Industrial Safety Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: industrial-safety

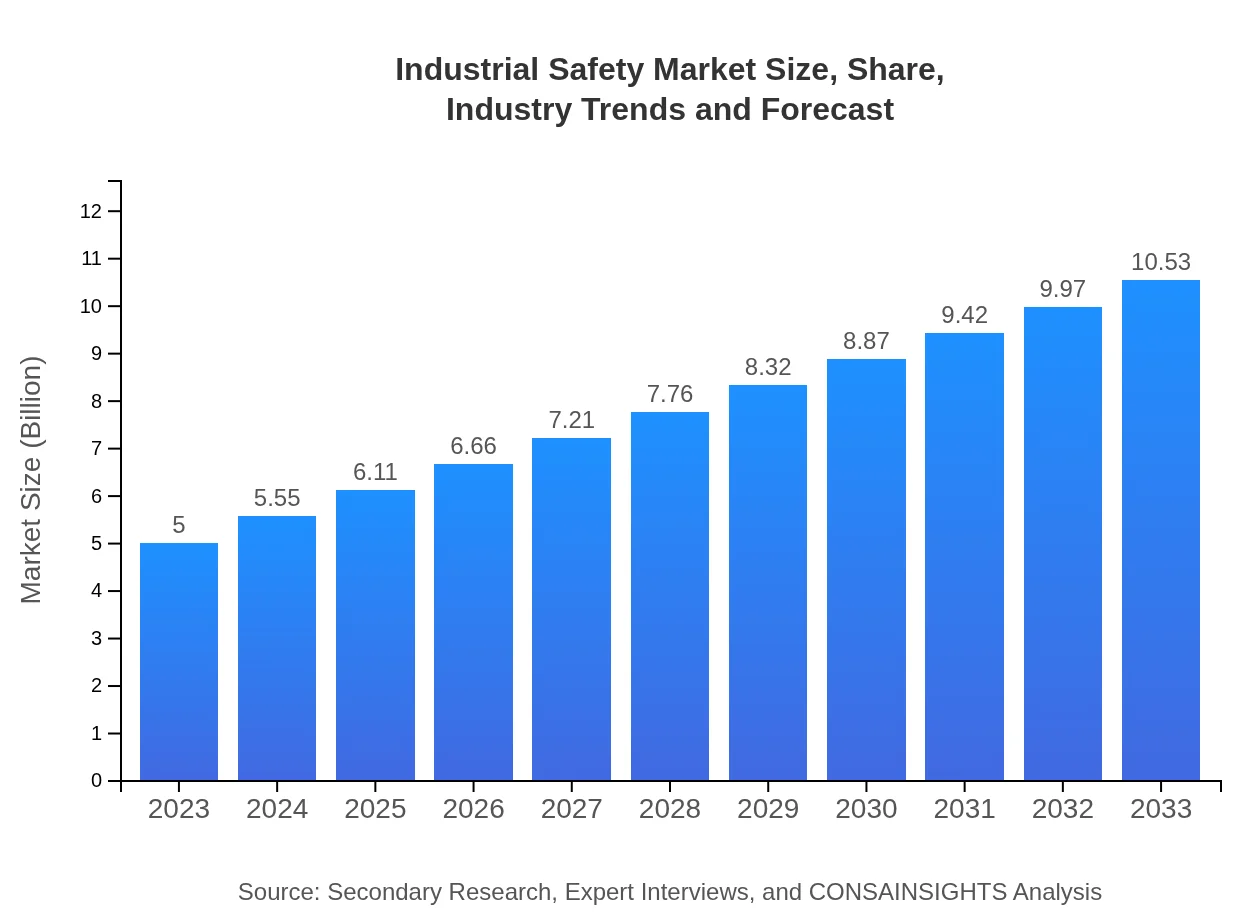

Industrial Safety Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides a comprehensive analysis of the Industrial Safety market from 2023 to 2033. It includes insights on market size, trends, segmentation, regional analysis, and key players in the industry, aiming to equip stakeholders with essential data for informed decision-making.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Honeywell , 3M, DuPont, MSA Safety |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Industrial Safety Market Overview

Customize Industrial Safety Market Report market research report

- ✔ Get in-depth analysis of Industrial Safety market size, growth, and forecasts.

