Automatic Train Control Market Report

First published: 12 October 2024 | Last updated: 22 January 2026 | Report Code: automatic-train-control

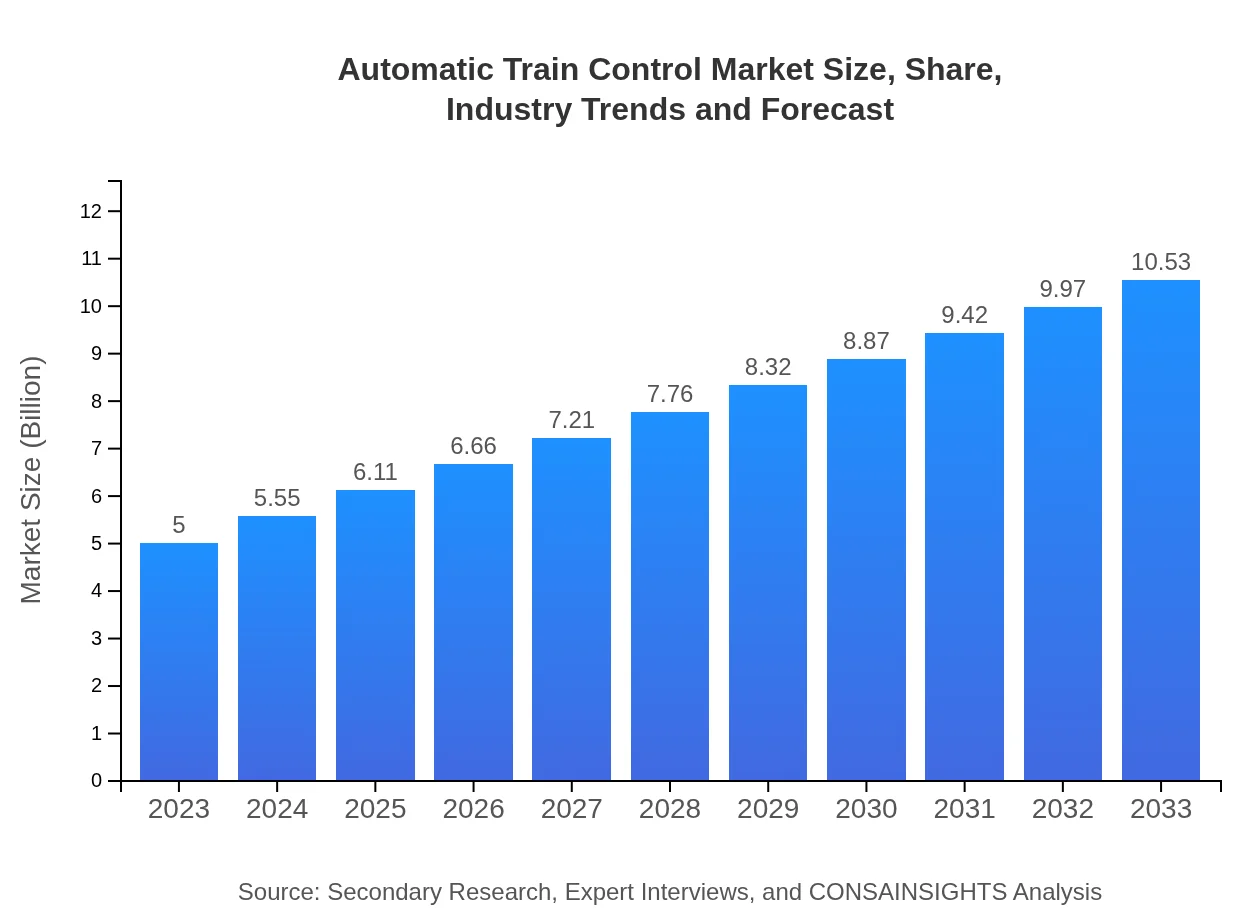

Automatic Train Control Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides a comprehensive analysis of the Automatic Train Control market, focusing on the projected growth from 2023 to 2033. It includes market size insights, key trends, regional dynamics, and company profiles of leading players in the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Siemens AG, Alstom, Bombardier Inc., Thales Group |

| Published Date | 12 October 2024 |

| Last Modified Date | 22 January 2026 |

Automatic Train Control Market Overview

Customize Automatic Train Control Market Report market research report

- ✔ Get in-depth analysis of Automatic Train Control market size, growth, and forecasts.

