Material Testing Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: material-testing

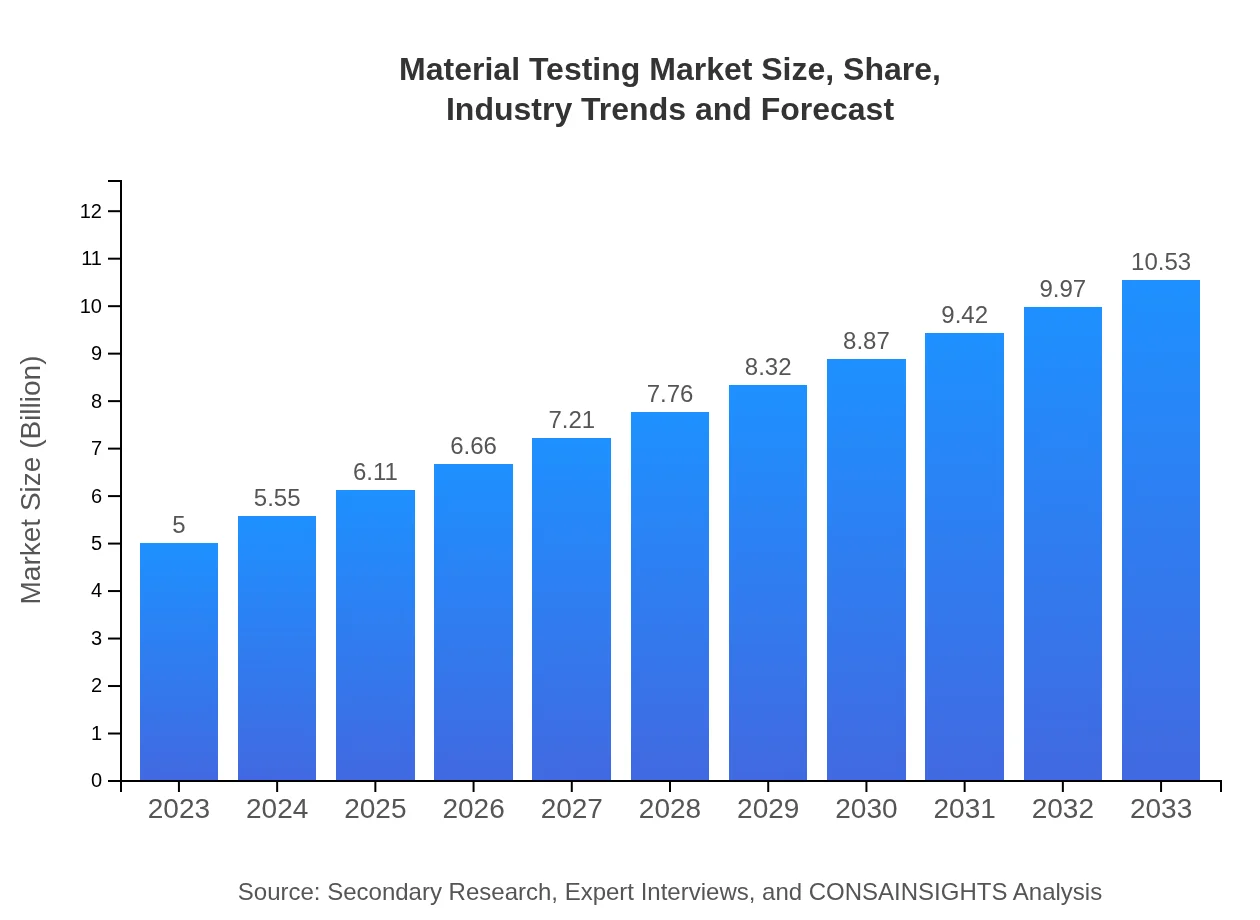

Material Testing Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides an in-depth analysis of the Material Testing market, exploring its dynamics, segmentation, technological advancements, and regional performance. It includes a comprehensive forecast for the period 2023 to 2033, highlighting growth opportunities and challenges in the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | SGS S.A., Intertek Group plc, Bureau Veritas |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Material Testing Market Overview

Customize Material Testing Market Report market research report

- ✔ Get in-depth analysis of Material Testing market size, growth, and forecasts.

