Cancer Registry Software Market Report

First published: 10 October 2024 | Last updated: 25 May 2026 | Report Code: cancer-registry-software

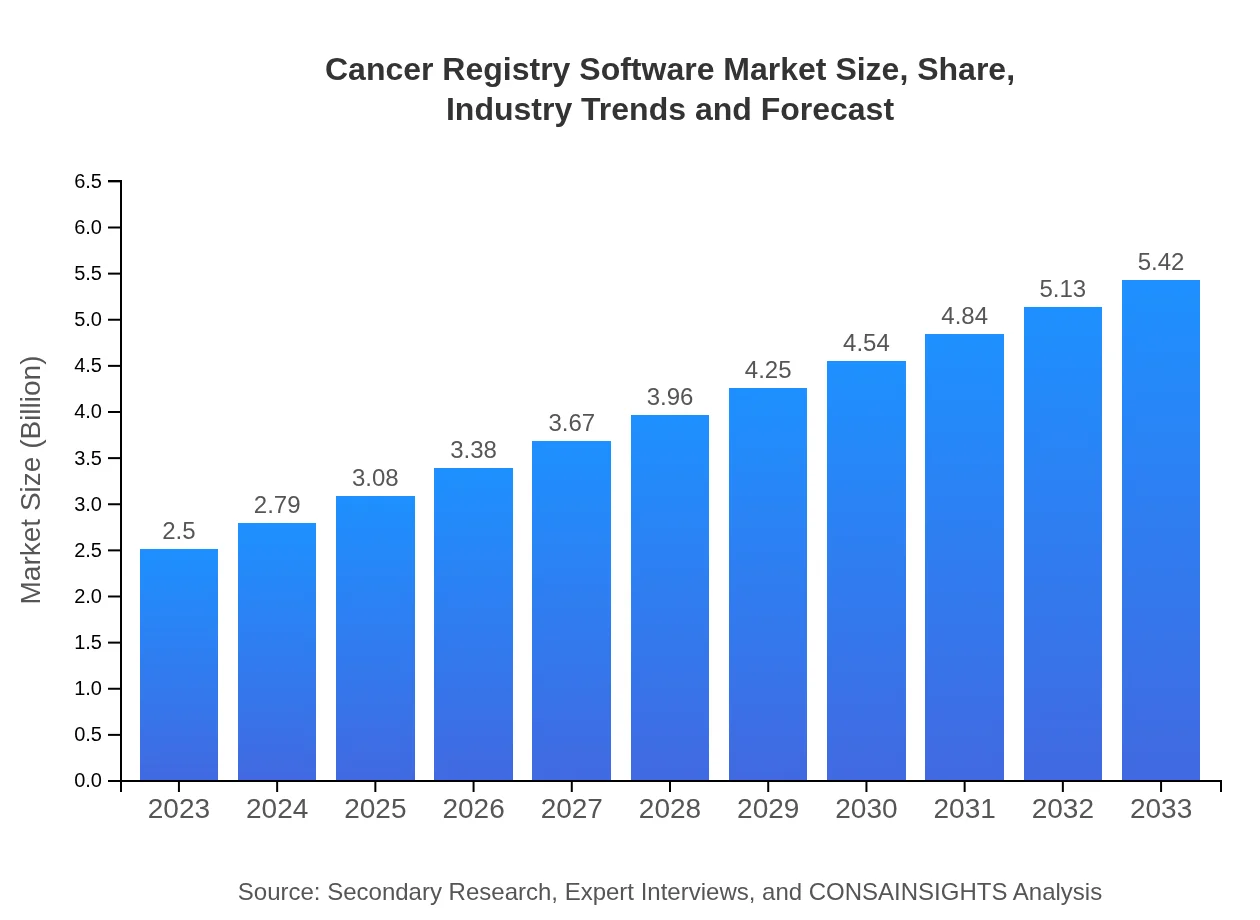

Cancer Registry Software Market — USD 2.5 billion in 2023, Growing to USD 5.42B by 2033 at 7.8% CAGR

This report provides an in-depth analysis of the Cancer Registry Software market from 2023 to 2033, covering market size, growth trends, regional insights, competitive landscape, and emerging technologies that are shaping the industry.

