Reports >

Life Sciences

>

Orthopedic Devices Market Report

Orthopedic Devices Market Report

First published: 08 October 2024 | Last updated: 25 May 2026 | Report Code: orthopedic-devices

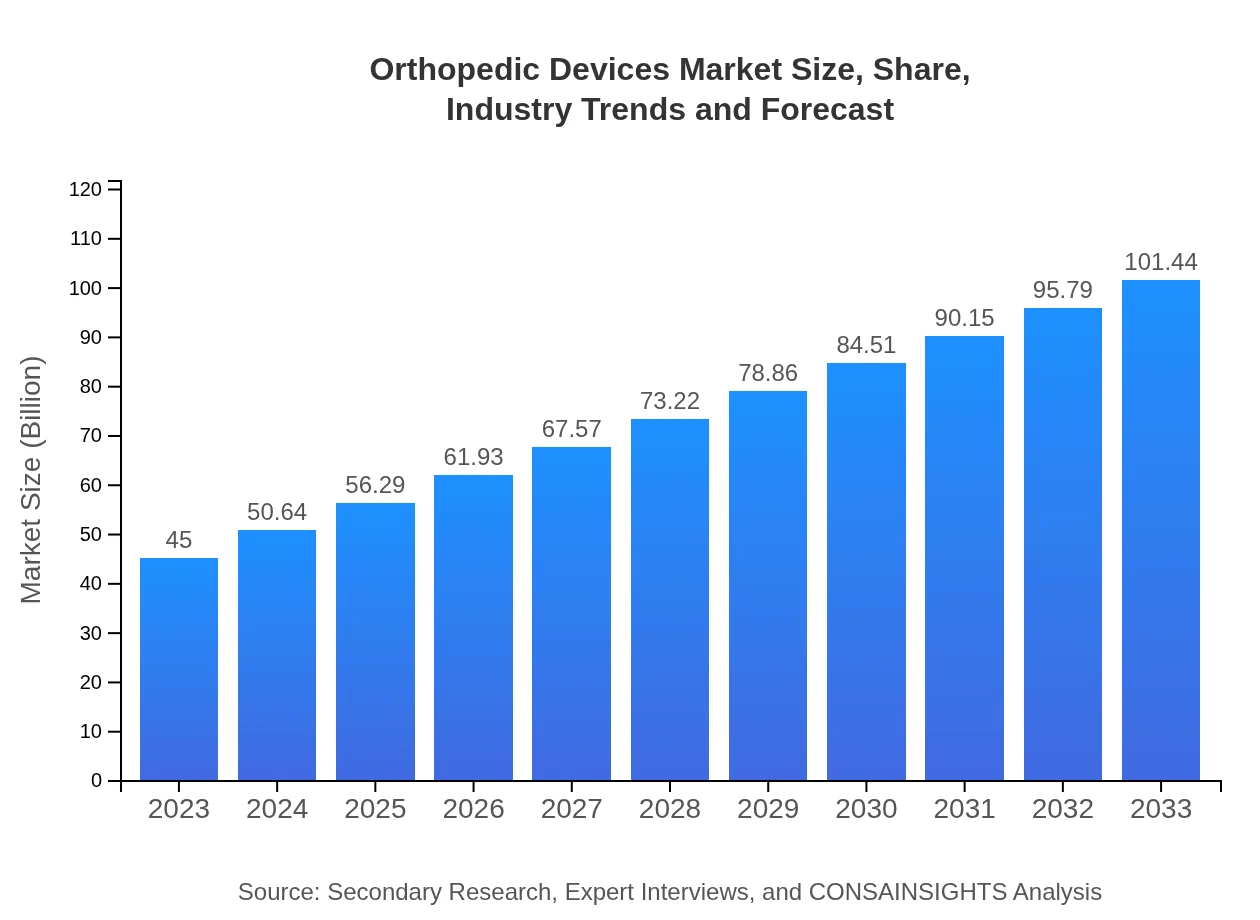

Orthopedic Devices Market — USD $45 Billion in 2023, Growing to USD 101.44null by 2033 at 8.2% CAGR

This report provides a comprehensive analysis of the orthopedic devices market from 2023 to 2033, focusing on trends, market size, segmentation, and regional insights to support strategic decision-making.