- ✔ Understand Material Testing's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Material Testing

What is the Market Size & CAGR of Material Testing market in 2023?

Material Testing Industry Analysis

Material Testing Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Material Testing Market Analysis Report by Region

Europe Material Testing Market Report:

Europe's Material Testing market, valued at $1.20 billion in 2023, is expected to double by 2033 to reach approximately $2.54 billion. The region's robust manufacturing base, particularly in automotive and aerospace, alongside the enforcement of rigorous testing standards, propels this growth. Emerging initiatives related to sustainability are also influencing the testing requirements.Asia Pacific Material Testing Market Report:

The Asia Pacific region accounted for a significant share of the Material Testing market in 2023, valued at approximately $1.01 billion, and is projected to grow to $2.13 billion by 2033. The growth is driven by rapid industrialization, expanding automotive and electronics manufacturing, and increasing regulatory compliance. China and India are key contributors to this growth, where investments in infrastructure and manufacturing are escalating.North America Material Testing Market Report:

North America is a prominent market, with a value of about $1.82 billion in 2023, projected to reach $3.83 billion by 2033. This growth is fueled by stringent quality control standards and the presence of well-established industries such as aerospace and automotive. The U.S. remains a leader, with advanced testing technologies and a strong focus on R&D.South America Material Testing Market Report:

In South America, the Material Testing market is expected to grow modestly from $0.40 billion in 2023 to approximately $0.85 billion in 2033. Brazil and Argentina drive the growth, mainly due to increased investments in construction and automotive sectors, although economic challenges can affect expansion rates.Middle East & Africa Material Testing Market Report:

The Middle East and Africa region holds a market size of $0.56 billion in 2023, anticipated to reach $1.17 billion by 2033. The growth is attributed to increased industrial activity and infrastructure projects, particularly in countries like the UAE and South Africa, fostering demand for reliable material testing solutions.Tell us your focus area and get a customized research report.

