Zinc Chemicals Market Report

First published: 04 October 2024 | Last updated: 02 February 2026 | Report Code: zinc-chemicals

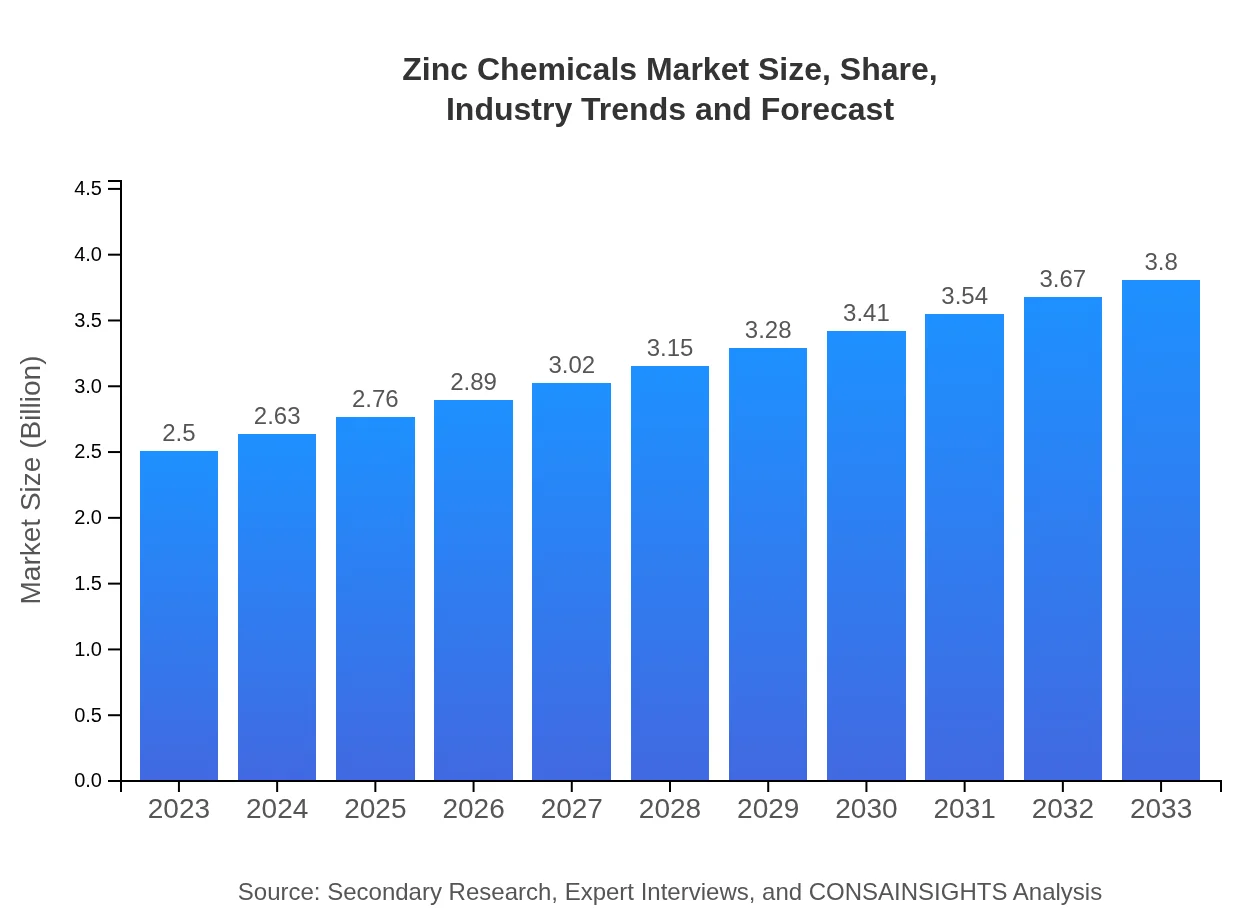

Zinc Chemicals Market — USD $2.5 Billion in 2023, Growing to USD 3.80B by 2033 at 4.2% CAGR

This market report provides comprehensive insights into the Zinc Chemicals market, covering market size, industry analysis, regional breakdowns, and future forecasts from 2023 to 2033, offering valuable data for stakeholders and decision-makers.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $2.50 Billion |

| CAGR (2023-2033) | 4.2% |

| 2033 Market Size | $3.80 Billion |

| Top Companies | Zinc Nacional, American Zinc Recycling Corp., Mitsubishi Materials Corporation, Umicore |

| Published Date | 04 October 2024 |

| Last Modified Date | 02 February 2026 |

Zinc Chemicals Market Overview

Customize Zinc Chemicals Market Report market research report

- ✔ Get in-depth analysis of Zinc Chemicals market size, growth, and forecasts.

