Fuel Cell Powertrain Market Report

First published: 27 September 2024 | Last updated: 02 February 2026 | Report Code: fuel-cell-powertrain

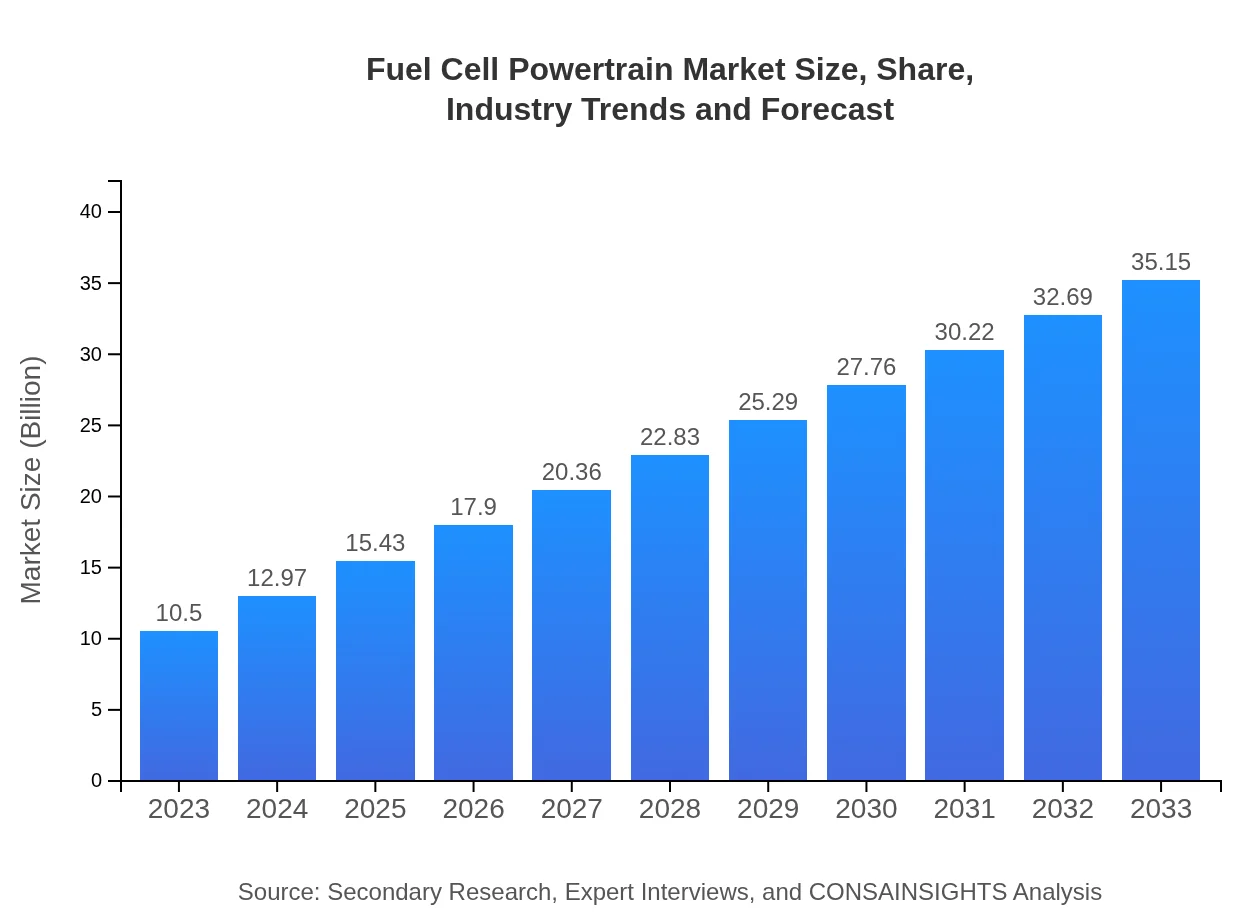

Fuel Cell Powertrain Market — USD 10.5 billion in 2023, Growing to USD 35.15B by 2033 at 12.3% CAGR

This report analyzes the Fuel Cell Powertrain market, offering insights into the market size, growth trends, and competitive landscape from 2023 to 2033.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $10.50 Billion |

| CAGR (2023-2033) | 12.3% |

| 2033 Market Size | $35.15 Billion |

| Top Companies | Ballard Power Systems, Plug Power, Toyota Motor Corporation, Hydrogenics (Cummins Inc.), Bloom Energy |

| Published Date | 27 September 2024 |

| Last Modified Date | 02 February 2026 |

Fuel Cell Powertrain Market Overview

Customize Fuel Cell Powertrain Market Report market research report

- ✔ Get in-depth analysis of Fuel Cell Powertrain market size, growth, and forecasts.

