Automotive Display Market Report

First published: 27 September 2024 | Last updated: 02 February 2026 | Report Code: automotive-display

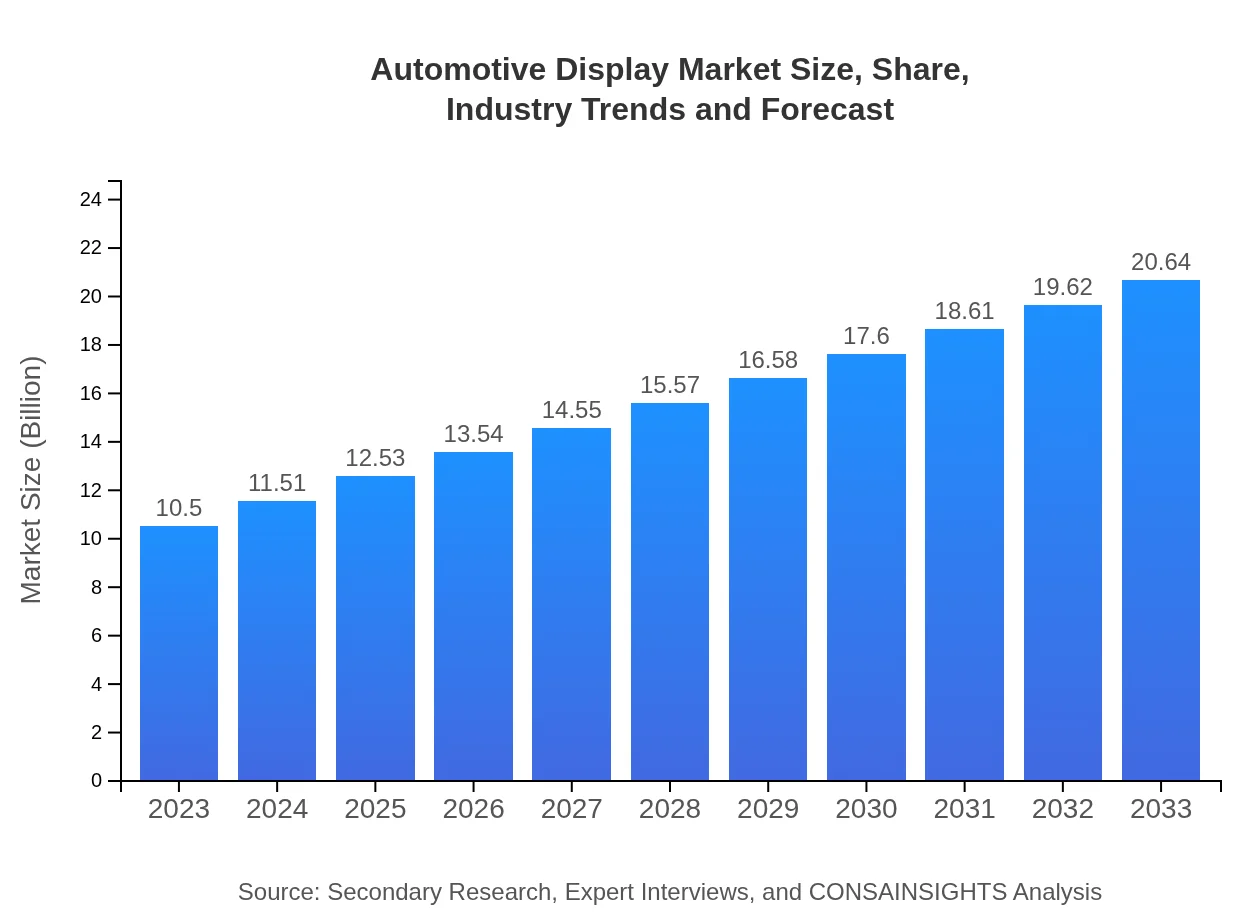

Automotive Display Market — USD 10.5 billion in 2023, Growing to USD 20.64B by 2033 at 6.8% CAGR

This report provides a comprehensive analysis of the Automotive Display market, highlighting key insights and data trends from 2023 to 2033. It aims to offer valuable information on market size, segmentation, regional performance, and future forecasts.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $10.50 Billion |

| CAGR (2023-2033) | 6.8% |

| 2033 Market Size | $20.64 Billion |

| Top Companies | Robert Bosch GmbH, Continental AG, Denso Corporation, LG Display Co., Ltd., Panasonic Corporation |

| Published Date | 27 September 2024 |

| Last Modified Date | 02 February 2026 |

Automotive Display Market Overview

Customize Automotive Display Market Report market research report

- ✔ Get in-depth analysis of Automotive Display market size, growth, and forecasts.

