Advanced Structural Ceramics Market Report

First published: 04 October 2024 | Last updated: 02 February 2026 | Report Code: advanced-structural-ceramics

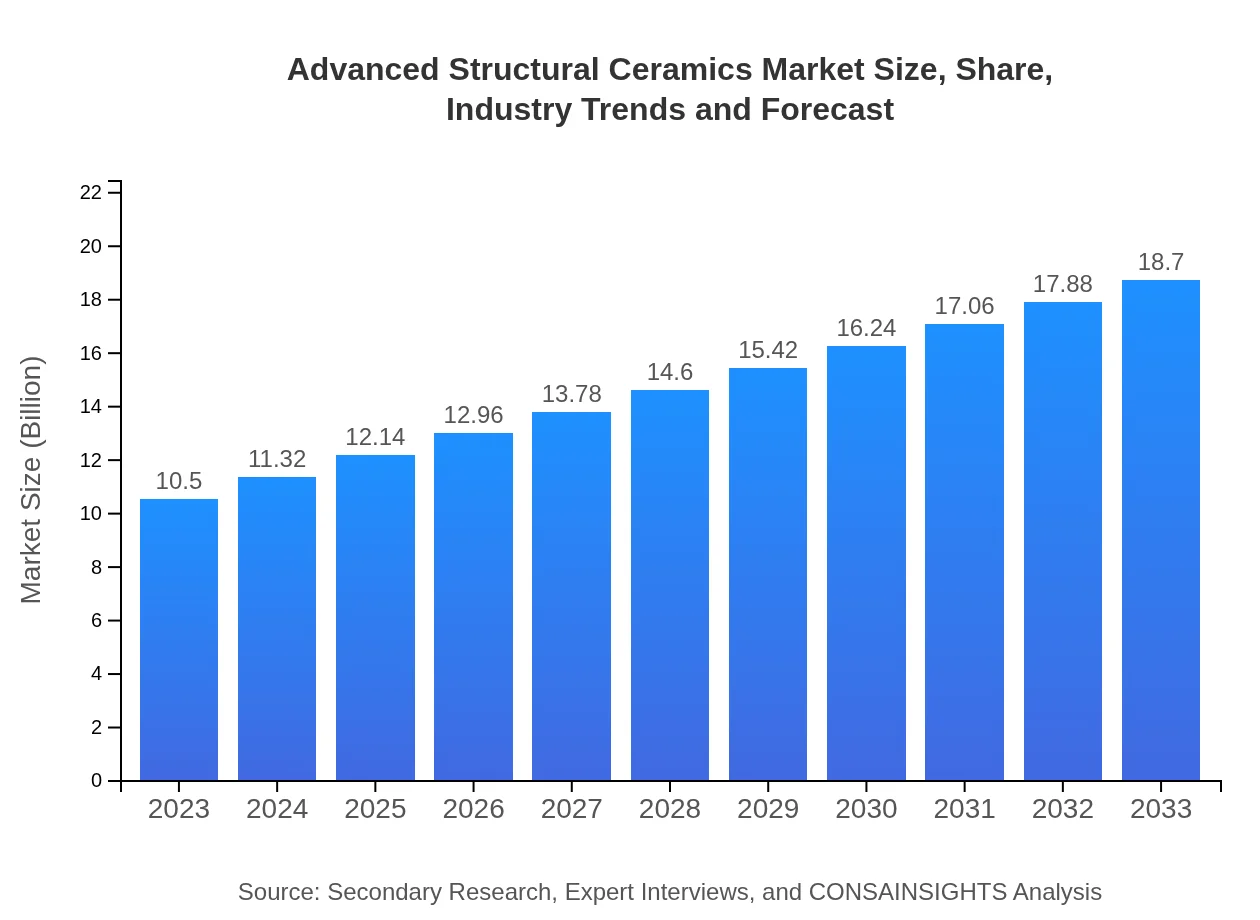

Advanced Structural Ceramics Market — USD 10.5 billion in 2023, Growing to USD 18.70B by 2033 at 5.8% CAGR

This report provides a comprehensive analysis of the Advanced Structural Ceramics market, highlighting market trends, size projections, segmentation, and insights from 2023 to 2033. It aims to deliver key data and forecasts relevant to stakeholders in the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $10.50 Billion |

| CAGR (2023-2033) | 5.8% |

| 2033 Market Size | $18.70 Billion |

| Top Companies | CeramTec, Kyocera Corporation, Morgan Advanced Materials |

| Published Date | 04 October 2024 |

| Last Modified Date | 02 February 2026 |

Advanced Structural Ceramics Market Overview

Customize Advanced Structural Ceramics Market Report market research report

- ✔ Get in-depth analysis of Advanced Structural Ceramics market size, growth, and forecasts.

