Reports >

Aerospace And Defense

>

Satcom Equipment Market Report

Satcom Equipment Market Report

First published: 12 October 2024 | Last updated: 03 February 2026 | Report Code: satcom-equipment

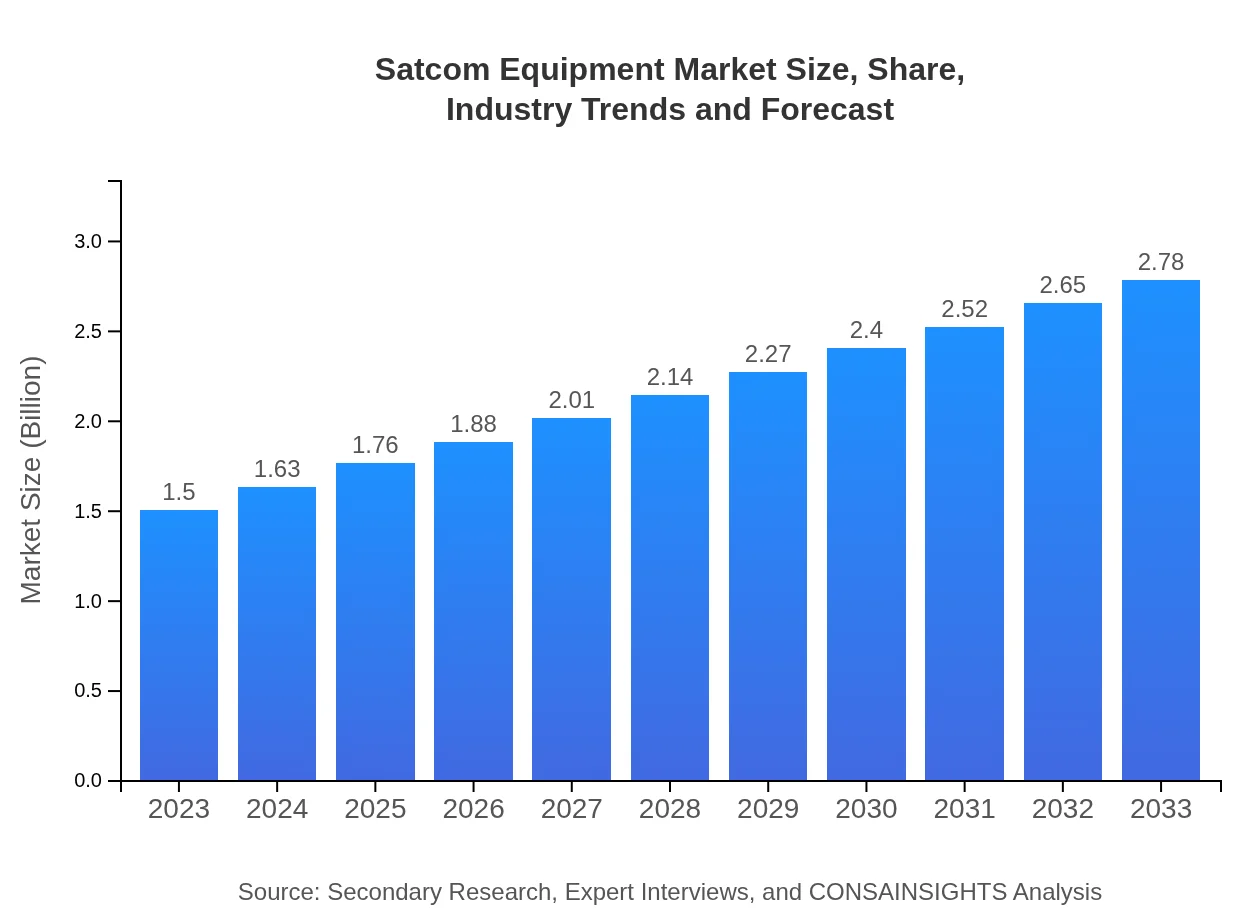

Satcom Equipment Market — USD $1.5 Billion in 2023, Growing to USD 2.78B by 2033 at 6.2% CAGR

This report provides a comprehensive analysis of the Satcom Equipment market, including market trends, forecasts from 2023 to 2033, and insights into segment performance and regional dynamics.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $1.50 Billion |

| CAGR (2023-2033) | 6.2% |

| 2033 Market Size | $2.78 Billion |

| Top Companies | Hughes Network Systems, Thales Group, SES S.A. |

| Published Date | 12 October 2024 |

| Last Modified Date | 03 February 2026 |

Satcom Equipment Market Overview

Customize Satcom Equipment Market Report market research report

- ✔ Get in-depth analysis of Satcom Equipment market size, growth, and forecasts.