- ✔ Understand Automatic Train Control's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Automatic Train Control

What is the Market Size & CAGR of Automatic Train Control market in 2023?

Automatic Train Control Industry Analysis

Automatic Train Control Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Automatic Train Control Market Analysis Report by Region

Europe Automatic Train Control Market Report:

The European Automatic Train Control market is expected to rise from $1.29 billion in 2023 to $2.71 billion by 2033. The region's commitment to enhancing rail safety and implementing sustainable transport solutions is driving the adoption of advanced ATC systems, supported by significant EU funding and initiatives.Asia Pacific Automatic Train Control Market Report:

In the Asia Pacific region, the ATC market is projected to grow from $1.00 billion in 2023 to $2.10 billion by 2033. The region's rapid urbanization, investment in railway infrastructure, and government-led initiatives to enhance public transport systems contribute to this expansion. Countries like China and India are leaders in adopting innovative rail solutions, driving market demand.North America Automatic Train Control Market Report:

In North America, the market is projected to grow significantly from $1.78 billion in 2023 to $3.75 billion by 2033. Strong governmental policies promoting safety and efficiency in the rail sector, combined with technological advancements, are pivotal for this growth, especially with the modernization of existing rail networks.South America Automatic Train Control Market Report:

The South American market for Automatic Train Control is expected to rise from $0.25 billion in 2023 to $0.52 billion by 2033. Investments in metro and rail infrastructure are growing, primarily driven by urban development projects and increasing population density in major cities like São Paulo and Buenos Aires.Middle East & Africa Automatic Train Control Market Report:

In the Middle East and Africa, the ATC market is anticipated to increase from $0.68 billion in 2023 to $1.44 billion by 2033. Growing urban rail projects, investment in transportation infrastructure, and a focus on safety enhancements are key factors fueling this growth.Tell us your focus area and get a customized research report.