- ✔ Understand Automotive Display's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Automotive Display

What is the Market Size & CAGR of Automotive Display market in 2023?

Automotive Display Industry Analysis

Automotive Display Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Automotive Display Market Analysis Report by Region

Europe Automotive Display Market Report:

The European Automotive Display market is projected to increase from USD 2.89 billion in 2023 to USD 5.68 billion by 2033. European manufacturers are at the forefront of developing advanced infotainment systems and are significantly investing in electric vehicle technologies.Asia Pacific Automotive Display Market Report:

The Asia Pacific region is anticipated to dominate the Automotive Display market driven by significant automotive production, particularly in countries like China, Japan, and South Korea. The market in this region was valued at approximately USD 2.20 billion in 2023 and is expected to grow to USD 4.33 billion by 2033. The growing middle-class population and increased disposable income are contributing to the demand for advanced vehicle technologies.North America Automotive Display Market Report:

In North America, the market is projected to grow from USD 3.50 billion in 2023 to USD 6.89 billion in 2033. The region is known for its advanced technological adoption and stringent safety regulations, which drive demand for sophisticated display systems.South America Automotive Display Market Report:

The South American Automotive Display market remains comparatively smaller, valued at USD 0.94 billion in 2023 with a forecasted growth to USD 1.86 billion by 2033. The growth in this region is expected to come from increased vehicle production and the introduction of new automotive technologies.Middle East & Africa Automotive Display Market Report:

The market in the Middle East and Africa is expected to grow from USD 0.96 billion in 2023 to USD 1.89 billion by 2033. The increasing demand for luxury vehicles equipped with cutting-edge technology is driving market growth in this region.Tell us your focus area and get a customized research report.