- ✔ Understand Satcom Equipment's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Satcom Equipment

What is the Market Size & CAGR of Satcom Equipment market in 2023?

Satcom Equipment Industry Analysis

Satcom Equipment Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Satcom Equipment Market Analysis Report by Region

Europe Satcom Equipment Market Report:

For Europe, the market is anticipated to advance from $0.37 billion in 2023 to $0.68 billion in 2033. The European market is bolstered by the increasing demand for secure satellite communications and collaborations among countries for enhanced connectivity solutions.Asia Pacific Satcom Equipment Market Report:

The Asia Pacific region sees substantial growth in the Satcom Equipment market, expected to rise from $0.30 billion in 2023 to $0.56 billion by 2033. This is driven by extensive investments in telecommunications infrastructure and government initiatives to enhance connectivity in rural areas. The region is becoming a hotspot for satellite launches and technology innovations.North America Satcom Equipment Market Report:

North America illustrates a dominating market presence with values expected to increase from $0.49 billion in 2023 to $0.90 billion by 2033. Factors accounting for this growth include high military expenditure, advancements in satellite technology, and strong demand for broadband services, enhancing user connectivity.South America Satcom Equipment Market Report:

In South America, the market is projected to expand from $0.14 billion in 2023 to $0.26 billion by 2033. The focus on improving telecommunication networks and broadcasting services in remote regions fosters a positive growth environment for satellite technology.Middle East & Africa Satcom Equipment Market Report:

The Middle East and Africa region is set to witness growth from $0.20 billion in 2023 to $0.38 billion by 2033, backed by rising investments in satellite infrastructures and initiatives to bridge digital divides in remote areas.Tell us your focus area and get a customized research report.