- ✔ Understand Advanced Structural Ceramics's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Advanced Structural Ceramics

What is the Market Size & CAGR of Advanced Structural Ceramics market in 2023?

Advanced Structural Ceramics Industry Analysis

Advanced Structural Ceramics Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Advanced Structural Ceramics Market Analysis Report by Region

Europe Advanced Structural Ceramics Market Report:

The European Advanced Structural Ceramics market is valued at $3.52 billion in 2023 and is anticipated to reach $6.26 billion by 2033. Government initiatives promoting sustainability and lightweight materials are key growth drivers in this region.Asia Pacific Advanced Structural Ceramics Market Report:

In the Asia Pacific region, the Advanced Structural Ceramics market is estimated to be valued at $1.95 billion in 2023, growing to $3.47 billion by 2033. Rapid industrialization and increasing demand for high-performance materials drive this growth, with China leading in production and consumption.North America Advanced Structural Ceramics Market Report:

North America holds a significant share, valued at $3.67 billion in 2023, projected to grow to $6.54 billion by 2033. The demand from the aerospace and defense sectors propels market growth, alongside continued innovations.South America Advanced Structural Ceramics Market Report:

The South American market for Advanced Structural Ceramics is smaller, valued at $0.86 billion in 2023 and expected to rise to $1.52 billion by 2033. The growth is primarily driven by emerging market economies investing in infrastructure and advanced technologies.Middle East & Africa Advanced Structural Ceramics Market Report:

In the Middle East and Africa, the market is valued at $0.51 billion in 2023 and is expected to grow to $0.90 billion by 2033, supported by increasing investments in technology and manufacturing capabilities.Tell us your focus area and get a customized research report.