- ✔ Understand Industrial Safety's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Industrial Safety

What is the Market Size & CAGR of Industrial Safety market in 2023?

Industrial Safety Industry Analysis

Industrial Safety Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Industrial Safety Market Analysis Report by Region

Europe Industrial Safety Market Report:

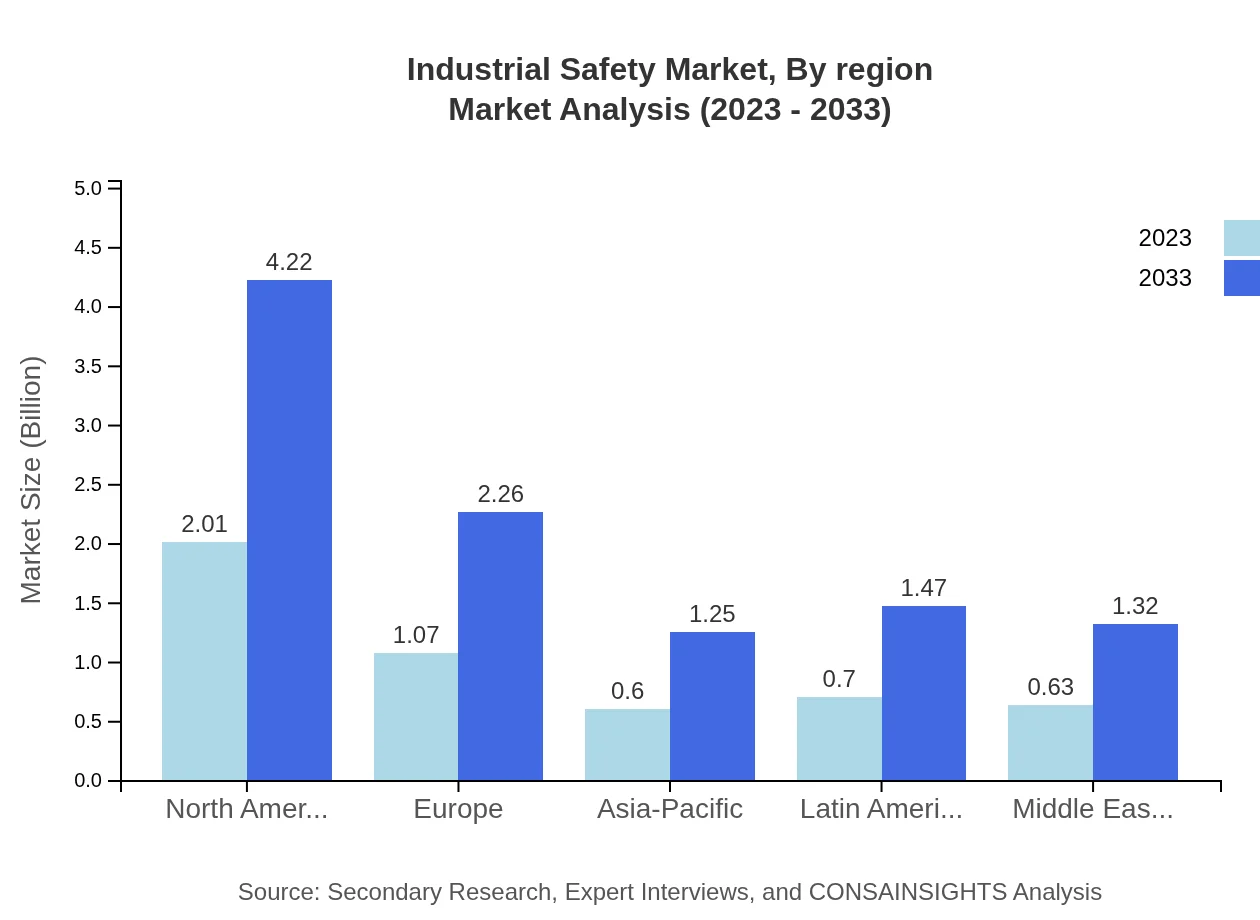

The European market for Industrial Safety is anticipated to grow from $1.70 billion in 2023 to $3.57 billion by 2033. Regulatory frameworks across countries like Germany and France are driving demand for enhanced safety systems and training programs.Asia Pacific Industrial Safety Market Report:

The Asia Pacific region, projected to grow from $0.85 billion in 2023 to $1.79 billion by 2033, represents a vital market for industrial safety due to rapid industrialization and improved safety regulations. Countries like China and India are experiencing a surge in infrastructure development, driving demand for safety equipment.North America Industrial Safety Market Report:

North America stands as one of the largest markets for Industrial Safety, from $1.77 billion in 2023 rising to $3.72 billion by 2033. Stringent regulations and a strong awareness of workplace safety significantly contribute to this growth, supported by innovations from major industry players.South America Industrial Safety Market Report:

In South America, the market is expected to increase from $0.32 billion in 2023 to $0.68 billion by 2033. The focus on improving workplace safety standards and increasing industrial activities, particularly in Brazil and Argentina, are anticipated to boost market growth.Middle East & Africa Industrial Safety Market Report:

The Middle East and Africa are poised for growth, with market size moving from $0.36 billion in 2023 to $0.76 billion by 2033. Factors such as infrastructural investments and growing regulations around safety in oil-rich nations contribute to the expected rise in market demand.Tell us your focus area and get a customized research report.

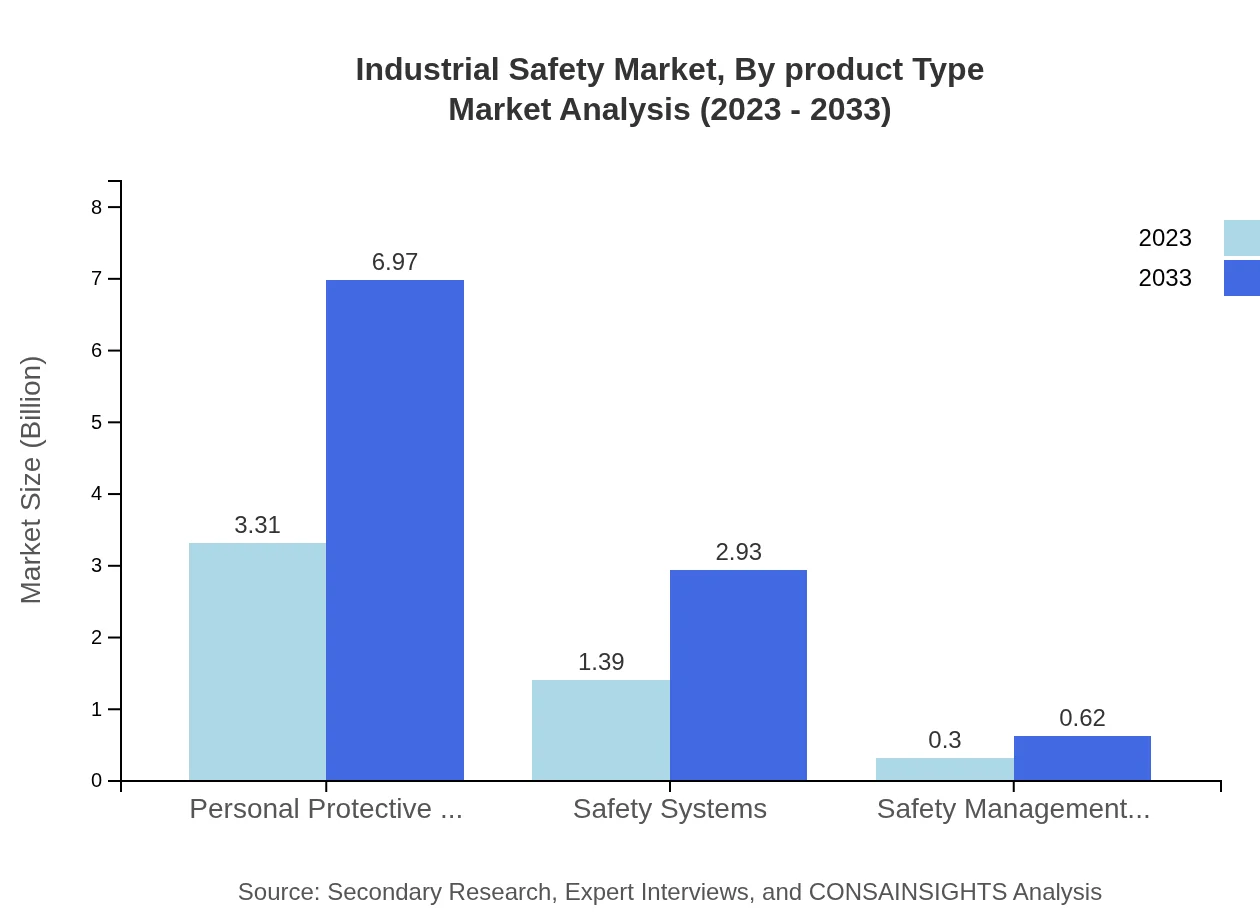

Industrial Safety Market Analysis By Product Type

In product segmentation, Personal Protective Equipment (PPE) dominates with a market size of $3.31 billion in 2023 and projected to grow to $6.97 billion by 2033, holding a significant share of 66.24%. Safety systems and safety management software follow, indicating diverse innovation and investment across categories.

