Automatic Fire Sprinklers Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: automatic-fire-sprinklers

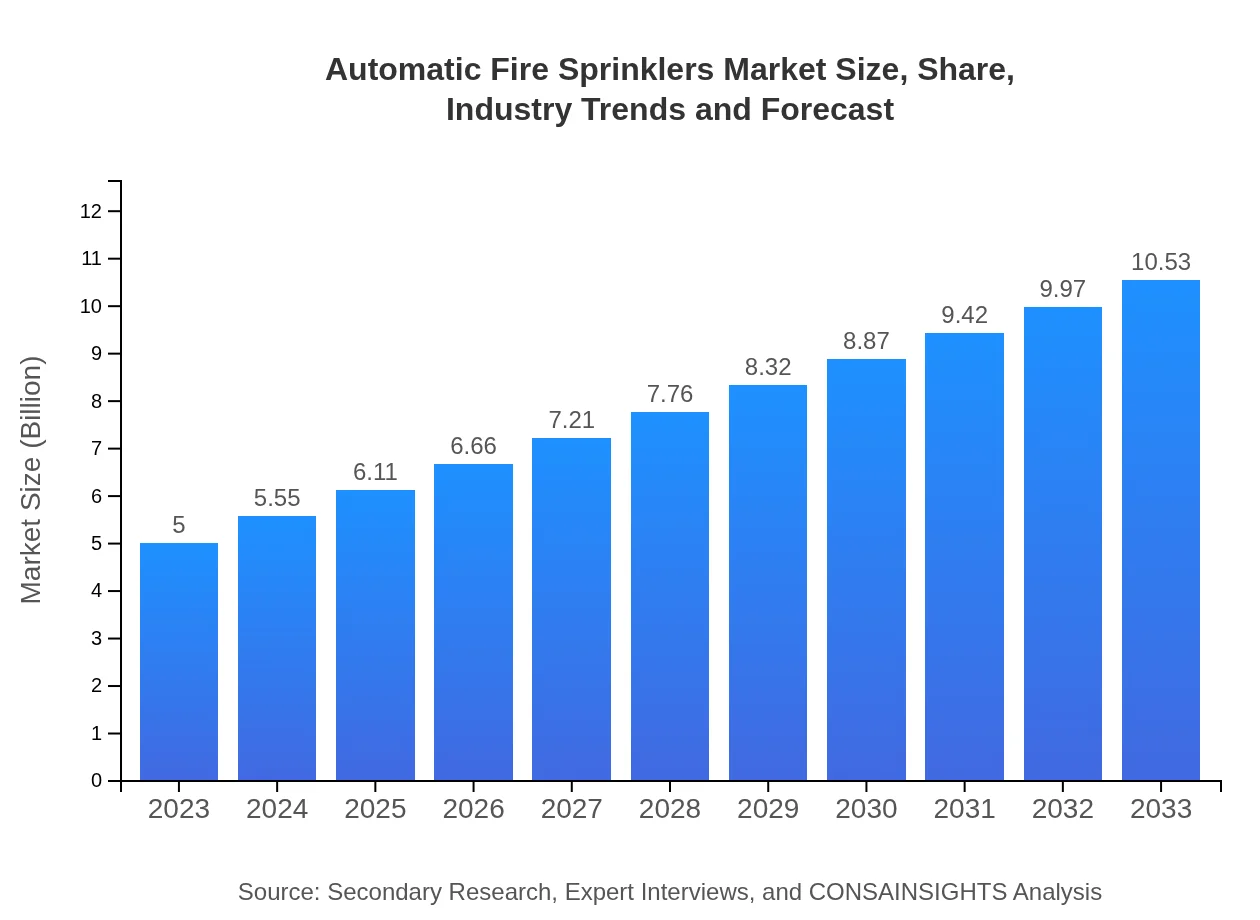

Automatic Fire Sprinklers Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides an in-depth analysis of the Automatic Fire Sprinklers market, covering market size, growth trends, and regional insights for the forecast period from 2023 to 2033.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Tyco SimplexGrinnell, Johnson Controls, Viking Group Inc., Reliable Automatic Sprinkler Co. Inc., Siemens AG |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Automatic Fire Sprinklers Market Overview

Customize Automatic Fire Sprinklers Market Report market research report

- ✔ Get in-depth analysis of Automatic Fire Sprinklers market size, growth, and forecasts.