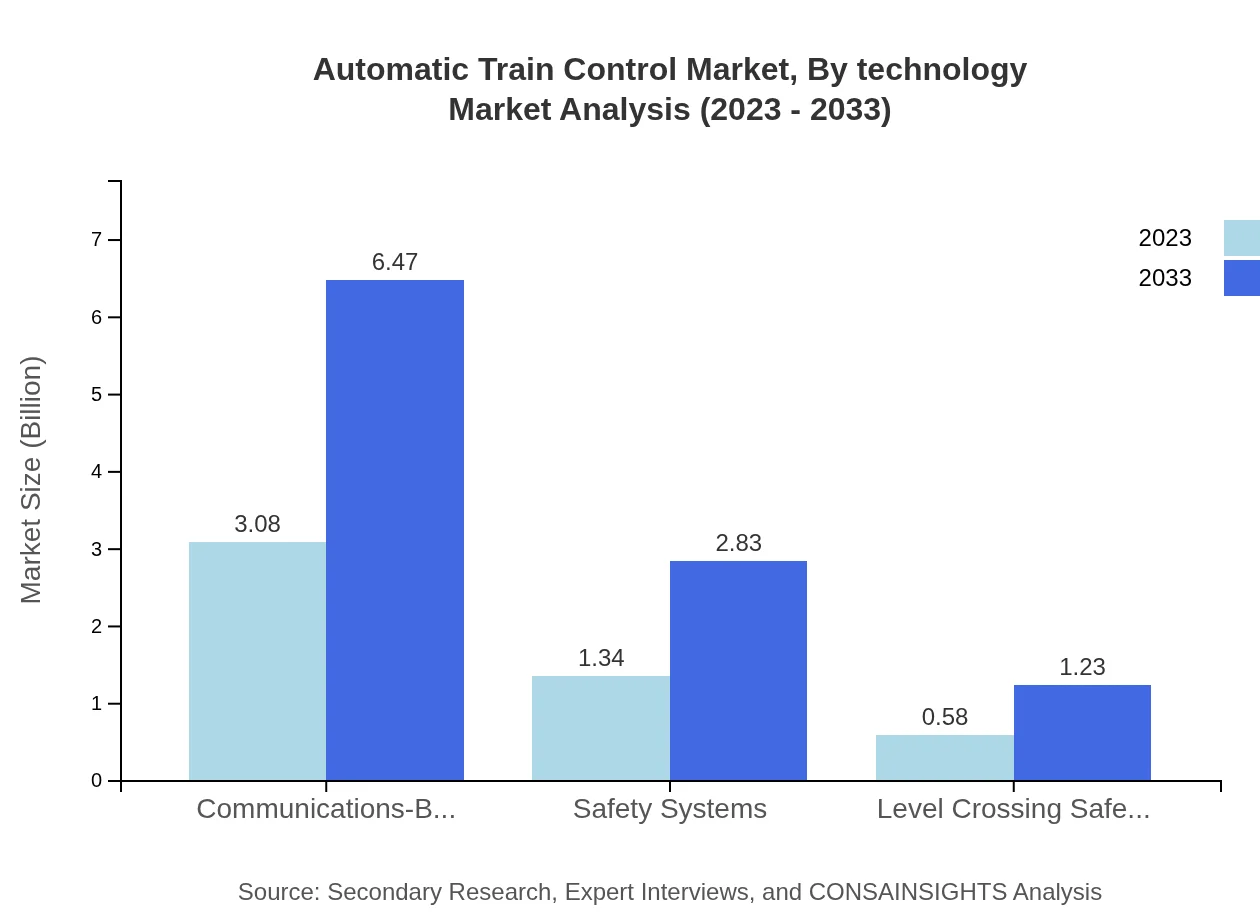

Automatic Train Control Market Analysis By Technology

The ATC market by technology encompasses advancements such as Communications-Based Train Control (CBTC) and Automatic Train Protection (ATP). The CBTC segment alone is projected to grow, with significant investments being funneled into this technology to enhance urban transport efficiency. These technological advancements are aimed at reducing human errors while enhancing the safety and reliability of train operations.