Key Takeaways

- Global market expands from $45.00 Billion in 2023 to $101.44 Billion in 2033 at an 8.2% CAGR.

- North America is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- North America leads regionally, rising from $15.7 Billion in 2023 to $35.4 Billion in 2033.

- Europe and Asia Pacific show substantial absolute growth between 2023 and 2033, reflecting rising demand and technological uptake.

- Segment diversity includes implants, surgical instruments, materials like metal and polymer, and distribution via online and offline channels.

- Prominent manufacturers include Stryker Corporation, Zimmer Biomet Holdings, Inc., DePuy Synthes, and Medtronic.

Orthopedic Devices Market Report — Executive Summary

North America remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. The Orthopedic Devices Market Report presents a decade outlook driven by demographic shifts, rising incidence of musculoskeletal conditions, and technological advancement in device design and surgical techniques. The market is sized at $45.00 Billion in 2023 and is expected to reach $101.44 Billion by 2033 at a CAGR of 8.2% for 2023 to 2033. Product innovation, minimally invasive procedures, and adoption of advanced materials are key trends shaping demand. Hospitals, ambulatory surgical centers, rehabilitation centers, and orthopedic clinics represent primary end users, while implants, surgical instruments and accessories constitute major device categories. Regional performance varies: North America is the largest regional market. Market participants such as Stryker Corporation, Zimmer Biomet Holdings, Inc., DePuy Synthes and Medtronic are active in product development and competitive strategies. The report combines primary interviews and secondary sources to deliver actionable insight for manufacturers, investors and healthcare providers.

Key Growth Drivers

- Aging populations increase demand for joint replacement and spine procedures, expanding device utilization.

- Technological advancements in implants and surgical tools enhance outcomes and broaden indications for orthopedic interventions.

- Growth in ambulatory surgical centers and minimally invasive techniques shifts volumes toward outpatient procedures.

- Wider adoption of advanced materials such as metals, polymers and ceramics improves device performance and longevity.

- Expansion of digital and online distribution channels increases accessibility to orthopedic products for providers and patients.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $45.00 Billion |

| CAGR (2023-2033) | 8.2% |

| 2033 Market Size | $101.44 Billion |

| Top Companies | Stryker Corporation, Zimmer Biomet Holdings, Inc., DePuy Synthes, Medtronic |

| Published Date | 08 October 2024 |

| Last Modified Date | 25 May 2026 |

Orthopedic Devices Market Overview

Customize Orthopedic Devices Market Report market research report

- ✔ Get in-depth analysis of Orthopedic Devices market size, growth, and forecasts.

- ✔ Understand Orthopedic Devices's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Orthopedic Devices

What is the Market Size & CAGR of Orthopedic Devices Market Report market in 2023?

Orthopedic Devices Industry Analysis

Orthopedic Devices Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Orthopedic Devices Market Report Market Analysis Report by Region

Europe Orthopedic Devices Market Report:

Europe grows from $12.63 Billion in 2023 to $28.47 Billion in 2033. Regional expansion is driven by demand for joint replacement and spine solutions, investment in minimally invasive procedures, and steady adoption of advanced device materials.Asia Pacific Orthopedic Devices Market Report:

Asia Pacific grows from $9.89 Billion in 2023 to $22.3 Billion in 2033. Growth in the region is supported by expanding healthcare access, rising surgical volumes, aging demographics and heightened uptake of modern orthopedic implants and instruments.North America Orthopedic Devices Market Report:

