Silicon Epitaxial Wafer Market Report

First published: 14 September 2024 | Last updated: 31 January 2026 | Report Code: silicon-epitaxial-wafer

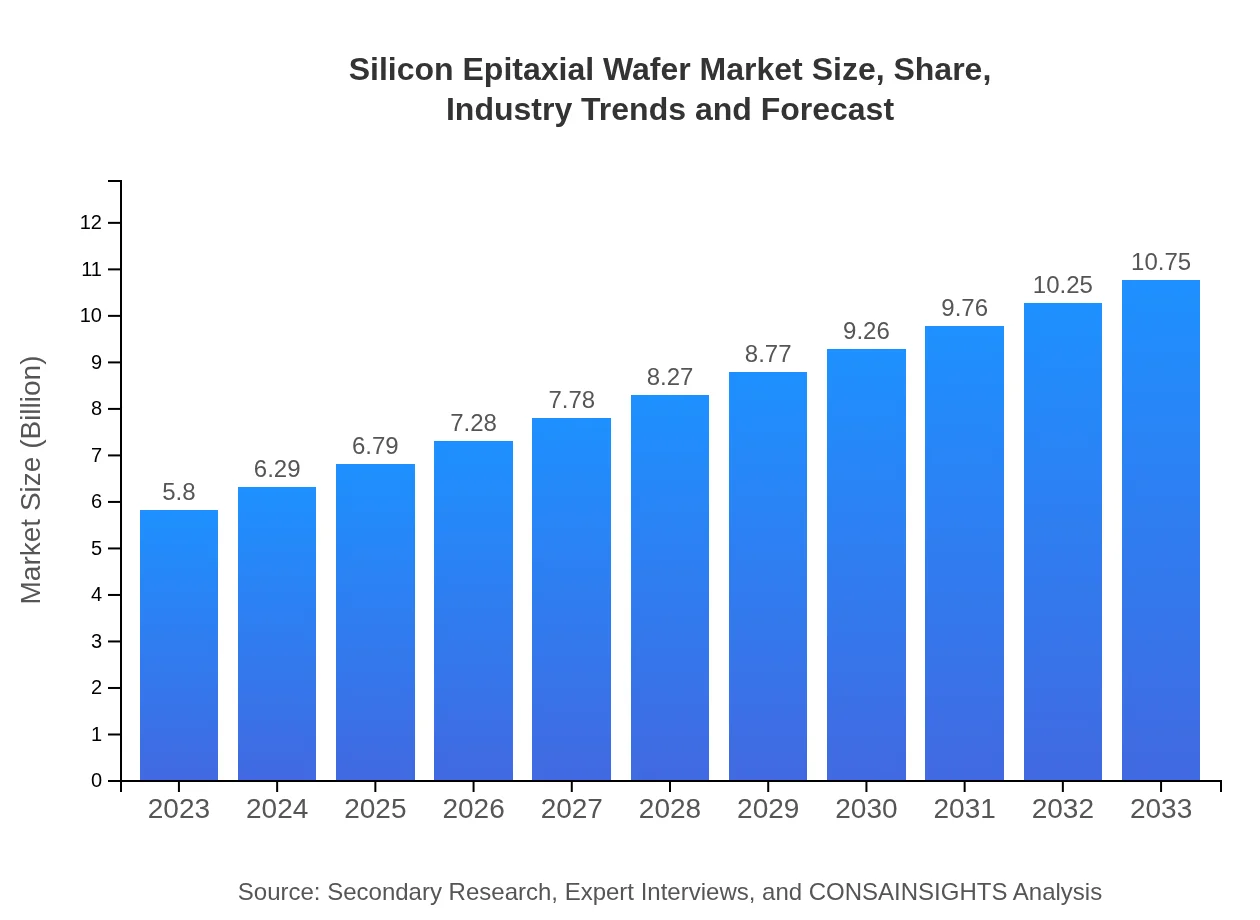

Silicon Epitaxial Wafer Market — USD $5.8 Billion in 2023, Growing to USD 10.75B by 2033 at 6.2% CAGR

This report provides a comprehensive analysis of the Silicon Epitaxial Wafer market, focusing on trends, projections, and key players from 2023 to 2033. It covers market size, growth rates, industry insights, and detailed breakdowns by segments and regions.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.80 Billion |

| CAGR (2023-2033) | 6.2% |

| 2033 Market Size | $10.75 Billion |

| Top Companies | MEMC Electronic Materials, Inc., Samsung Electronics, Silicon Materials, Inc., Nihon Superior Co., Ltd., GlobalWafers Co., Ltd. |

| Published Date | 14 September 2024 |

| Last Modified Date | 31 January 2026 |

Silicon Epitaxial Wafer Market Overview

Customize Silicon Epitaxial Wafer Market Report market research report

- ✔ Get in-depth analysis of Silicon Epitaxial Wafer market size, growth, and forecasts.