- ✔ Understand Automatic Fire Sprinklers's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Automatic Fire Sprinklers

What is the Market Size & CAGR of Automatic Fire Sprinklers market in 2023?

Automatic Fire Sprinklers Industry Analysis

Automatic Fire Sprinklers Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Automatic Fire Sprinklers Market Analysis Report by Region

Europe Automatic Fire Sprinklers Market Report:

The European market is poised to increase from $1.47 billion in 2023 to $3.09 billion by 2033. The region's proactive stance on fire safety, supported by rigorous regulations and a growing emphasis on environmental sustainability, particularly in countries like Germany and the UK, sustains market growth.Asia Pacific Automatic Fire Sprinklers Market Report:

In the Asia Pacific, the Automatic Fire Sprinklers market is projected to grow from $0.94 billion in 2023 to $1.97 billion by 2033. Factors such as increasing urbanization, rising industrial activities, and stringent regulations contribute significantly to this growth. Countries like China and India are expected to dominate due to high construction rates and a focus on safety measures.North America Automatic Fire Sprinklers Market Report:

North America is anticipated to see substantial growth from $1.86 billion in 2023 to $3.91 billion by 2033. The presence of key players, along with stringent fire safety regulations, particularly in the United States, drives market expansion, further bolstered by technological advancements.South America Automatic Fire Sprinklers Market Report:

The South America market is expected to expand from $0.12 billion in 2023 to $0.24 billion in 2033. Though smaller in comparison to other regions, the growing focus on industrial safety regulations and urban development initiatives in countries like Brazil and Argentina will foster growth.Middle East & Africa Automatic Fire Sprinklers Market Report:

In the Middle East and Africa, the market is expected to grow from $0.62 billion in 2023 to $1.31 billion by 2033. Rapid urbanization and an increase in construction projects, coupled with heightened safety regulations, particularly in the UAE and Saudi Arabia, contribute to this growth.Tell us your focus area and get a customized research report.