- ✔ Understand Fuel Cell Powertrain's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Fuel Cell Powertrain

What is the Market Size & CAGR of Fuel Cell Powertrain market in 2023?

Fuel Cell Powertrain Industry Analysis

Fuel Cell Powertrain Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Fuel Cell Powertrain Market Analysis Report by Region

Europe Fuel Cell Powertrain Market Report:

Europe's market is projected to grow from $2.76 billion in 2023 to $9.25 billion by 2033, driven by stringent emission regulations and a collective push towards carbon neutrality among EU nations.Asia Pacific Fuel Cell Powertrain Market Report:

In the Asia Pacific region, the Fuel Cell Powertrain market is projected to grow from $2.02 billion in 2023 to $6.76 billion by 2033. Countries like Japan and South Korea are leading the charge with notable advancements in fuel cell technology and significant government investments.North America Fuel Cell Powertrain Market Report:

North America holds a substantial share, with the market size anticipated to expand from $3.66 billion in 2023 to $12.26 billion by 2033. The United States, particularly, is focusing on developing hydrogen infrastructure, enhancing market prospects.South America Fuel Cell Powertrain Market Report:

The Fuel Cell Powertrain market in South America, although smaller, is expected to rise from $0.62 billion in 2023 to $2.08 billion by 2033. Increasing environmental concerns and the push for renewable energy are stimulating growth.Middle East & Africa Fuel Cell Powertrain Market Report:

The Middle East and Africa region is expected to see growth from $1.43 billion to $4.80 billion during the same period, driven by increasing investments in hydrogen production and renewable energy initiatives.Tell us your focus area and get a customized research report.