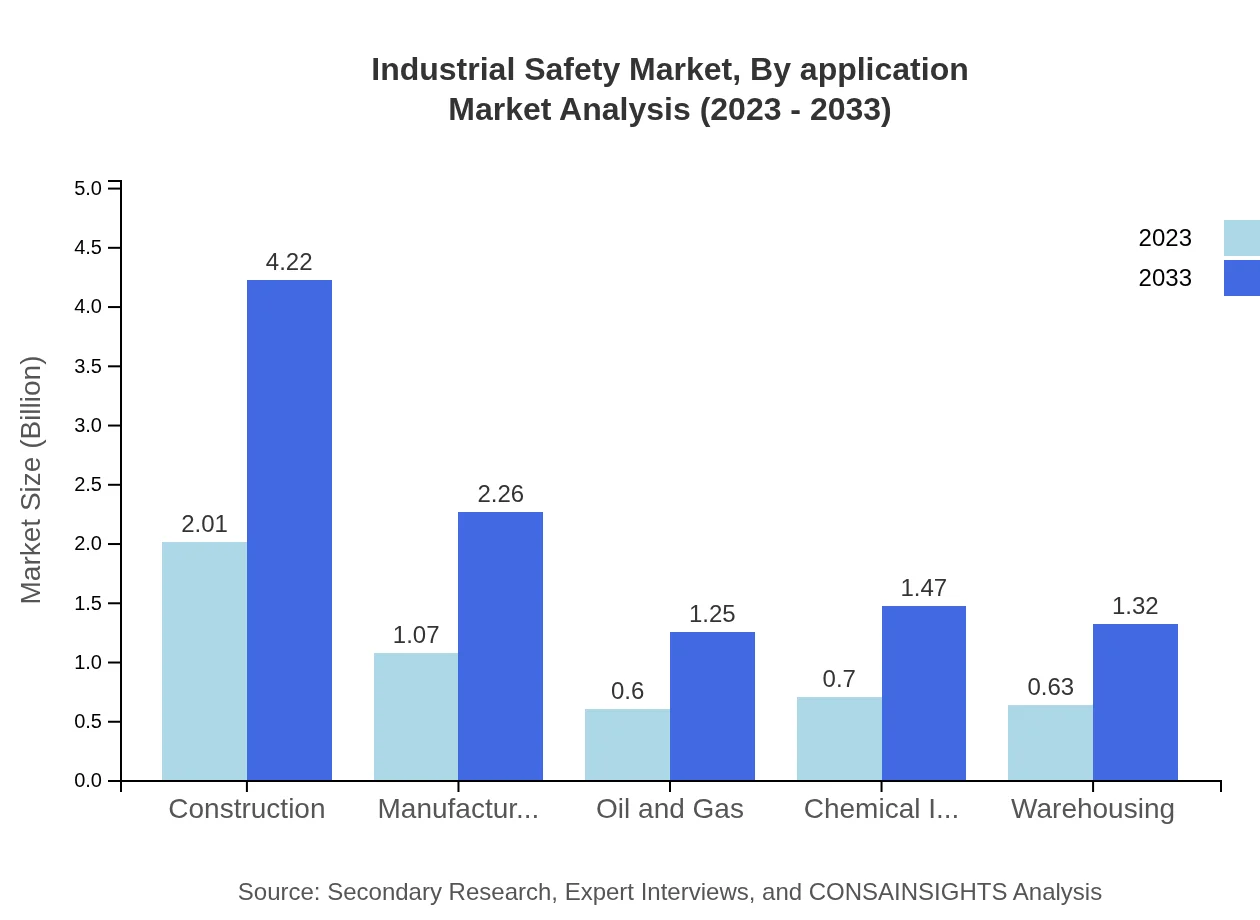

Industrial Safety Market Analysis By Application

By application, the construction and manufacturing sectors are substantial consumers of industrial safety products, with each segment registering high growth rates. The construction sector reflects a market share of 40.14%, while other sectors like oil and gas and healthcare also contribute significantly to the safety landscape, emphasizing the need for tailored solutions.