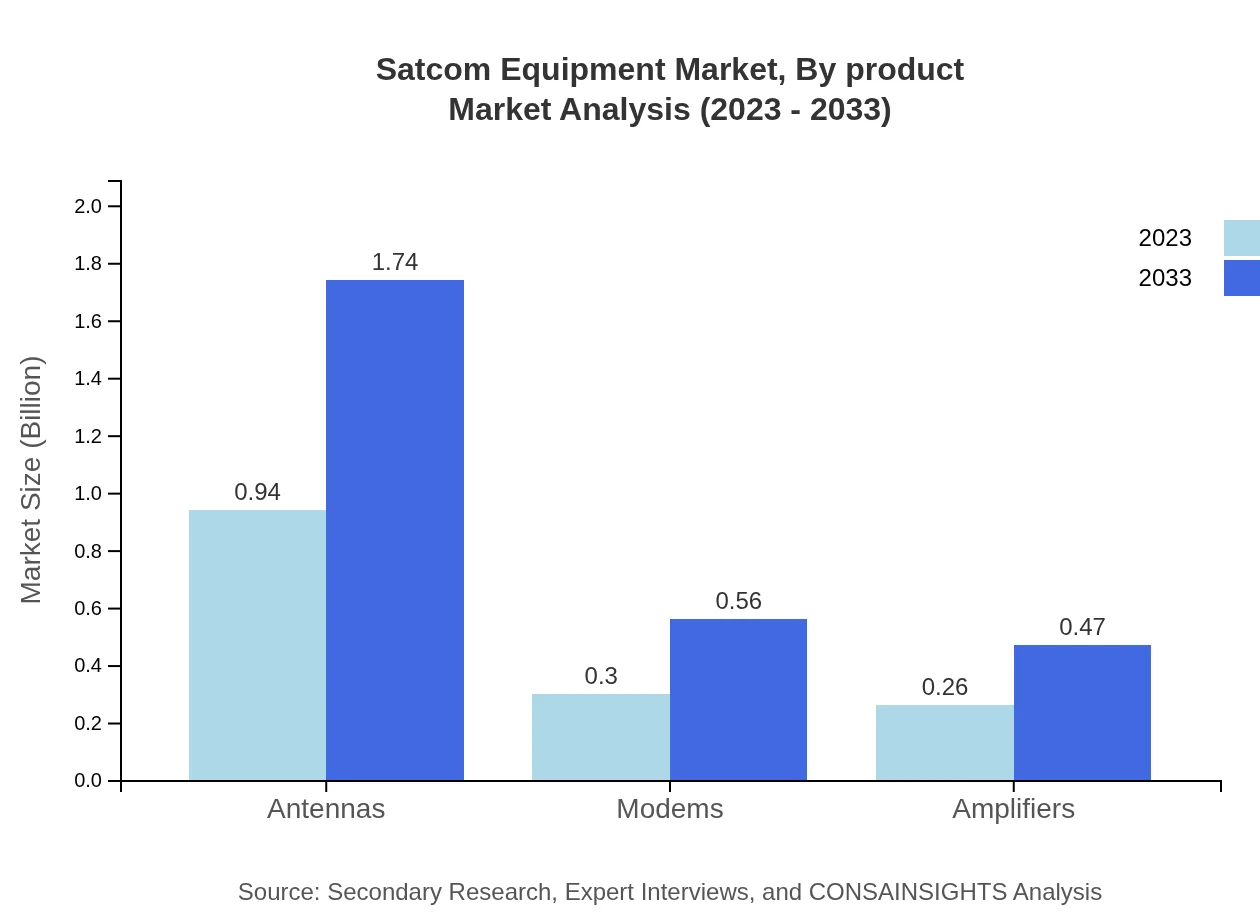

Satcom Equipment Market Analysis By Product

The Antennas segment continues to dominate the Satcom Equipment market, anticipated to grow from $0.94 billion in 2023 to $1.74 billion by 2033, holding a market share of 62.75%. Followed by Modems, expanding from $0.30 billion to $0.56 billion, accounting for a share of 20.18%. Amplifiers also show growth from $0.26 billion to $0.47 billion with a 17.07% market share. Each segment plays a critical role in ensuring seamless communication and enhancing connectivity across various applications.