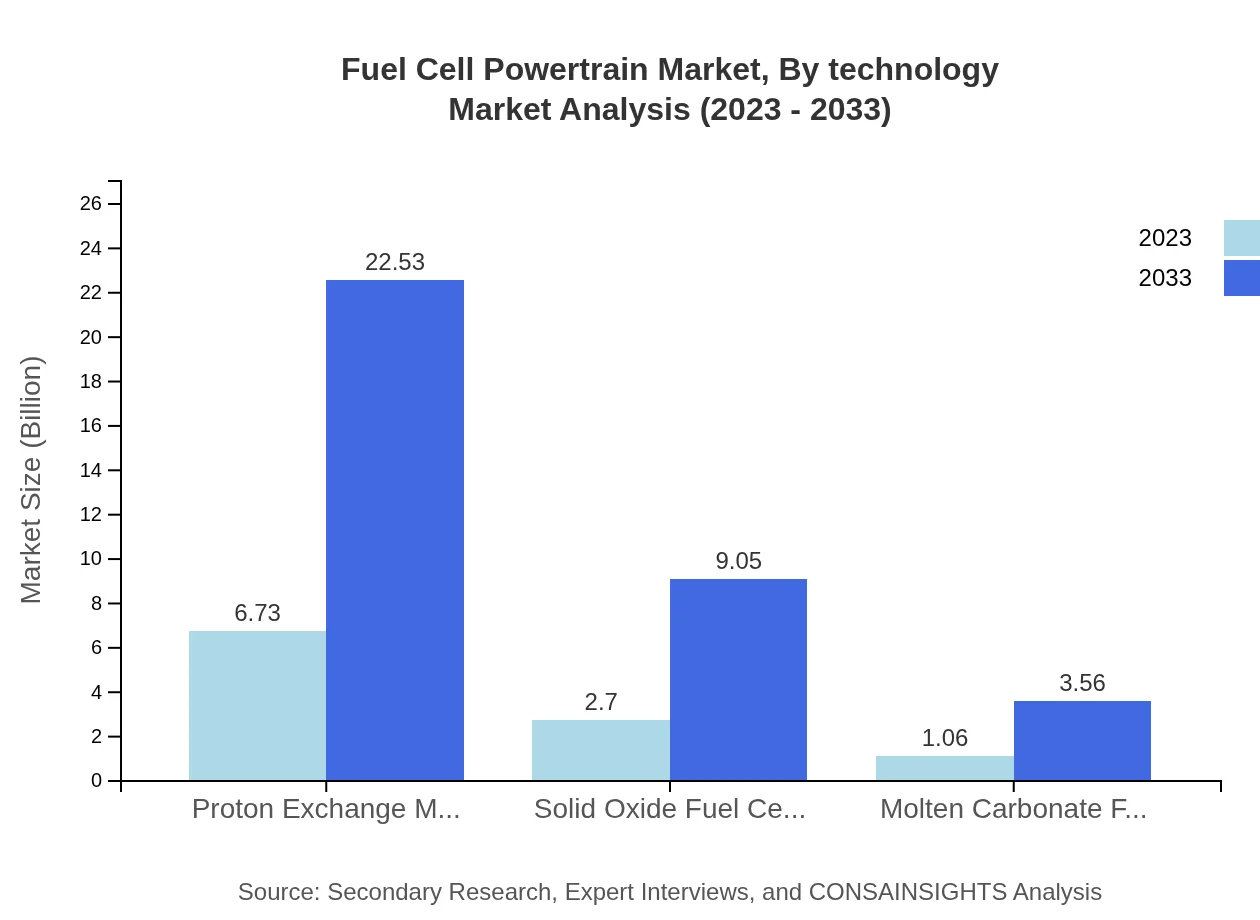

Fuel Cell Powertrain Market Analysis By Technology

The Fuel Cell Powertrain market by technology is predominantly led by Proton Exchange Membrane Fuel Cells (PEMFC), accounting for a market size of $6.73 billion in 2023 and expected to reach $22.53 billion by 2033. Solid Oxide Fuel Cells (SOFC) and Molten Carbonate Fuel Cells (MCFC) are also significant, with SOFC expected to grow from $2.70 billion to $9.05 billion during the same period.

