Mobile Edge Computing Market Report

First published: 18 September 2024 | Last updated: 31 January 2026 | Report Code: mobile-edge-computing

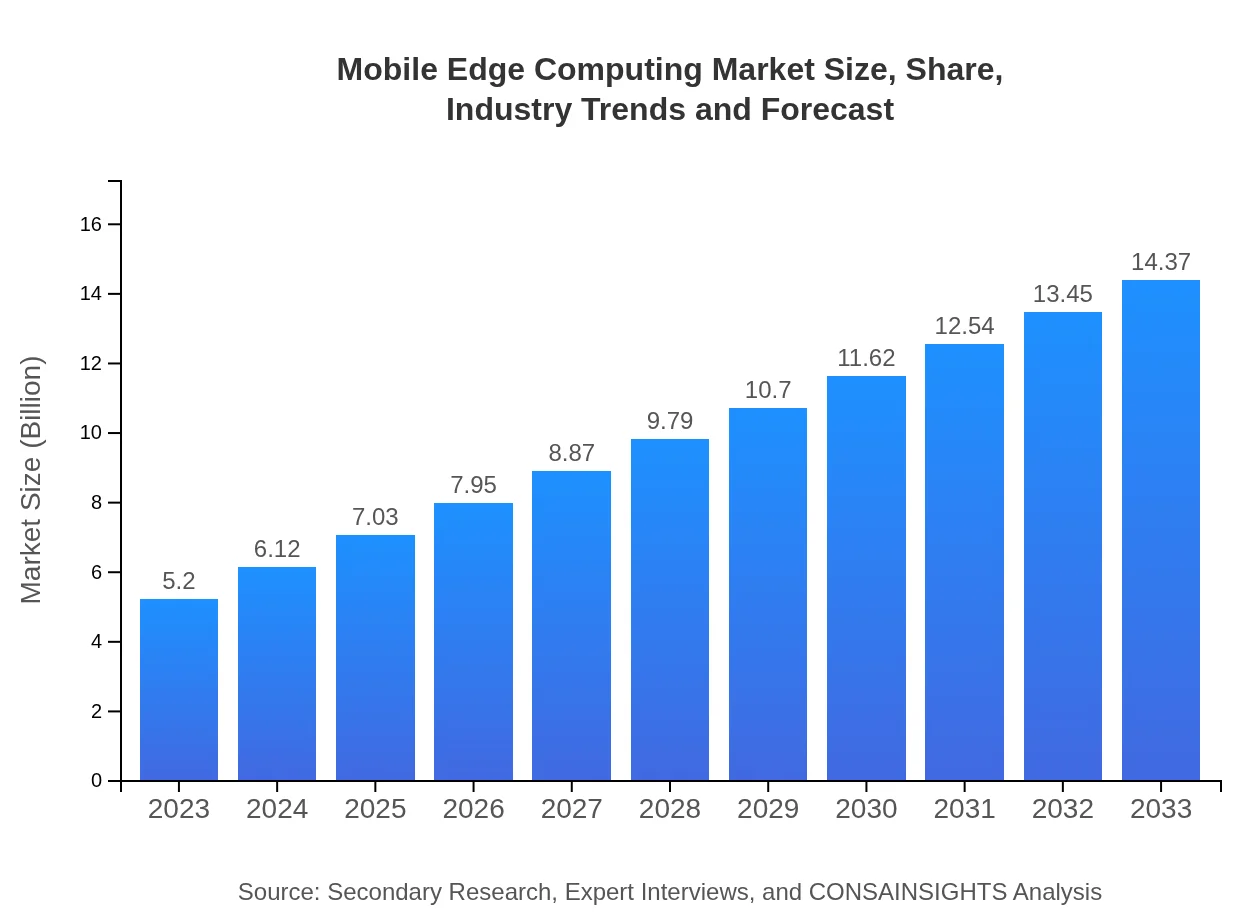

Mobile Edge Computing Market — USD 5.2 billion in 2023, Growing to USD 14.37B by 2033 at 10.3% CAGR

This report provides an in-depth analysis of the Mobile Edge Computing market from 2023 to 2033, covering essential insights, trends, and forecasts that shape the future landscape of this industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.20 Billion |

| CAGR (2023-2033) | 10.3% |

| 2033 Market Size | $14.37 Billion |

| Top Companies | IBM, Intel Corporation, Hewlett Packard Enterprise (HPE), Nokia |

| Published Date | 18 September 2024 |

| Last Modified Date | 31 January 2026 |

Mobile Edge Computing Market Overview

Customize Mobile Edge Computing Market Report market research report

- ✔ Get in-depth analysis of Mobile Edge Computing market size, growth, and forecasts.

