Automated Ophthalmic Perimeters Market Report

First published: 08 October 2024 | Last updated: 25 May 2026 | Report Code: automated-ophthalmic-perimeters

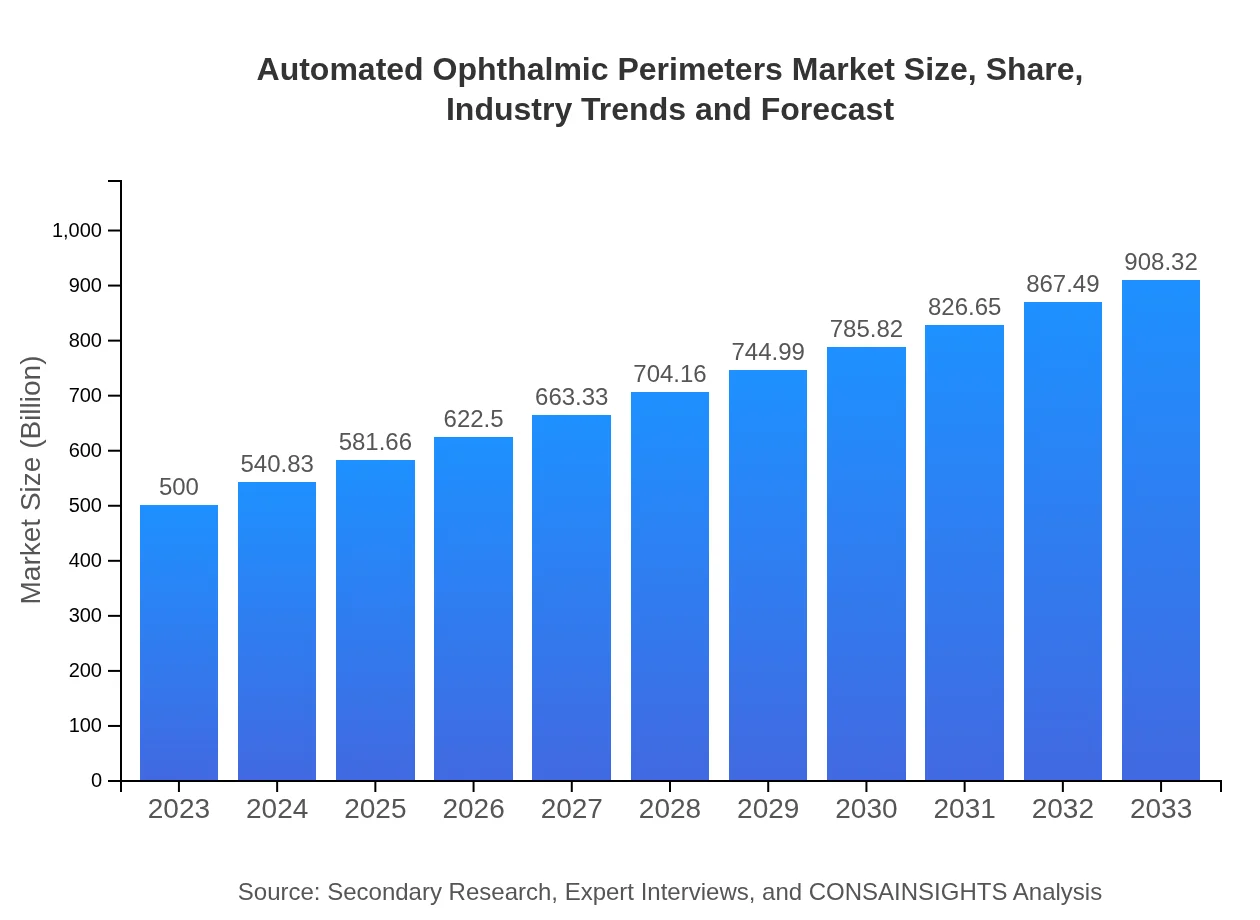

Automated Ophthalmic Perimeters Market — USD 500 million in 2023, Growing to USD 908.32M by 2033 at 6% CAGR

This report provides an in-depth analysis of the Automated Ophthalmic Perimeters market, covering market size, industry trends, and forecasts from 2023 to 2033. Insights are included on technological advancements, regional dynamics, and major players shaping the industry.