North America is largest regional market, rising from $15.7 Billion in 2023 to $35.4 Billion in 2033. The region’s scale reflects established procedure volumes, rapid uptake of advanced implants and surgical technologies, and strong hospital and outpatient infrastructure.South America Orthopedic Devices Market Report:

Latin America grows from $4.31 Billion in 2023 to $9.72 Billion in 2033. Market gains are underpinned by improving healthcare infrastructure, increased elective procedures and growing availability of orthopedic products across public and private providers.Middle East & Africa Orthopedic Devices Market Report:

Middle East and Africa grows from $2.46 Billion in 2023 to $5.55 Billion in 2033. Drivers include gradual infrastructure development, increased focus on trauma care and wider adoption of orthopedic solutions in urban healthcare centers.Tell us your focus area and get a customized research report.

Research Methodology

Orthopedic Devices Market Analysis By Device Type

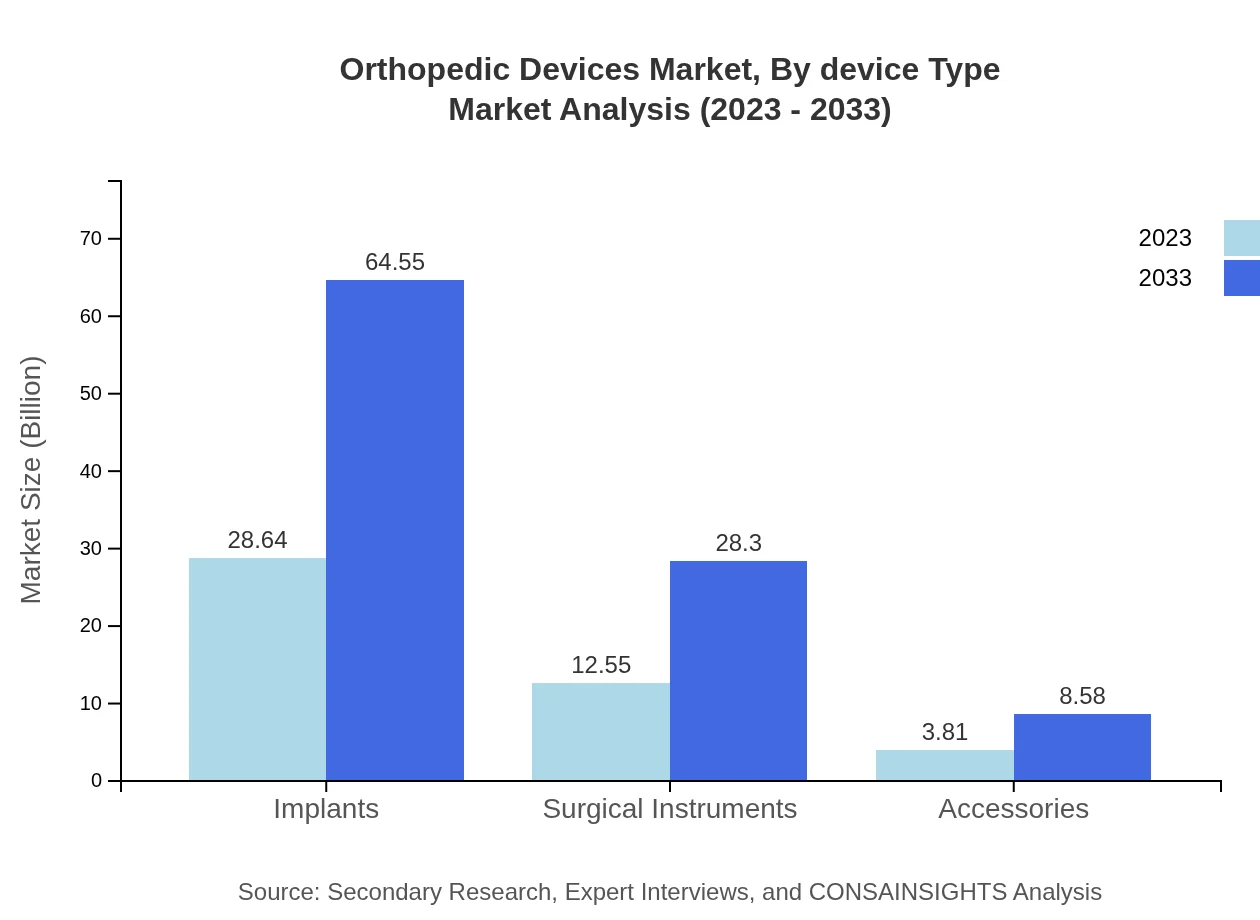

The orthopedic devices market is primarily segmented by product type, including joint replacement devices, trauma devices, spinal products, and surgical instruments. Joint replacement devices hold a dominant share, accounting for 50.7% of the market, with a forecasted market size of $51.43 billion by 2033. Trauma devices and spinal products are also significant, reflecting a growing clinical focus on repair and reconstruction technologies.