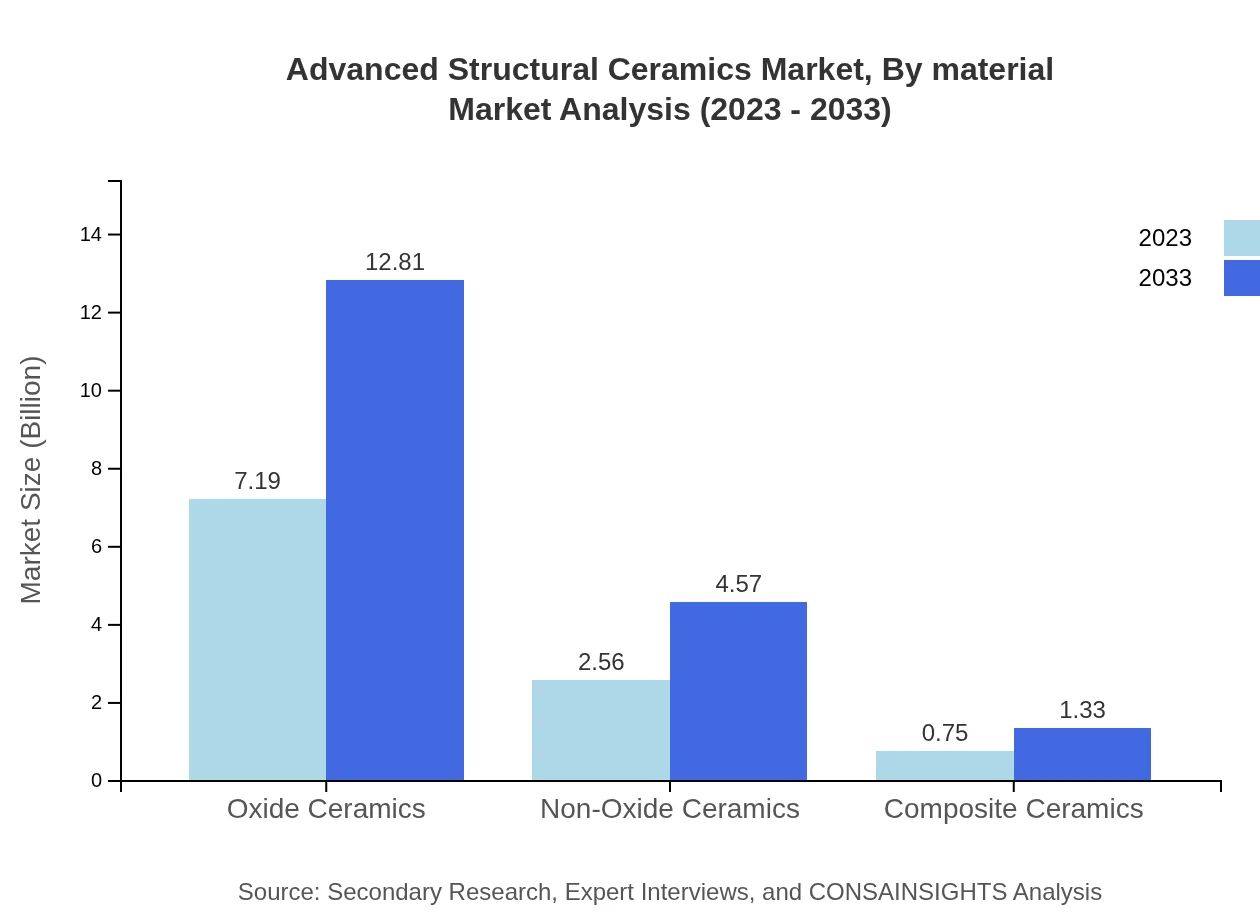

Advanced Structural Ceramics Market Analysis By Material

The material segments of Advanced Structural Ceramics include oxide ceramics, which dominate the market due to high demand in various applications, accounting for about 68.47% of the market share in 2023. Non-oxide ceramics are also gaining traction, accounting for 24.41% of the market share, while composite ceramics represent 7.12%.