Satcom Equipment Market Analysis By Application

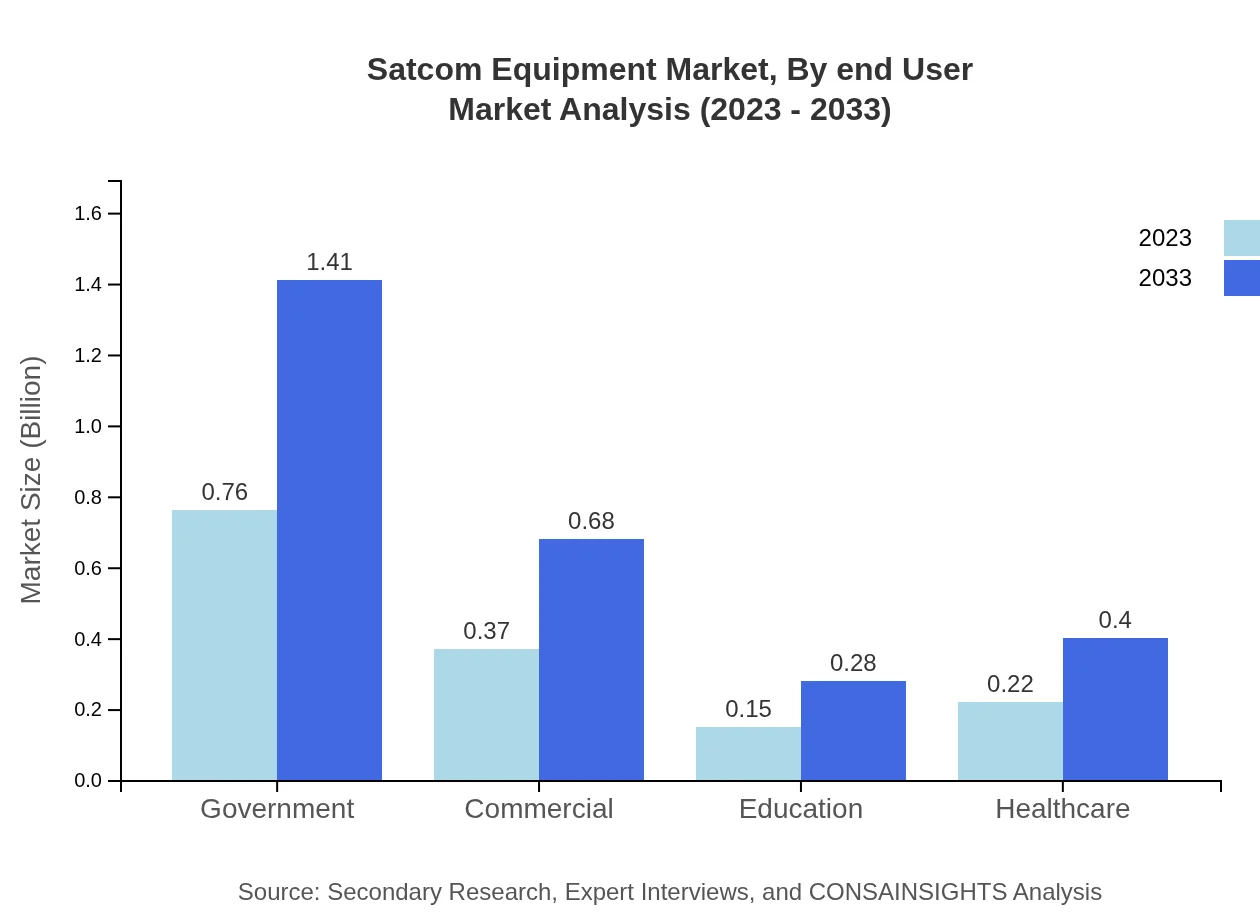

In the Satcom Equipment market, the Government sector leads with a market size of $0.76 billion in 2023 to reach $1.41 billion by 2033, representing a significant 50.89% market share. This is followed by Commercial applications expected to grow from $0.37 billion to $0.68 billion, accounting for 24.47%. The Education and Healthcare sectors are also prominent, with increasing demands for satellite communication technologies in remote learning and telemedicine respectively.