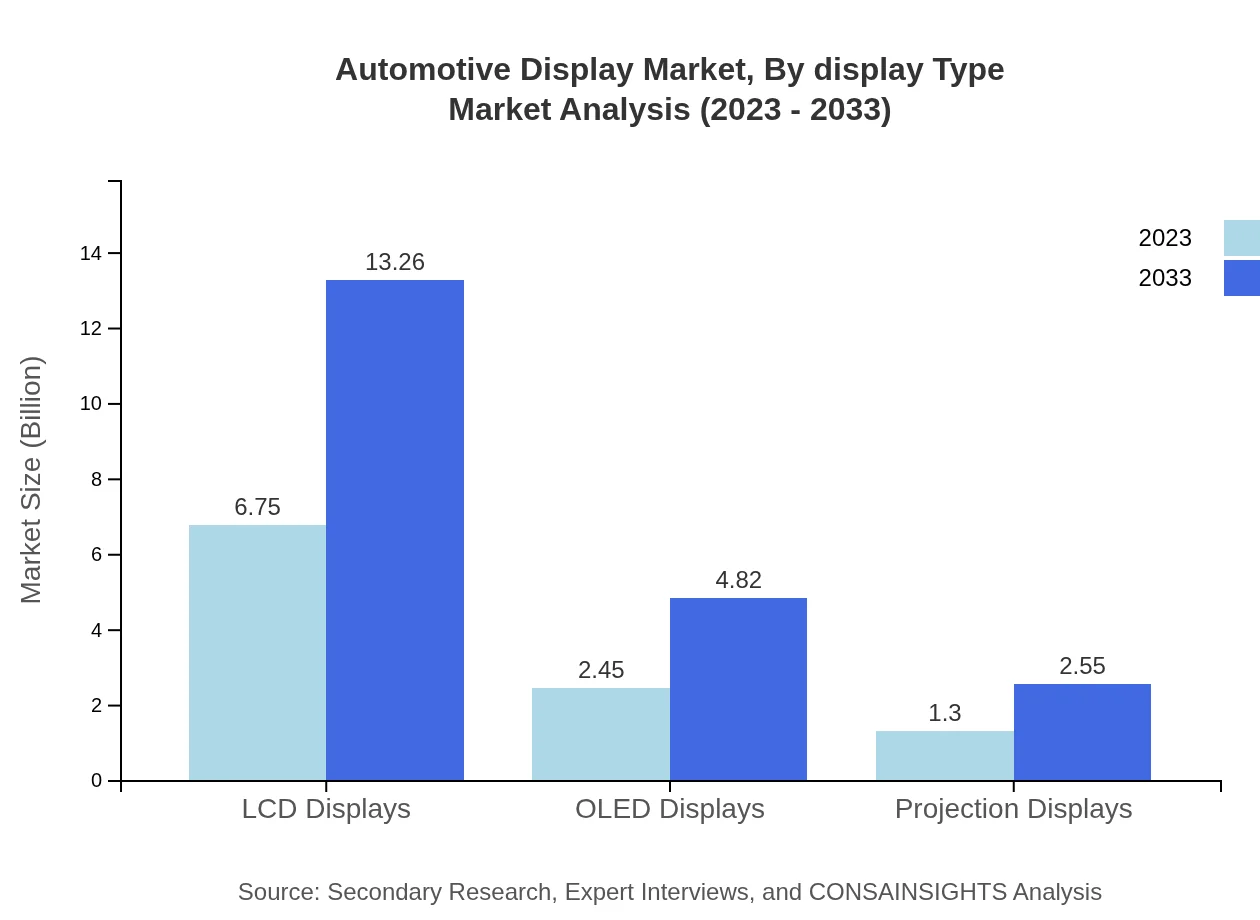

Automotive Display Market Analysis By Display Type

In terms of display type, LCD displays dominate the Automotive Display market with a size of USD 6.75 billion in 2023, projected to grow to USD 13.26 billion by 2033. OLED displays follow, with growth expectations from USD 2.45 billion in 2023 to USD 4.82 billion by 2033. Head-up displays also show significant potential growth fueled by the increasing trend of augmented reality in vehicles.