- ✔ Understand Mobile Edge Computing's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Mobile Edge Computing

What is the Market Size & CAGR of Mobile Edge Computing market in 2023?

Mobile Edge Computing Industry Analysis

Mobile Edge Computing Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Mobile Edge Computing Market Analysis Report by Region

Europe Mobile Edge Computing Market Report:

Europe is projected to see steady growth from $1.31 billion in 2023 to $3.62 billion by 2033. The emphasis on sustainability initiatives and smart cities is a critical driver for MEC adoption, aligning with Europe’s broader digital agenda.Asia Pacific Mobile Edge Computing Market Report:

The Asia Pacific region is anticipated to experience significant growth, with the market expanding from $1.12 billion in 2023 to $3.10 billion by 2033. Rapid industrialization and urbanization, coupled with government initiatives promoting digital transformation, are fueling adoption of MEC solutions in countries like China and India.North America Mobile Edge Computing Market Report:

North America leads the MEC market, projected to grow from $1.91 billion in 2023 to $5.29 billion by 2033. The presence of major telcos and technology vendors, along with substantial investments in 5G deployments, drives this growth, facilitating the integration of MEC in city planning and critical infrastructure.South America Mobile Edge Computing Market Report:

In South America, the Mobile Edge Computing market is expected to grow from $0.22 billion in 2023 to $0.59 billion by 2033. Limited infrastructure in many areas has led organizations to explore MEC as a means to enhance service delivery and operational efficiency.Middle East & Africa Mobile Edge Computing Market Report:

The Middle East and Africa region will see the market grow from $0.64 billion in 2023 to $1.77 billion by 2033. Investments in digital infrastructure and diversification of economic activities are promoting interest in MEC to leverage data-driven decision-making.Tell us your focus area and get a customized research report.