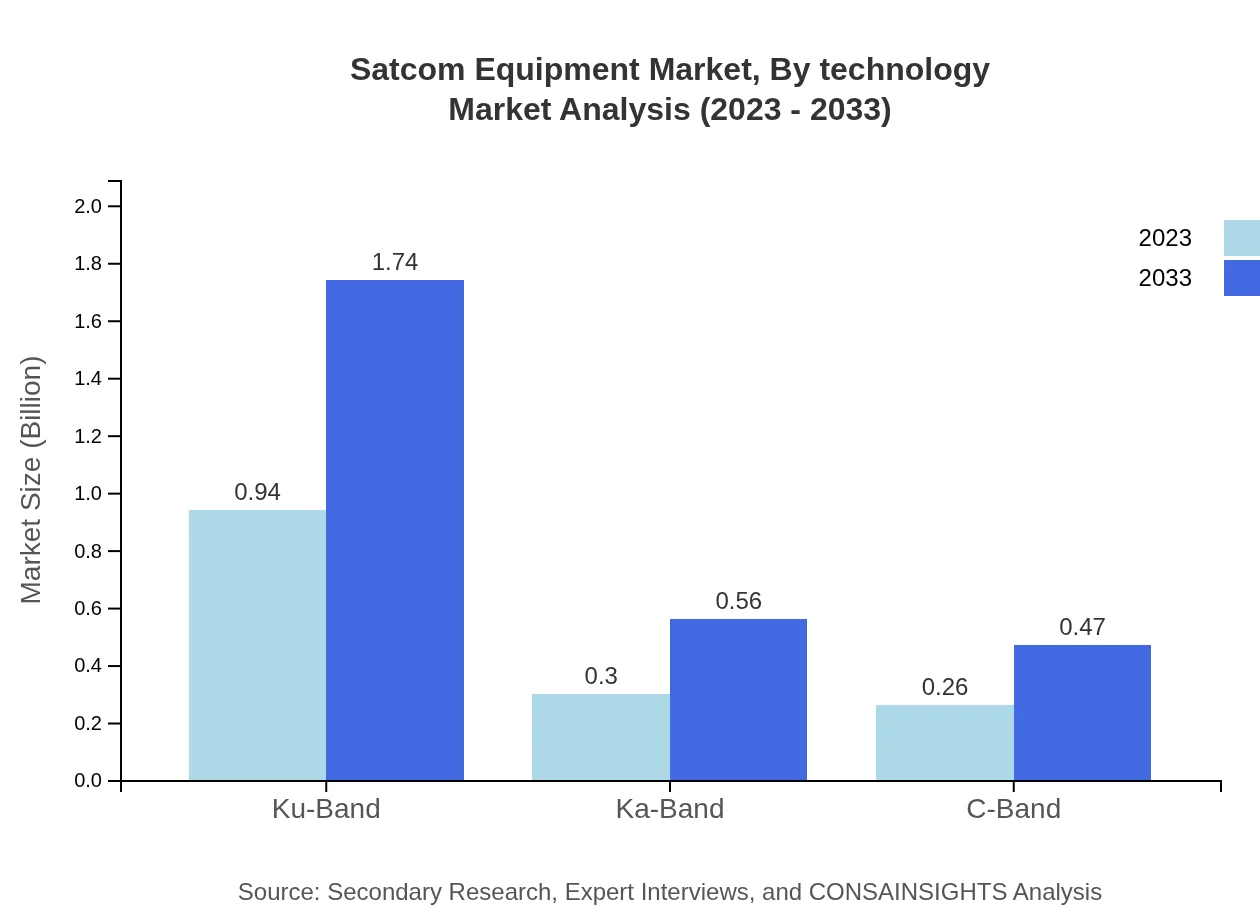

Satcom Equipment Market Analysis By Technology

The Ku-Band segment dominates the Satcom Equipment market, valued at $0.94 billion in 2023 and projected to reach $1.74 billion by 2033, maintaining a 62.75% share. The Ka-Band and C-Band segments also show consistent growth, with a focus on enhanced communication capabilities and expanding operational bandwidth to meet increasing consumer demands in various industries.