- ✔ Understand Zinc Chemicals's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Zinc Chemicals

What is the Market Size & CAGR of Zinc Chemicals market in 2023?

Zinc Chemicals Industry Analysis

Zinc Chemicals Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Zinc Chemicals Market Analysis Report by Region

Europe Zinc Chemicals Market Report:

Europe demonstrates a steady growth trajectory for the Zinc Chemicals market, starting from $0.86 billion in 2023 and projected to grow to $1.30 billion by 2033. Europe's focus on green chemistry and sustainable product development prominently drives the market toward eco-friendly zinc chemical solutions.Asia Pacific Zinc Chemicals Market Report:

The Asia Pacific region holds a significant share of the Zinc Chemicals market, valued at $0.47 billion in 2023 and projected to reach $0.71 billion by 2033. Key growth drivers include increased industrialization and rapid urbanization in countries like China and India, alongside rising demand for construction materials and agriculture applications.North America Zinc Chemicals Market Report:

North America, with a market size of $0.86 billion in 2023, is anticipated to reach $1.31 billion by 2033. The growth is bolstered by advancements in technologies and strong demand in the automotive and construction sectors, alongside consistent regulatory support for sustainable practices.South America Zinc Chemicals Market Report:

South America presents unique challenges for the Zinc Chemicals market, with a current market valuation of -$0.02 billion in 2023, expected to decline further to -$0.03 billion by 2033. Factors impacting this downturn include economic instability and a shift toward alternative chemicals in various applications.Middle East & Africa Zinc Chemicals Market Report:

The Middle East and Africa region's Zinc Chemicals market, valued at $0.33 billion in 2023, is projected to increase to $0.51 billion by 2033. The region's growing construction projects and agricultural initiatives are the primary factors fueling this growth.Tell us your focus area and get a customized research report.