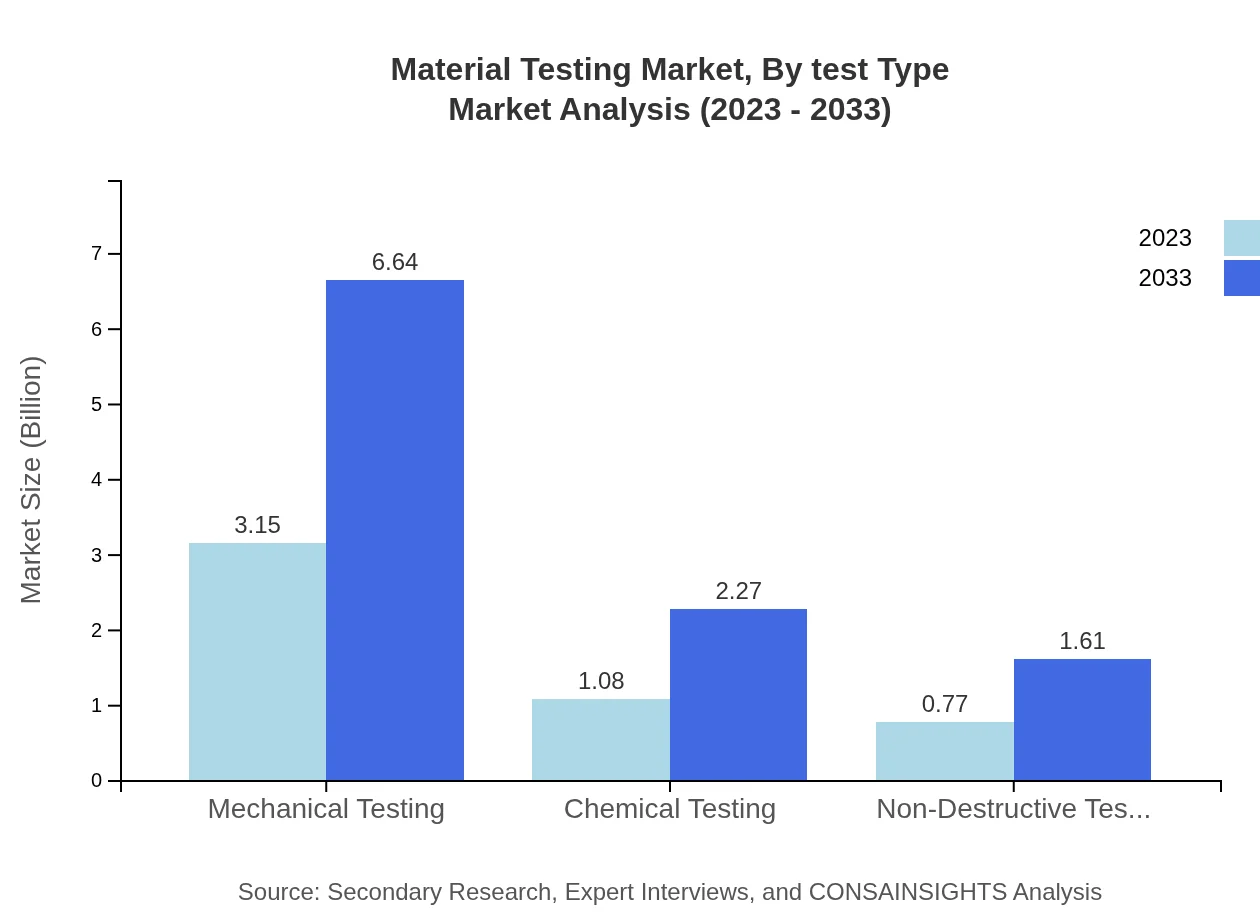

Material Testing Market Analysis By Test Type

The market by test type includes segments such as mechanical testing, chemical testing, and non-destructive testing. Mechanical testing dominates the market with an expected growth from $3.15 billion in 2023 to $6.64 billion in 2033, driven by standards in construction and manufacturing. Similarly, chemical testing is crucial for ensuring material performance, projected to grow from $1.08 billion to $2.27 billion in the same period. Non-destructive testing, essential in industries like aerospace, is also seeing significant growth.