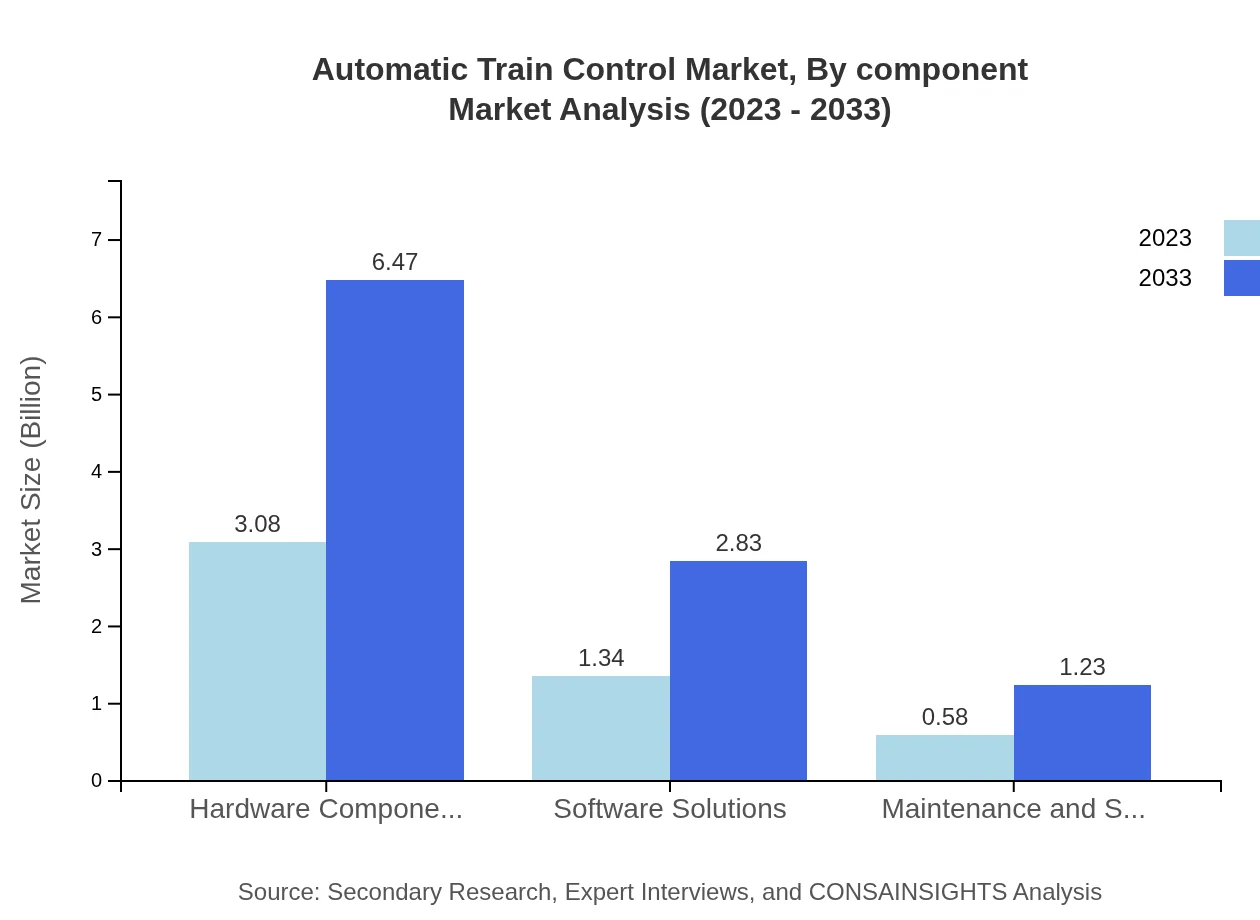

Automatic Train Control Market Analysis By Component

The market segmentation by component includes hardware components, software solutions, and maintenance services. In 2023, hardware components account for a substantial market share, projected to be valued at $3.08 billion. Software solutions are also gaining prominence for their role in data management, system efficiency, and real-time monitoring capabilities.