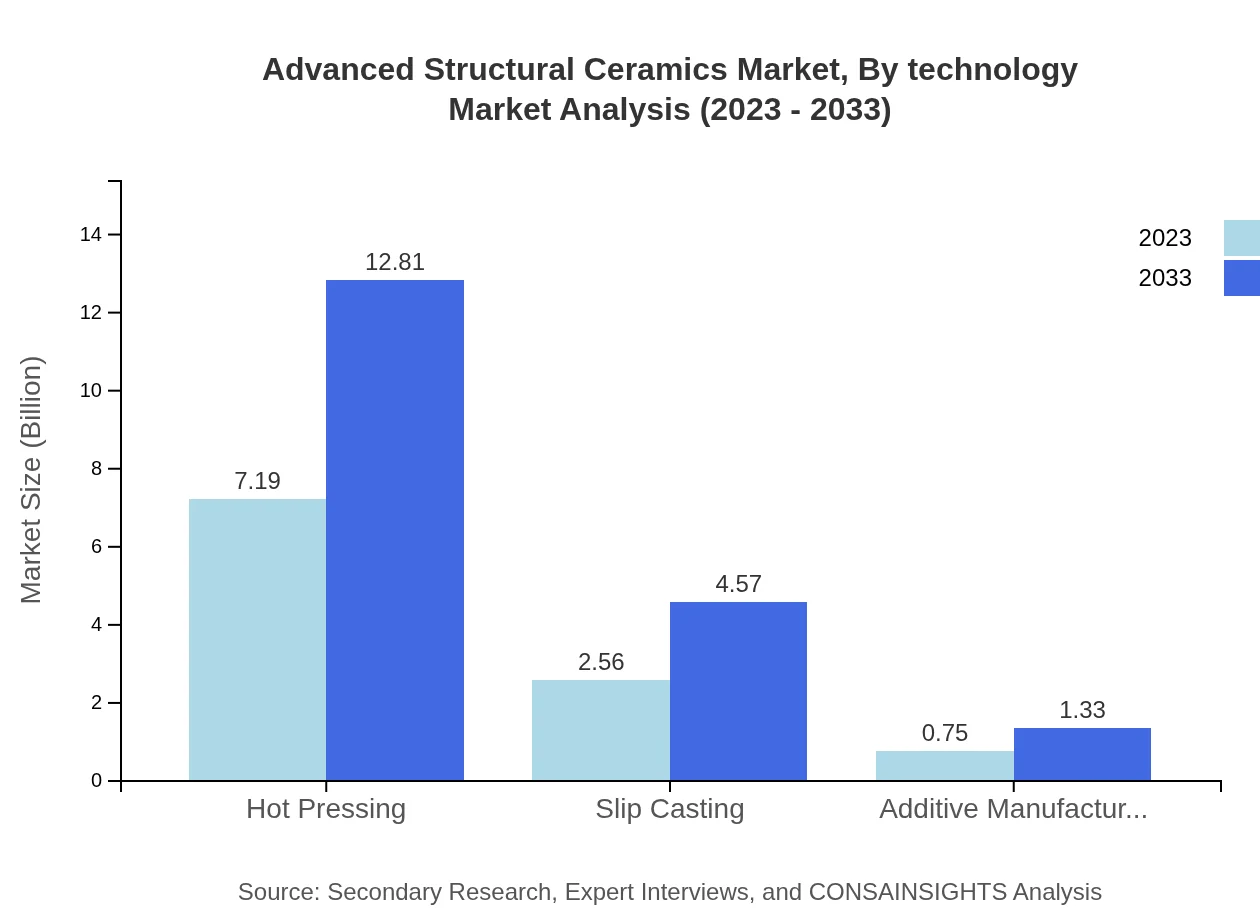

Advanced Structural Ceramics Market Analysis By Technology

In terms of technology, the Hot Pressing technique remains predominant, capturing 68.47% of the market share in 2023. This is followed closely by Slip Casting, making up 24.41% of the market, with the emerging Additive Manufacturing technology representing a growth potential at 7.12%.