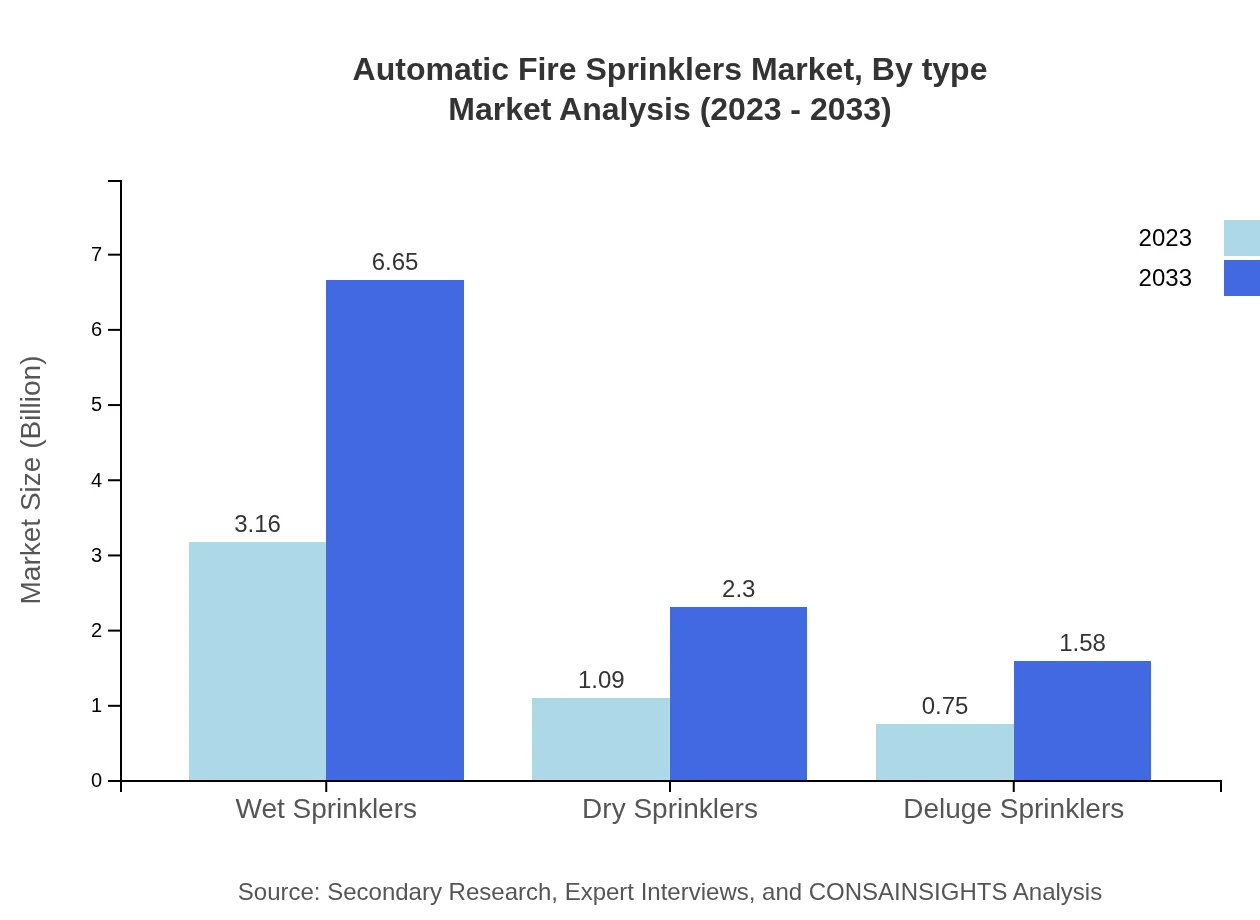

Automatic Fire Sprinklers Market Analysis By Type

The market by type is dominated by wet sprinklers, which accounted for a market size of $3.16 billion in 2023, expected to rise to $6.65 billion by 2033, holding a consistent market share of 63.22%. Dry sprinklers follow with a size of $1.09 billion, growing to $2.30 billion, and share 21.81%. Deluge sprinklers, while smaller, show promise, increasing from $0.75 billion to $1.58 billion in the same period.