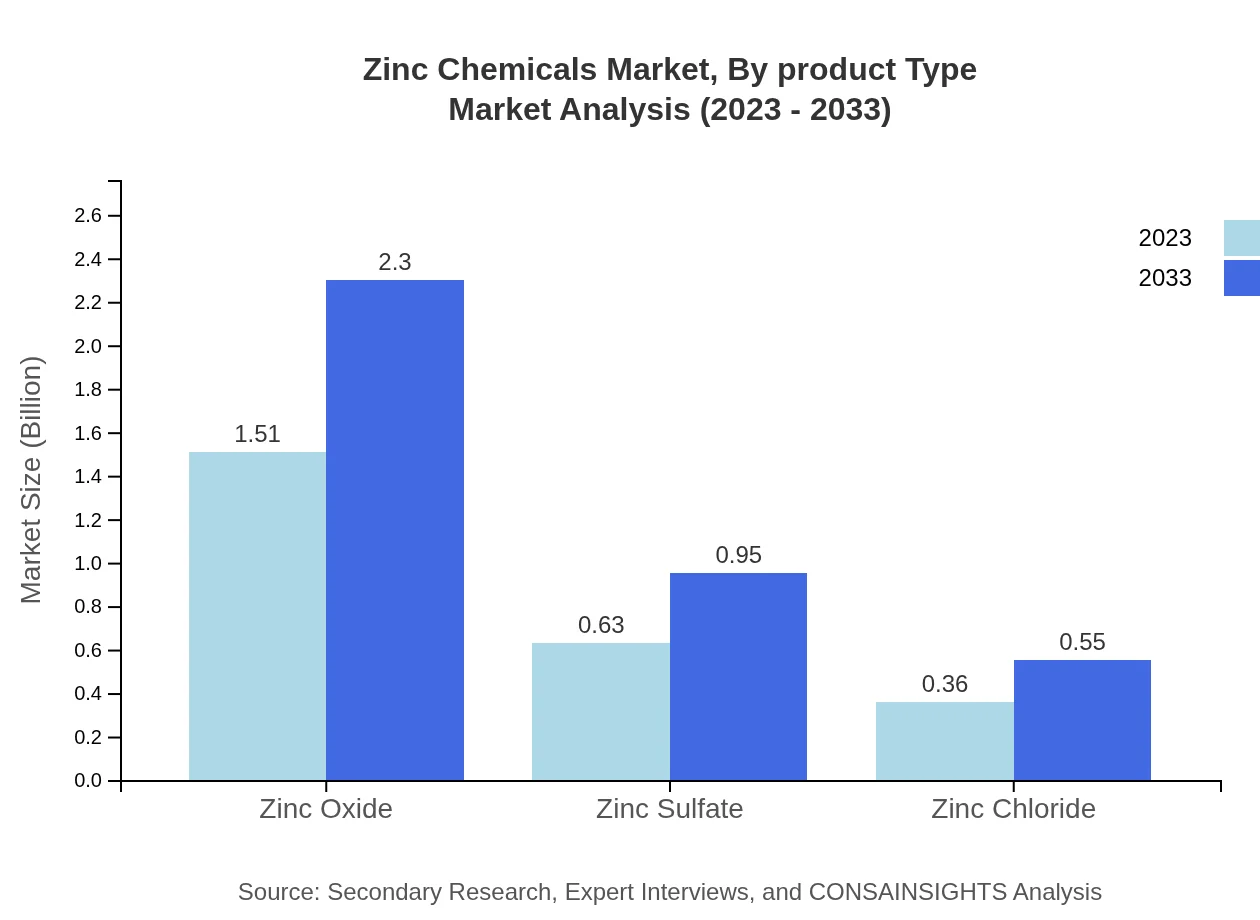

Zinc Chemicals Market Analysis By Product Type

The product types in the Zinc Chemicals market include Zinc Oxide, Zinc Sulfate, and Zinc Chloride. Zinc Oxide remains a leading segment, with a market size of $1.51 billion in 2023, forecasted to grow to $2.30 billion by 2033. Zinc Sulfate and Zinc Chloride follow, representing niche yet significant contributions due to their specialized applications in agriculture and food preservation.

