Bone Densitometers Market Report

First published: 08 October 2024 | Last updated: 28 May 2026 | Report Code: bone-densitometers

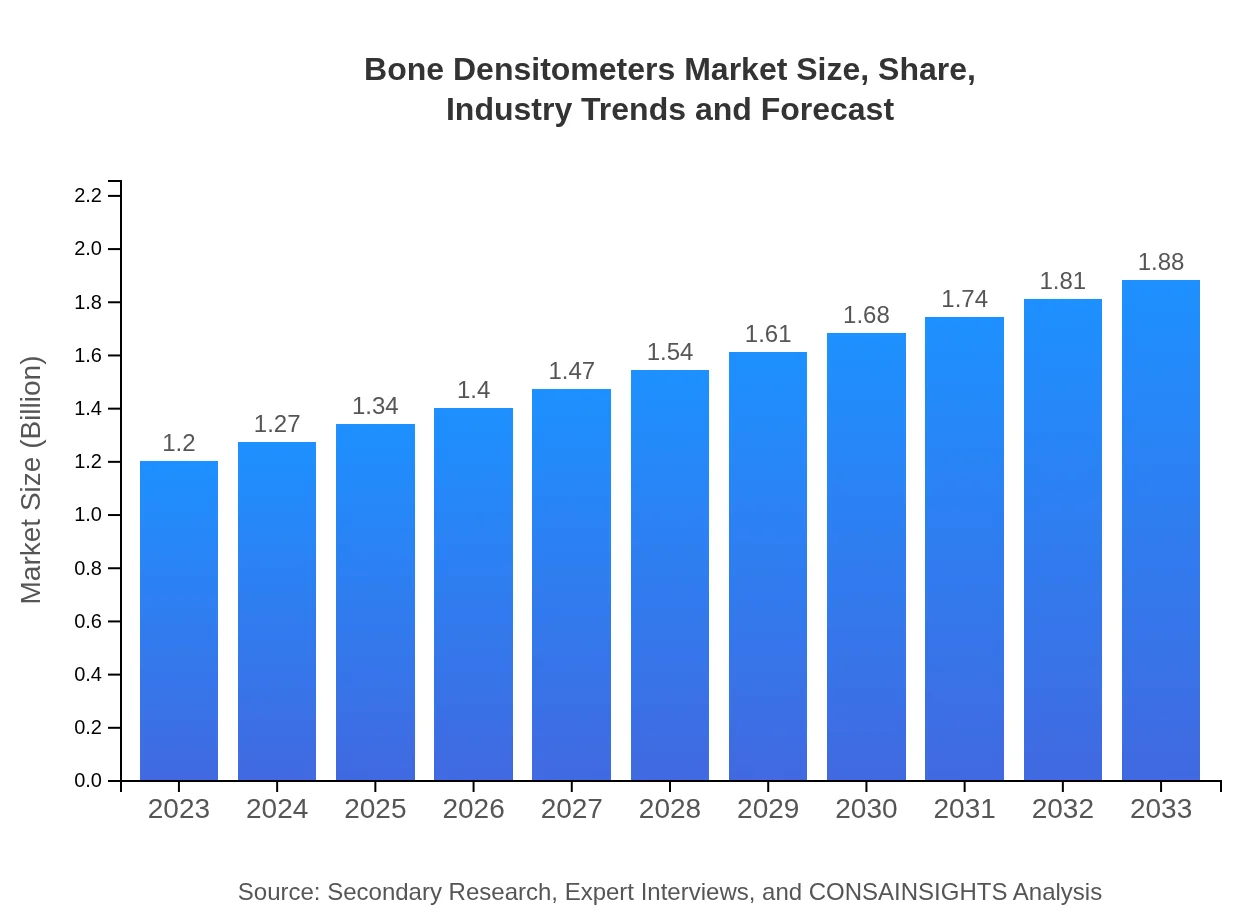

Bone Densitometers Market — USD 1.2 billion in 2023, Growing to USD 1.88B by 2033 at 4.5% CAGR

This report provides a comprehensive analysis of the Bone Densitometers market, including market size, growth trends, regional insights, and forecasts for the period 2023 to 2033. It aims to equip stakeholders with crucial data enabling informed strategic decisions.

Key Takeaways

- Global market value increases from $1.20 Billion in 2023 to $1.88 Billion in 2033, reflecting a 4.5% CAGR over 2023 to 2033.