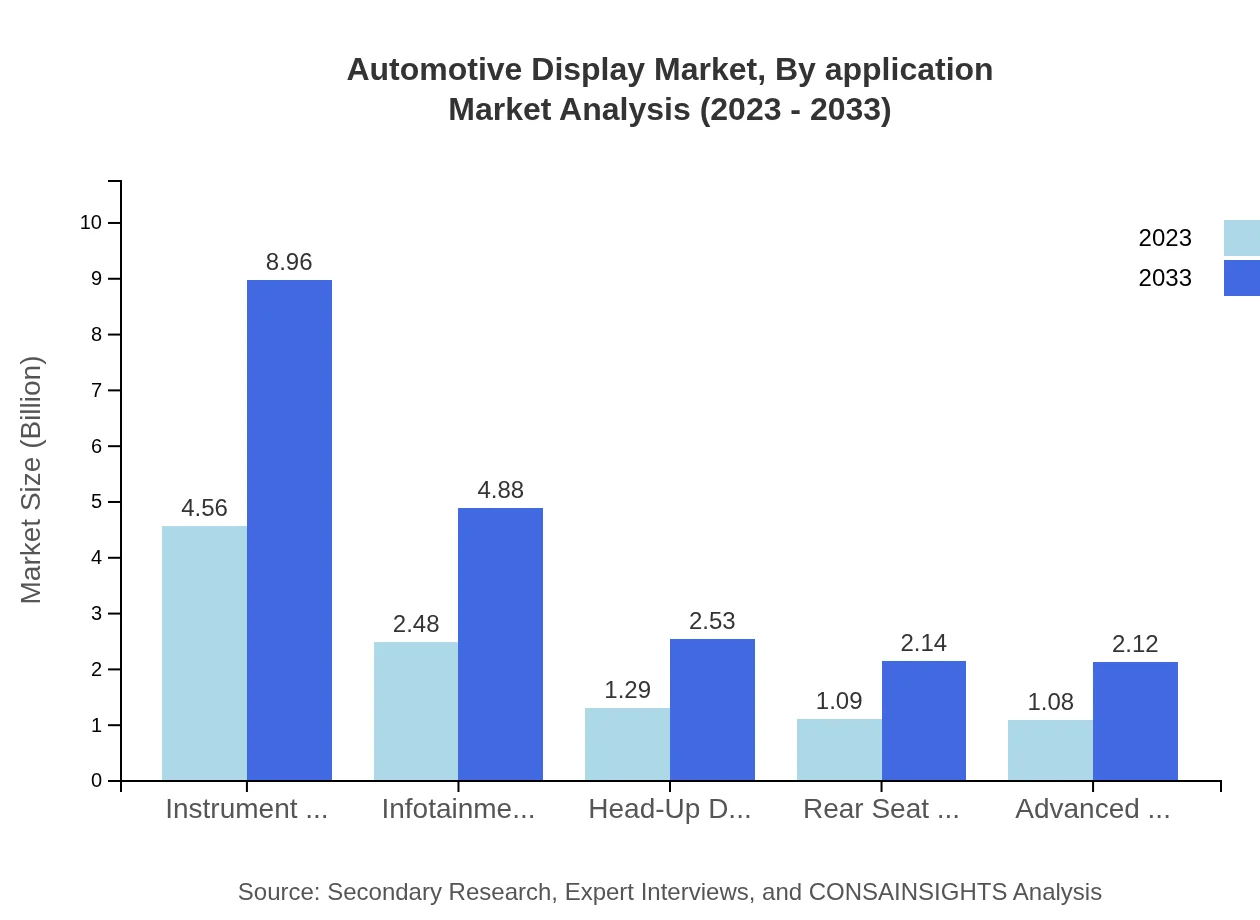

Automotive Display Market Analysis By Application

The application segment highlights infotainment systems and instrument clusters as key categories. Infotainment systems contribute USD 2.48 billion in 2023, expected to reach USD 4.88 billion by 2033, while instrument clusters held a market of USD 4.56 billion in 2023, predicted to grow to USD 8.96 billion by 2033.