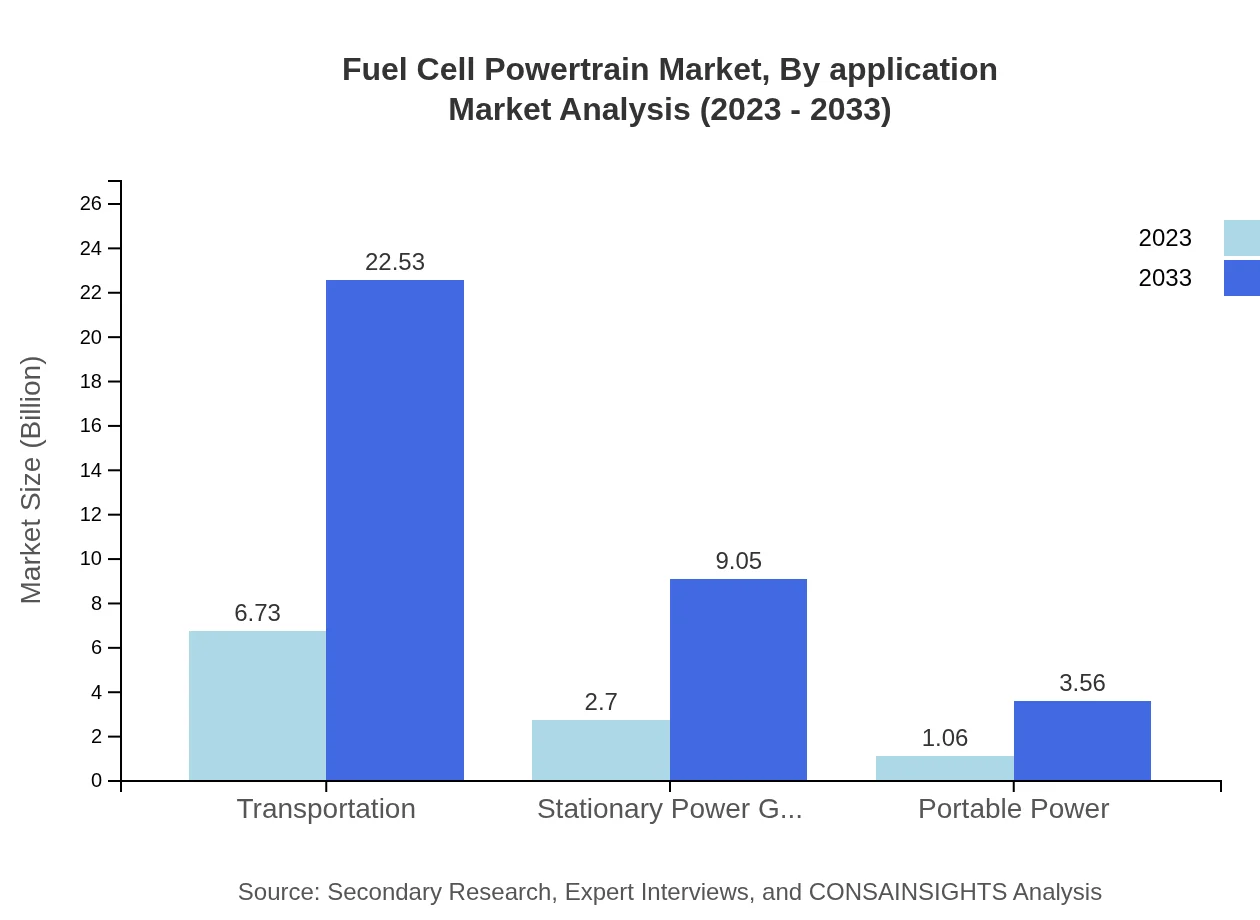

Fuel Cell Powertrain Market Analysis By Application

Transportation leads the application segment, constituting a market size of $6.73 billion in 2023 and anticipated to reach $22.53 billion by 2033. It is followed by industrial applications expected to grow significantly from $2.70 billion to $9.05 billion and utilities which will see an increase from $1.06 billion to $3.56 billion.

