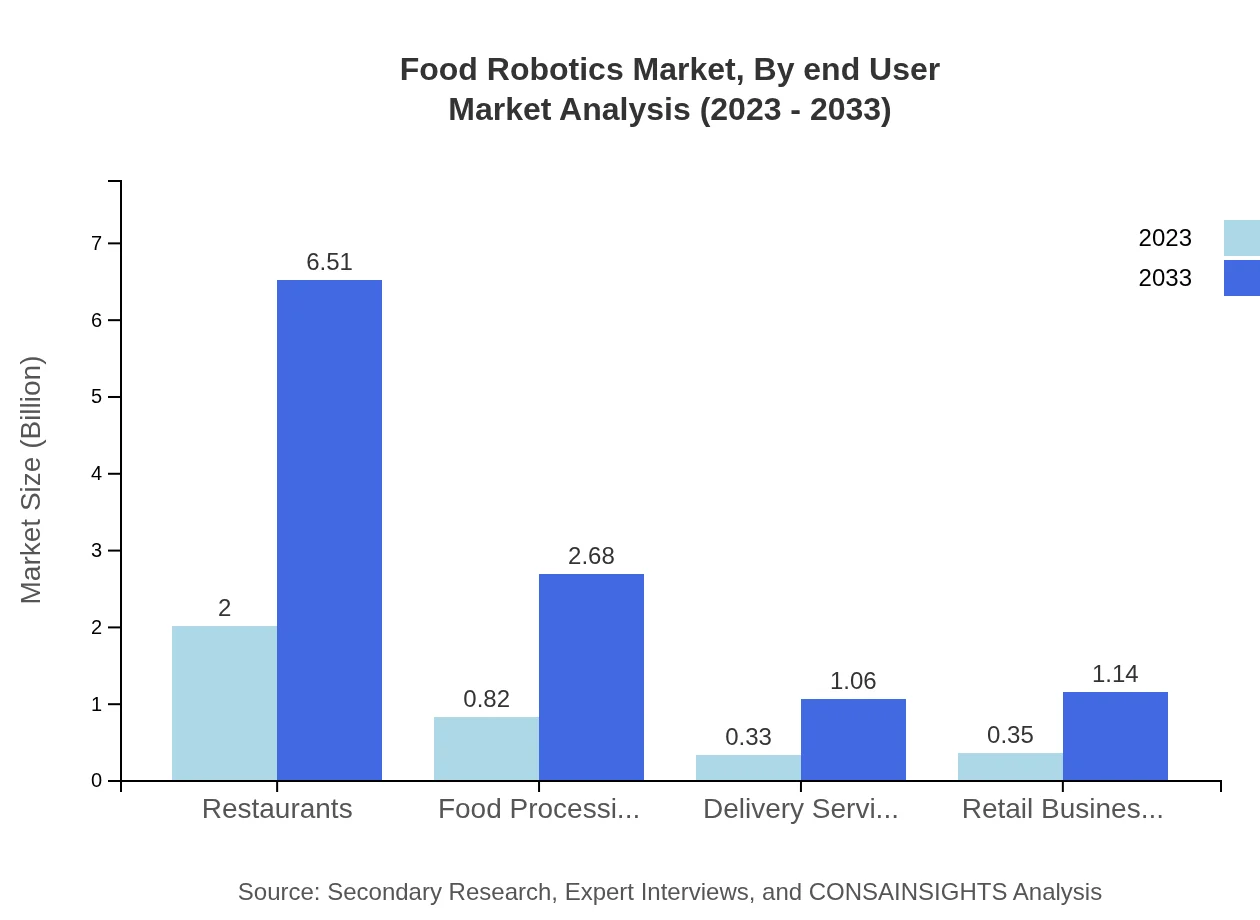

The major applications of Food Robotics include restaurants, food processing plants, and delivery services. Restaurants currently account for the largest share at 57.16%, projected to grow from $2.00 billion in 2023 to $6.51 billion by 2033. Food processing plants are also witnessing substantial growth, expected to rise from $0.82 billion to $2.68 billion in the same period.

Food Robotics Market Analysis By End User

End-users of Food Robotics comprise sectors like restaurants, retail businesses, and food processing plants. The restaurant segment leads with substantial market share, while food processing is witnessing new innovations that could reshape operations leading to better efficiency.