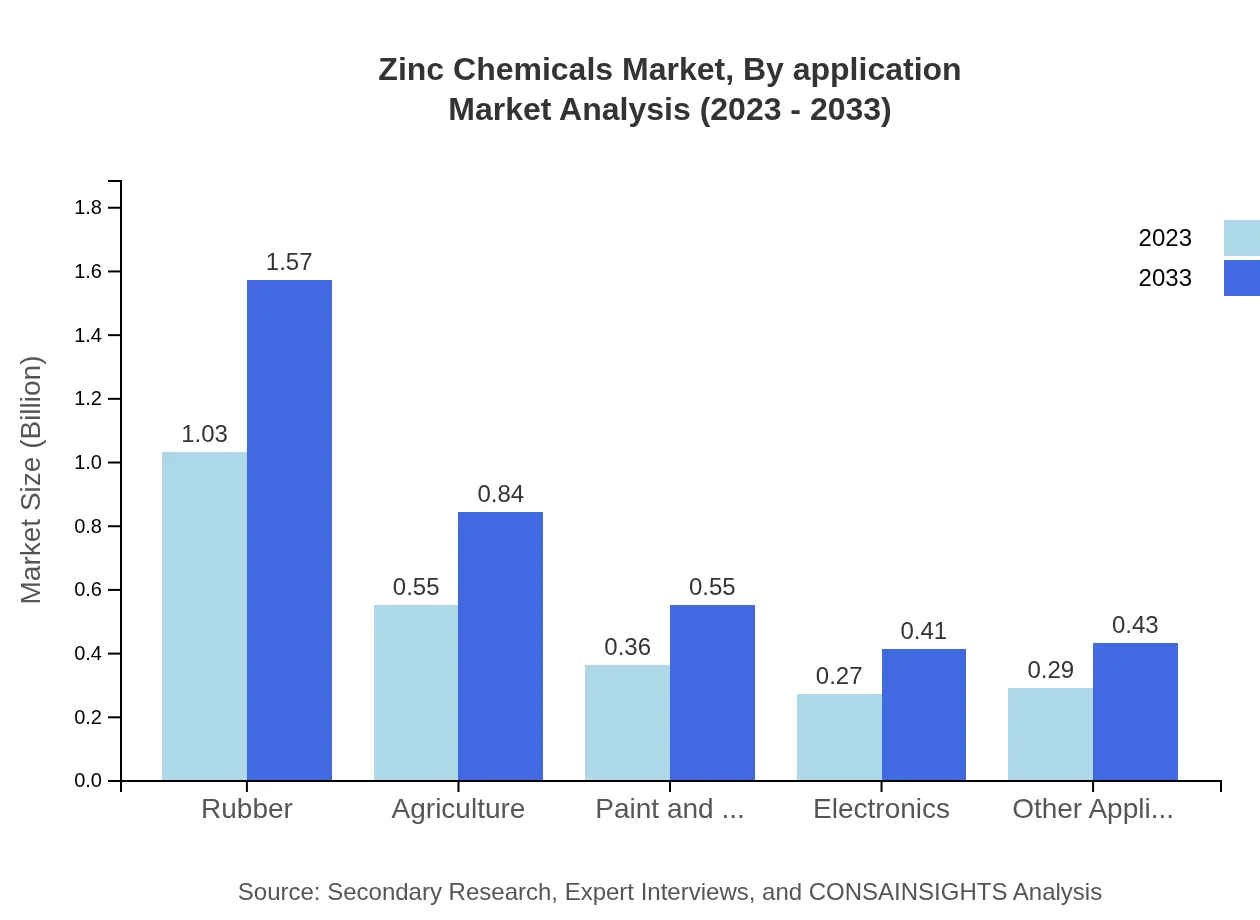

Zinc Chemicals Market Analysis By Application

The applications of Zinc Chemicals cover a wide array of sectors, including the automotive, construction, and agricultural industries. In 2023, the rubber segment is the largest, valued at $1.03 billion, projected to grow to $1.57 billion by 2033. Other notable applications include agriculture ($0.55 billion to $0.84 billion) and paints and coatings ($0.36 billion to $0.55 billion).