Orthopedic Devices Market Analysis By Application

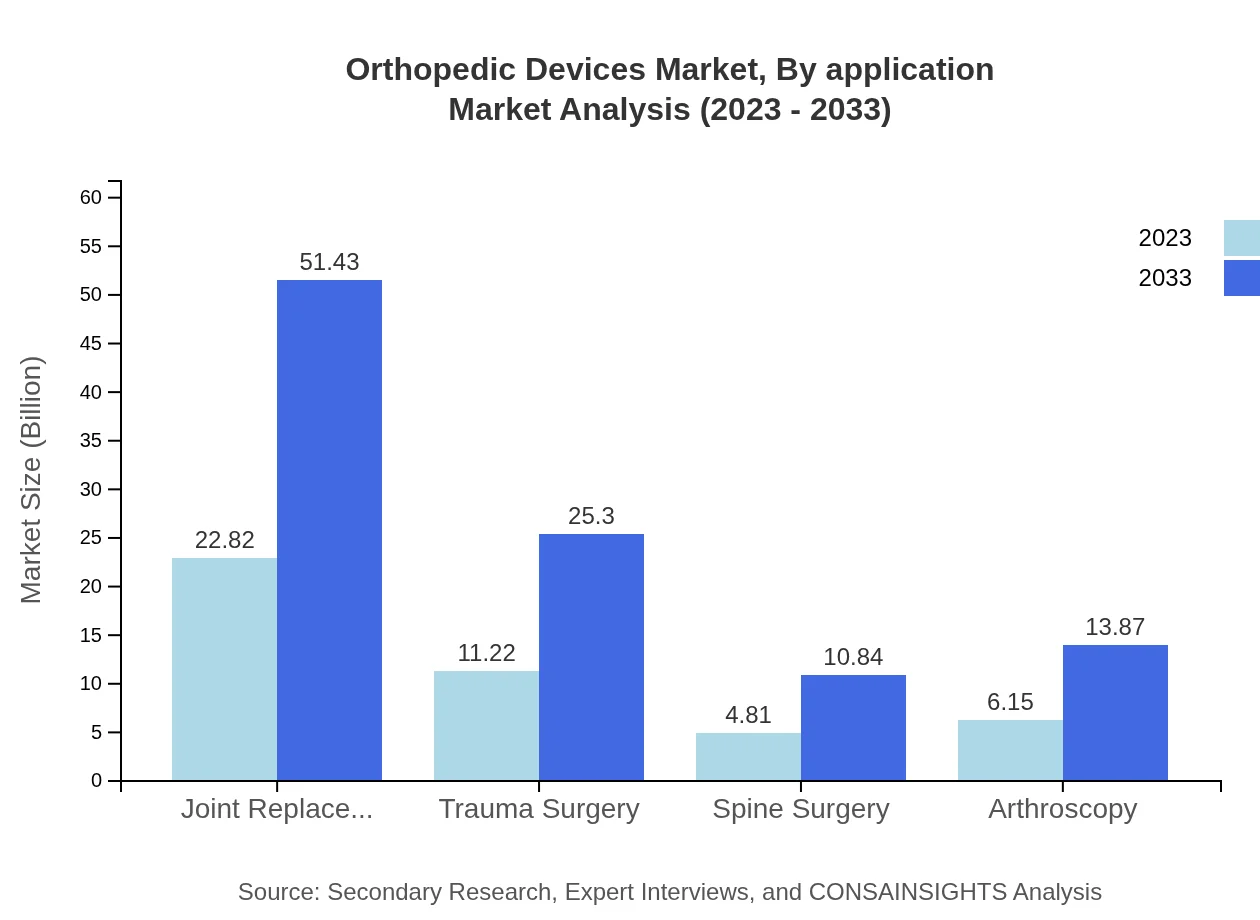

The application segment encompasses joint replacement, trauma surgery, spine surgery, and arthroscopy. Joint replacement, including hip and knee implants, is a key component, expected to grow significantly due to the aging population. Trauma surgery accounts for a substantial percentage of procedures alongside increasing sports-related injuries, contributing to overall market growth.

