Reports >

Chemicals And Materials

>

Silicon Metal Market Report

Silicon Metal Market Report

First published: 04 October 2024 | Last updated: 02 February 2026 | Report Code: silicon-metal

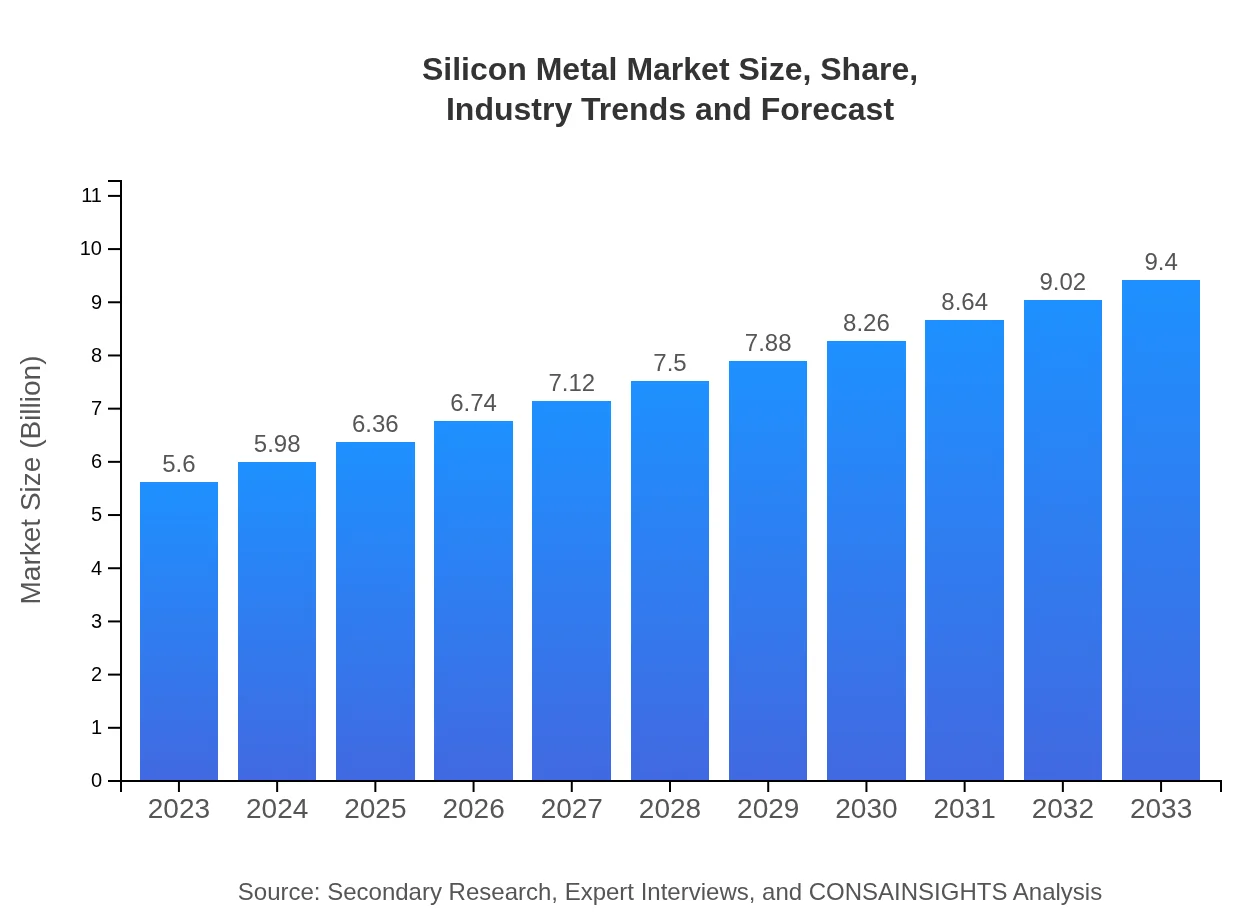

Silicon Metal Market — USD 5.6 billion in 2023, Growing to USD 9.40B by 2033 at 5.2% CAGR

This report provides an in-depth analysis of the Silicon Metal market from 2023 to 2033, covering market size, growth trends, segmentation, regional insights, innovations, and key players, offering a comprehensive view of this vital industrial sector.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.60 Billion |

| CAGR (2023-2033) | 5.2% |

| 2033 Market Size | $9.40 Billion |

| Top Companies | Silicor Materials Inc., Wacker Chemie AG, DowSil, Elkem ASA, China National BlueStar (Group) Co., Ltd. |

| Published Date | 04 October 2024 |

| Last Modified Date | 02 February 2026 |

Silicon Metal Market Overview

Customize Silicon Metal Market Report market research report

- ✔ Get in-depth analysis of Silicon Metal market size, growth, and forecasts.