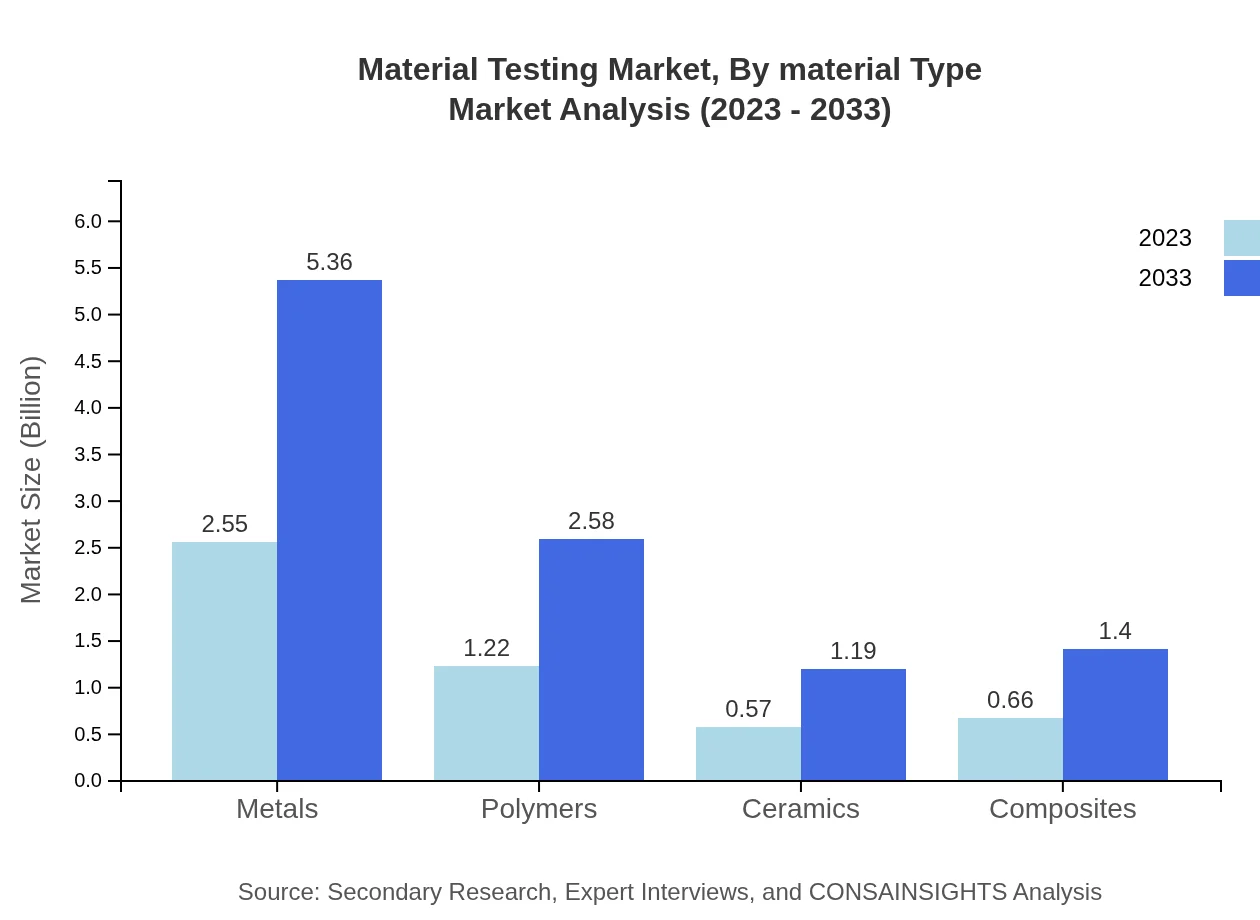

Material Testing Market Analysis By Material Type

Segments in the material type include metals, polymers, ceramics, and composites. The metals segment leads the market with a performance expected to grow from $2.55 billion in 2023 to $5.36 billion in 2033. Polymers are also significant, projected to increase from $1.22 billion to $2.58 billion. Each material segment faces unique challenges as they require specific testing methods to comply with regulatory standards and performance expectations.