Key Takeaways

- Global market value rises from $2.50 Billion in 2023 to $5.42 Billion in 2033 at a 7.8% CAGR.

- North America is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- Europe moves from $0.67 Billion to $1.45 Billion over the forecast period, reflecting steady digital adoption.

- Asia Pacific grows from $0.50 Billion in 2023 to $1.08 Billion in 2033 amid rising healthcare digitization.

- Key vendors include Cerner Corporation, McKesson Corporation, Epic Systems Corporation, IBM Watson Health, and Allscripts Healthcare Solutions.

Cancer Registry Software Market Report — Executive Summary

North America remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. The Cancer Registry Software Market Report details a projected increase from $2.50 Billion in 2023 to $5.42 Billion in 2033 at a 7.8% CAGR. Growth is driven by expanding need for structured cancer data, regulatory compliance, and digital transformation across healthcare. Regions show varied expansions: North America leads in absolute value, while Europe and Asia Pacific also record notable gains. Product and deployment categories include software, services, cloud-based and on-premises options. Vendors such as Cerner Corporation, McKesson Corporation, Epic Systems Corporation, IBM Watson Health, and Allscripts Healthcare Solutions are active, focusing on analytics, interoperability, and AI-enabled features to support reporting, research, and clinical decision-making.

Key Growth Drivers

- Rising demand for accurate cancer data to support treatment outcomes and research initiatives.

- Healthcare digitalization and EMR integration increasing adoption of registry software.

- Regulatory and reporting requirements prompting investment in compliant data management solutions.

- Development of analytics, interoperability, and AI features enhancing registry capabilities.

- Growing institutional focus on data-driven public health and clinical research applications.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $2.50 Billion |

| CAGR (2023-2033) | 7.8% |

| 2033 Market Size | $5.42 Billion |

| Top Companies | Cerner Corporation, McKesson Corporation, Epic Systems Corporation, IBM Watson Health, Allscripts Healthcare Solutions |

| Published Date | 10 October 2024 |

| Last Modified Date | 25 May 2026 |

Cancer Registry Software Market Overview

Customize Cancer Registry Software Market Report market research report

- ✔ Get in-depth analysis of Cancer Registry Software market size, growth, and forecasts.

- ✔ Understand Cancer Registry Software's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Cancer Registry Software

What is the Market Size & CAGR of Cancer Registry Software Market Report market in 2023?

Cancer Registry Software Industry Analysis

Cancer Registry Software Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Cancer Registry Software Market Report Market Analysis Report by Region

Europe Cancer Registry Software Market Report:

Europe grows from $0.67 Billion in 2023 to $1.45 Billion in 2033. Expansion is linked to regulatory reporting needs, rising adoption of digital health solutions, and collaborative research programs that rely on high-quality cancer data.Asia Pacific Cancer Registry Software Market Report:

Asia Pacific grows from $0.5 Billion in 2023 to $1.08 Billion in 2033. Growth is driven by accelerating healthcare digitalization, increasing cancer awareness, and investments in data infrastructure to support clinical registries and research.North America Cancer Registry Software Market Report:

North America is largest regional market, rising from $0.91 Billion in 2023 to $1.98 Billion in 2033. Regional expansion reflects strong healthcare IT investments, integration with electronic health records, and institutional emphasis on registry-driven research and compliance.South America Cancer Registry Software Market Report:

Latin America grows from $0.2 Billion in 2023 to $0.44 Billion in 2033. Momentum reflects growing prioritization of health data systems, enhanced reporting requirements, and gradual uptake of registry solutions by hospitals and research centers.Middle East & Africa Cancer Registry Software Market Report:

Middle East and Africa grows from $0.21 Billion in 2023 to $0.46 Billion in 2033. Expansion is associated with improving healthcare IT adoption, regulatory modernization, and growing use of registries for public health surveillance and clinical research.Tell us your focus area and get a customized research report.