- ✔ Understand Silicon Metal's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Silicon Metal

What is the Market Size & CAGR of Silicon Metal market in 2023?

Silicon Metal Industry Analysis

Silicon Metal Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Silicon Metal Market Analysis Report by Region

Europe Silicon Metal Market Report:

The European market in 2023 was estimated at USD 1.64 billion, with projections indicating a rise to USD 2.76 billion by 2033. The focus on renewable energy solutions across the EU is driving demand, supported by stringent regulations promoting sustainability.Asia Pacific Silicon Metal Market Report:

In 2023, the Asia Pacific market for Silicon Metal was valued at USD 1.15 billion and is expected to reach USD 1.93 billion by 2033, reflecting a steady growth rate driven primarily by China's robust electronics and solar industries. The region is poised to remain a dominant player, emphasizing high production capacities and technological advancements.North America Silicon Metal Market Report:

North America displayed a Silicon Metal market size of USD 1.84 billion in 2023, anticipated to expand to USD 3.09 billion by 2033. This growth is spurred by a surge in electric vehicle production and technological manufacturing, particularly in the US which is focusing on sustainable practices.South America Silicon Metal Market Report:

The South American market was valued at USD 0.33 billion in 2023, projected to grow to USD 0.55 billion by 2033. While relatively small, emerging sectors like renewable energy are fostering interest and gradually increasing demand for silicon metal in this region.Middle East & Africa Silicon Metal Market Report:

The Middle East and Africa market stood at USD 0.64 billion in 2023 with a forecasted growth to USD 1.07 billion by 2033. Growth in this region is being driven by infrastructural developments and increased investments in solar energy projects.Tell us your focus area and get a customized research report.