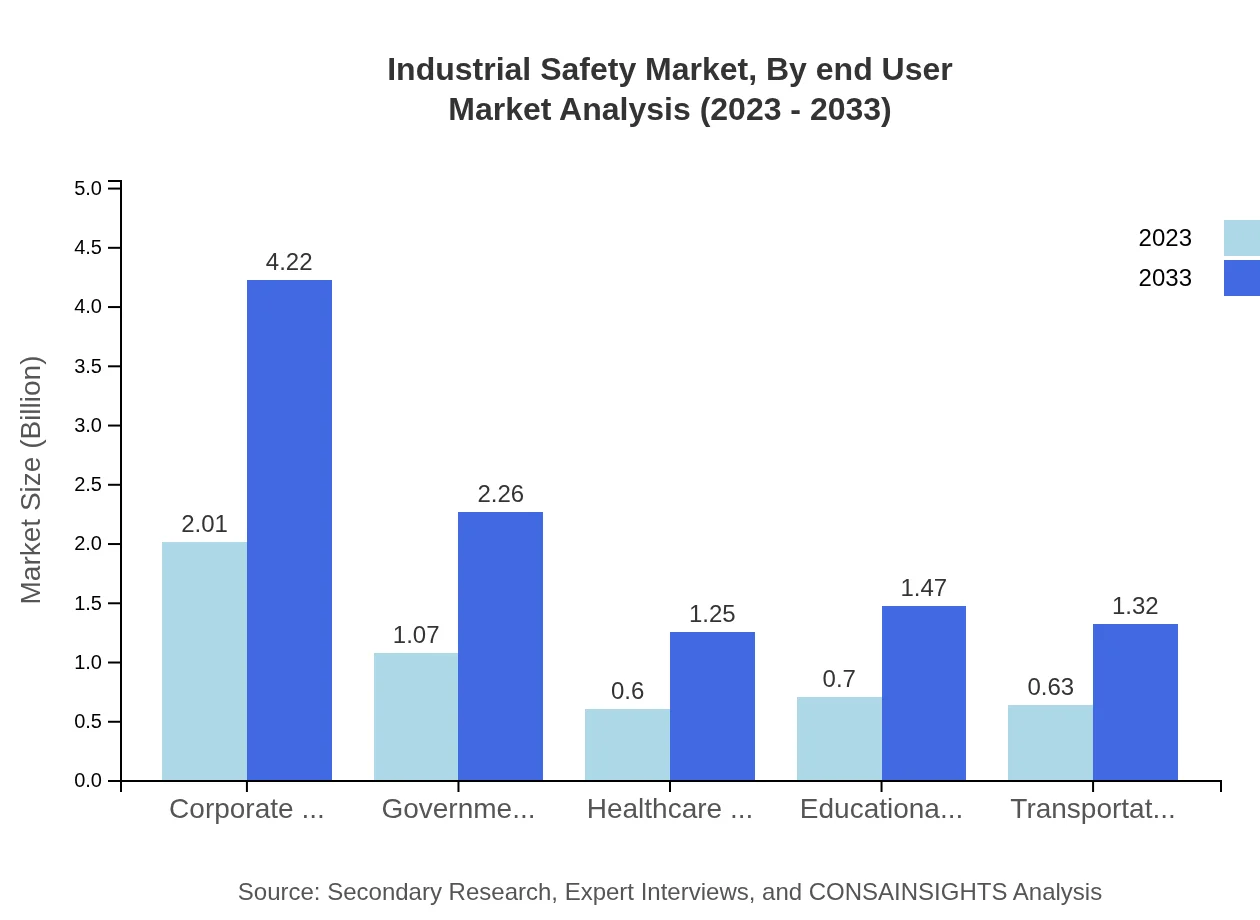

Industrial Safety Market Analysis By End User

End-user segmentation reveals government bodies and corporate enterprises as primary users of industrial safety products. Corporate enterprises lead with a market share of 40.14%, while sectors such as healthcare and education are witnessing increased investments in safety measures, highlighting the expanding relevance of safety technologies.

Industrial Safety Market Analysis By Region

Regionally, North America and Europe lead in market shares and growth potential. North America's commitment to strict safety regulations and innovative practices significantly enhances its leading position. Meanwhile, emerging markets in the Asia Pacific and Latin America showcase rapid growth opportunities due to increased industrial activities.

Industrial Safety Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Industrial Safety Industry

Honeywell :

A global leader in safety equipment, Honeywell innovates a wide range of personal protective equipment (PPE) and safety systems, focusing on comprehensive workplace safety solutions.3M:

3M is renowned for its diverse safety product offerings, including respiratory protection and hearing conservation, leading through innovation and addressing specific industry needs.DuPont:

DuPont provides advanced protective solutions and safety clothing, emphasizing research and development to meet evolving safety challenges.MSA Safety:

MSA Safety specializes in safety equipment and systems for critical protection, tackling various hazards with high-quality solutions for industrial applications.We're grateful to work with incredible clients.

FAQs

What is the market size of industrial Safety?

The industrial safety market is projected to reach approximately $5 billion by 2033, growing at a CAGR of 7.5% from its current estimated size. This significant growth reflects increasing investments in safety technologies and compliance standards.

What are the key market players or companies in this industrial Safety industry?