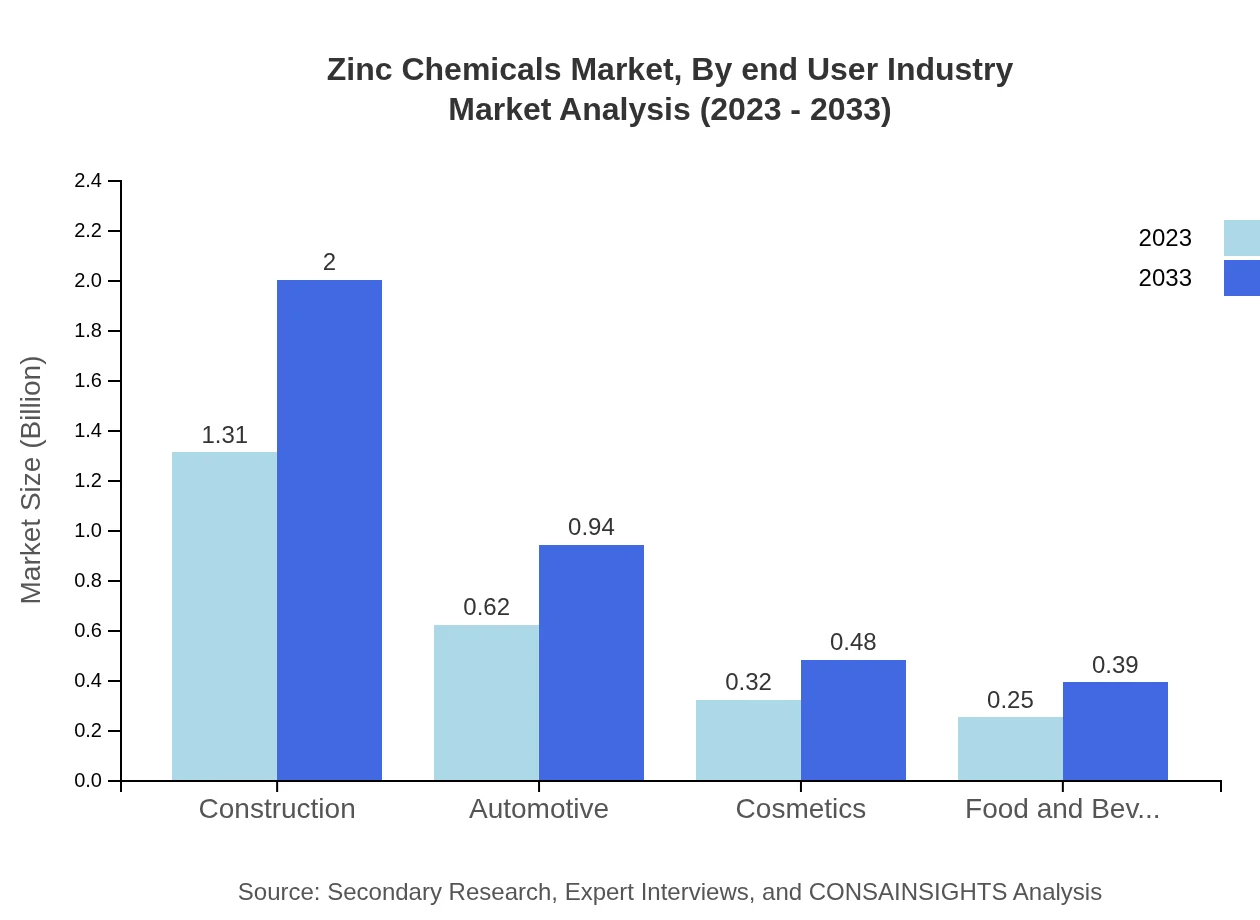

Zinc Chemicals Market Analysis By End User Industry

Zinc Chemicals serve several end-user industries, notably construction with a market size of $1.31 billion in 2023, expected to rise to $2.00 billion by 2033, and automotive, expected to grow from $0.62 billion to $0.94 billion in the same period. Other industries such as cosmetics and food and beverage also significantly contribute to market dynamics.