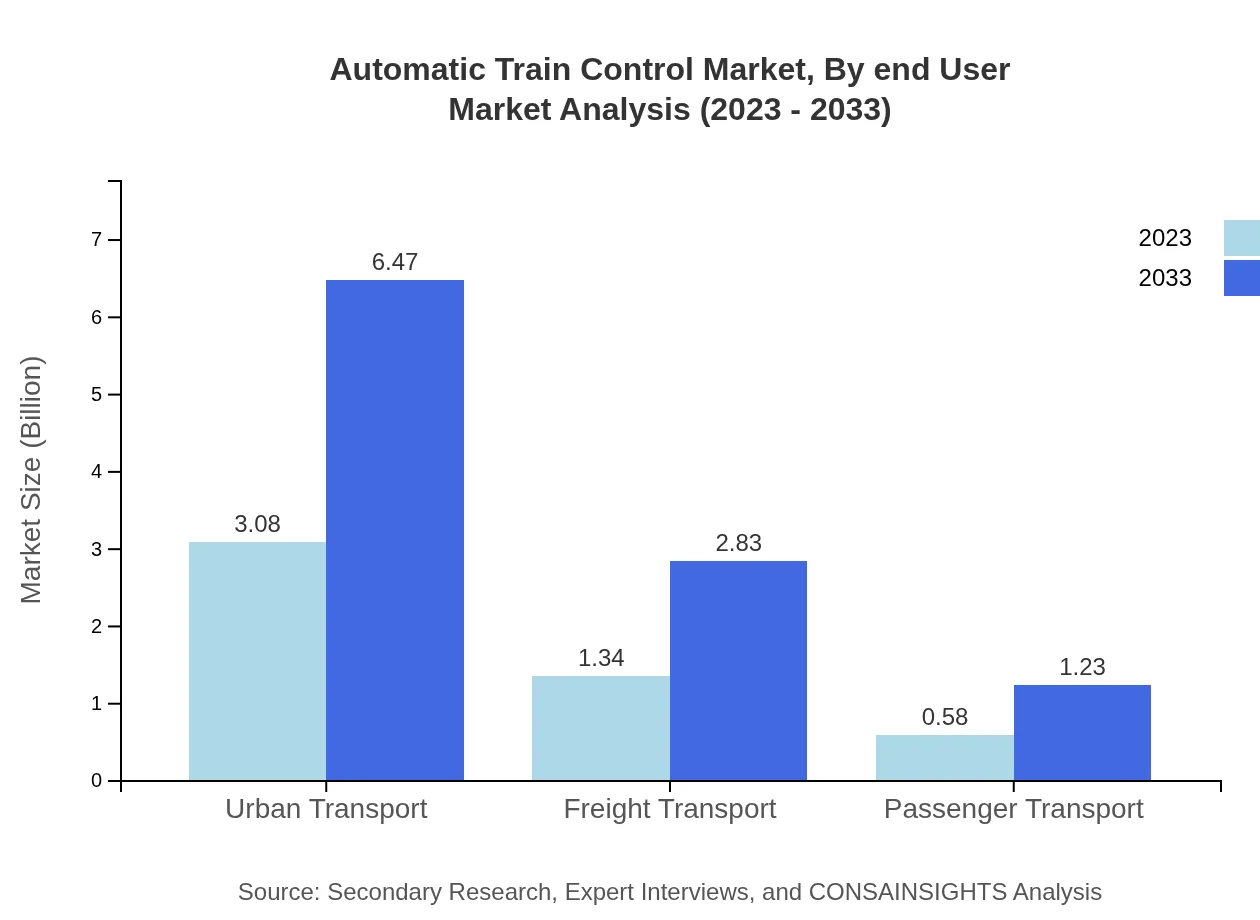

Automatic Train Control Market Analysis By End User

The end-user segmentation highlights urban transport, freight transport, and passenger transport. Urban transport dominates the market, constituting approximately 61.5% of the share in 2023. Freight transport, accounting for about 26.85%, is also expected to see growth in demand as logistics operations continue to modernize.