Key Takeaways

- Global market value rises from $500.00 Billion in 2023 to $908.32 Billion in 2033, reflecting a 6% CAGR over 2023 to 2033.

- North America is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- Technology enhancements and adoption in glaucoma screening and retinal disease diagnostics are core expansion drivers.

- Top vendors include Carl Zeiss AG, Humphrey Instruments, Nidek Co. Ltd., and Topcon Corporation, focusing on innovation and device accuracy.

Automated Ophthalmic Perimeters Market Report — Executive Summary

North America remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. The Automated Ophthalmic Perimeters market is expanding underpinned by rising demand for accurate visual field testing and enhanced patient experience. Market value moves from $500.00 Billion in 2023 to $908.32 Billion by 2033 at a 6% CAGR over 2023 to 2033. Key enablers include advances in digital imaging, automated testing systems, and software solutions facilitating glaucoma screening and retinal disease monitoring. Vendors such as Carl Zeiss AG, Humphrey Instruments, Nidek Co. Ltd., and Topcon Corporation are prioritizing product refinement and regulatory compliance. Regional adoption varies, with North America holding the largest share. Market segmentation spans product types like static and kinetic perimeters, technology nodes including optical coherence tomography, end users ranging from hospitals to research laboratories, and distribution channels such as direct and online sales. Looking ahead, integration with telemedicine frameworks and tighter performance standards will influence procurement and deployment strategies across healthcare providers.

Key Growth Drivers

- Increased prevalence of eye disorders spurring demand for routine visual field testing and monitoring.

- Technological progress in digital imaging and automated testing systems improving diagnostic precision and workflow efficiency.

- Rising awareness of early screening benefits driving adoption across hospitals, clinics, and diagnostic centers.

- Regulatory clearances for advanced devices encouraging wider clinical deployment and investment in ophthalmic diagnostics.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $500.00 Million |

| CAGR (2023-2033) | 6% |

| 2033 Market Size | $908.32 Million |

| Top Companies | Carl Zeiss AG, Humphrey Instruments, Nidek Co. Ltd., Topcon Corporation |

| Published Date | 08 October 2024 |

| Last Modified Date | 25 May 2026 |

Automated Ophthalmic Perimeters Market Overview

Customize Automated Ophthalmic Perimeters Market Report market research report

- ✔ Get in-depth analysis of Automated Ophthalmic Perimeters market size, growth, and forecasts.

- ✔ Understand Automated Ophthalmic Perimeters's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Automated Ophthalmic Perimeters

What is the Market Size & CAGR of Automated Ophthalmic Perimeters Market Report market in 2023?

Automated Ophthalmic Perimeters Industry Analysis

Automated Ophthalmic Perimeters Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Automated Ophthalmic Perimeters Market Report Market Analysis Report by Region

Europe Automated Ophthalmic Perimeters Market Report:

Europe grows from $145.35 Billion in 2023 to $264.05 Billion in 2033. Expansion is driven by increasing screening initiatives for eye diseases, uptake of digital imaging technologies, and regulatory pathways supporting device deployment.Asia Pacific Automated Ophthalmic Perimeters Market Report:

Asia Pacific grows from $97.75 Billion in 2023 to $177.58 Billion in 2033. Growth factors include rising awareness of eye health, broader access to diagnostic services, and investment in automated testing equipment within clinical settings.North America Automated Ophthalmic Perimeters Market Report:

North America is largest regional market, rising from $175.85 Billion in 2023 to $319.46 Billion in 2033. Regional momentum is linked to established clinical infrastructure, high adoption of advanced diagnostic devices, and investments in ophthalmic screening programs.South America Automated Ophthalmic Perimeters Market Report:

Latin America grows from $44.15 Billion in 2023 to $80.2 Billion in 2033. Market growth reflects expanding diagnostic capacity, higher prioritization of ophthalmic screening, and gradual adoption of automated perimeter solutions.Middle East & Africa Automated Ophthalmic Perimeters Market Report:

Middle East and Africa grows from $36.9 Billion in 2023 to $67.03 Billion in 2033. Drivers include improving healthcare infrastructure, increased screening efforts, and gradual integration of advanced diagnostic technologies.Tell us your focus area and get a customized research report.

Research Methodology

Automated Ophthalmic Perimeters Market Analysis By Product Type

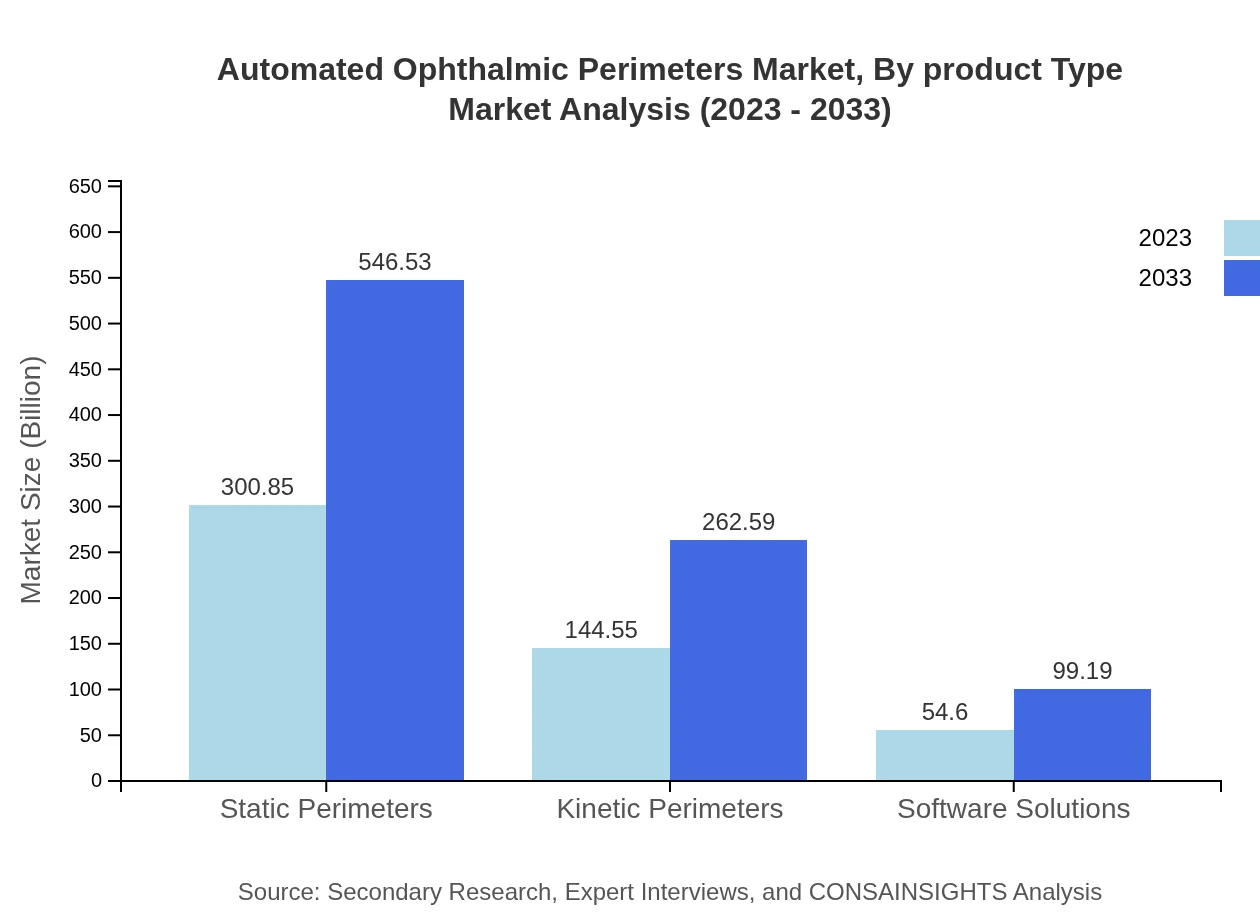

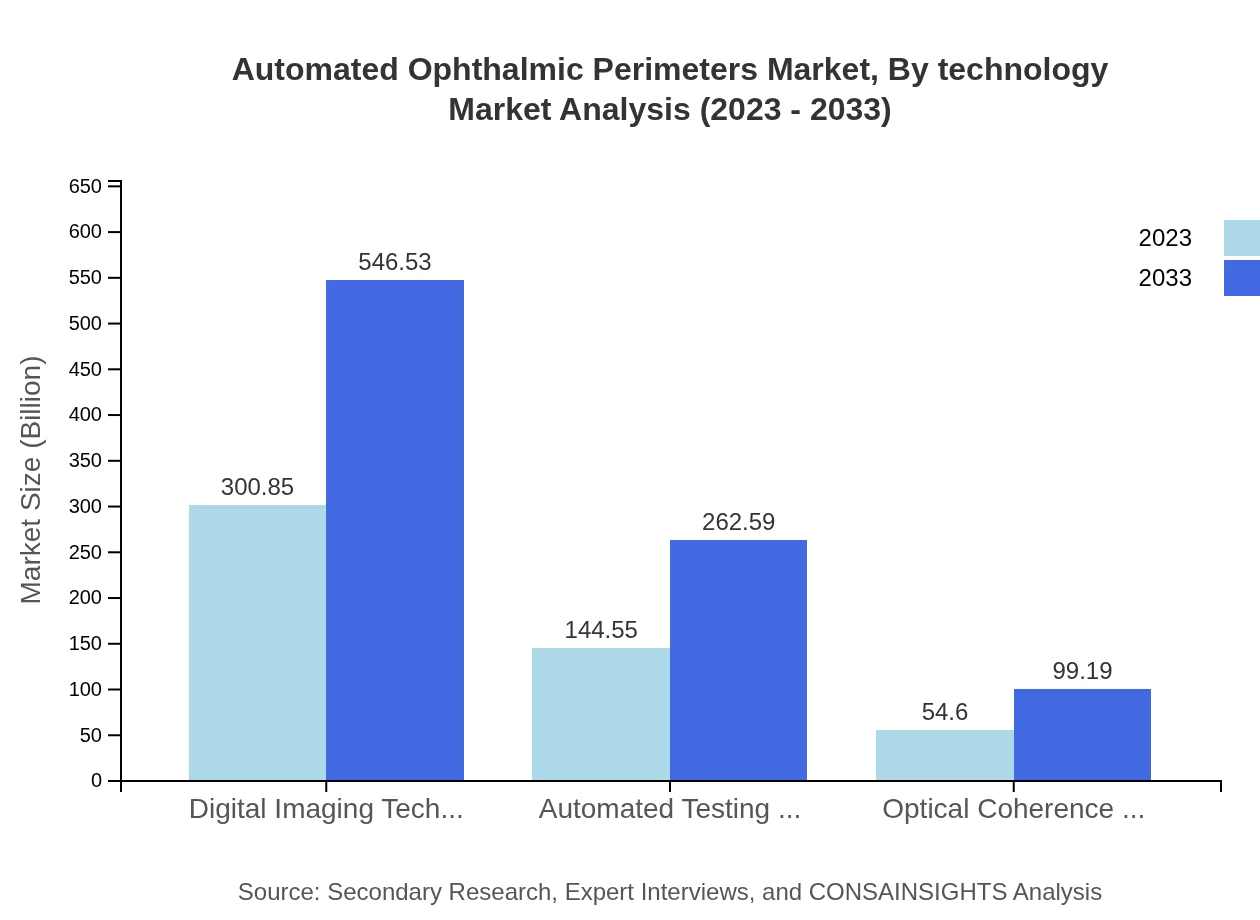

The market is segmented by product type, including Digital Imaging Technology, Automated Testing Systems, and Optical Coherence Tomography. Digital Imaging Technology dominates with a market size of $300.85 million in 2023, expected to grow to $546.53 million by 2033, retaining a 60.17% market share. Automating testing systems also hold substantial value with market sizes growing from $144.55 million to $262.59 million over the same period.