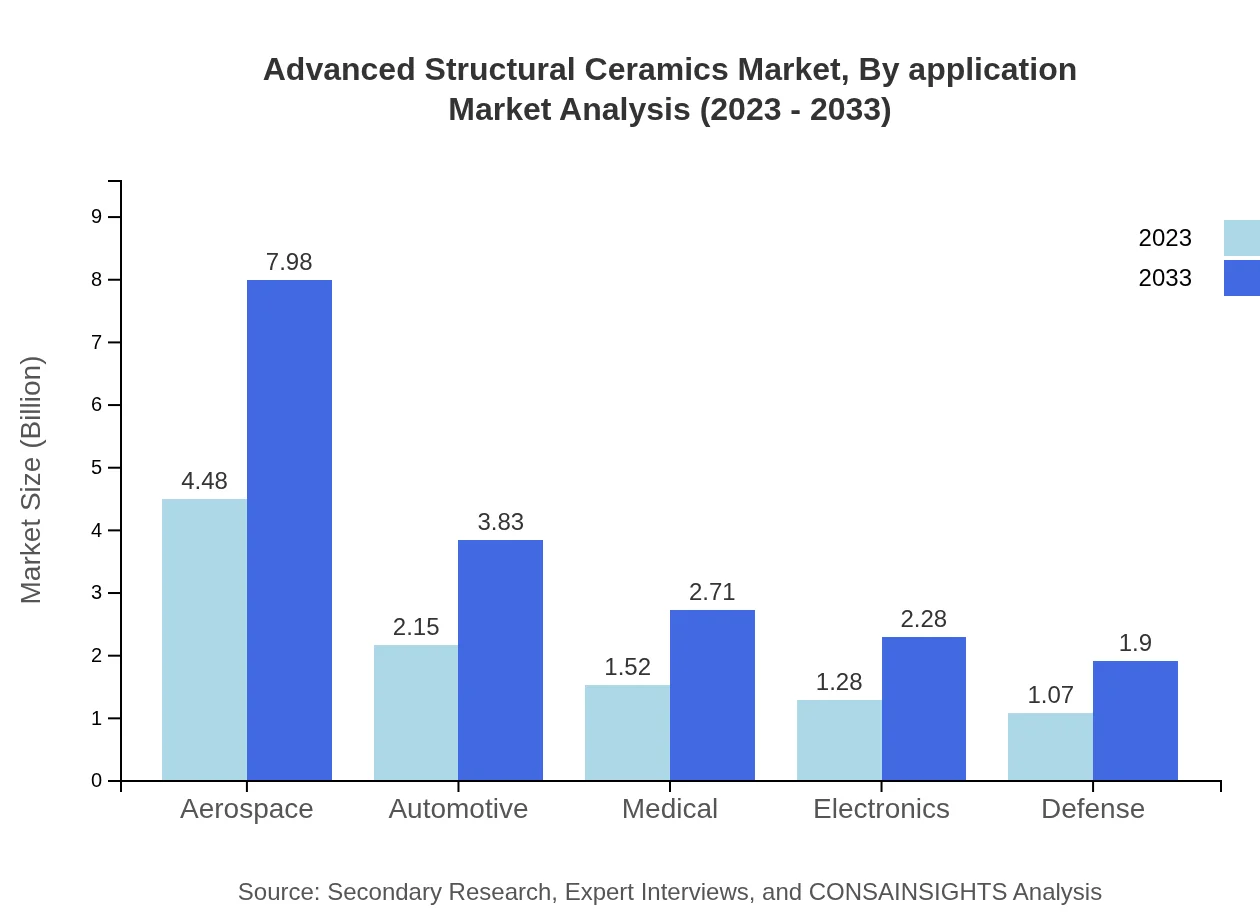

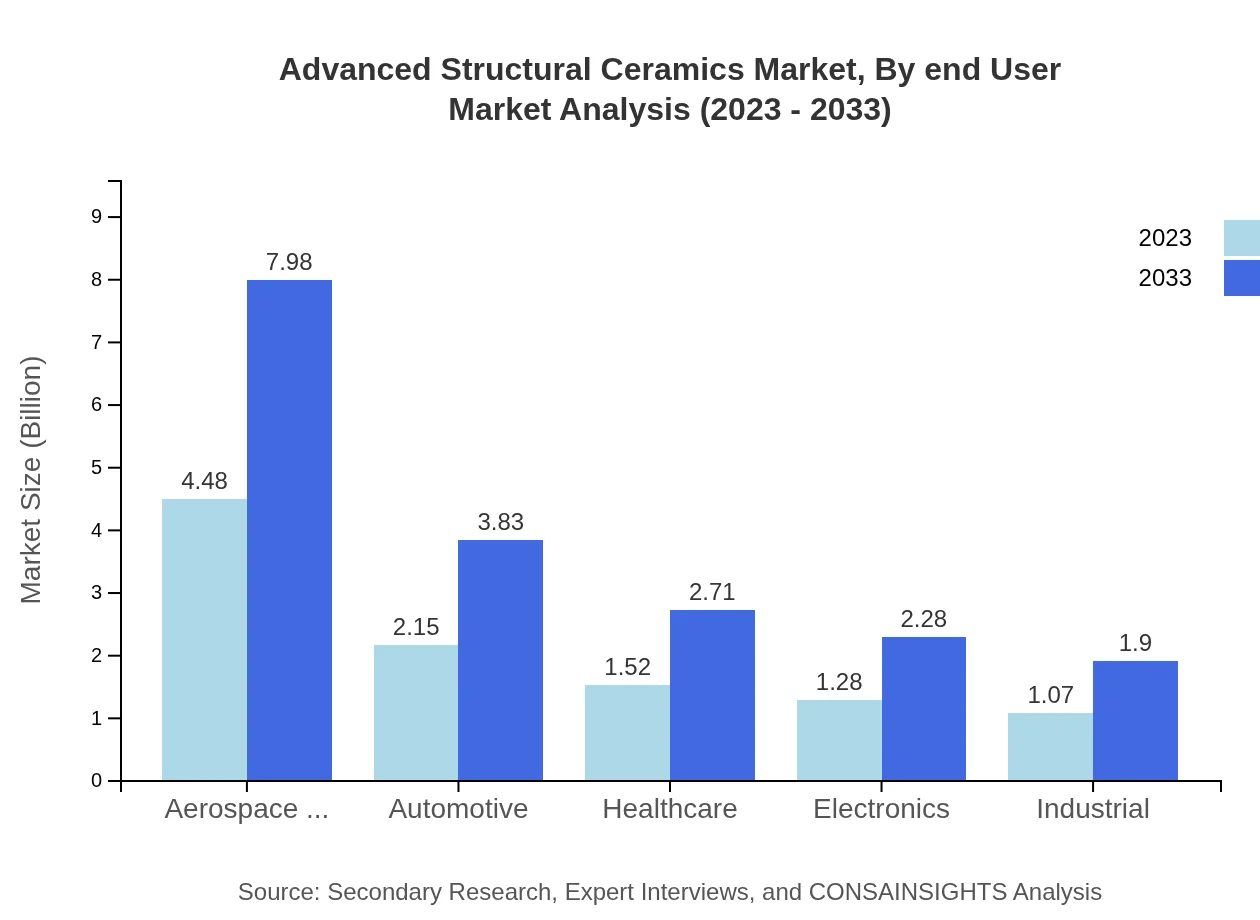

Advanced Structural Ceramics Market Analysis By Application

Applications dominate the aerospace and defense sectors, contributing significantly to market size with a share of 42.66% in 2023. Other key applications include automotive (20.47%), healthcare (14.49%), and electronics (12.2%), which are vital to market growth.

Advanced Structural Ceramics Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Advanced Structural Ceramics Industry

CeramTec:

CeramTec is a leading global manufacturer of advanced ceramics with applications in various industries including medical, automotive, and electronics, emphasizing high-performance and innovative products.Kyocera Corporation:

Kyocera is well-known for its extensive range of ceramic products, leveraging advanced material science to create components for electronics and telecommunications, as well as medical applications.Morgan Advanced Materials:

Morgan Advanced Materials specializes in advanced ceramics and insulation systems, focusing on technological innovation to improve efficiency in electronics and healthcare solutions.We're grateful to work with incredible clients.

FAQs

What is the market size of advanced Structural Ceramics?

The global advanced structural ceramics market is projected to reach approximately USD 10.5 billion by 2033, growing at a CAGR of 5.8% from a value that reflects significant expansion and opportunity for key stakeholders in this sector.

What are the key market players or companies in the advanced Structural Ceramics industry?

Key players in the advanced structural ceramics market include major corporations such as CeramTec, Kyocera Corporation, CoorsTek, and Saint-Gobain. These companies drive innovation and set industry standards, contributing to market growth by expanding product portfolios and enhancing technological capabilities.