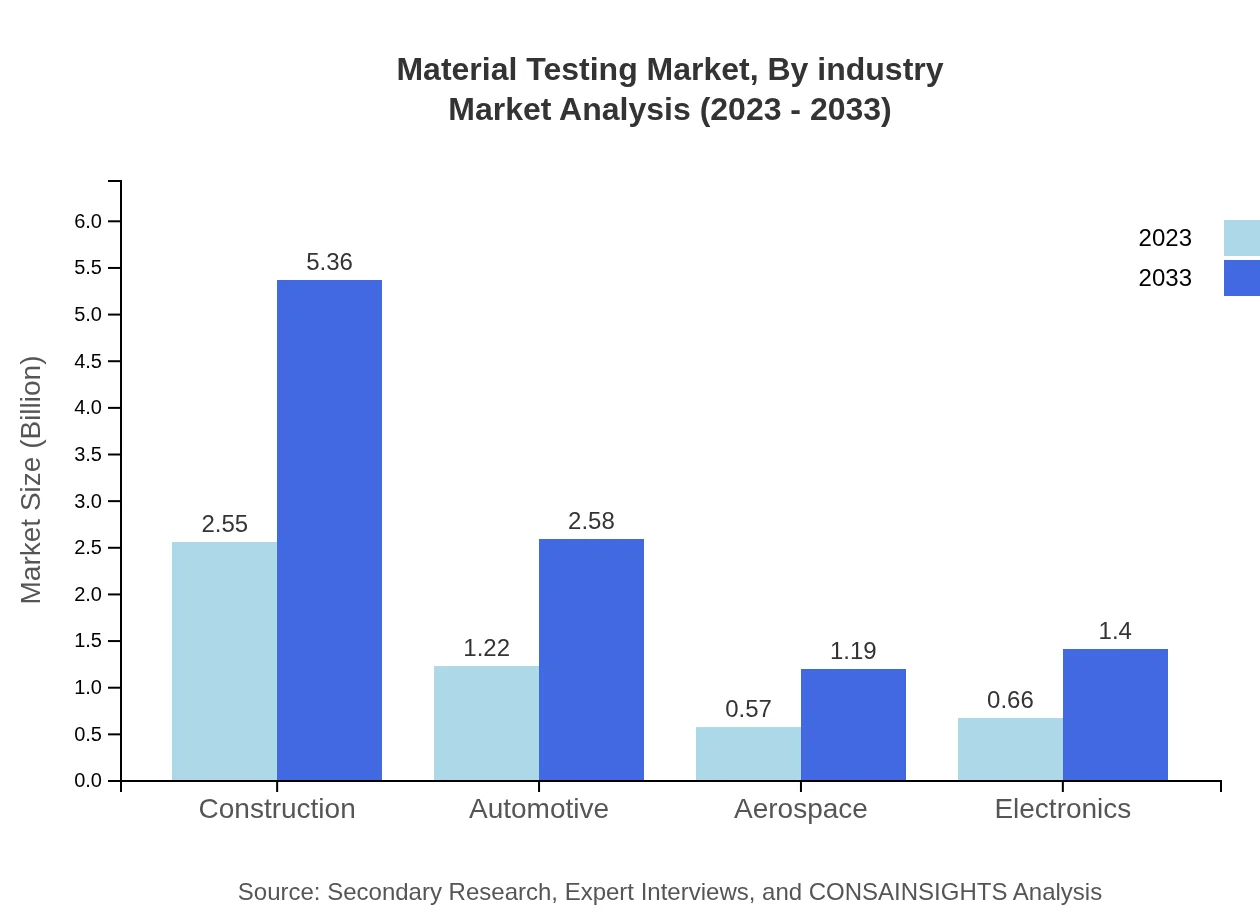

Material Testing Market Analysis By Industry

The industry-specific segmentation highlights notable sectors such as construction, automotive, aerospace, and electronics. The construction industry expects remarkable growth from $2.55 billion in 2023 to $5.36 billion by 2033, driven by a surge in infrastructure projects. The automotive segment is also significant, anticipated to grow from $1.22 billion to $2.58 billion, as vehicle safety and reliability become prime concerns.