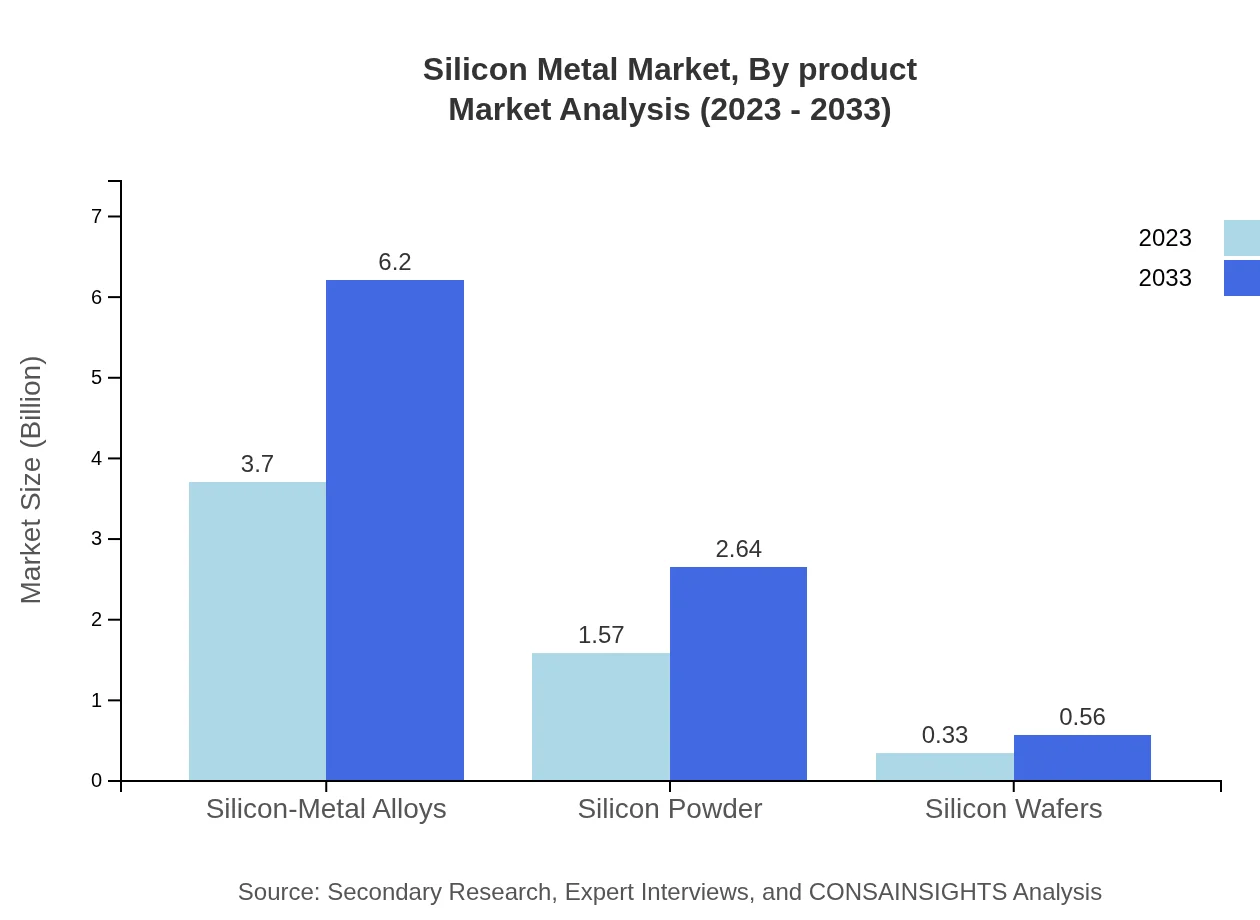

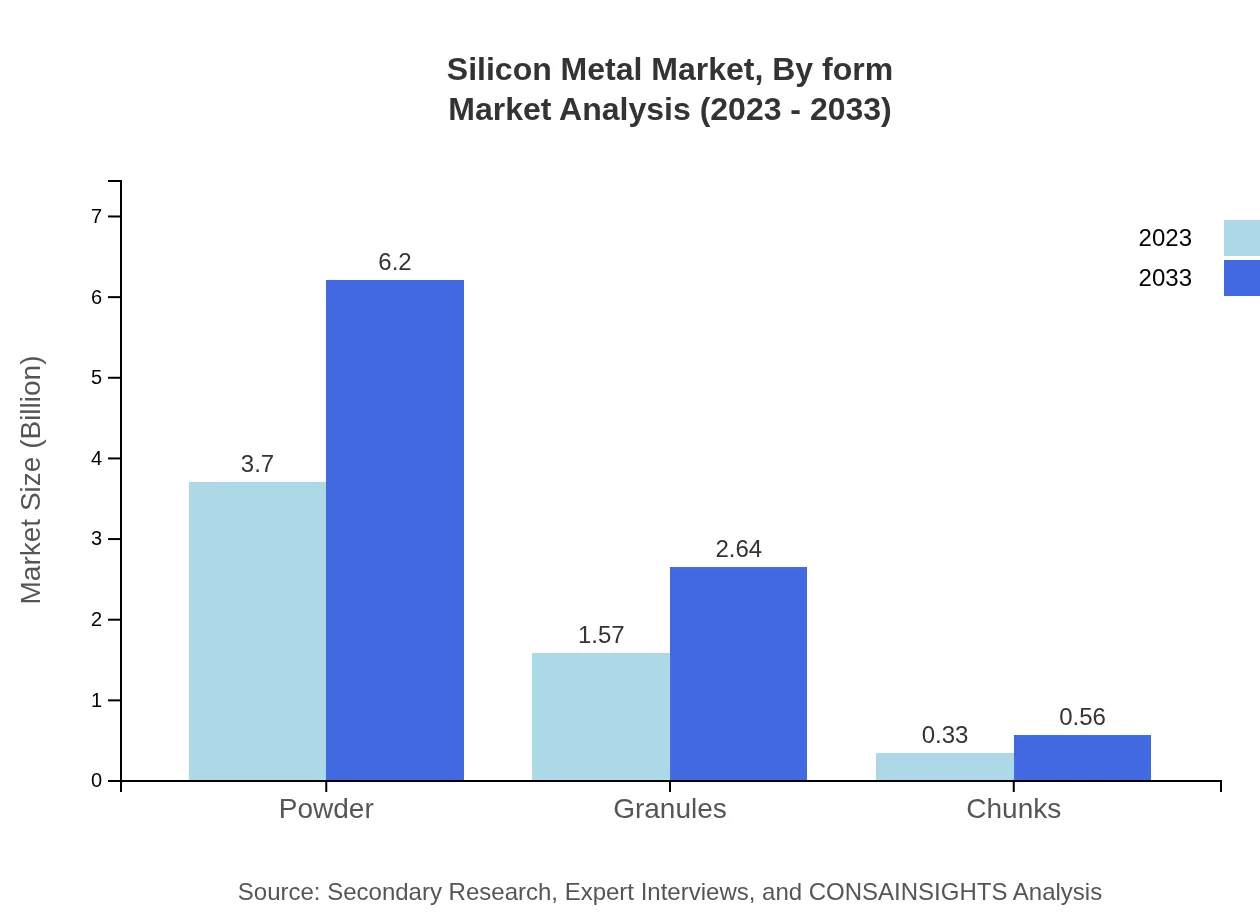

Silicon Metal Market Analysis By Product

The product segmentation showcases silicon powder dominating the market with a size of USD 3.70 billion in 2023 and expanding to USD 6.20 billion by 2033, holding a market share of 66%. Granules follow with a market valuation of USD 1.57 billion expected to grow to USD 2.64 billion. Chunks represent the smallest market segment, estimated at USD 0.33 billion scaling up to USD 0.56 billion. Silicon-Metal alloys also show significant growth potential, mirroring similar trends.