- ✔ Understand Silicon Epitaxial Wafer's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Silicon Epitaxial Wafer

What is the Market Size & CAGR of Silicon Epitaxial Wafer market in 2023?

Silicon Epitaxial Wafer Industry Analysis

Silicon Epitaxial Wafer Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Silicon Epitaxial Wafer Market Analysis Report by Region

Europe Silicon Epitaxial Wafer Market Report:

Europe's market for Silicon Epitaxial Wafers is forecasted to grow from $1.51 billion in 2023 to $2.80 billion by 2033, bolstered by stringent energy efficiency regulations and a push towards sustainable technologies.Asia Pacific Silicon Epitaxial Wafer Market Report:

The Asia Pacific region is a major market for Silicon Epitaxial Wafers, estimated to be worth $1.18 billion in 2023 and projected to grow to $2.19 billion by 2033. This growth is driven by the presence of leading semiconductor manufacturers and a high demand for consumer electronics.North America Silicon Epitaxial Wafer Market Report:

North America holds a significant share of the market, projected to reach $4.06 billion by 2033, up from $2.19 billion in 2023. The region benefits from advanced technological innovations and a strong automotive sector driving demand for high-performance chips.South America Silicon Epitaxial Wafer Market Report:

In South America, the Silicon Epitaxial Wafer market is expected to grow from $0.41 billion in 2023 to $0.76 billion by 2033. The growth is primarily attributed to the increasing investments in telecom infrastructure and renewable energy projects.Middle East & Africa Silicon Epitaxial Wafer Market Report:

The Middle East and Africa are anticipated to reach $0.95 billion by 2033, growing from $0.51 billion in 2023, driven by growing investments in technology infrastructure and renewable energy.Tell us your focus area and get a customized research report.