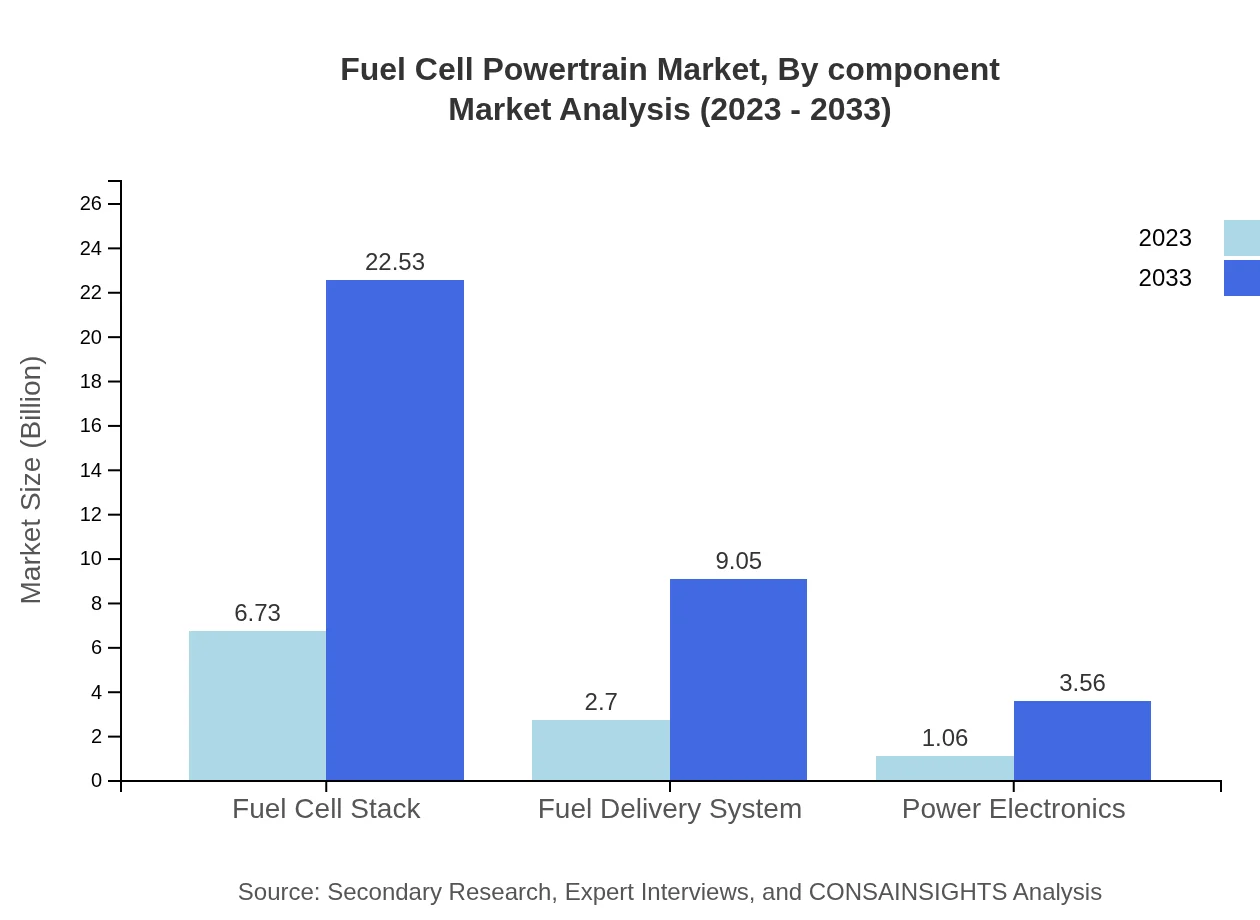

Fuel Cell Powertrain Market Analysis By Component

Components such as Fuel Cell Stacks accounted for a considerable share, with market sizes of $6.73 billion in 2023 reaching $22.53 billion by 2033. Fuel Delivery Systems and Power Electronics are also integral, expected to grow from $2.70 billion to $9.05 billion and from $1.06 billion to $3.56 billion respectively.