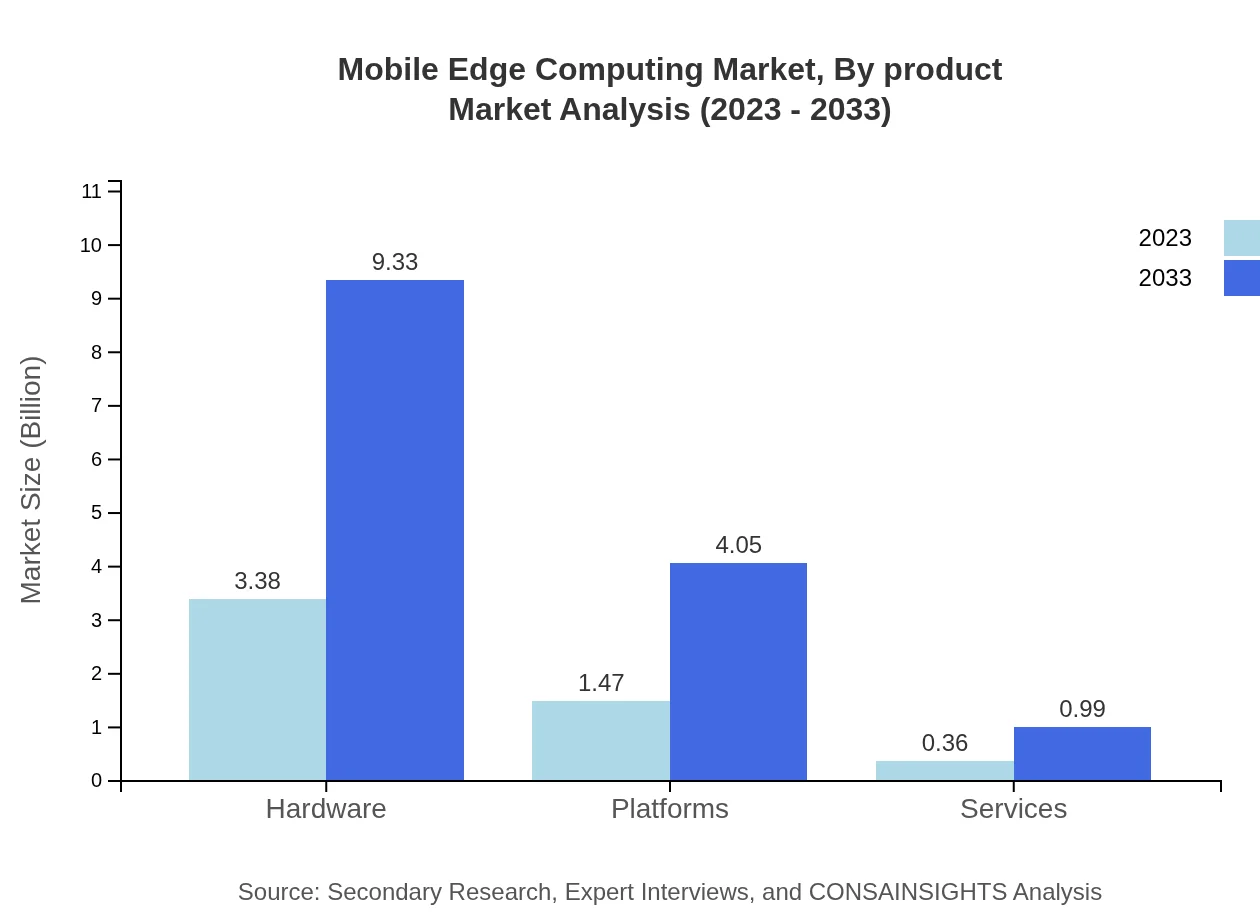

Mobile Edge Computing Market Analysis By Product

The Mobile Edge Computing market can be analyzed by its segments, such as hardware, platforms, and services. The hardware segment is expected to dominate, growing from $3.38 billion in 2023 to $9.33 billion by 2033. Platforms and services are also critical, revealing insights about the industry's extensive capabilities and integration levels.