- North America is the largest region, growing from $0.43 Billion in 2023 to $0.67 Billion in 2033.

- North America is largest regional market; Middle East and Africa is regional market region based on implied CAGR across 2023 to 2033.

- Europe expands from $0.34 Billion in 2023 to $0.53 Billion in 2033; Asia Pacific moves from $0.24 Billion to $0.38 Billion.

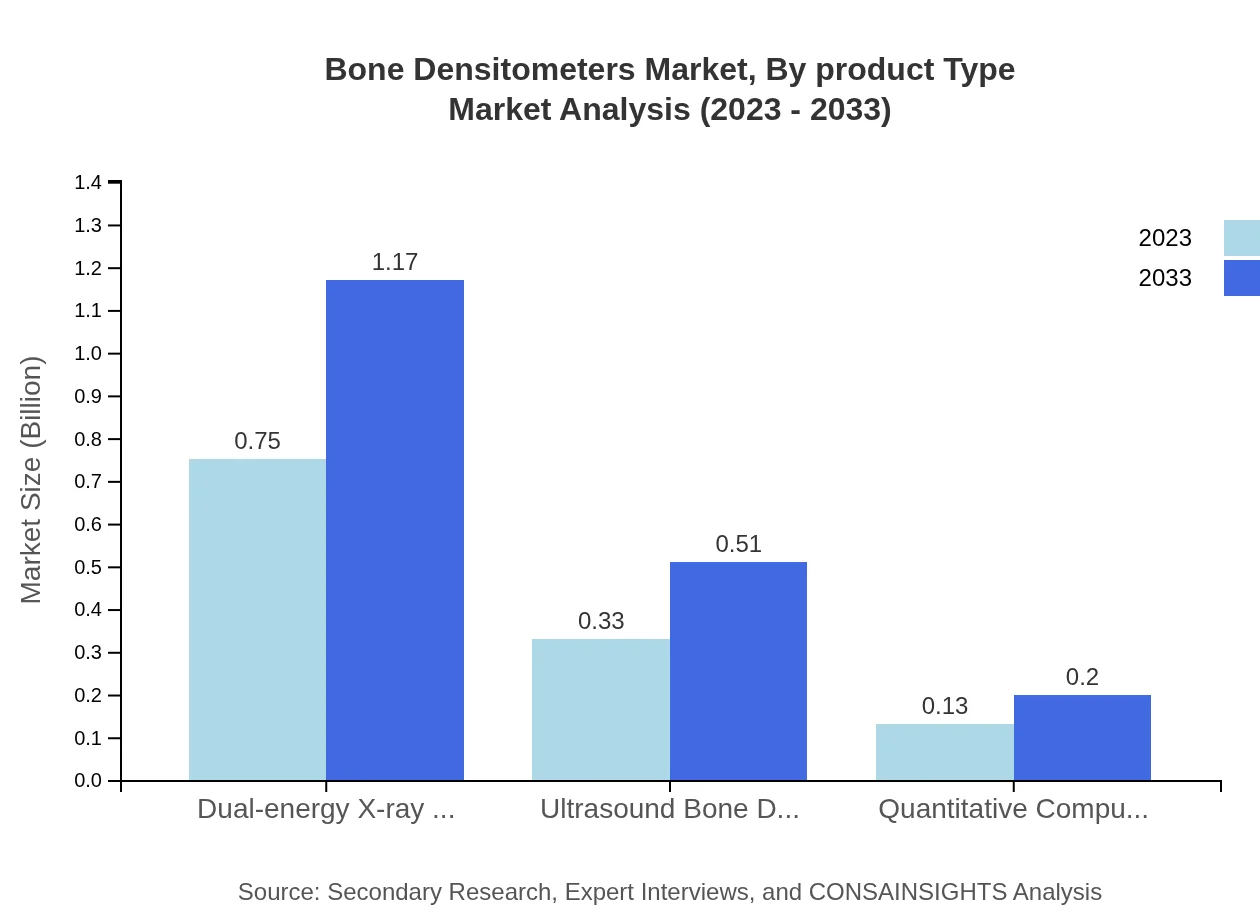

- Key product types include Dual-energy X-ray Absorptiometry (DXA), ultrasound devices and Quantitative Computed Tomography (QCT); major players include Hologic, Inc., GE Healthcare, Siemens Healthineers and osteoporosis Diagnostics, Inc.