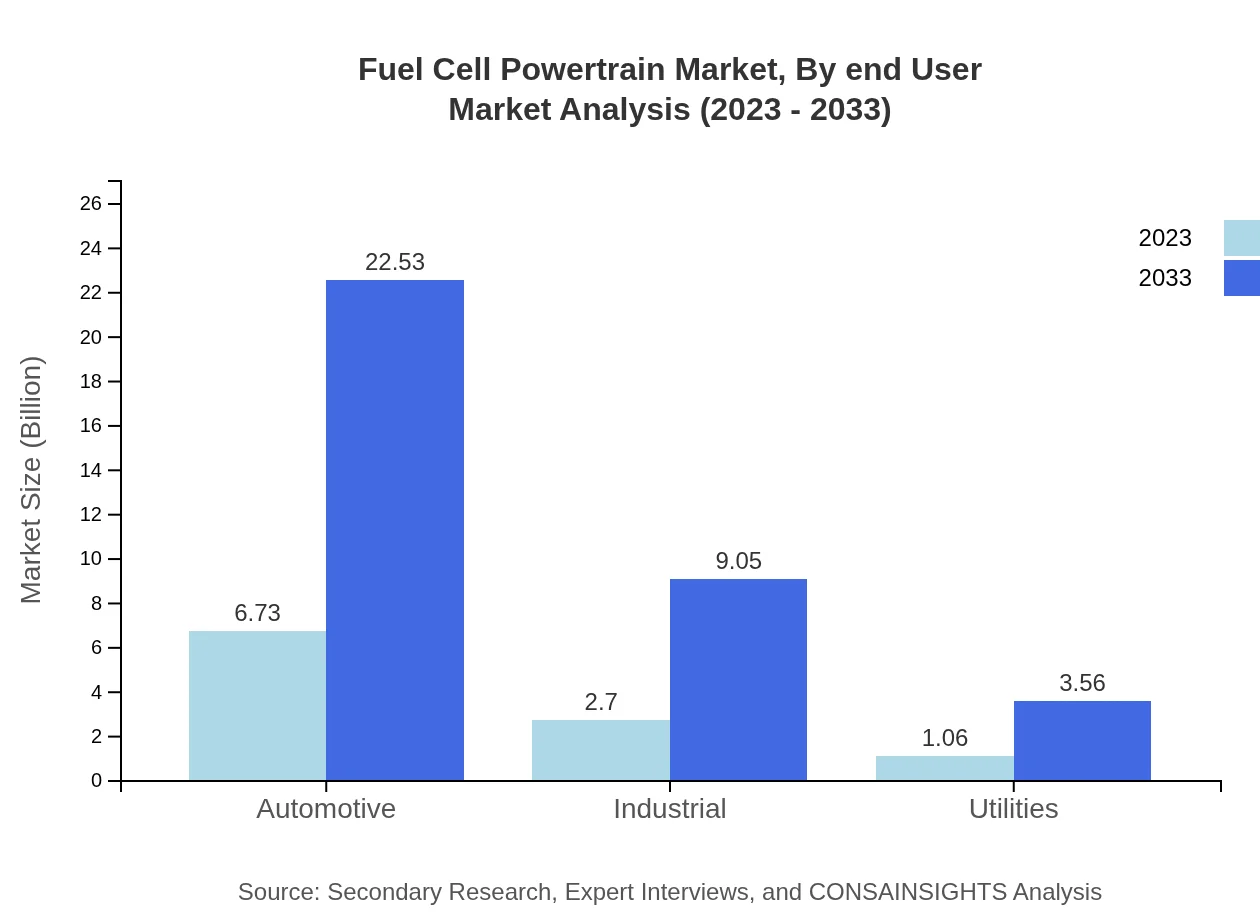

Fuel Cell Powertrain Market Analysis By End User

The end-user segment reflects significant growth, particularly in automotive where the market size is projected to grow from $6.73 billion to $22.53 billion. The industrial segment will also show robust growth, expanding from $2.70 billion to $9.05 billion and utilities from $1.06 billion to $3.56 billion by 2033.

Fuel Cell Powertrain Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Fuel Cell Powertrain Industry

Ballard Power Systems:

A leader in the fuel cell market, Ballard focuses on developing specific fuel cell products for automotive and stationary applications.Plug Power:

Plug Power specializes in alternative energy technology with a focus on hydrogen fuel cell systems for logistics and stationary power applications.Toyota Motor Corporation:

As a pioneer in fuel cell technology in the automotive sector, Toyota continues to invest heavily in hydrogen-powered vehicles and infrastructure development.Hydrogenics (Cummins Inc.):

Hydrogenics is a provider of hydrogen generation and fuel cell products while being heavily involved in hydrogen generation and fueling stations.Bloom Energy:

Bloom Energy is known for its solid oxide fuel cells, providing clean and reliable energy solutions for various industries.We're grateful to work with incredible clients.

FAQs

What is the market size of fuel Cell Powertrain?

The global Fuel Cell Powertrain market was valued at $10.5 billion in 2023, with a projected CAGR of 12.3% over the next decade. By 2033, the market is expected to expand significantly, reflecting the increasing demand for clean energy solutions.

What are the key market players or companies in this fuel Cell Powertrain industry?

Key players in the fuel cell powertrain industry include companies like Toyota, Hyundai, Ballard Power Systems, Plug Power, and Panasonic. These companies are instrumental in driving innovation and capturing market share through advanced technologies and strategic partnerships.

What are the primary factors driving the growth in the fuel Cell Powertrain industry?

Factors driving the fuel cell powertrain market include escalating demand for sustainable transportation solutions, government support for clean energy initiatives, advancements in hydrogen production technologies, and growing investment in fuel cell research and development.

Which region is the fastest Growing in the fuel Cell Powertrain?

The Asia Pacific region is the fastest-growing market for fuel cell powertrains, projected to grow from $2.02 billion in 2023 to $6.76 billion by 2033. This growth is driven by increased adoption of fuel cell vehicles and supportive government policies.

Does ConsaInsights provide customized market report data for the fuel Cell Powertrain industry?

Yes, ConsaInsights offers customized market report data tailored to specific needs within the fuel cell powertrain industry. Clients can gain insights into market trends, forecasts, and competitive landscapes according to their requirements.

What deliverables can I expect from this fuel Cell Powertrain market research project?

Deliverables from the fuel-cell-powertrain market research project include detailed market analysis reports, competitive landscape assessments, regional market insights, and forecasts by various segments, allowing clients to make informed business decisions.

What are the market trends of fuel Cell Powertrain?

Current trends in the fuel cell powertrain market include increasing investments in hydrogen infrastructure, a shift toward electrification of transportation, rising environmental regulations, and a focus on developing cost-effective fuel cells for broader industrial applications.