Research Methodology

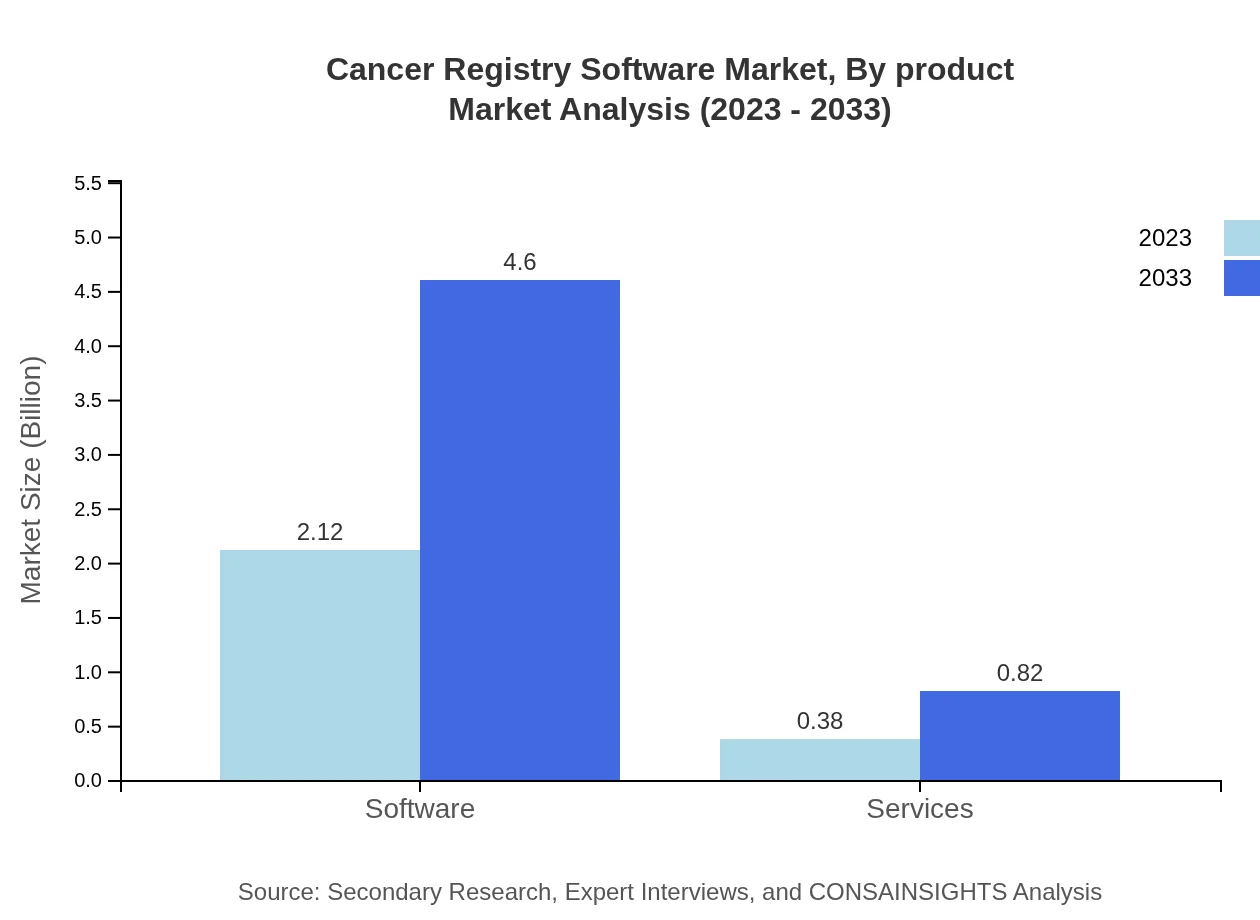

Cancer Registry Software Market Analysis By Product

The Cancer Registry Software market is predominantly categorized into software solutions and services. The software segment is leading the market with a size of $2.12 billion in 2023, projected to grow to $4.60 billion by 2033, consistently holding an 84.79% market share. In contrast, the services segment, valued at $0.38 billion in 2023, is expected to see growth to $0.82 billion by 2033, corresponding to a market share of 15.21%.