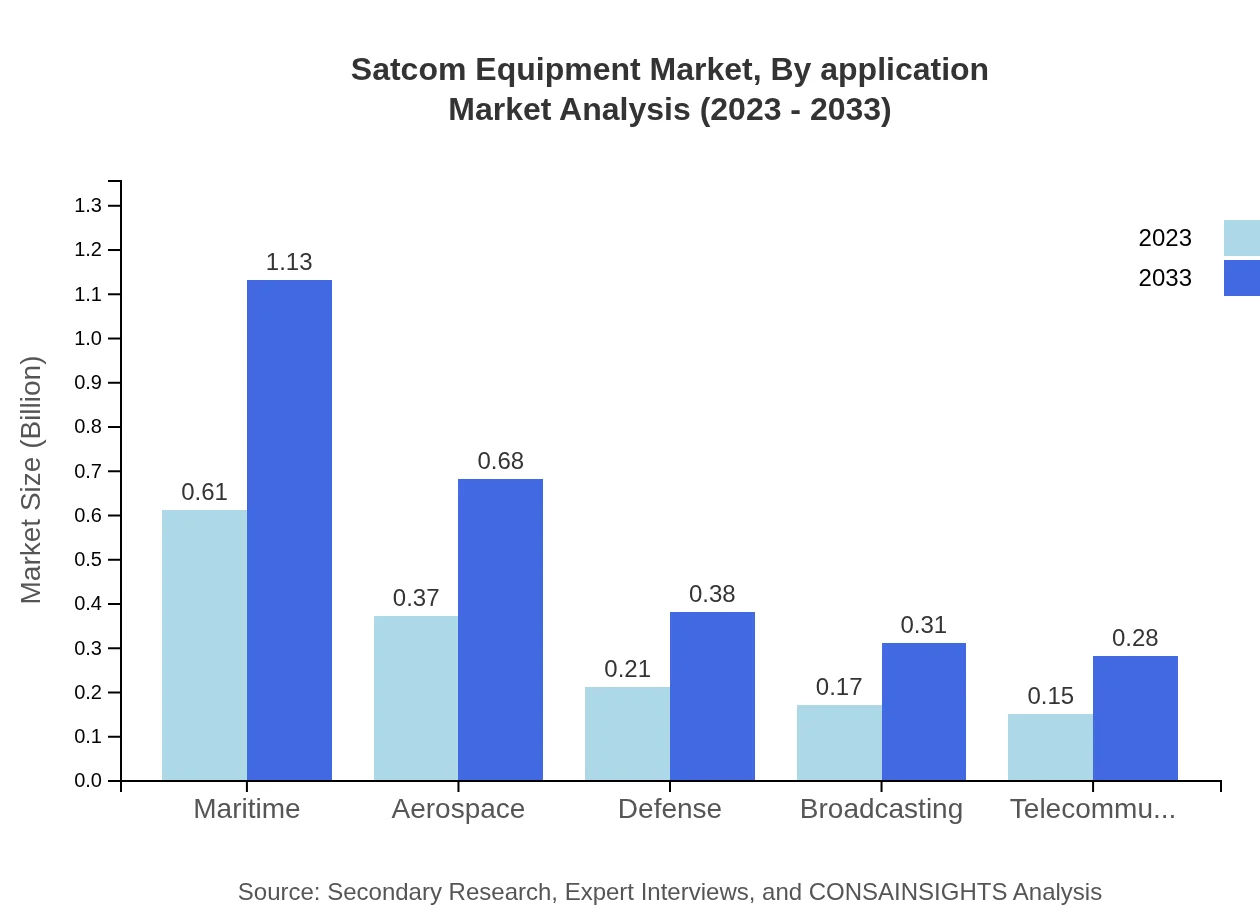

Satcom Equipment Market Analysis By End User

The Maritime sector holds a significant portion of the market, increasing from $0.61 billion in 2023 to $1.13 billion by 2033, signifying a 40.49% market share. Aerospace and Defense sectors follow closely with respective market sizes escalating from $0.37 billion and $0.21 billion to $0.68 billion and $0.38 billion by 2033. Each of these sectors demonstrates a rising dependency on satellite solutions for mission-critical operations.