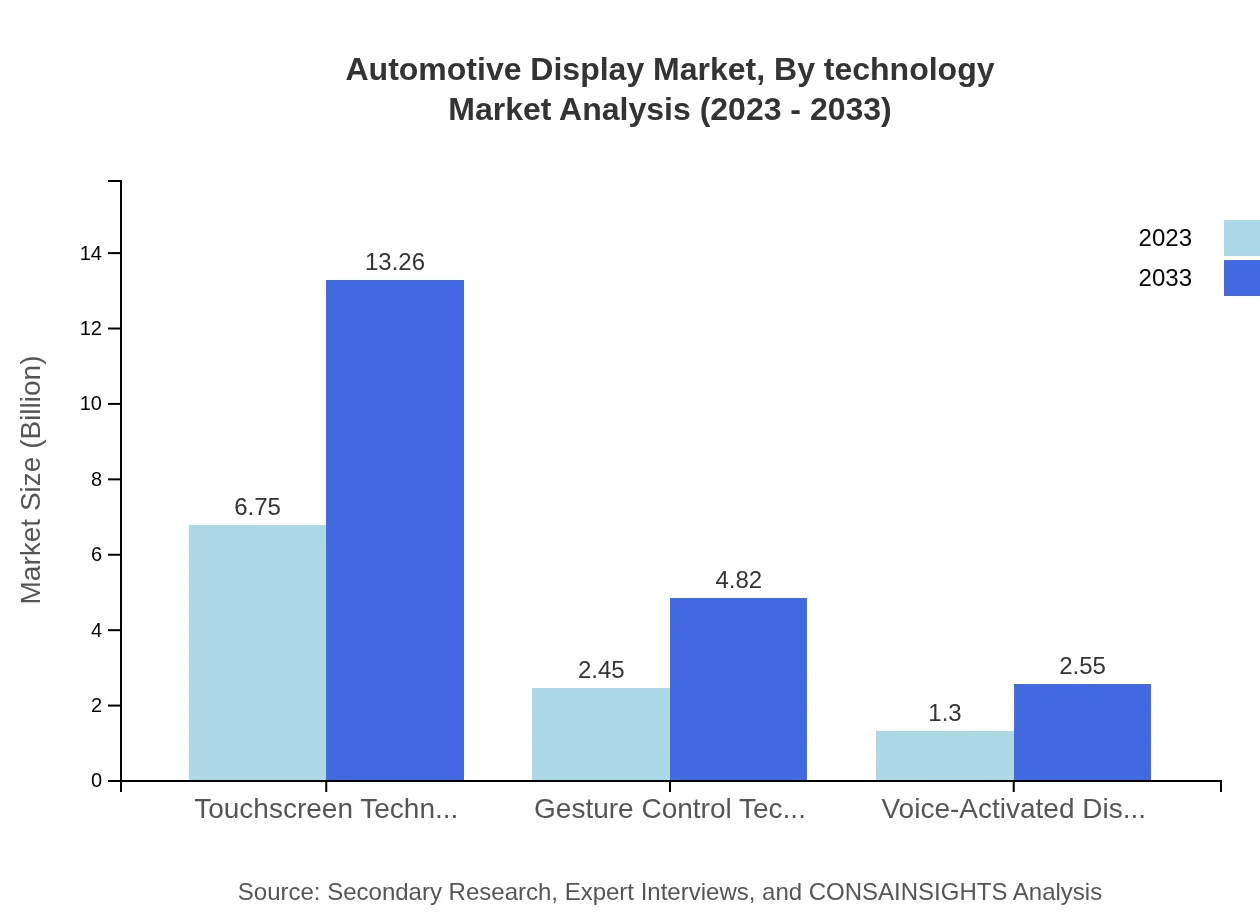

Automotive Display Market Analysis By Technology

Technology-wise, touchscreen technology is expected to maintain its lead with a valuation of USD 6.75 billion in 2023, anticipated to increase to USD 13.26 billion by 2033. Voice-activated displays and gesture control technologies are also gaining momentum, with notable growth rates.