Cancer Registry Software Market Analysis By Application

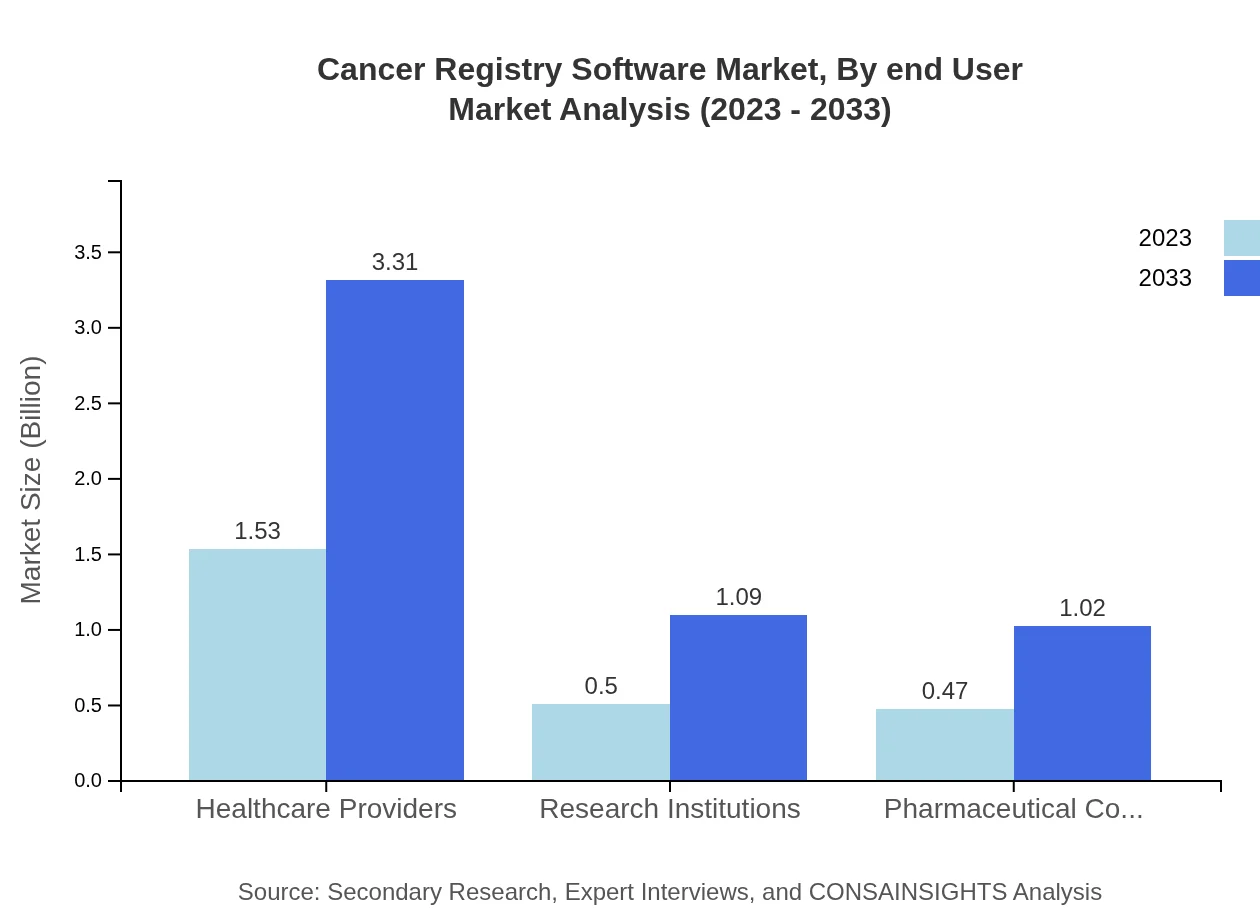

The market is segmented by application into healthcare providers, research institutions, pharmaceutical companies, and government agencies. The healthcare providers segment holds the largest share, valued at $1.53 billion in 2023 and expected to grow to $3.31 billion by 2033, representing 61.02% of the market. Research institutions and pharmaceutical companies also contribute significantly, with sizes of $0.50 billion and $0.47 billion in 2023, respectively.