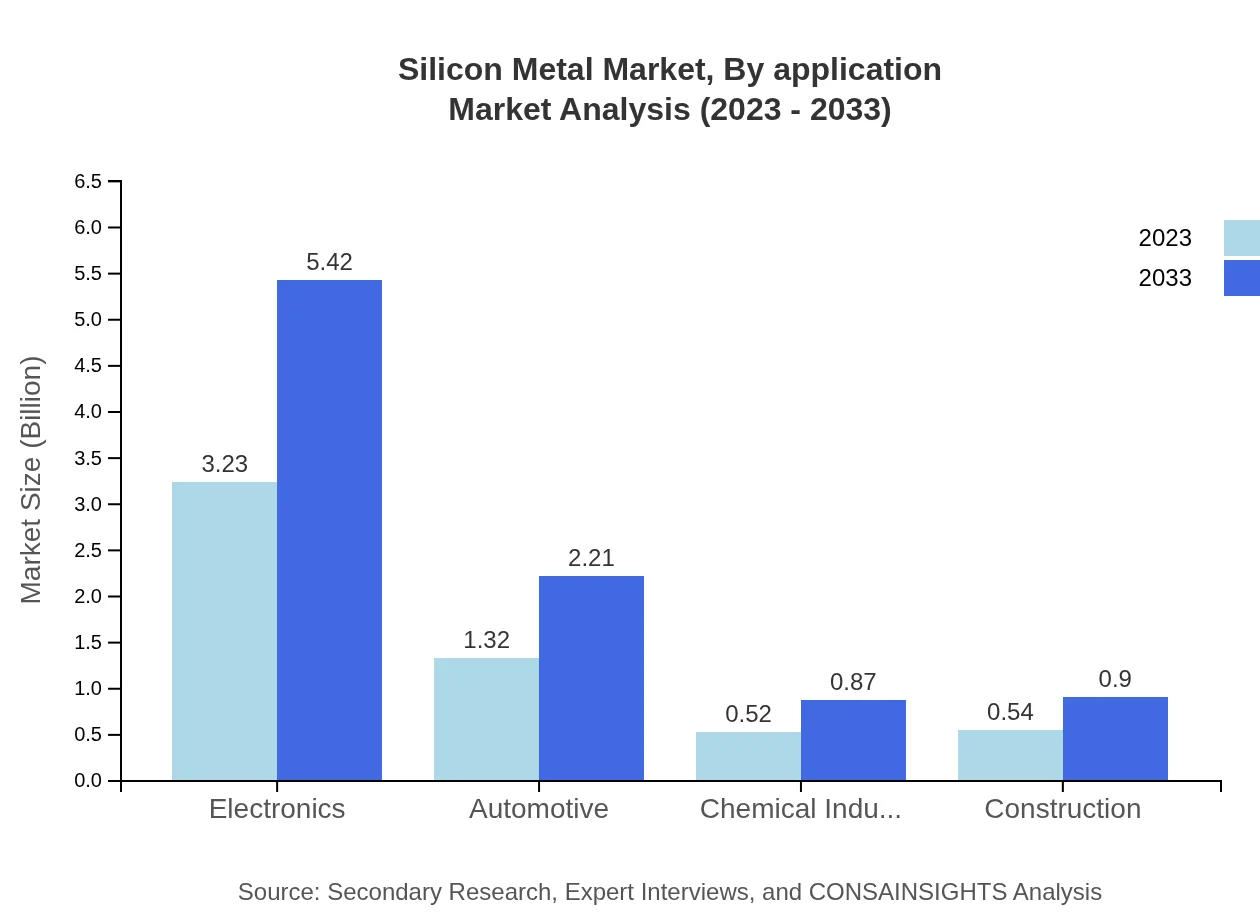

Silicon Metal Market Analysis By Application

Consumer electronics lead the application segment, with a size of USD 3.23 billion in 2023, expected to grow to USD 5.42 billion by 2033, accounting for 57.68% of the total share. The solar industry also presents remarkable growth prospects, from USD 1.32 billion to USD 2.21 billion, while other applications like automotive and aerospace, although smaller, are expanding.