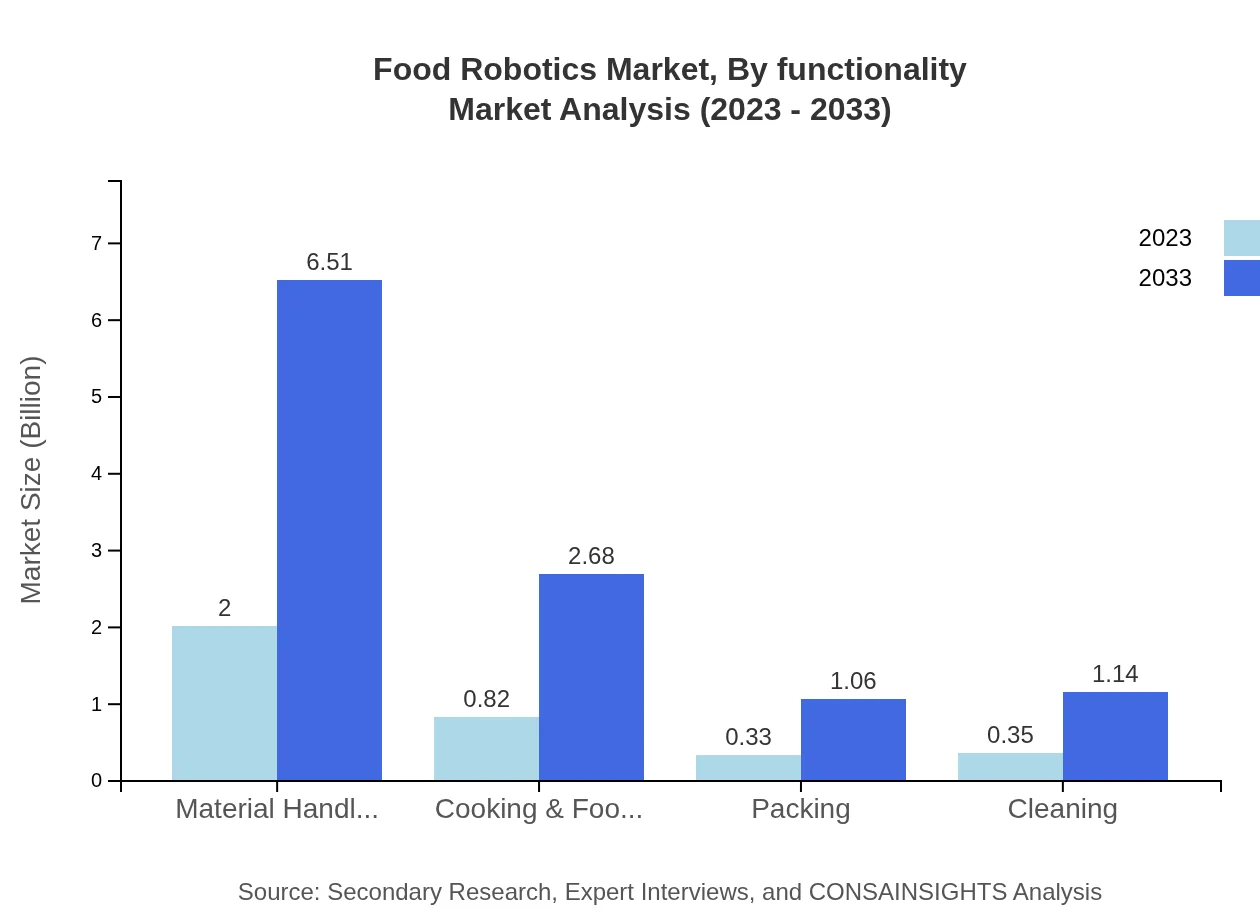

Food Robotics Market Analysis By Functionality

Key functionalities of Food Robotics include cooking and food preparation, packaging, cleaning, and inventory management. Cooking and food preparation robots are particularly popular, growing from $0.82 billion in 2023 to $2.68 billion by 2033.