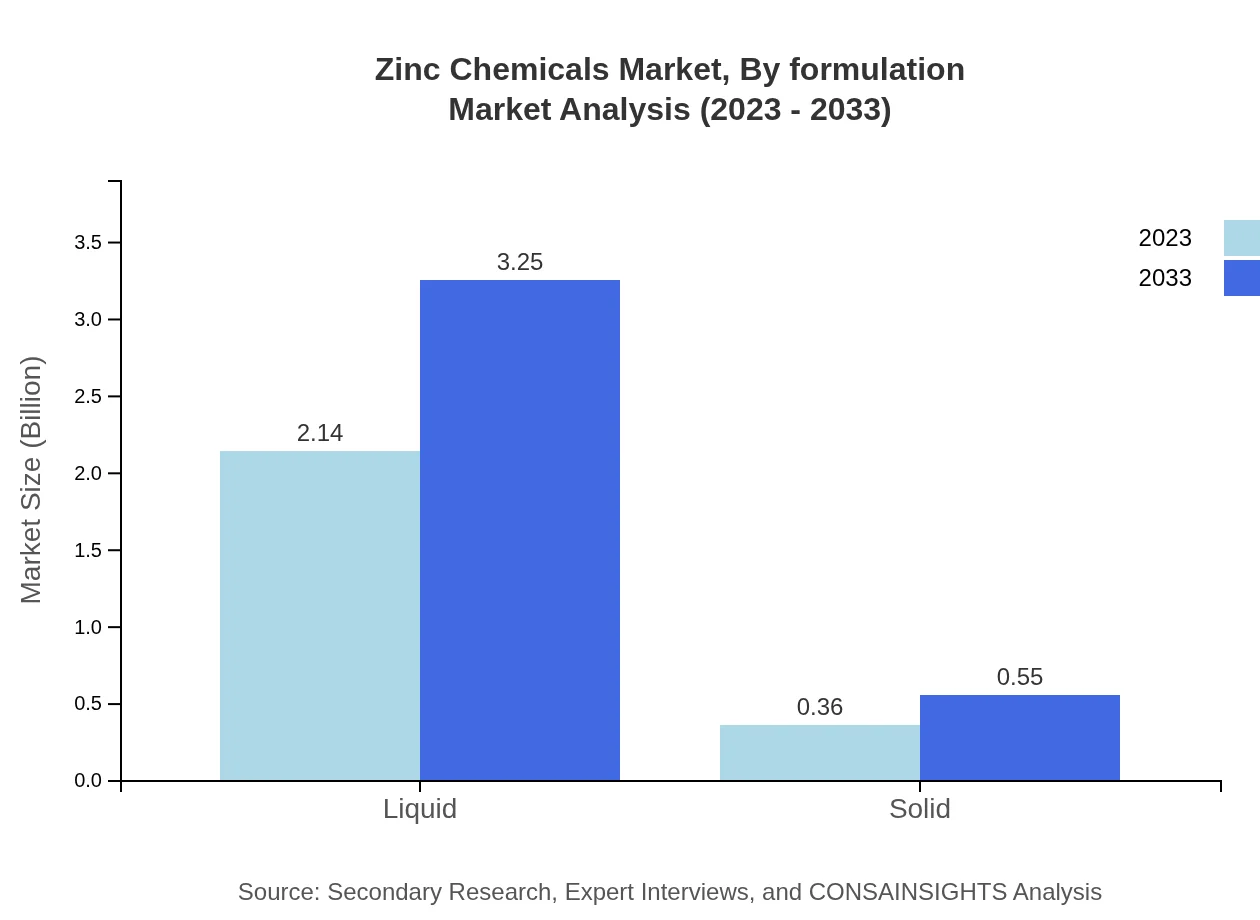

Zinc Chemicals Market Analysis By Formulation

Formulation plays a critical role in the Zinc Chemicals market. The liquid form dominates with a market size of $2.14 billion in 2023, looking towards $3.25 billion by 2033. Solid forms represent a smaller share, which still holds significance due to specific applications requiring solid state.