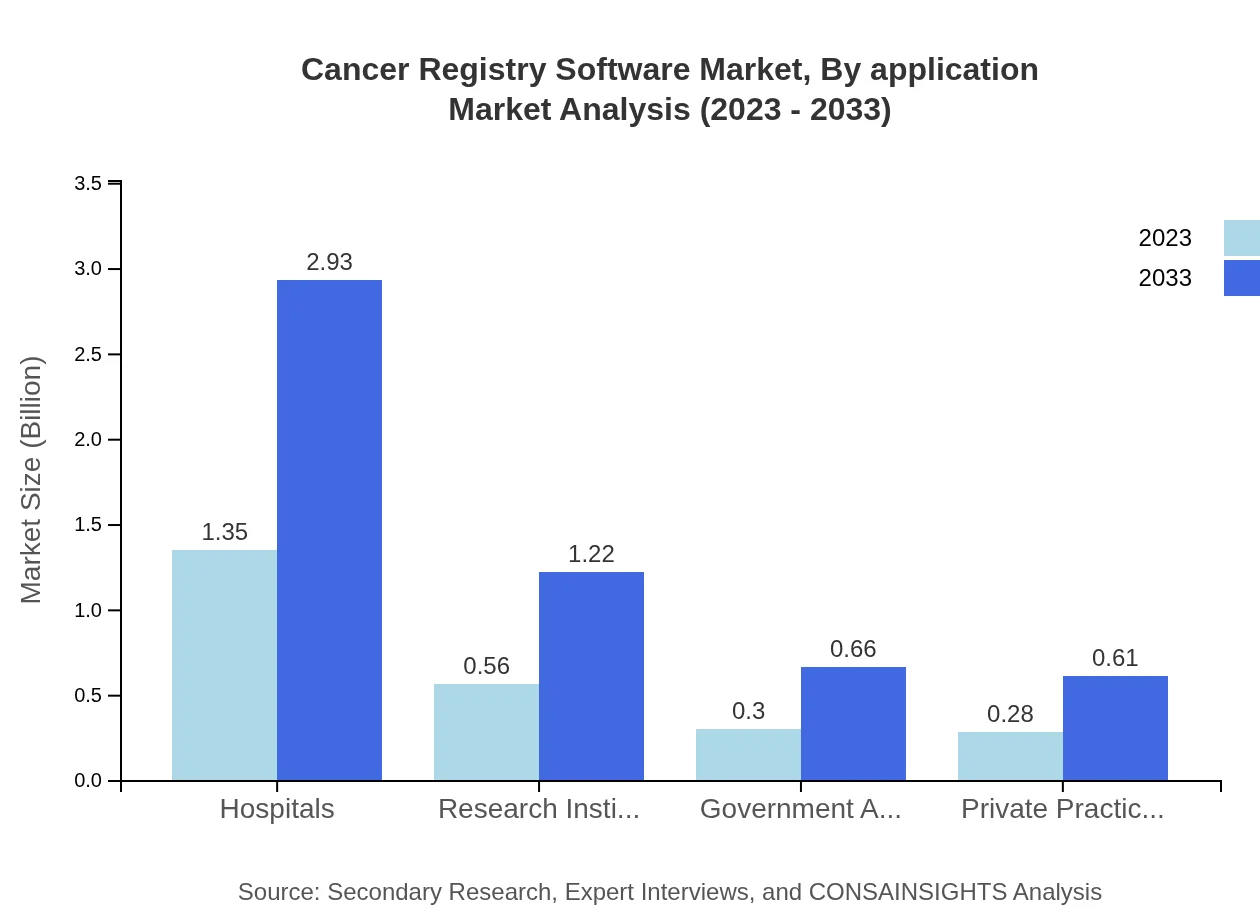

Cancer Registry Software Market Analysis By End User

End-users of the Cancer Registry Software include hospitals, research institutes, government agencies, and private practices. Hospitals lead with a market size of $1.35 billion in 2023, projected to grow to $2.93 billion by 2033, accounting for 54.14% of the market share. Research institutes are also key players, with market sizes anticipated to grow from $0.56 billion to $1.22 billion in the same period.