Orthopedic Devices Market Analysis By End User

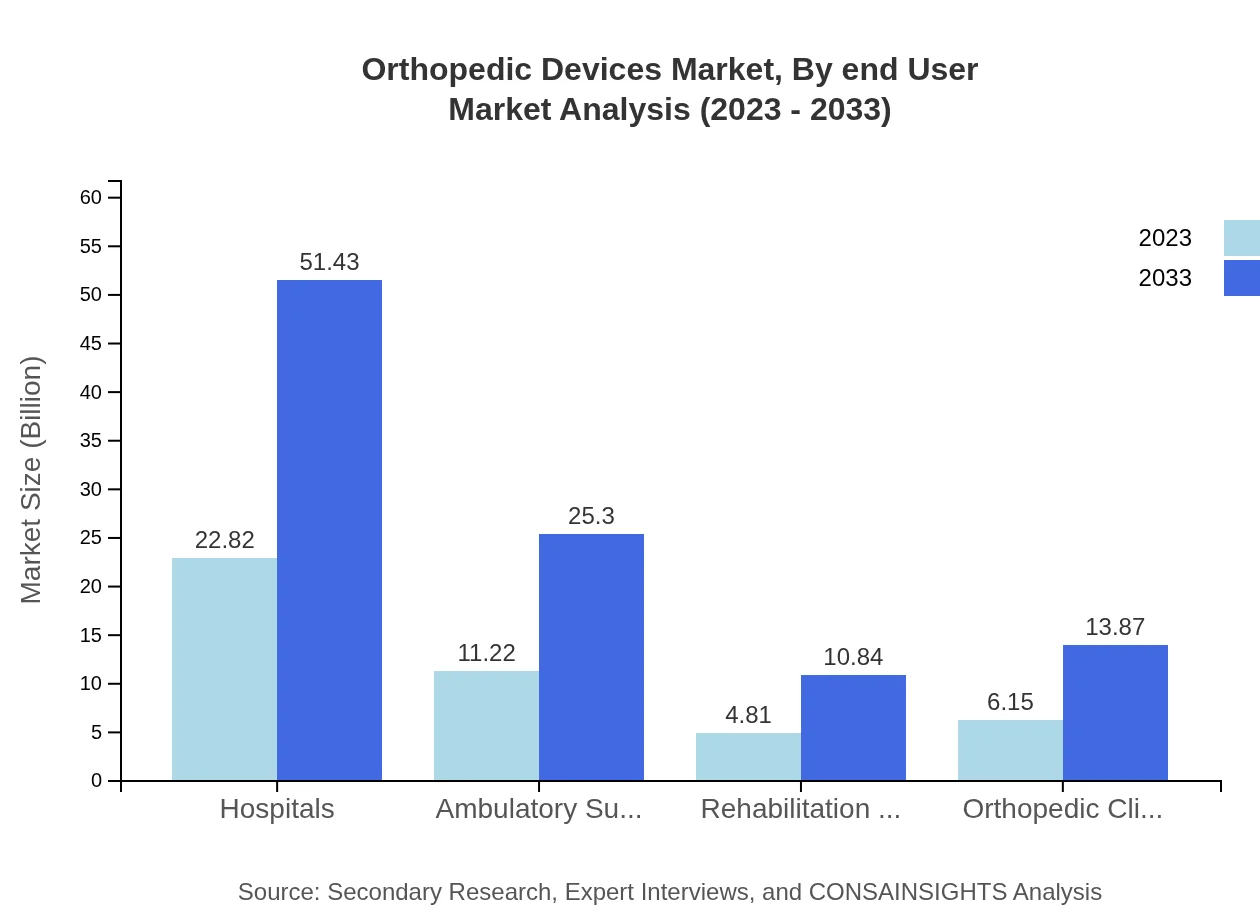

Hospitals represent the largest end-user segment, making up 50.7% of the market share in 2023, and anticipated to grow substantially over the forecast period. Ambulatory Surgical Centers and orthopedic clinics are also notable segments, reflecting a shift toward outpatient surgeries and increased accessibility for patients.