Bone Densitometers Market Report — Executive Summary

Regional analysis shows North America as largest market and Middle East and Africa as fastest-growing region by implied CAGR. The Bone Densitometers Market Report examines factors shaping demand for diagnostic equipment used to measure bone mineral density. The market was valued at $1.20 Billion in 2023 and is forecast to reach $1.88 Billion by 2033 at a 4.5% CAGR for 2023 to 2033. Growth is supported by demographic shifts, rising prevalence of bone disorders, and wider adoption of standard assessment techniques. Product innovation—especially in DXA, ultrasound systems and QCT—and improved software integration are notable trends. Regional dynamics include North America as the largest market and Middle East and Africa as the regional market region. The report analyzes segmentation by product type, application, end user and distribution channel, and profiles leading companies such as Hologic, Inc., GE Healthcare, Siemens Healthineers and osteoporosis Diagnostics, Inc. Findings are intended to support strategic planning, investment decisions and competitive assessment within the life-sciences sector.

Key Growth Drivers

- Increasing incidence of bone-related conditions and greater screening demand among aging populations.

- Wider clinical acceptance of DXA and improvements in imaging accuracy driving equipment replacement and adoption.

- Investment in integrated software solutions that streamline diagnostics and reporting workflows.

- Expansion of diagnostic services in hospitals and clinics, increasing demand through established end users.

- Manufacturers’ focus on product innovation and validation to meet evolving clinical needs and regulatory expectations.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $1.20 Billion |

| CAGR (2023-2033) | 4.5% |

| 2033 Market Size | $1.88 Billion |

| Top Companies | Hologic, Inc., GE Healthcare, Siemens Healthineers, osteoporosis Diagnostics, Inc. |

| Published Date | 08 October 2024 |

| Last Modified Date | 28 May 2026 |

Bone Densitometers Market Overview

Customize Bone Densitometers Market Report market research report

- ✔ Get in-depth analysis of Bone Densitometers market size, growth, and forecasts.

- ✔ Understand Bone Densitometers's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Bone Densitometers

What is the Market Size & CAGR of Bone Densitometers Market Report market in 2023?

Bone Densitometers Industry Analysis

Bone Densitometers Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Bone Densitometers Market Report Market Analysis Report by Region

Europe Bone Densitometers Market Report:

Europe grows from $0.34 Billion in 2023 to $0.53 Billion in 2033. Demand is influenced by increasing awareness of bone health, expanding diagnostic services in clinical settings, and incorporation of advanced imaging methods into practice.Asia Pacific Bone Densitometers Market Report:

Asia Pacific grows from $0.24 Billion in 2023 to $0.38 Billion in 2033. Market expansion is tied to broader access to diagnostic care, growing geriatric populations and gradual adoption of standard bone density assessment technologies.North America Bone Densitometers Market Report:

North America is largest regional market, rising from $0.43 Billion in 2023 to $0.67 Billion in 2033. 43 Billion in 2023 and is expected to grow to $0.67 Billion by 2033. Regional adoption is driven by established clinical protocols, higher screening rates and investment in hospital-based diagnostic infrastructure, supporting the region’s leading market position.South America Bone Densitometers Market Report:

Latin America grows from $0.11 Billion in 2023 to $0.18 Billion in 2033. Growth drivers include expanding healthcare infrastructure, rising diagnostic service availability and increasing attention to preventive bone health screening.Middle East & Africa Bone Densitometers Market Report:

Middle East and Africa is fastest-growing region by implied CAGR, increasing from $0.07 Billion in 2023 to $0.12 Billion in 2033. 07 Billion in 2023 to $0.12 Billion in 2033 and is identified as the regional growth market with an implied 5.54% CAGR. Expansion reflects emerging diagnostic capacity, greater screening initiatives and investment in imaging technologies.Tell us your focus area and get a customized research report.

Research Methodology

Bone Densitometers Market Analysis By Product Type

The market for Bone Densitometers is segmented by product type into DXA, ultrasound, and QCT systems. DXA continues to account for the majority share, driven by its accuracy in measuring bone mineral density. In 2023, DXA holds approximately 62.29% of the market share, with expectations to maintain this share through 2033 as adoption rates remain high. Ultrasound bone densitometers, at 27.2%, and QCT systems, at 10.51%, also play notable roles, particularly in specialty clinics and research settings.