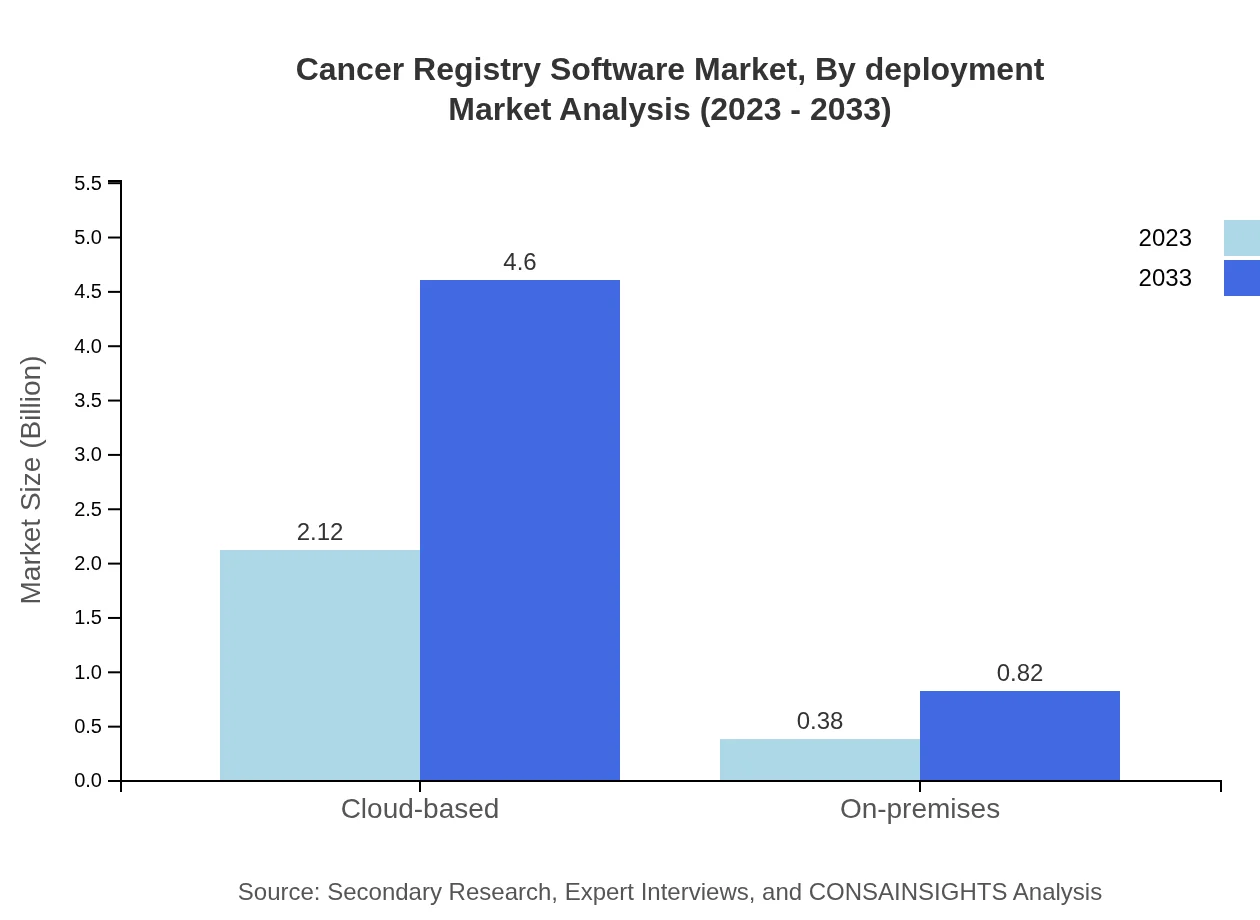

Cancer Registry Software Market Analysis By Deployment

In terms of deployment, the Cancer Registry Software market is categorized into cloud-based and on-premises solutions. The cloud-based segment leads the market, valued at $2.12 billion in 2023 and expected to grow to $4.60 billion by 2033, holding 84.79% of the market share. Meanwhile, on-premises solutions start at $0.38 billion and are forecasted to reach $0.82 billion, holding a 15.21% share.