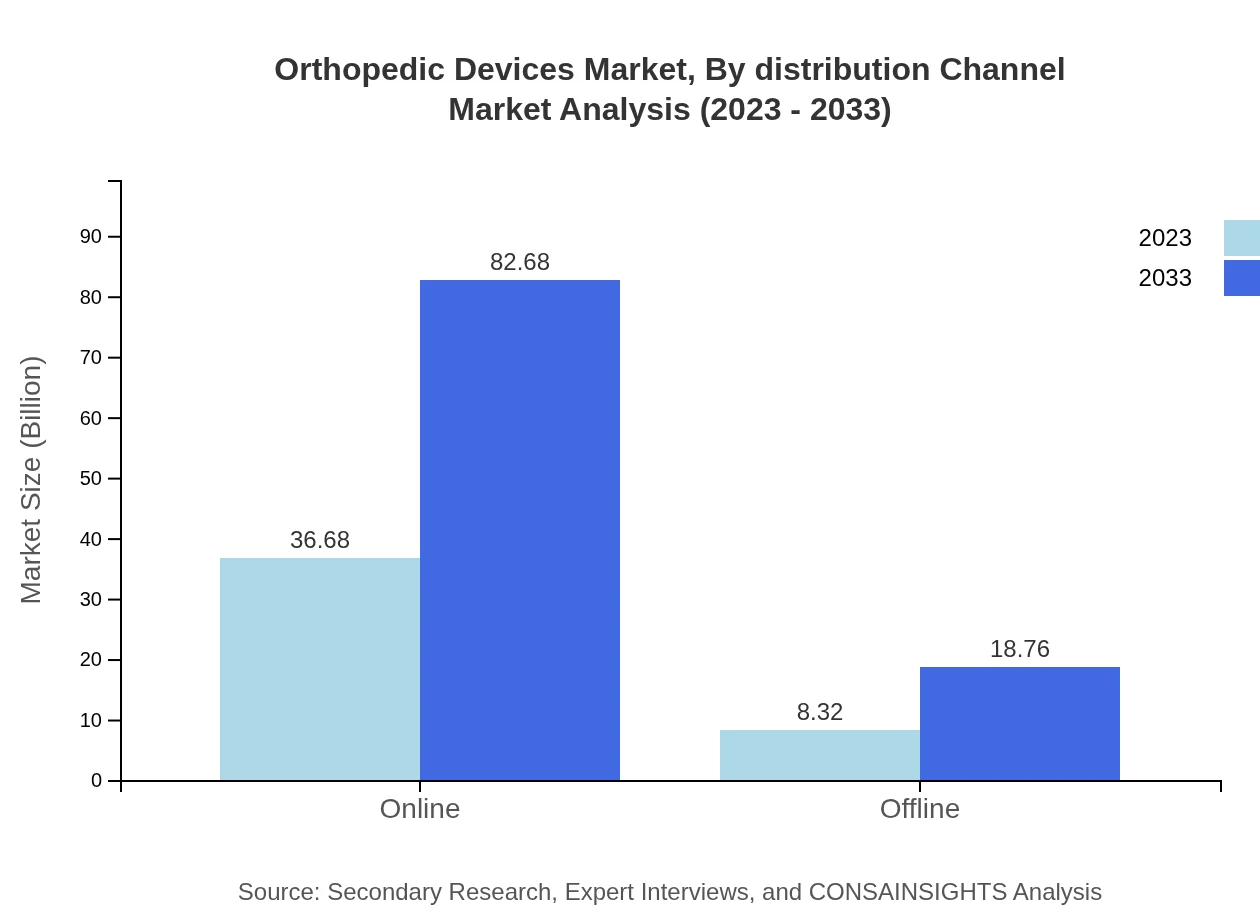

Orthopedic Devices Market Analysis By Distribution Channel

Distribution channels are segmented into online and offline provisions. Online channels are rapidly gaining traction, representing 81.51% of the market share in 2023, with expected growth driven by increased consumer access to information and services. Offline channels remain vital, particularly in established healthcare settings.