Automated Ophthalmic Perimeters Market Analysis By Application

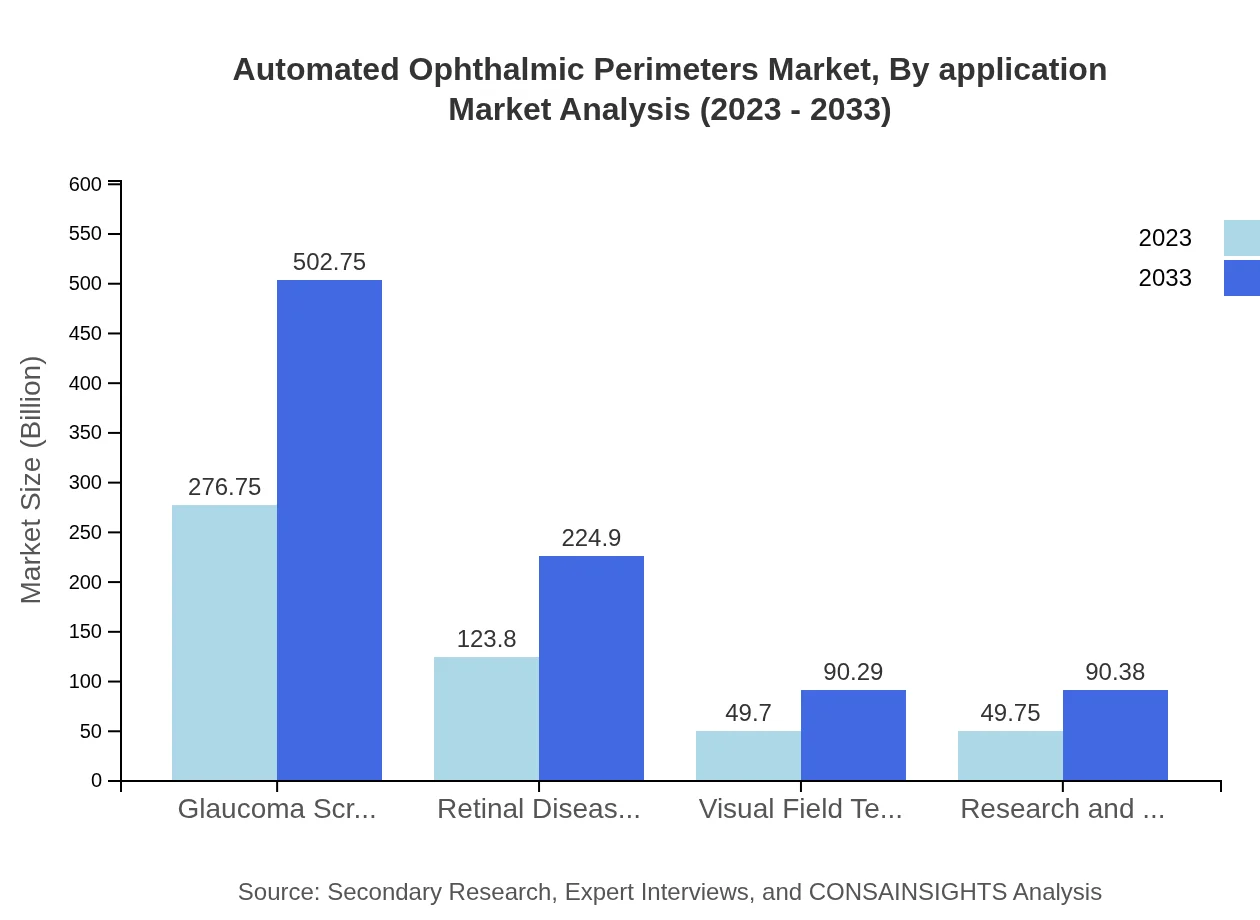

The applications for Automated Ophthalmic Perimeters include glaucoma screening, retinal disease screening, and visual field testing. Glaucoma screening is the leading application, holding a market size of $276.75 million in 2023, projected to grow to $502.75 million by 2033 with a steady market share of 55.35%. The consistent growth reflects the high volume of glaucoma patients and the need for regular monitoring.