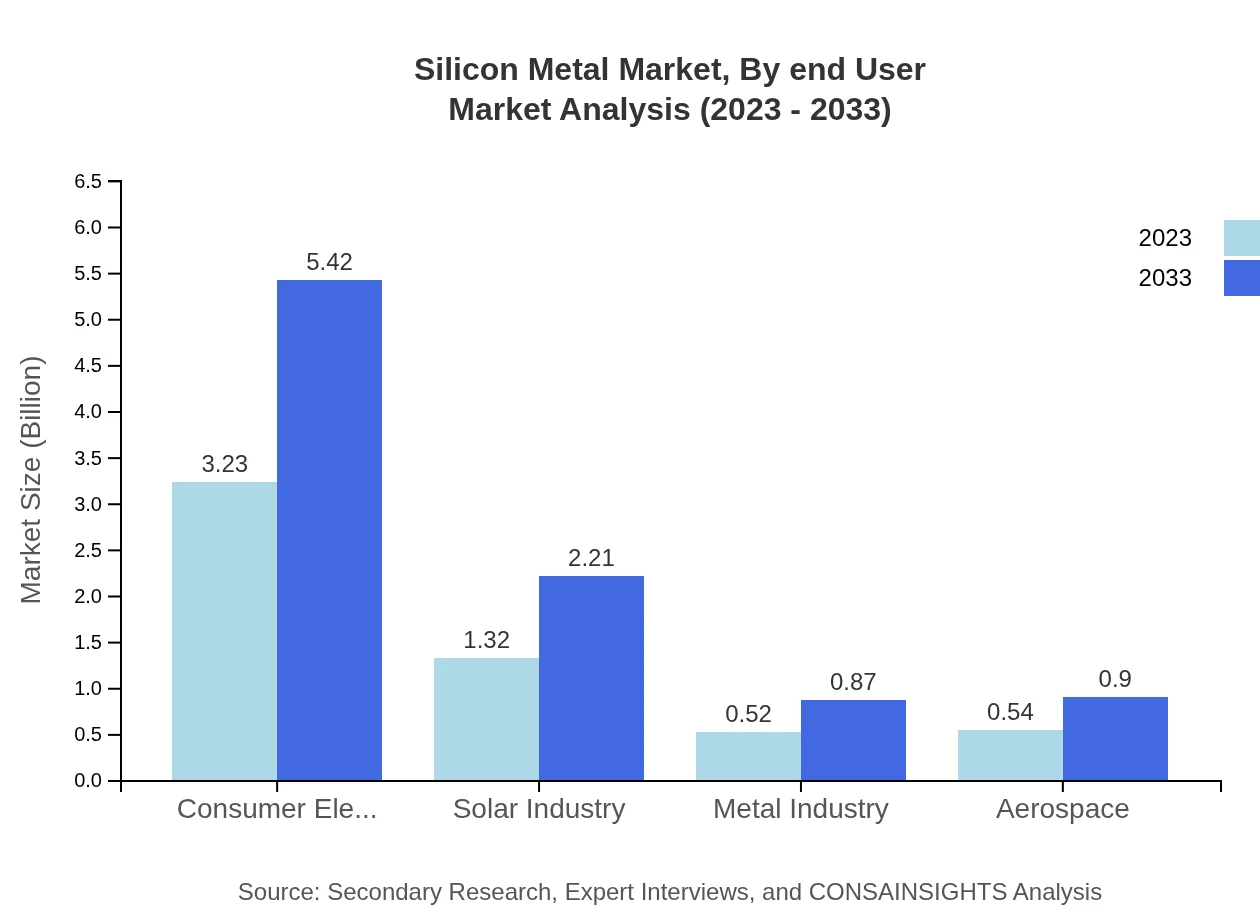

Silicon Metal Market Analysis By End User

End-user industries heavily influence market dynamics, with electronics and consumer sectors leading the charge. The chemical industry, pharmaceutical applications, and aerospace are also significant, contributing to sustainable growth and product demand in the metals and aeronautical engineering sectors.

Silicon Metal Market Analysis By Form

The form of silicon metal varies by end usage, with powder and granules being prominent. Customers often require customized silicon statements based on application needs, which drives the need for flexibility in manufacturing forms and sizes of silicon metal products.

Silicon Metal Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Silicon Metal Industry

Silicor Materials Inc.:

A leading provider of solar silicon, focusing on advancing manufacturing technologies to leverage the growing solar market.Wacker Chemie AG:

A global producer of silicon-based products, contributing significantly to various sectors including electronics, automotive, and construction.DowSil:

Known for its silicone solutions, DowSil is a critical player in the development of silicon products across industries.Elkem ASA:

A major supplier of silicon and silicon-based advanced materials for the aluminum, solar, and chemical industries.China National BlueStar (Group) Co., Ltd.:

A prominent Chinese player involved in the silicon sector, majorly serving the domestic and export markets.We're grateful to work with incredible clients.

FAQs

What is the market size of silicon Metal?

The global silicon metal market size is projected to reach approximately $5.6 billion by 2033, growing at a CAGR of 5.2%. The market indicates robust demand, attributed to increased application in metallurgy, electronics, and renewable energy sectors.

What are the key market players or companies in this silicon Metal industry?

Key players in the silicon metal industry include Wacker Chemie AG, Elkem ASA, and OCI Company Ltd. These companies lead the market with extensive product portfolios and technological advancements, catering to various sectors such as electronics and the automotive industry.

What are the primary factors driving the growth in the silicon metal industry?

Growth in the silicon metal industry is driven by rising demand for silicon-based products in consumer electronics, the solar industry, and the aerospace sector. Additionally, increasing investment in renewable energy and advancements in electric vehicles significantly bolster the market.

Which region is the fastest Growing in the silicon metal market?

The fastest-growing region in the silicon metal market is North America, expected to surge from $1.84 billion in 2023 to $3.09 billion by 2033. This growth is fueled by expanding technology sectors and the increasing adoption of silicon metal in energy applications.

Does ConsaInsights provide customized market report data for the silicon metal industry?

Yes, ConsaInsights offers customized market report data for the silicon metal industry. Clients can benefit from tailored insights based on specific needs, ensuring a comprehensive understanding of market dynamics and trends relevant to their strategic objectives.

What deliverables can I expect from this silicon metal market research project?

Deliverables from the silicon metal market research project include detailed market analysis reports, forecasts, regional breakdowns, and competitive landscape studies. These insights will assist in strategic planning and informed decision-making for stakeholders.

What are the market trends of silicon metal?

Current market trends for silicon metal include rising application in renewable energy technologies, especially solar panels, and increased usage in consumer electronics. Growth in automotive and aerospace sectors also drives innovation and demand for silicon-based solutions.