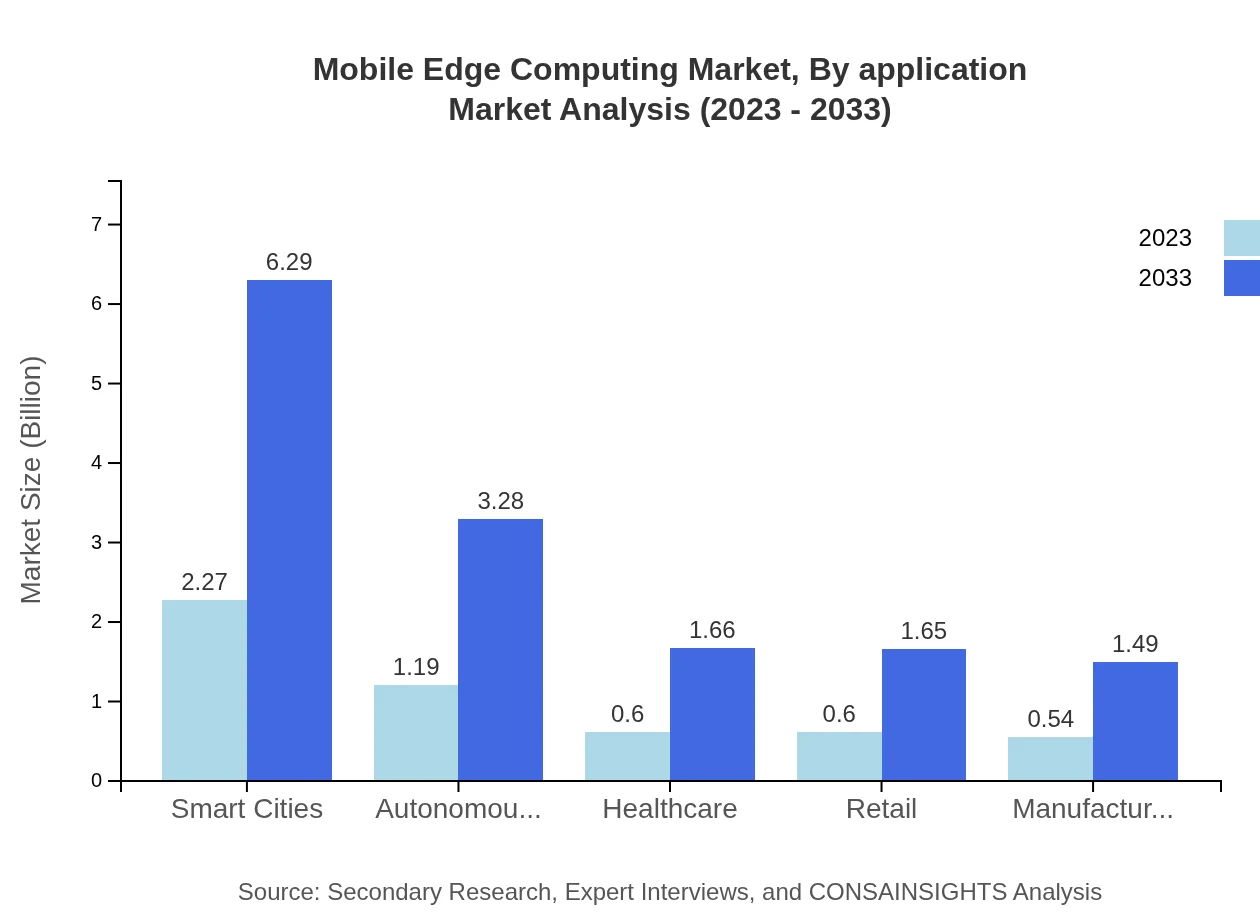

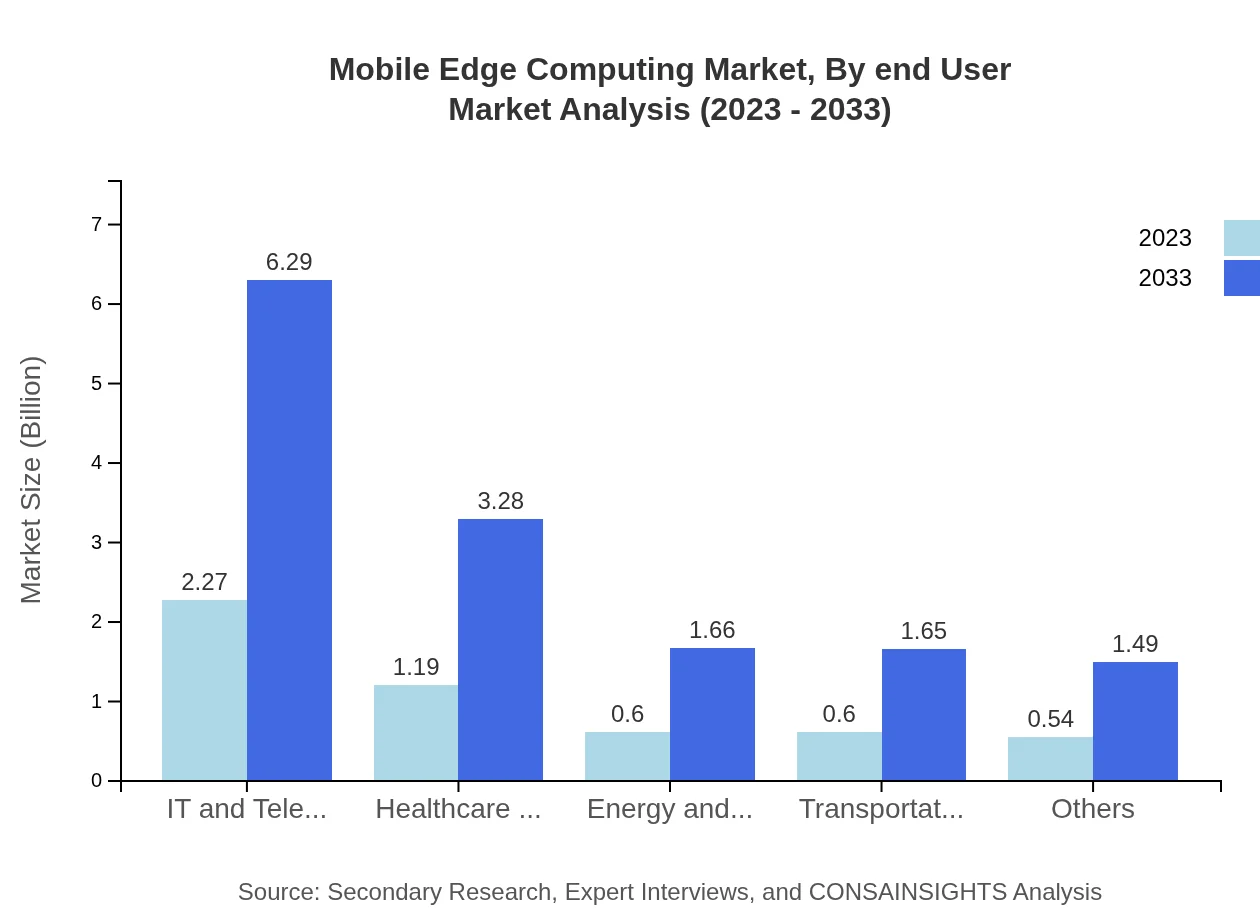

Mobile Edge Computing Market Analysis By Application

In terms of application, sectors like IT and telecom lead with a market share of 43.75% in 2023, expected to expand to 43.75% by 2033. Major applications also include smart cities and healthcare sectors, showcasing MEC’s adaptability.