Automated Ophthalmic Perimeters Market Analysis By End User

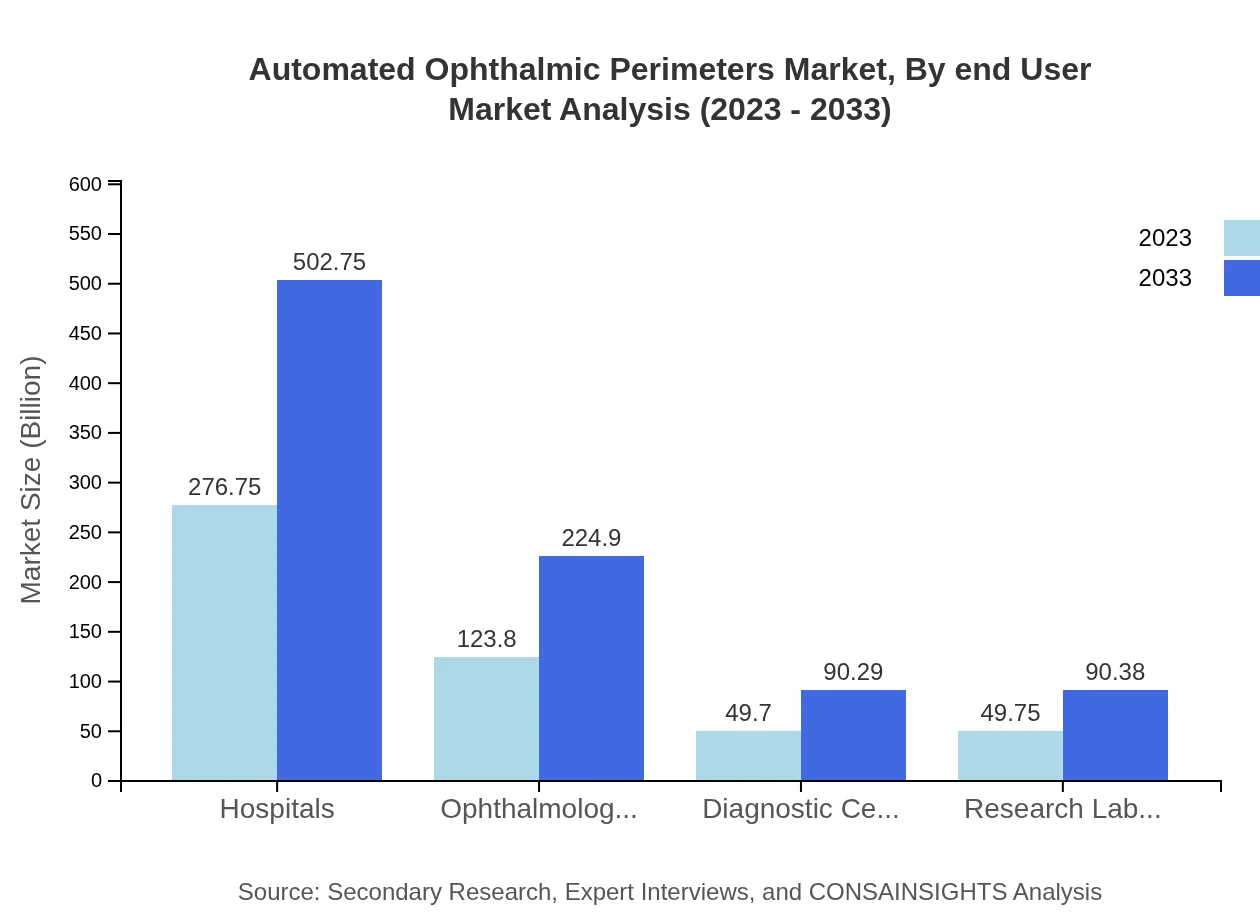

The market's end-users are categorized into hospitals, ophthalmology clinics, diagnostic centers, and research laboratories. Hospitals are the largest end-user segment, with market values expected to rise from $276.75 million in 2023 to $502.75 million by 2033. This growth is accelerated by increasing investments in healthcare facilities and technology integration in hospitals.

Automated Ophthalmic Perimeters Market Analysis By Technology

Technological advancements in Automated Ophthalmic Perimeters include digital imaging and telemedicine integration enhancing remote patient diagnostics. Leading this segment is digital imaging technology, leveraging advances that promote better diagnostic precision and efficiency with a market size projected to reach beyond $546 million by 2033.