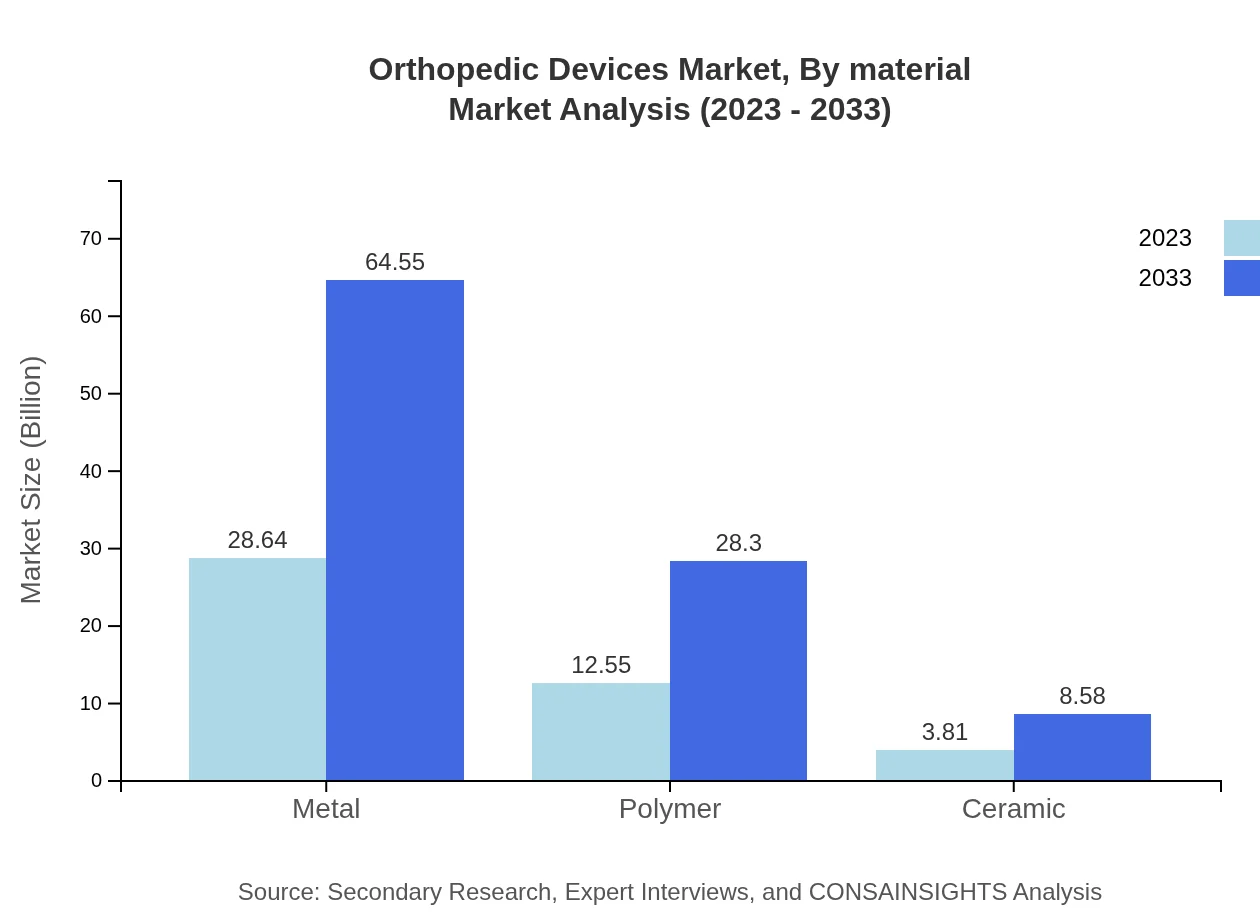

Orthopedic Devices Market Analysis By Material

The material segment comprises metal, polymer, and ceramic products. Metal remains the leading material used in orthopedic devices, representing 63.64% of the market in 2023. Polymers are increasingly utilized for their lightweight and biocompatible properties, driving innovations in newer orthopedic device designs.

Orthopedic Devices Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Orthopedic Devices Industry

Stryker Corporation:

Stryker is a leading medical technology company specializing in orthopedic devices, including joint replacement products and surgical equipment. Their innovative approach and advanced technologies have set benchmarks in orthopedic surgeries.Zimmer Biomet Holdings, Inc.:

Zimmer Biomet focuses on orthopedic and musculoskeletal health, offering a comprehensive portfolio of products, including implants and surgical tools. Their commitment to research and patient-focused solutions drives significant growth in the orthopedic market.DePuy Synthes:

As part of Johnson & Johnson, DePuy Synthes is at the forefront of orthopedic innovation, providing comprehensive solutions for joint reconstruction, trauma, and spinal surgery, and enhancing surgical outcomes through state-of-the-art technology.Medtronic :

Medtronic is known for its leadership in spinal surgery products and innovative therapies aimed at treating musculoskeletal disorders, providing patients with safer and more effective recovery solutions.We're grateful to work with incredible clients.

FAQs

What is the market size of the Orthopedic Devices Market Report in 2023?

The market size for 2023 is $45.00 Billion according to the report, reflecting baseline global demand across implants, instruments and related orthopedic products.

How big will the orthopedic devices market be by 2033?

By 2033 the market is projected to reach $101.44 Billion, reflecting expansion driven by demographic trends, technological progress, and increased procedural volumes.

What is CAGR for the forecast period 2023 to 2033?

The compound annual growth rate for 2023 to 2033 is 8.2%, representing the annualized growth from $45.00 Billion to $101.44 Billion over the period.

Is there a single fastest Growing region in the Orthopedic Devices Market Report market?

No single fastest-growing region is stated for the Orthopedic Devices Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Which companies are named as top participants?

Top companies listed include Stryker Corporation, Zimmer Biomet Holdings, Inc., DePuy Synthes and Medtronic, noted for product development and market presence.

Who are the primary end users highlighted in the report?

Primary end users include hospitals, ambulatory surgical centers, rehabilitation centers and orthopedic clinics, which together account for core procedural demand.

What are common device types covered?

Device categories covered are implants, surgical instruments and accessories, reflecting the range of products used in orthopedic diagnosis, treatment and rehabilitation.

How was the research conducted for this report?

Research included primary interviews with industry experts and secondary review of company reports and publications, supported by data triangulation and internal validation.