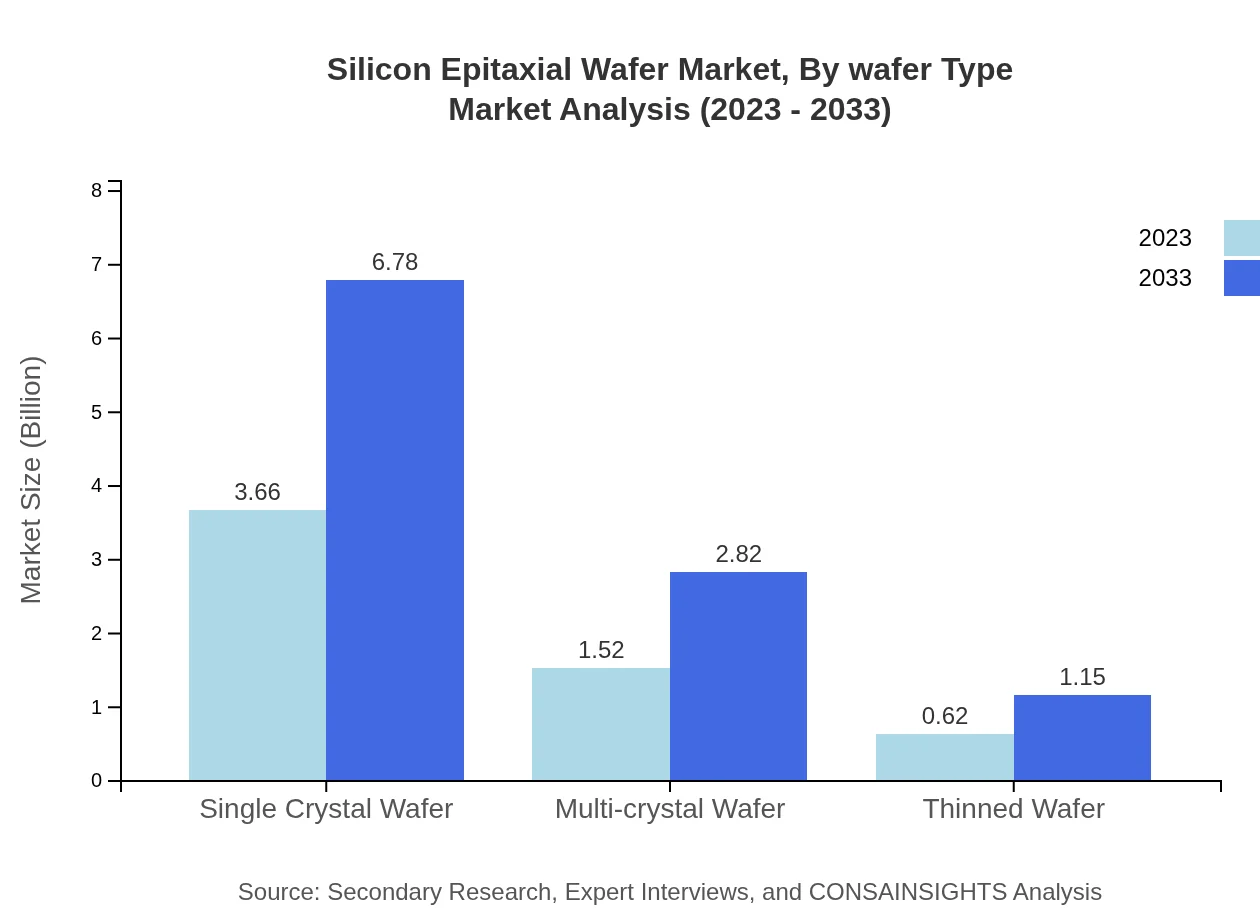

Silicon Epitaxial Wafer Market Analysis By Wafer Type

The market is primarily segmented into Single Crystal Wafers, Multi-crystal Wafers, and Thinned Wafers. The Single Crystal Wafer segment leads with a market size of $3.66 billion in 2023, increasing to $6.78 billion by 2033, accounting for 63.06% of the market share. The Multi-crystal Wafers are expected to grow from $1.52 billion to $2.82 billion, while Thinned Wafers will expand from $0.62 billion to $1.15 billion.