Automated Ophthalmic Perimeters Market Analysis By Distribution Channel

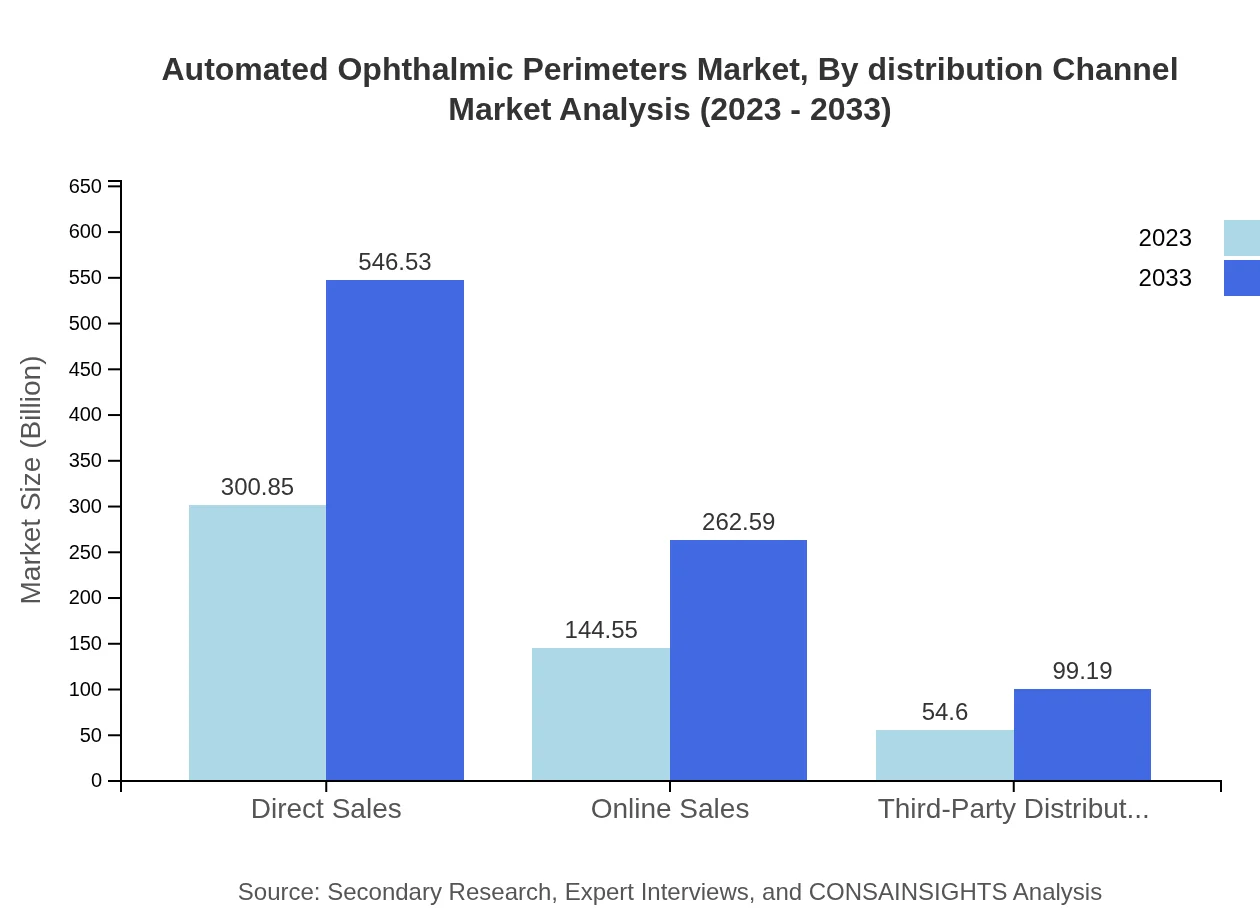

Distribution channels are critical for market reach, segmented into direct sales, online sales, and third-party distributors. Direct sales contribute significantly with a size of $300.85 million in 2023, with expected growth to $546.53 million by 2033. Online sales have also become increasingly important, reflecting the shift toward digital procurement in healthcare.

Automated Ophthalmic Perimeters Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Automated Ophthalmic Perimeters Industry

Carl Zeiss AG:

A key player in optical and optoelectronic systems, Zeiss produces advanced automated perimeters focused on superior quality and performance in eye diagnostics.Humphrey Instruments:

Specializes in visual field testing equipment and is known for innovative solutions in ophthalmology including automated visual field analyzers.Nidek Co. Ltd.:

Nidek provides a comprehensive portfolio of ophthalmic devices, including advanced automated perimeters that leverage cutting-edge technology for enhanced diagnostics.Topcon Corporation:

Another prominent market player known for developing sophisticated eye care equipment including automated perimeters aimed at improving patient care.We're grateful to work with incredible clients.

FAQs

What is the market size in 2023?

The market size for Automated Ophthalmic Perimeters in 2023 is $500.00 Billion as stated in the report data.

What is the projected market value in 2033?

The forecasted market value for 2033 is $908.32 Billion according to the provided figures.

What is CAGR for the forecast period?

The compound annual growth rate for the period 2023 to 2033 is 6% based on the supplied market projections.

Is there a single fastest Growing region in the Automated Ophthalmic Perimeters Market Report market?

No single fastest-growing region is stated for the Automated Ophthalmic Perimeters Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Which companies lead the market?

Top companies listed include Carl Zeiss AG, Humphrey Instruments, Nidek Co. Ltd., and Topcon Corporation.

What are the main product categories?

Primary product types include Static Perimeters, Kinetic Perimeters, and Software Solutions as outlined in the segmentation facts.

How are end users classified?

End users comprise Hospitals, Ophthalmology Clinics, Diagnostic Centers, and Research Laboratories according to the segmentation details.

What technologies drive device improvements?

Key technologies cited are Digital Imaging Technology, Automated Testing Systems, and Optical Coherence Tomography enhancing diagnostic capabilities.

Who conducted the research?

The methodology includes primary interviews with industry experts plus secondary research from company reports and publications, with data triangulation.

What distribution channels are used?

Distribution channels noted are Direct Sales, Online Sales, and Third-Party Distributors in the provided segment facts.