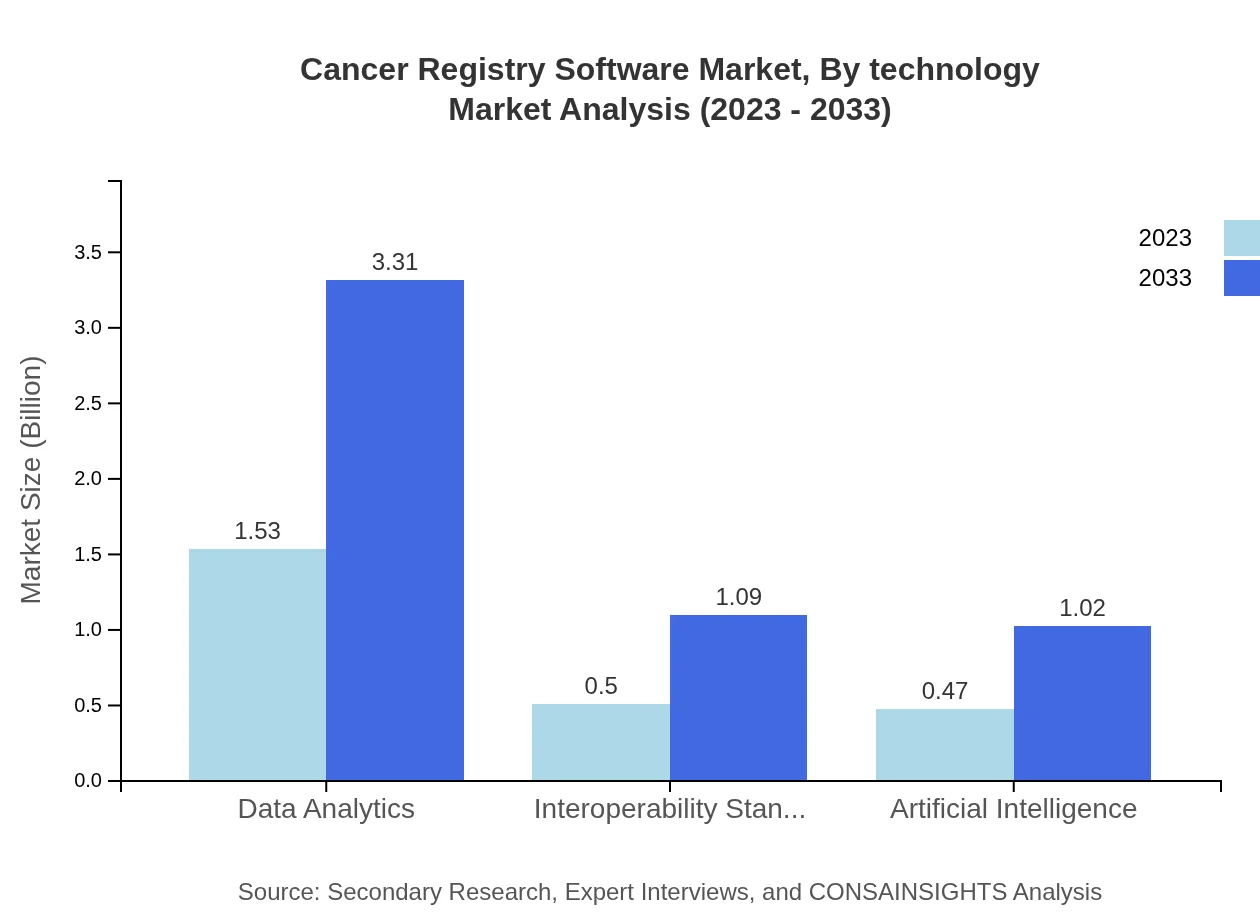

Cancer Registry Software Market Analysis By Technology

The technological advancements in the Cancer Registry Software market are evident in the segments of data analytics, interoperability standards, and artificial intelligence. Data analytics tools are projected to grow from $1.53 billion in 2023 to $3.31 billion by 2033, with a share of 61.02%. Similarly, interoperability standards and AI capabilities are crucial for the integration of cancer registries with other healthcare systems, with projected sizes of $0.50 billion and $0.47 billion respectively by 2033.

Cancer Registry Software Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Cancer Registry Software Industry

Cerner Corporation:

Cerner provides healthcare solutions, including comprehensive cancer registry software that enhances data management and improves patient outcomes.McKesson Corporation:

McKesson offers innovative solutions that streamline cancer data collection and reporting, emphasizing patient safety and treatment efficacy.Epic Systems Corporation:

Epic's software solutions are widely used for managing cancer registries, focusing on ease of access and integration with existing healthcare systems.IBM Watson Health:

IBM Watson Health utilizes AI-driven analytics to enhance the insights gained from cancer registries, supporting healthcare providers in delivering optimal patient care.Allscripts Healthcare Solutions:

Allscripts delivers interoperable cancer registry software that supports data sharing and compliance with health regulations.We're grateful to work with incredible clients.

FAQs

What is the market size of the industry in 2023?

The market size for the industry in 2023 is $2.50 Billion, as reported for the Cancer Registry Software market at the start of the forecast period.

What is the market size projected for 2033?