Key players in the industrial safety industry include notable companies across various sectors, focusing on innovative safety technologies, equipment manufacturing, and software solutions. These include major corporations specializing in Personal Protective Equipment (PPE), safety systems, and safety management software.

What are the primary factors driving the growth in the industrial Safety industry?

Growth in the industrial safety industry is primarily driven by stringent safety regulations, increased awareness of workplace safety, and advancements in safety technology. Additionally, the rising incidence of workplace hazards and the need for compliance with environmental and safety standards contribute significantly to market expansion.

Which region is the fastest Growing in the industrial Safety?

The fastest-growing region in the industrial safety market is North America, expected to increase from $1.77 billion in 2023 to $3.72 billion by 2033. This growth is attributed to robust regulatory frameworks and heightened safety awareness across various industries.

Does ConsaInsights provide customized market report data for the industrial Safety industry?

Yes, ConsaInsights offers customized market report data tailored to specific needs in the industrial safety industry. This includes detailed analyses, forecasts, and insights adapted to unique market segments and geographical regions.

What deliverables can I expect from this industrial Safety market research project?

Deliverables from the industrial safety market research project typically include a comprehensive report with market size data, trends, competitive analysis, regional breakdowns, and segment insights, alongside predictive analytics for strategic decision-making.

What are the market trends of industrial Safety?

Current trends in the industrial safety market include a shift towards digital safety management solutions, increased adoption of IoT-based safety systems, and a focus on sustainable and efficient PPE. There's also a growing emphasis on employee training and awareness initiatives.