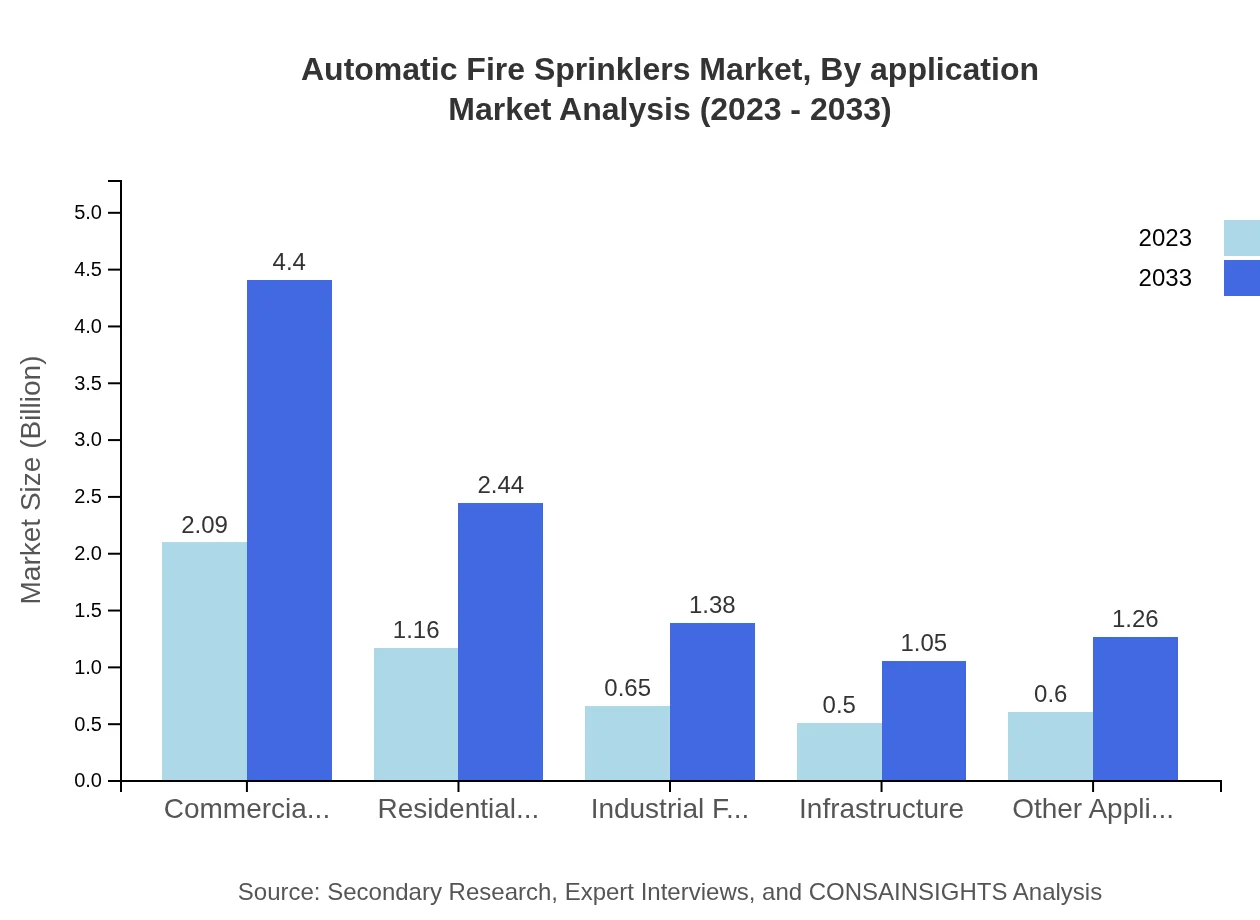

Automatic Fire Sprinklers Market Analysis By Application

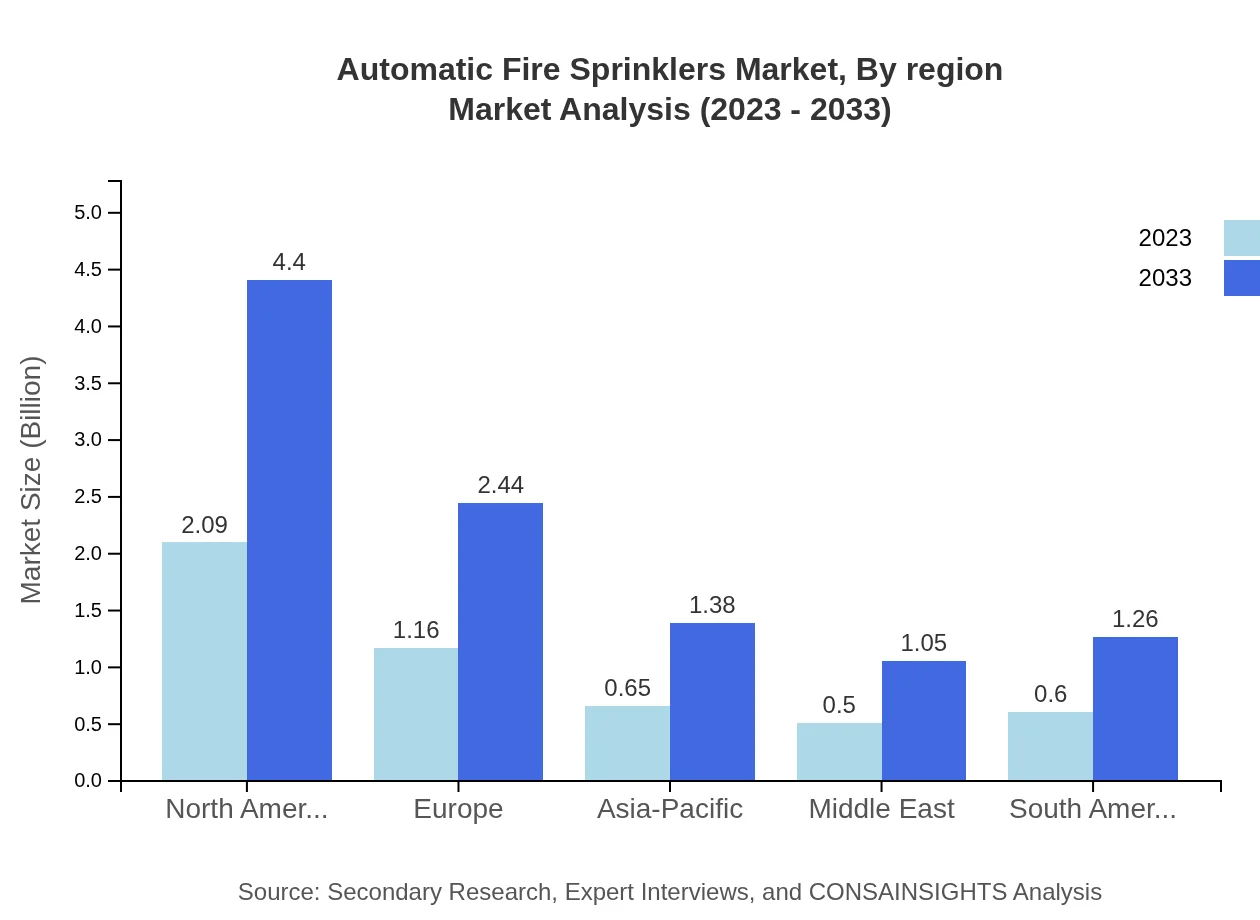

Commercial buildings dominate the application segment with a market size of $2.09 billion in 2023, projected to reach $4.40 billion by 2033, maintaining a share of 41.79%. Residential buildings come next, with $1.16 billion in 2023, growing to $2.44 billion, holding a share of 23.16%. Other notable sectors include industrial facilities and infrastructure, highlighting the widespread need for fire safety across various types of structures.