The market is projected to reach $5.42 Billion by 2033, reflecting growth across regions and increased adoption of digital registry solutions.

What is CAGR for the forecast period?

The reported compound annual growth rate for the forecast period 2023 to 2033 is 7.8%, based on the provided market projections.

Is there a single fastest Growing region in the Cancer Registry Software Market Report market?

No single fastest-growing region is stated for the Cancer Registry Software Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Which companies are leading the vendor landscape?

Top companies noted in the market include Cerner Corporation, McKesson Corporation, Epic Systems Corporation, IBM Watson Health, and Allscripts Healthcare Solutions.

Why are registries gaining importance in healthcare?

Registries support clinical decision-making, research and reporting, enabling better treatment tracking and compliance with regulatory and public health reporting requirements.

How do deployment options vary in the market?

Deployment options include cloud-based and on-premises configurations, allowing organizations to select models that match security, scalability, and integration needs.

What are common technology focuses in product development?

Product development prioritizes data analytics, interoperability standards, and artificial intelligence to improve data insights, exchange, and automated processing within registries.

Who are typical end users of cancer registry software?

Typical end users include healthcare providers, research institutions, and pharmaceutical companies that rely on registry data for care management and research.

What drives adoption in emerging regions?

Adoption in emerging regions is driven by increasing healthcare digitalization, demand for robust patient data, and investments in reporting and research infrastructure.