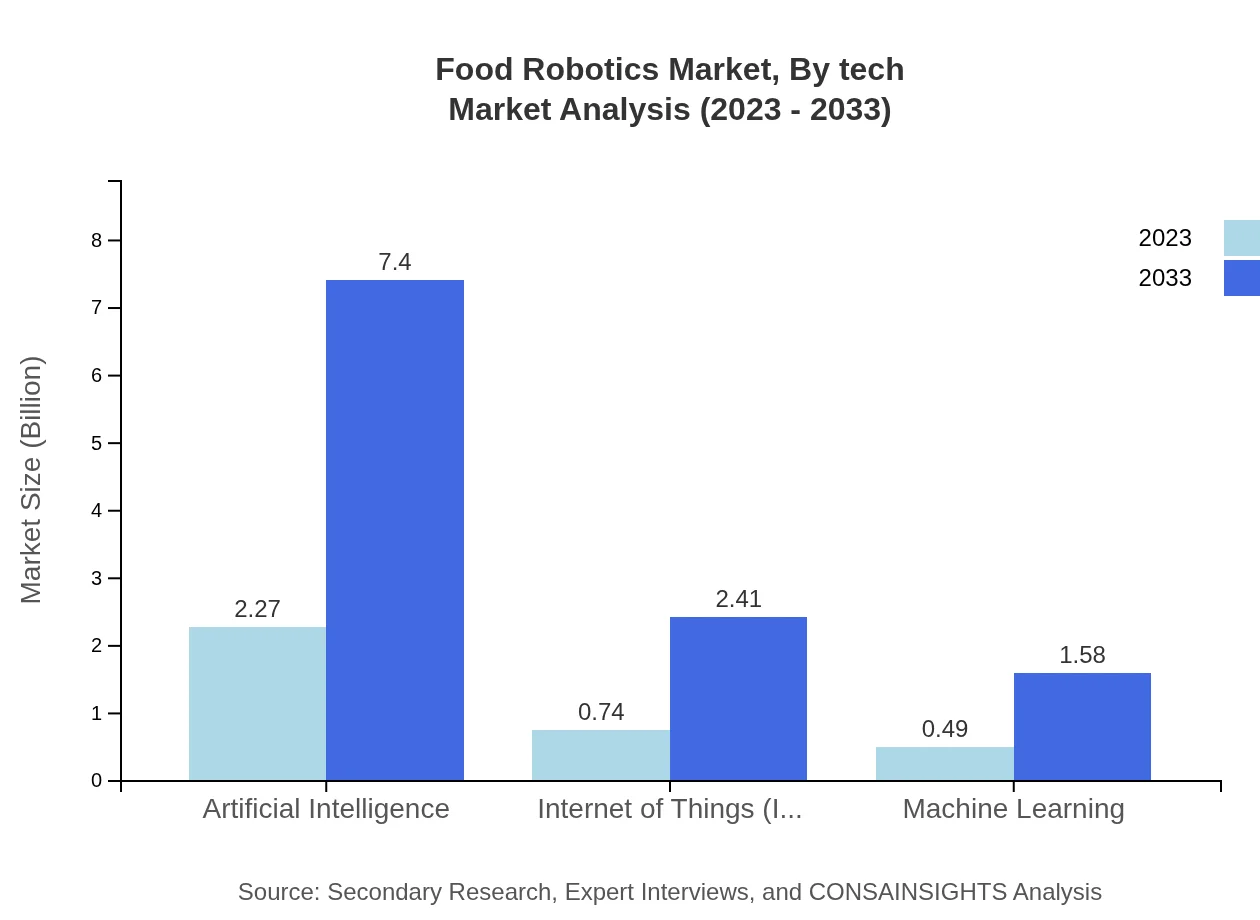

Food Robotics Market Analysis By Tech

Market segmentation by technology covers artificial intelligence (AI), IoT, and machine learning. AI remains the leader, with growth from $2.27 billion in 2023 to $7.40 billion by 2033. Ultimately, these technologies are vital for improving product performance and operational efficiency in the industry.

Food Robotics Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Food Robotics Industry

ABB Robotics:

A leader in industrial automation, ABB Robotics specializes in innovative robotic solutions for food processing and packaging, enhancing efficiency and productivity.KUKA AG:

KUKA AG provides cutting-edge robotics solutions tailored to the food industry, focusing on improving production speed and safety.Fanuc Corporation:

Fanuc is a prominent player in the robotics sector, offering versatile robotic systems that streamline food handling and processing.Yaskawa Electric Corporation:

Yaskawa focuses on advanced robotics technology, especially in food automation, contributing significantly to productivity improvements in food manufacturing.Robot Coupe:

Known for kitchen robots and food processing equipment, Robot Coupe leads in solutions designed to enhance culinary processes in various food services.We're grateful to work with incredible clients.

FAQs

What is the market size of food robotics?

The global food robotics market is valued at approximately $3.5 billion in 2023, with a robust Compound Annual Growth Rate (CAGR) of 12% projected, indicating significant growth potential through 2033.

What are the key market players or companies in the food robotics industry?

Key players in the food robotics industry include major companies that specialize in automation and robotics solutions for food preparation and processing, although specific names are not disclosed in this report.

What are the primary factors driving the growth in the food robotics industry?

The growth in the food robotics industry is driven by increased labor costs, rising demand for automation in food processing, and the need for efficient operations to enhance food safety and quality.

Which region is the fastest Growing in the food robotics market?

The fastest-growing region in the food robotics market is North America, expected to reach approximately $3.86 billion by 2033, followed closely by Europe and Asia Pacific, which also show substantial growth.

Does ConsaInsights provide customized market report data for the food robotics industry?

Yes, ConsaInsights offers tailored market reports to meet specific client needs within the food robotics industry, allowing businesses to gain detailed insights based on unique requirements.

What deliverables can I expect from this food robotics market research project?

Deliverables from the food robotics market research project include comprehensive market analysis reports, segment-wise data, trends, competitive landscape, and regional insights tailored to inform strategic decisions.

What are the market trends of food robotics?

Current trends in the food robotics market include increased integration of Artificial Intelligence, advancements in automation technologies, and a growing focus on flexibility in robotic solutions for various food industry applications.