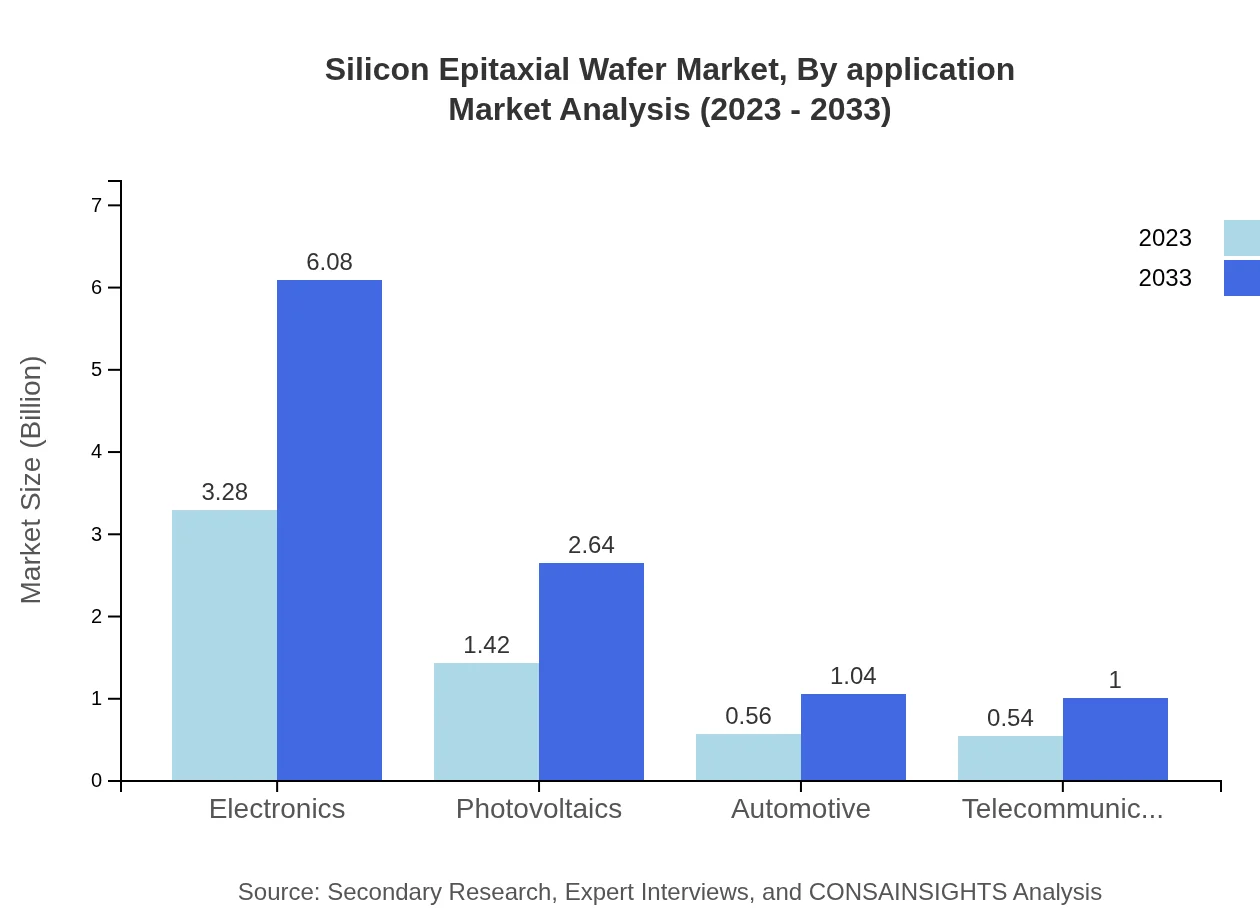

Silicon Epitaxial Wafer Market Analysis By Application

The applications of Silicon Epitaxial Wafers span across various sectors including Electronics, Photovoltaics, Automotive, Telecommunications, and Consumer Electronics. The Electronics segment leads with a market size of $3.28 billion in 2023, forecasted to grow to $6.08 billion by 2033, covering 56.55% of the market share, while the Photovoltaics segment is set to grow from $1.42 billion to $2.64 billion.