What are the primary factors driving the growth in the advanced Structural Ceramics industry?

Growth in the advanced structural ceramics industry is driven by technological advancements, increased demand in aerospace and defense applications, widespread use in medical and automotive sectors, and the developing need for lightweight, high-strength materials in various industries.

Which region is the fastest Growing in the advanced Structural Ceramics?

The fastest-growing region in the advanced structural ceramics market is North America, with the market expected to increase from USD 3.67 billion in 2023 to USD 6.54 billion by 2033. Europe also shows significant growth, rising from USD 3.52 billion to USD 6.26 billion during the same period.

Does ConsaInsights provide customized market report data for the advanced Structural Ceramics industry?

Yes, ConsaInsights offers customized market report data tailored to the specific needs of clients within the advanced structural ceramics industry, allowing for focused insights into market trends, competitive analysis, and regional dynamics.

What deliverables can I expect from this advanced Structural Ceramics market research project?

Deliverables from the advanced structural ceramics market research project include comprehensive reports detailing market size, growth forecasts, segment analysis, competitive landscape, and regional insights to inform strategic decision-making for stakeholders.

What are the market trends of advanced Structural Ceramics?

Current trends in the advanced structural ceramics market include a growing emphasis on sustainable and eco-friendly materials, advancements in manufacturing technologies such as additive manufacturing, and increasing applications in high-performance sectors such as electronics and medical devices.