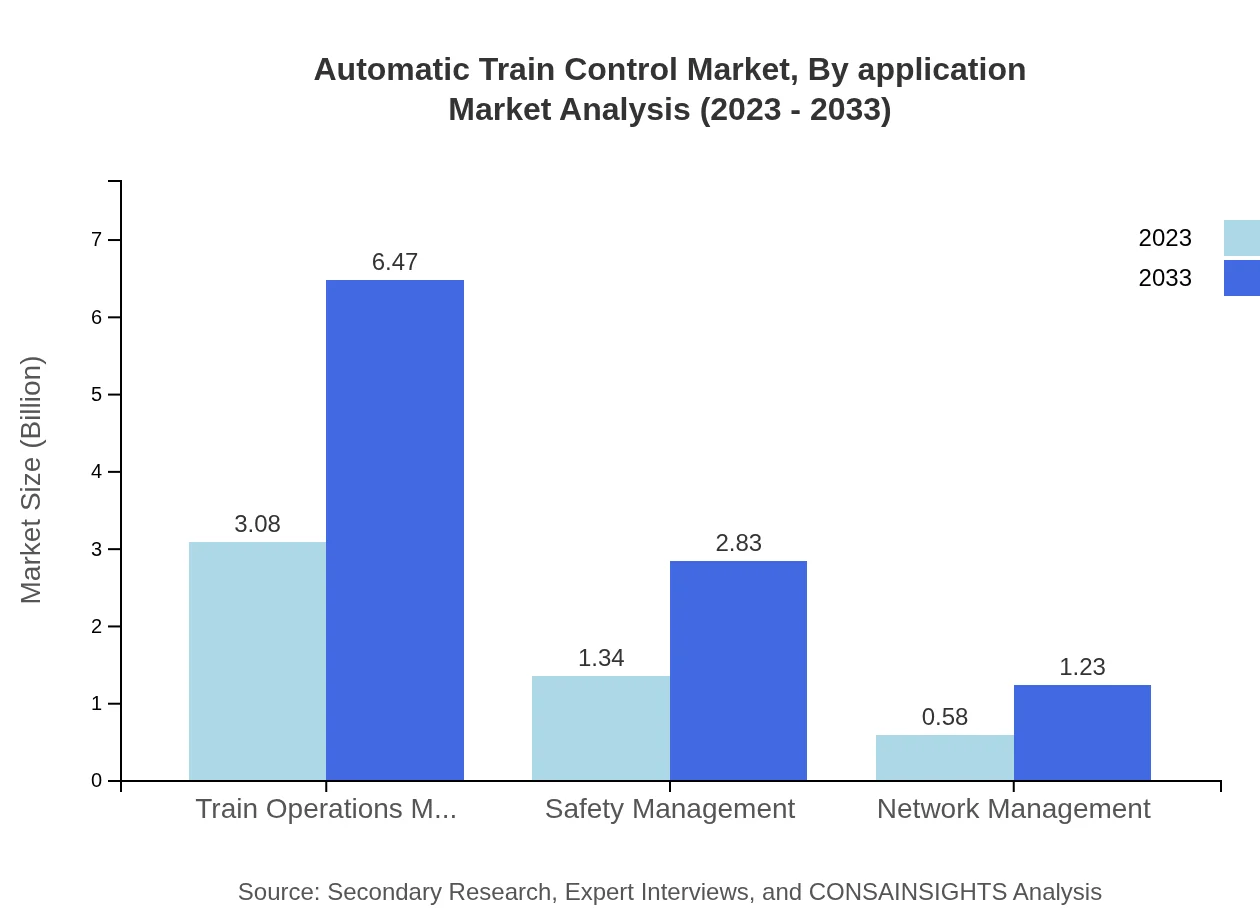

Automatic Train Control Market Analysis By Application

Applications of ATC systems range from safety management to network management and train operations management. The demand for safety management solutions is critical, accounting for a significant market portion, given the necessity for enhancing the safety and reliability of rail services.

Automatic Train Control Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Automatic Train Control Industry

Siemens AG:

Siemens AG is a leading industrial manufacturing company that plays a significant role in the ATC market through robust technology offerings focused on smart mobility solutions.Alstom:

Alstom specializes in rail transport and has developed advanced ATC systems that enhance the safety and efficiency of urban and suburban transport networks.Bombardier Inc.:

Bombardier is known for its cutting-edge rail systems, including automatic train control solutions that support the burgeoning demand for rapid transit systems.Thales Group:

Thales Group offers innovative solutions for rail systems, focusing on enhancing safety, performance, and passengers' confidence in automatic train operations.We're grateful to work with incredible clients.

FAQs

What is the market size of automatic Train Control?

The global automatic train control market is projected to grow from $5 billion in 2023 to a size reflecting a 7.5% CAGR through 2033, driven by advancements in transportation safety and reduced operational costs.

What are the key market players or companies in this automatic Train Control industry?

Key players in the automatic train control industry include companies specializing in railway technology and systems integration, contributing to innovations in train operations and safety enhancements.

What are the primary factors driving the growth in the automatic Train Control industry?

Key drivers of growth in the automatic train control market include rising urbanization, increasing demand for safety standards in rail transportation, and government investments in infrastructure modernization.

Which region is the fastest Growing in the automatic Train Control?

North America is the fastest-growing region for automatic train control, expanding from $1.78 billion in 2023 to $3.75 billion in 2033, highlighting significant investments in rail infrastructure.

Does ConsaInsights provide customized market report data for the automatic Train Control industry?

Yes, ConsaInsights offers customized market report data for the automatic train control industry, tailored to meet specific business needs and strategic objectives.

What deliverables can I expect from this automatic Train Control market research project?

Deliverables include comprehensive reports featuring regional market analyses, growth forecasts, key player insights, and detailed segmentation data for informed strategic decision-making.

What are the market trends of automatic Train Control?

Current market trends include increased adoption of digital signaling solutions, integration of AI and IoT technologies, and a rising focus on sustainability in rail transport systems.