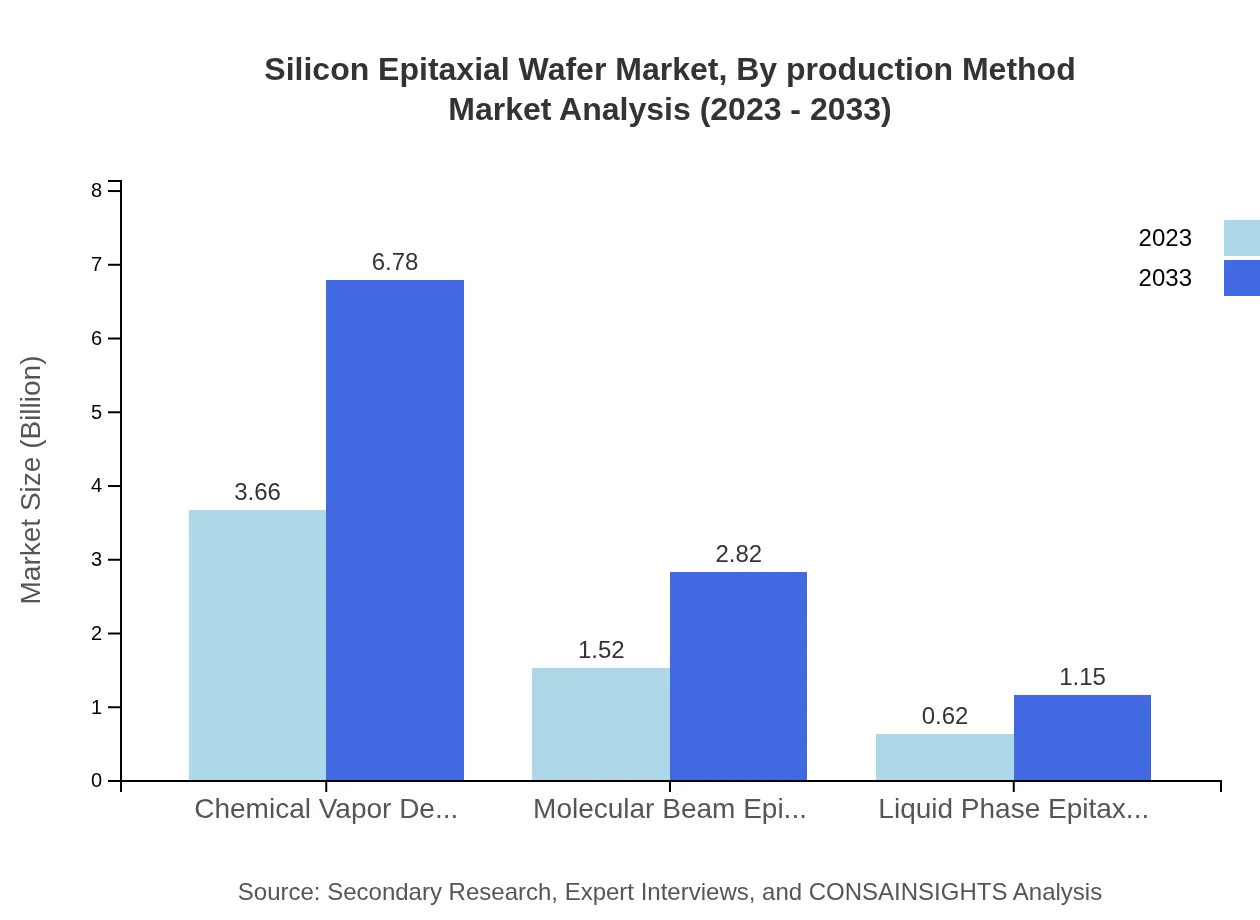

Silicon Epitaxial Wafer Market Analysis By Production Method

Production methods like Chemical Vapor Deposition (CVD), Molecular Beam Epitaxy (MBE), and Liquid Phase Epitaxy (LPE) highlight the market dynamics. CVD holds the largest share at $3.66 billion projected in 2023 and expected to reach $6.78 billion by 2033, while MBE and LPE segments will grow steadily, capturing 26.2% and 10.74% respectively.