Satcom Equipment Market Analysis By Distribution Channel

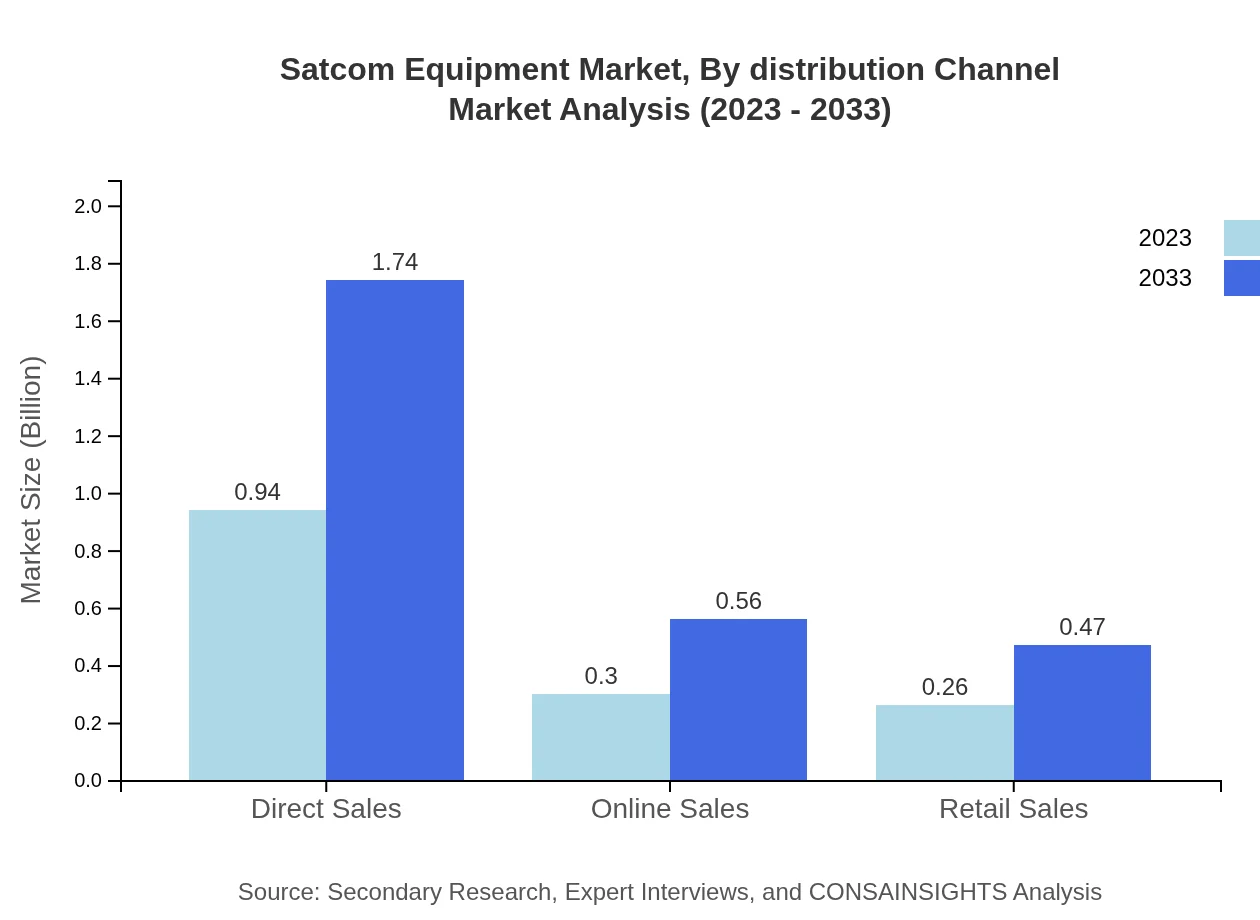

Direct Sales leads the distribution channels within the Satcom Equipment market, projected to grow from $0.94 billion to $1.74 billion with a 62.75% share. Online Sales and Retail Sales also play vital roles, growing from $0.30 billion to $0.56 billion and $0.26 billion to $0.47 billion respectively, indicating a shift toward digital channels for customer engagement.

Satcom Equipment Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Satcom Equipment Industry

Hughes Network Systems:

Hughes Network Systems is a leading provider of satellite broadband services and software technologies, renowned for its innovative hybrid satellite techniques that enhance communication reliability.Thales Group:

Thales Group excels in offering satellite communication systems, providing robust solutions across defense, aerospace, and transportation sectors while investing heavily in R&D for future innovations.SES S.A.:

SES S.A. is a prominent satellite operator offering various satellite communication services worldwide, focusing on broadband and video solutions through its extensive fleet of satellites.We're grateful to work with incredible clients.

FAQs

What is the market size of Satcom Equipment?

The global Satcom Equipment market is valued at approximately $1.5 billion in 2023, with an expected CAGR of 6.2% over the next decade. This growth reflects the increasing demand for satellite communications across various sectors.

What are the key market players or companies in the Satcom Equipment industry?

Key players in the Satcom Equipment market include major technology firms and specialized manufacturers of satellite communication technologies, each contributing significantly to advancements and innovations in the field.

What are the primary factors driving the growth in the Satcom Equipment industry?

Growth in the Satcom Equipment industry is primarily driven by the rising demand for broadband connectivity, increasing reliance on satellite services for defense and disaster recovery, and continuous technological advancements in satellite communication.

Which region is the fastest Growing in the Satcom Equipment market?

North America is currently the fastest-growing region in the Satcom Equipment market, with projected growth from $0.49 billion in 2023 to $0.90 billion by 2033, supported by widespread adoption of satellite technology.

Does ConsaInsights provide customized market report data for the Satcom Equipment industry?

Yes, ConsaInsights offers customized market report data for the Satcom Equipment industry, allowing clients to obtain insights tailored to their specific needs and strategic interests in the market.

What deliverables can I expect from this Satcom Equipment market research project?

Deliverables from the Satcom Equipment market research project typically include comprehensive market analysis, trend reports, competitor insights, and forecasts for market growth, segmented by region and equipment type.

What are the market trends of Satcom Equipment?

Key trends in the Satcom Equipment market include the rising adoption of Ku-Band and Ka-Band technologies, increased investment in satellite infrastructure, and a shift towards integrated communication solutions across various sectors.