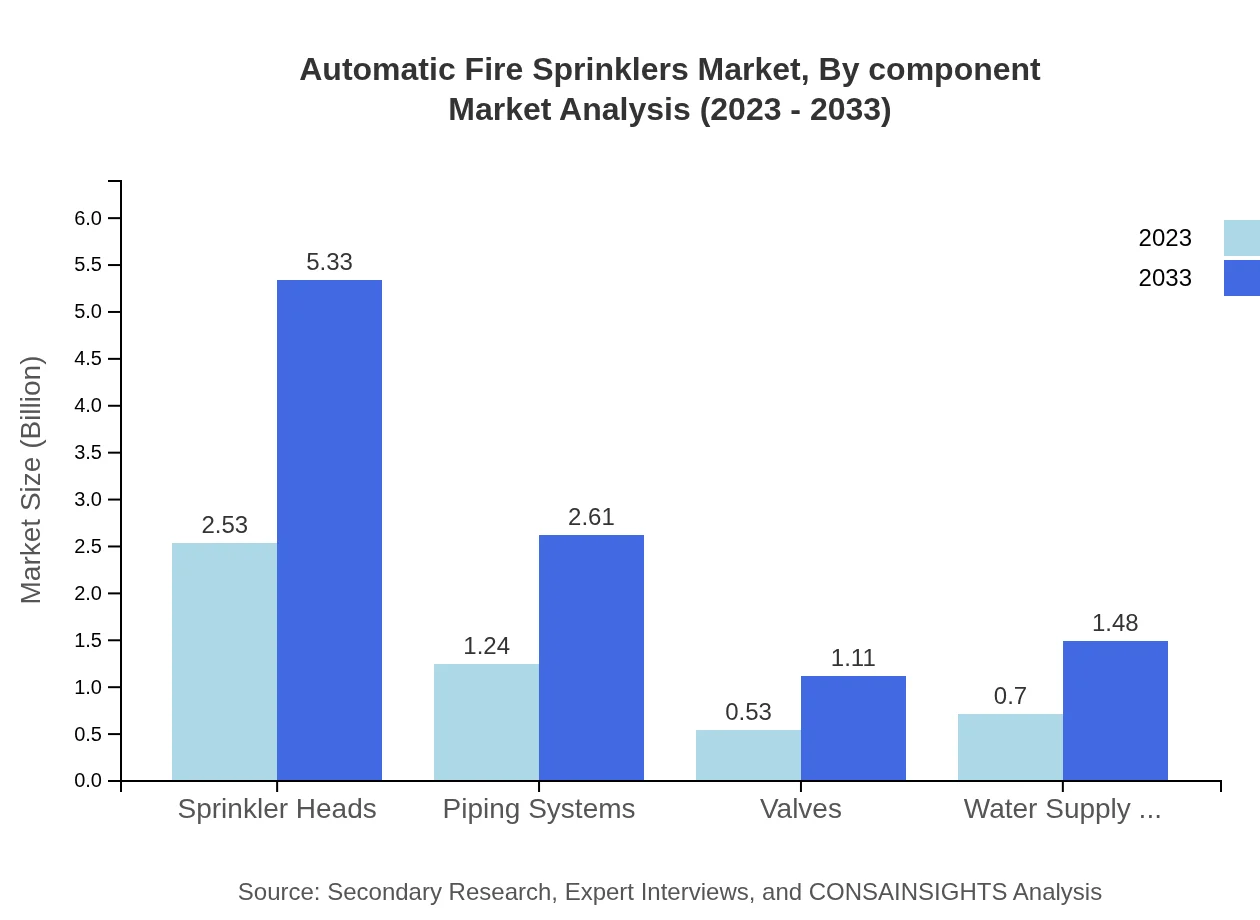

Automatic Fire Sprinklers Market Analysis By Component

In terms of components, sprinkler heads lead the market with a size of $2.53 billion in 2023, expected to rise to $5.33 billion by 2033, representing a 50.61% share. Piping systems and valves also play significant roles, contributing sizes of $1.24 billion and $0.53 billion respectively in 2023, indicating the critical infrastructure required for effective fire protection.

Automatic Fire Sprinklers Market Analysis By Region

Regional analysis shows North America leading the market, followed by Europe and Asia Pacific. North America achieved a market size of $1.86 billion in 2023, expected to grow to $3.91 billion by 2033, representing a share of 41.79%. Europe and APAC are also experiencing robust growth rates, indicating a well-distributed expansion of fire safety technology.

Automatic Fire Sprinklers Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Automatic Fire Sprinklers Industry

Tyco SimplexGrinnell:

A leader in fire protection solutions, offering a wide range of fire sprinkler systems and services aimed at enhancing safety in commercial and industrial sectors.Johnson Controls:

Global leader in diversified technology and multi industrial systems, providing fire safety products and services, including advanced automatic fire sprinklers.Viking Group Inc.:

A major player in the automatic sprinkler systems market, known for innovative fire protection technology and reliable support services across multiple sectors.Reliable Automatic Sprinkler Co. Inc.:

Offers an extensive range of automatic fire protection solutions and fire protection equipment, well-regarded for quality and efficiency.Siemens AG:

A multinational company providing technology solutions, including advanced fire safety products and systems, reflecting a commitment to safety innovations.We're grateful to work with incredible clients.

FAQs

What is the market size of automatic Fire Sprinklers?

The global automatic fire sprinklers market is projected to reach around $5 billion by 2033, growing at a CAGR of 7.5% from 2023. This growth reflects increasing investments in safety systems across various sectors.

What are the key market players or companies in the automatic Fire Sprinklers industry?

Key players in the automatic fire sprinklers market include renowned companies specializing in fire protection systems, contributing significantly to the industry's innovation and market growth.

What are the primary factors driving the growth in the automatic Fire Sprinklers industry?

The growth of the automatic fire sprinklers industry is driven by rising safety regulations, increased urbanization, and heightened awareness about building safety among commercial and residential sectors.

Which region is the fastest Growing in the automatic Fire Sprinklers?

In the automatic fire sprinklers market, North America is anticipated to experience the fastest growth, projected to expand from $1.86 billion in 2023 to $3.91 billion by 2033, at the forefront of safety regulations.

Does ConsaInsights provide customized market report data for the automatic Fire Sprinklers industry?

Yes, ConsaInsights offers customized market report data tailored to specific needs in the automatic fire sprinklers industry, ensuring detailed insights for informed decision-making.

What deliverables can I expect from this automatic Fire Sprinklers market research project?

Expect comprehensive deliverables including market analysis reports, regional insights, segmentation data, and strategic recommendations tailored to the automatic fire sprinklers market.

What are the market trends of automatic Fire Sprinklers?

Current trends in the automatic fire sprinklers market include a shift towards smart automation technologies, integration of IoT in fire protection systems, and increased demand for eco-friendly solutions.