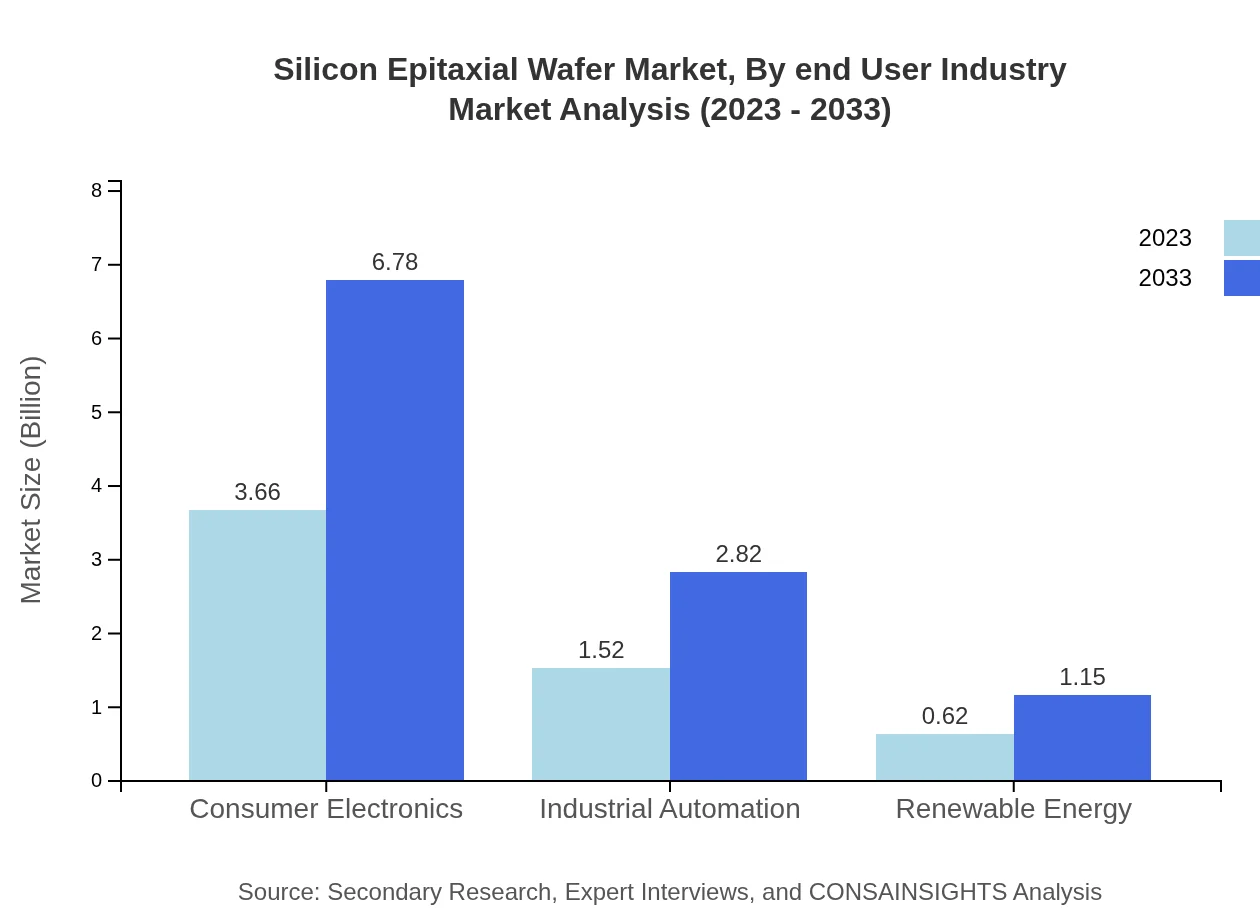

Silicon Epitaxial Wafer Market Analysis By End User Industry

Key end-user industries include Consumer Electronics, Industrial Automation, Renewable Energy, and Automotive. The Consumer Electronics market is leading, projected to reach $6.78 billion by 2033 from $3.66 billion in 2023, holding a dominant share of 63.06%, indicating robust demand and innovative product development.

Silicon Epitaxial Wafer Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Silicon Epitaxial Wafer Industry

MEMC Electronic Materials, Inc.:

A leading global supplier of silicon wafers and epitaxial wafers, known for its innovations in wafer technology and significant market share.Samsung Electronics:

A major player in the semiconductor industry that manufactures and supplies high-quality silicon epitaxial wafers primarily for consumer electronics.Silicon Materials, Inc.:

Specializes in producing advanced epitaxial wafers, contributing to high-performance renewable energy applications.Nihon Superior Co., Ltd.:

Recognized for innovative technologies in silicon wafer manufacturing, focusing on enhancing yield and quality.GlobalWafers Co., Ltd.:

A significant player in the semiconductor wafer market, focusing on high-quality silicon products and epitaxy technologies.We're grateful to work with incredible clients.

FAQs

What is the market size of silicon Epitaxial Wafer?

The silicon epitaxial wafer market size is projected to reach $5.8 billion by 2033, with a compound annual growth rate (CAGR) of 6.2% from 2023 to 2033. This growth reflects increasing demand across various sectors.

What are the key market players or companies in the silicon Epitaxial Wafer industry?

Key players in the silicon epitaxial wafer industry include major manufacturers like SUMCO Corporation, Shin-Etsu Chemical Co., and GlobalWafers. These companies are integral in driving innovation and production capacities within the market.

What are the primary factors driving the growth in the silicon Epitaxial Wafer industry?

Factors driving growth in the silicon epitaxial wafer industry include rising semiconductor applications, technological advancements in electronics, and increased demand for renewable energy solutions, notably in photovoltaics and consumer electronics sectors.

Which region is the fastest Growing in the silicon Epitaxial Wafer market?

The Asia Pacific region is currently the fastest-growing market for silicon epitaxial wafers, expected to grow from $1.18 billion in 2023 to $2.19 billion by 2033, reflecting rapid advancements in electronics and manufacturing capabilities.

Does ConsaInsights provide customized market report data for the silicon Epitaxial Wafer industry?

Yes, ConsaInsights provides customized market report data tailored to specific needs within the silicon epitaxial wafer industry, ensuring comprehensive insights and analytics to support strategic decision-making for clients.

What deliverables can I expect from this silicon Epitaxial Wafer market research project?

Deliverables from the silicon epitaxial wafer market research project include detailed market reports, segmentation analysis, forecasts, competitive landscapes, and recommendations tailored to assist stakeholders in strategic planning and investment decisions.

What are the market trends of silicon Epitaxial Wafer?

Current trends in the silicon epitaxial wafer market include a shift towards thinner wafers, growing adoption in automotive electronics, and increasing applications in renewable energy technologies, particularly photovoltaics, driven by advancements in manufacturing processes.