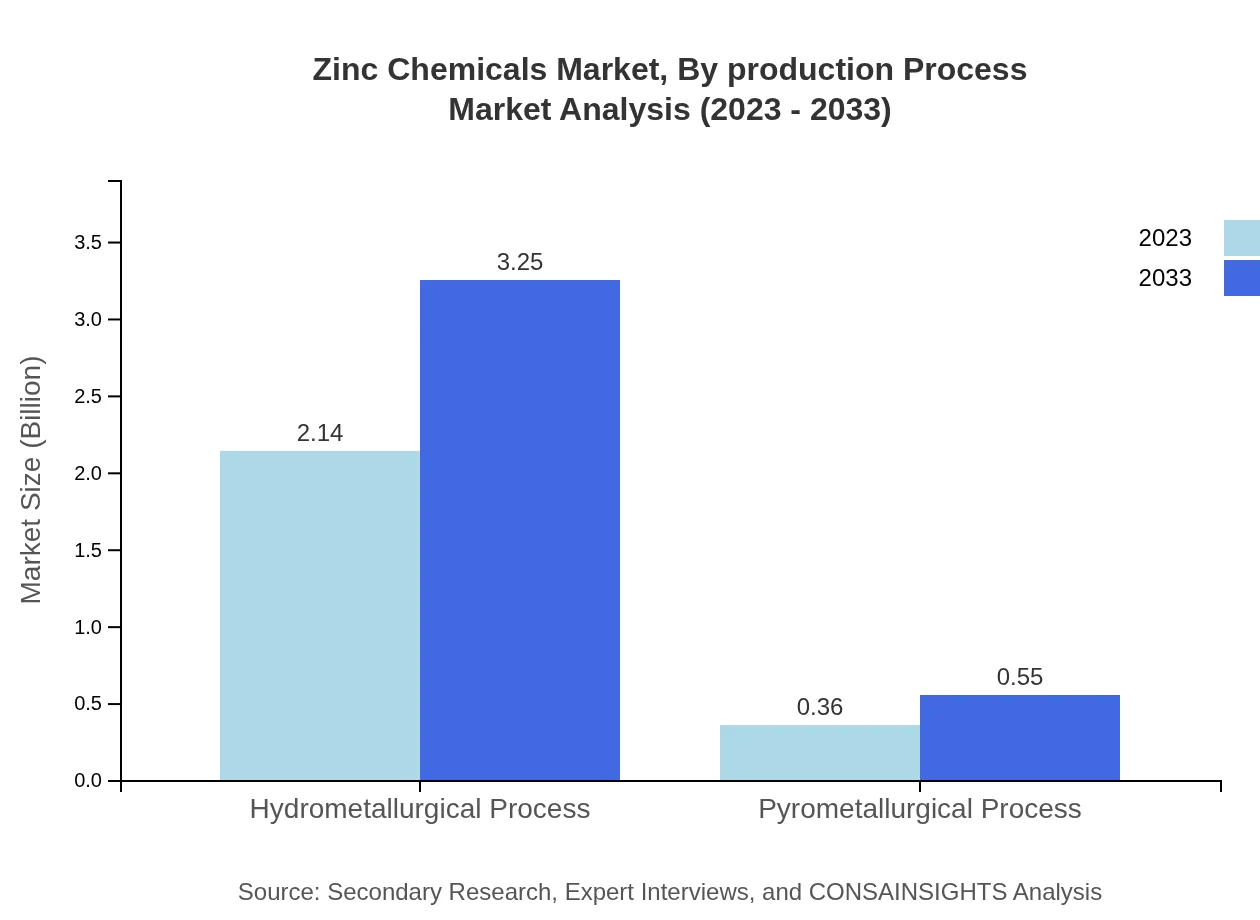

Zinc Chemicals Market Analysis By Production Process

Zinc Chemicals can be produced through various processes, with hydrometallurgical methods leading the way, valued at $2.14 billion in 2023, projected to reach $3.25 billion by 2033. Pyrometallurgical processes form a lesser segment yet maintain relevance for certain product lines.

Zinc Chemicals Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Zinc Chemicals Industry

Zinc Nacional:

A leading player in the Zinc Chemicals market, Zinc Nacional specializes in the production of high-quality zinc oxide and other related products, serving various applications across industries.American Zinc Recycling Corp.:

Known for its sustainable practices, American Zinc Recycling focuses on the recycling and production of zinc-based products, contributing significantly to the Zinc Chemicals industry.Mitsubishi Materials Corporation:

A major player in the Asian market, Mitsubishi Materials Corporation manufactures a diverse range of zinc chemicals used in electronics, automotive, and construction sectors.Umicore:

Umicore is recognized for its innovative solutions in the Zinc Chemicals space, emphasizing sustainability and performance across its product lines.We're grateful to work with incredible clients.

FAQs

What is the market size of zinc Chemicals?

The zinc chemicals market is valued at approximately $2.5 billion in 2023, with a projected CAGR of 4.2% through 2033. This steady growth indicates a robust demand across various sectors including rubber, agriculture, and construction.

What are the key market players or companies in the zinc Chemicals industry?

Key players in the zinc chemicals industry include companies such as ZincOx Resources, Mundra Group, and US Zinc. These companies lead in production and innovation, contributing significantly to market dynamics and technological advancements.

What are the primary factors driving the growth in the zinc Chemicals industry?

Growth is driven by increased demand in automotive, construction, and agricultural sectors. Innovations in zinc applications, along with environmental regulations favoring zinc-based products, further bolster market expansion.

Which region is the fastest Growing in the zinc Chemicals?

The fastest-growing region for zinc chemicals is North America, expected to increase from $0.86 billion in 2023 to $1.31 billion by 2033. This growth is supported by advancements in construction and automotive industries.

Does ConsaInsights provide customized market report data for the zinc Chemicals industry?

Yes, ConsaInsights offers customized reports tailored to specific market needs within the zinc-chemicals industry. Clients can request detailed analysis and insights specific to their business objectives.

What deliverables can I expect from this zinc Chemicals market research project?

Deliverables from the market research project include comprehensive reports, market trends analysis, competitive landscape evaluations, and segmented data across various regions and applications for informed decision-making.

What are the market trends of zinc Chemicals?

Current trends include a shift toward sustainable zinc applications, increased usage in electric vehicles, and a rising focus on health-oriented products. The market is also seeing innovations in production processes and materials.