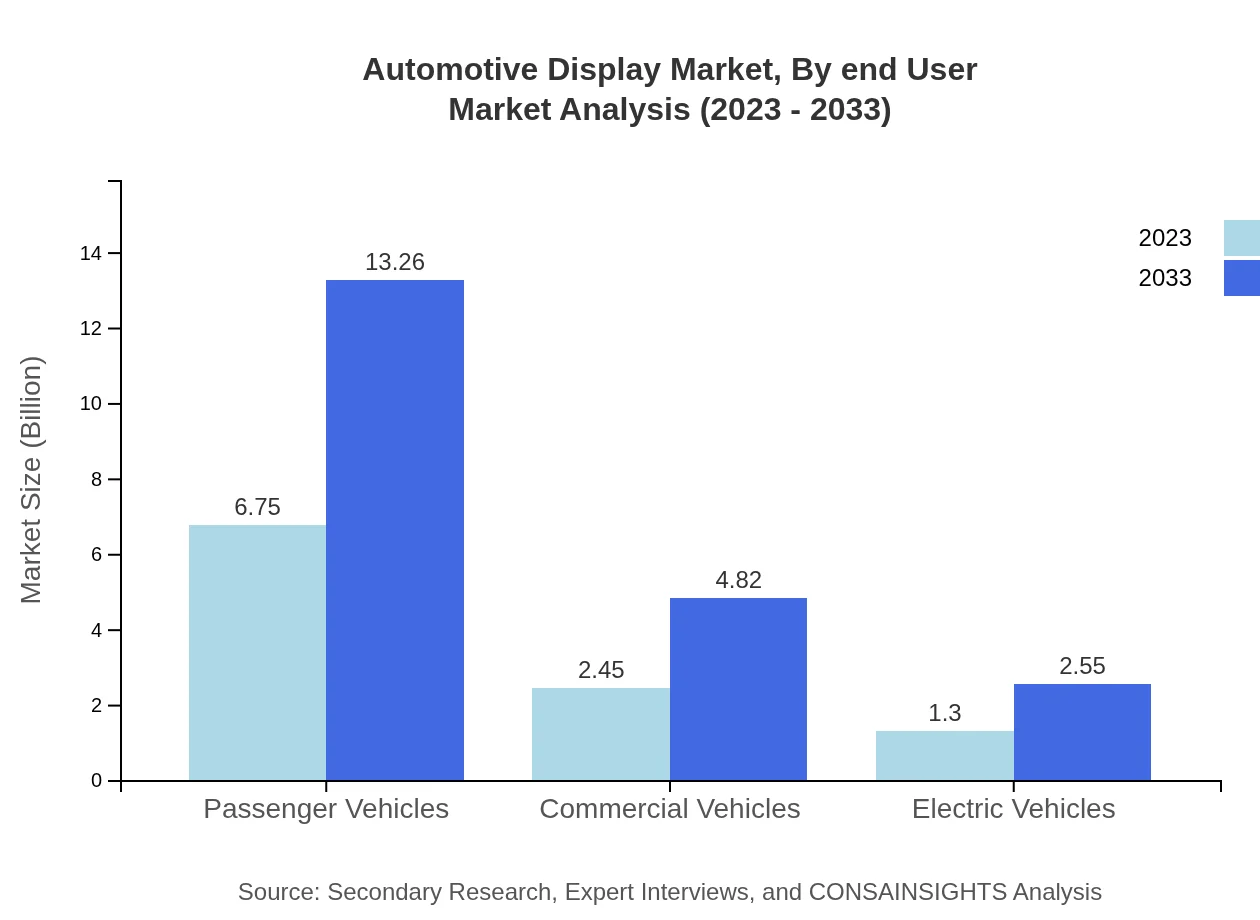

Automotive Display Market Analysis By End User

Passenger vehicles hold the largest market share, contributing USD 6.75 billion in 2023 and expected to grow to USD 13.26 billion by 2033. Commercial vehicles and electric vehicles also represent important segments, with steady growth predicted in line with advancements in automotive technology.

Automotive Display Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Automotive Display Industry

Robert Bosch GmbH:

A leading global supplier of technology and services, Bosch is at the forefront of automotive display systems, offering integrated solutions for both driver interfaces and infotainment systems.Continental AG:

Continental specializes in automotive technology and is known for its pioneering work in display systems, particularly in developing driver assistance and infotainment solutions.Denso Corporation:

One of the largest automotive suppliers worldwide, Denso focuses on developing advanced cockpit technologies, aiming at enhancing driver safety and overall user experience.LG Display Co., Ltd.:

A key player in the display technology sector, LG is instrumental in pushing the boundaries of OLED and LCD technology for automotive applications.Panasonic Corporation:

Panasonic is known for its innovative automotive infotainment systems and has made significant contributions to the Automotive Display market, particularly in electric vehicles.We're grateful to work with incredible clients.

FAQs

What is the market size of automotive display?

The automotive display market is valued at approximately $10.5 billion in 2023, with a projected growth at a CAGR of 6.8%. By 2033, the market is expected to expand significantly, reflecting the industry's evolving landscape.

What are the key market players or companies in the automotive display industry?

Key players in the automotive display market include leading technology firms and automotive manufacturers committed to digital innovation. Major companies are focusing on enhancing user experience through advanced display technology, contributing significantly to market dynamics.

What are the primary factors driving the growth in the automotive display industry?

The automotive display market is driven by increased demand for advanced infotainment systems, strict safety regulations necessitating vehicle technology upgrades, and the growing trend towards electric vehicles. Consumer preferences for enhanced digital interfaces also play a crucial role.

Which region is the fastest Growing in the automotive display?

Asia Pacific is currently the fastest-growing region in the automotive display market, expected to grow from $2.20 billion in 2023 to $4.33 billion by 2033. Other significant regions include Europe and North America, each showing robust growth trends.

Does ConsaInsights provide customized market report data for the automotive display industry?

Yes, ConsaInsights offers customized market report data for the automotive display industry, tailoring insights to meet specific client needs. This allows companies to make informed business decisions based on nuanced market trends and projections.

What deliverables can I expect from this automotive display market research project?

Deliverables from the automotive display market research will include detailed reports, data analytics, market forecasts, and competitive landscape assessments. Clients will receive comprehensive insights tailored to understand market dynamics and strategic opportunities.

What are the market trends of automotive display?

Key market trends include the rising adoption of touchscreen technology and voice-activated displays, along with the growing preference for OLED displays in vehicles. Additionally, there is a steady shift towards integrating augmented reality in automotive displays to enhance user engagement.