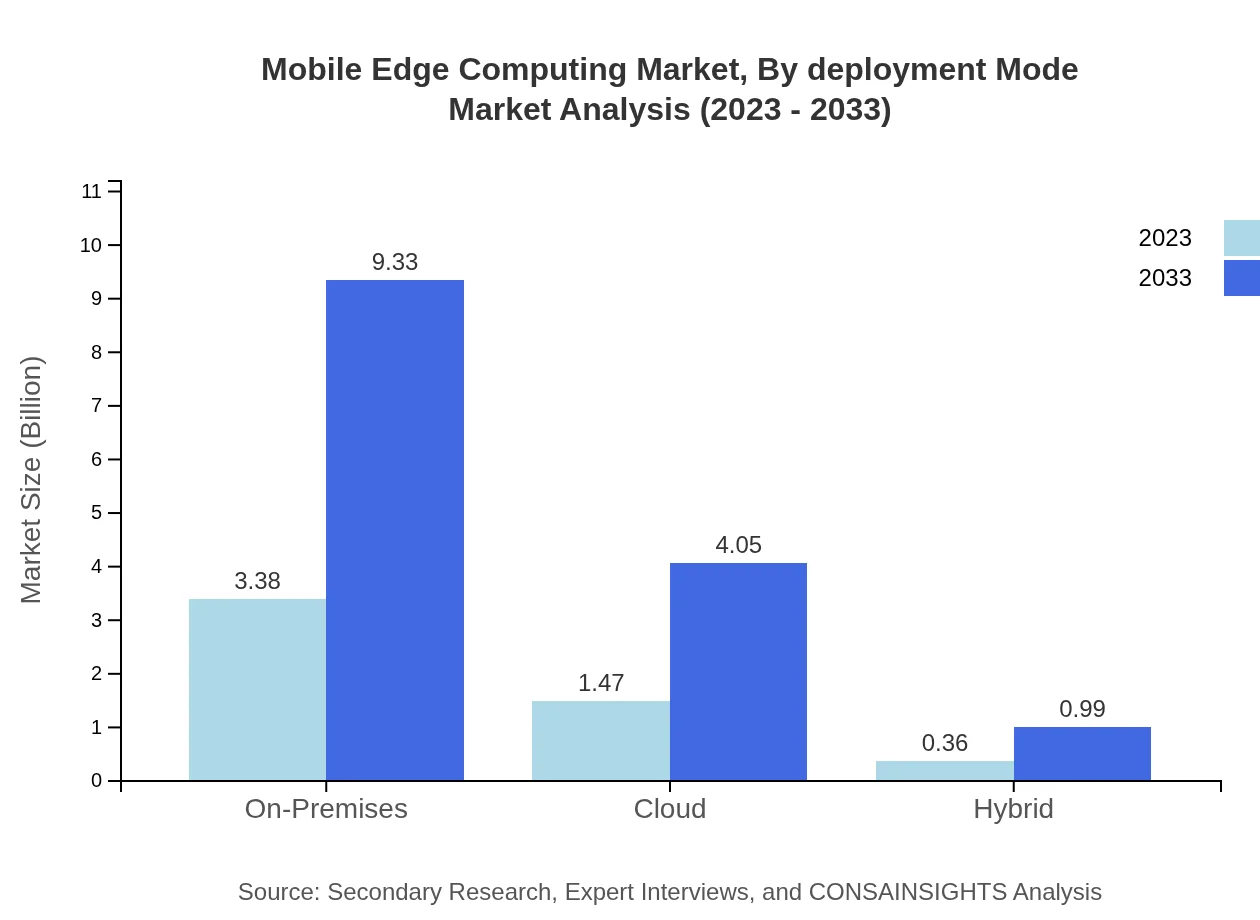

Mobile Edge Computing Market Analysis By Deployment Mode

The deployment mode is categorized into on-premises, cloud, and hybrid solutions. On-premises solutions will stay the predominant choice, maintaining a 64.94% market share through 2033, as many organizations prefer complete control over their data.

Mobile Edge Computing Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Mobile Edge Computing Industry

IBM:

IBM is a leader in cloud and edge computing solutions, offering products that cater to various industries, enhancing data processing capabilities at the edge.Intel Corporation:

Intel provides cutting-edge hardware and platforms for MEC, facilitating rapid data processing and real-time analytics for businesses worldwide.Hewlett Packard Enterprise (HPE):

HPE offers a comprehensive suite of edge computing products, focusing on integrating MEC with cloud solutions for enhanced scalability.Nokia :

Nokia is pioneering MEC solutions within telecommunications, enhancing network performance and reducing latency for mobile operators globally.We're grateful to work with incredible clients.

FAQs

What is the market size of mobile Edge Computing?

The mobile-edge-computing market is valued at approximately $5.2 billion in 2023. It is projected to experience a compound annual growth rate (CAGR) of 10.3%, indicating robust growth through 2033.

What are the key market players or companies in the mobile Edge Computing industry?

Key players in the mobile-edge-computing industry include major technology companies that provide hardware, software, and services tailored to edge computing solutions, focusing on innovations to enhance application performance and low-latency processing.

What are the primary factors driving the growth in the mobile Edge Computing industry?

Growth in mobile-edge-computing is driven by increasing demand for low-latency processing, IoT proliferation, the rise of smart cities, and enhanced application performance. The efficiency and speed of data processing continue to be paramount in various sectors.

Which region is the fastest Growing in mobile Edge Computing?

North America holds a significant market share in mobile-edge-computing, projected to grow from $1.91 billion in 2023 to $5.29 billion by 2033. Europe and Asia-Pacific are also experiencing substantial growth in this region.

Does ConsInsights provide customized market report data for the mobile Edge Computing industry?

Yes, ConsInsights offers customized market report data for the mobile-edge-computing industry, allowing clients to obtain tailored insights and analyses that align with their specific business needs and industry requirements.

What deliverables can I expect from this mobile Edge Computing market research project?

Deliverables from the market research project include detailed market size analysis, growth forecasts, trends, competitive landscape, customer insights, and regional overviews to support strategic decision-making in mobile-edge-computing.

What are the market trends of mobile Edge Computing?

Current trends in mobile-edge-computing include advancements in hardware capabilities, a growing emphasis on security and privacy, expansion of edge computing use in sectors like healthcare and manufacturing, and the adoption of hybrid cloud models.