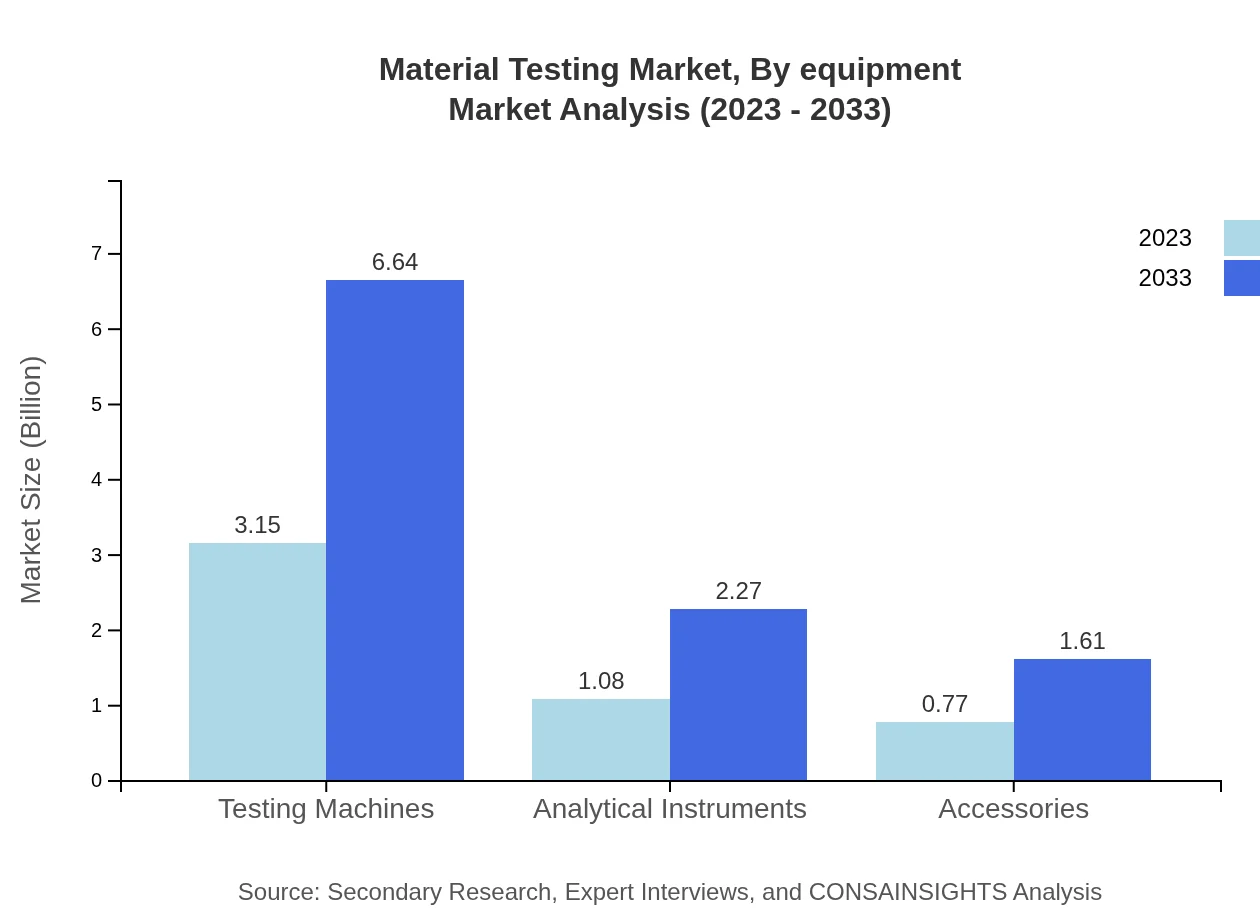

Material Testing Market Analysis By Equipment

Key equipment in the Material Testing market includes analytical instruments, testing machines, and accessories. Testing machines dominate with sales expected to rise from $3.15 billion to $6.64 billion by 2033. Analytical instruments also grow significantly, catering to specialized testing needs, reaching $2.27 billion. The accessories segment is projected at a significant increase, ensuring complete testing solutions.

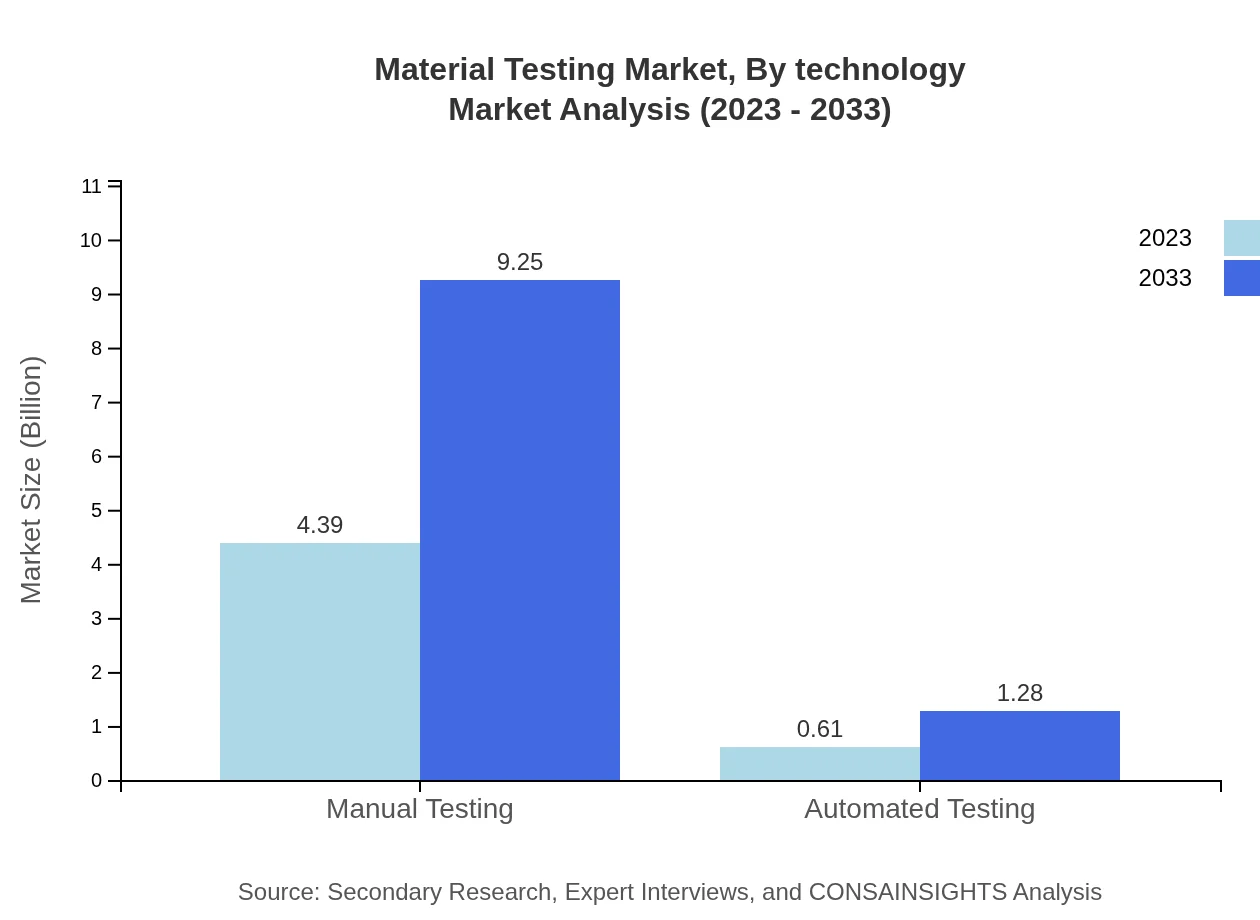

Material Testing Market Analysis By Technology

The technological advancements in Material Testing include manual testing and automated testing methods. Manual testing currently holds a significant share of the market at 87.86%, projected to grow from $4.39 billion to $9.25 billion by 2033. However, the automated testing segment is gaining traction, growing from $0.61 billion to $1.28 billion as industries look to enhance efficiency and accuracy in testing processes.

Material Testing Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Material Testing Industry

SGS S.A.:

SGS is a leading inspection, verification, testing, and certification company. It is known for its extensive range of testing services, including material testing for construction and manufacturing industries, ensuring compliance and safety.Intertek Group plc:

Intertek provides quality and safety solutions, offering extensive material testing services to various industries. Their innovative testing methodologies and certifications contribute significantly to quality assurance processes.Bureau Veritas:

Bureau Veritas is a noted international company specializing in testing, inspection, and certification. They provide a wide spectrum of testing services and a solid technical foundation for material testing across sectors.We're grateful to work with incredible clients.

FAQs

What is the market size of material testing?

The global material testing market is valued at approximately $5 billion in 2023 and is projected to grow with a CAGR of 7.5%, reaching significant heights by 2033.

What are the key market players or companies in the material testing industry?

Key players include major organizations involved in manufacturing and providing material testing solutions across various application sectors such as construction, automotive, aerospace, and electronics.

What are the primary factors driving the growth in the material testing industry?

The growth is driven by increasing demand for quality assurance, stringent regulatory standards across industries, technological advancements in testing processes, and the rising focus on safety and quality in materials.

Which region is the fastest Growing in the material testing market?

Europe is projected to grow rapidly, with market values increasing from $1.20 billion in 2023 to $2.54 billion by 2033, while Asia Pacific's market will rise from $1.01 billion to $2.13 billion.

Does ConsaInsights provide customized market report data for the material testing industry?

Yes, ConsaInsights offers tailored market report data for the material testing industry, allowing businesses to obtain insights that meet their specific needs and strategic objectives.

What deliverables can I expect from this material testing market research project?

Clients can expect comprehensive reports, market analysis charts, detailed segment breakdowns, and key insights on competitive strategies and industry trends affecting the material testing market.

What are the market trends of material testing?

Trends include the adoption of automated and digital testing methodologies, increased investment in R&D for innovative materials, and a growing emphasis on sustainability in material testing practices.