Bone Densitometers Market Analysis By Application

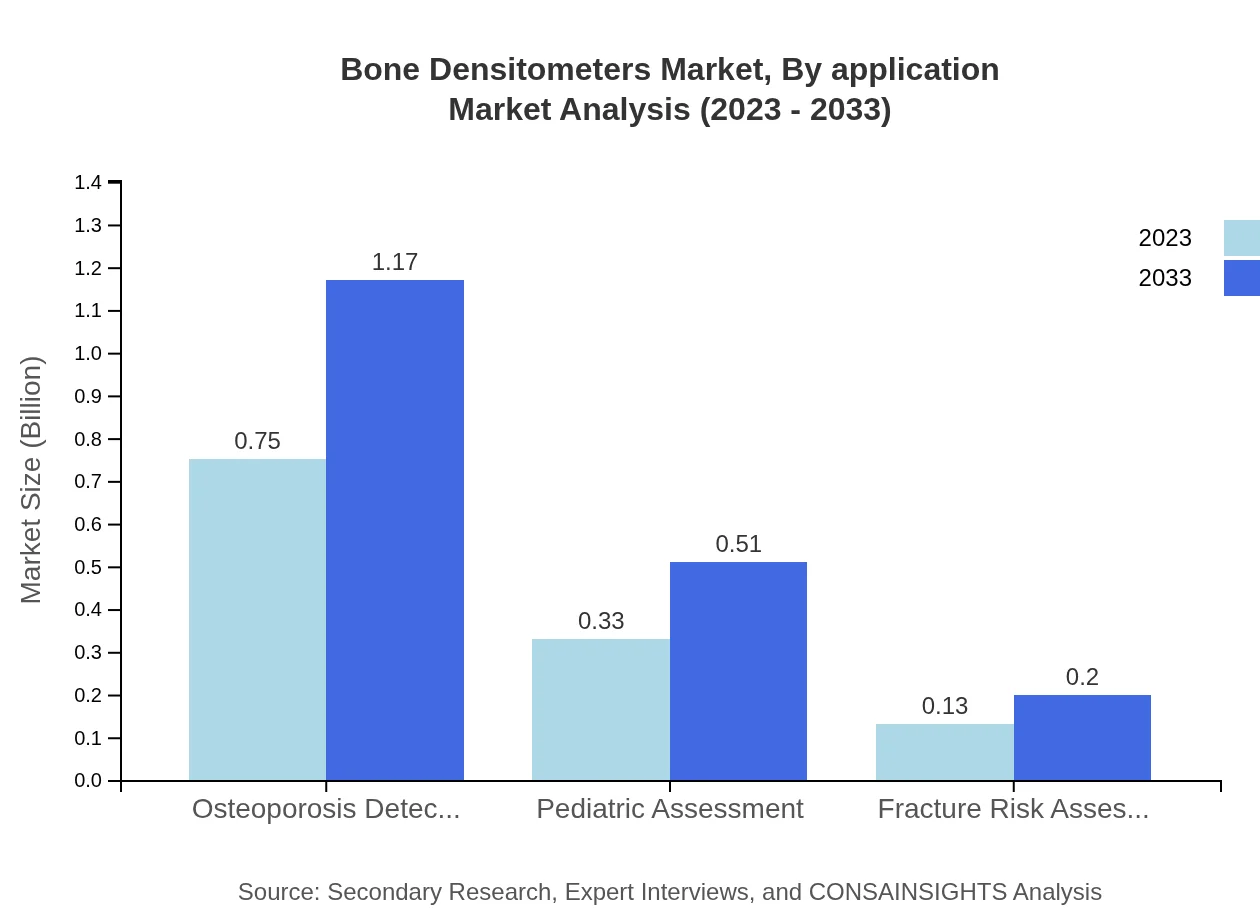

Applications of Bone Densitometers include osteoporosis detection, pediatric assessment, and fracture risk assessment. Osteoporosis detection dominates this segment, representing 62.29% of market size in 2023, and is expected to reach similar levels by 2033. Pediatric assessments and fracture risk evaluations are likewise significant, standing at 27.2% and 10.51%, respectively.

Bone Densitometers Market Analysis By End User

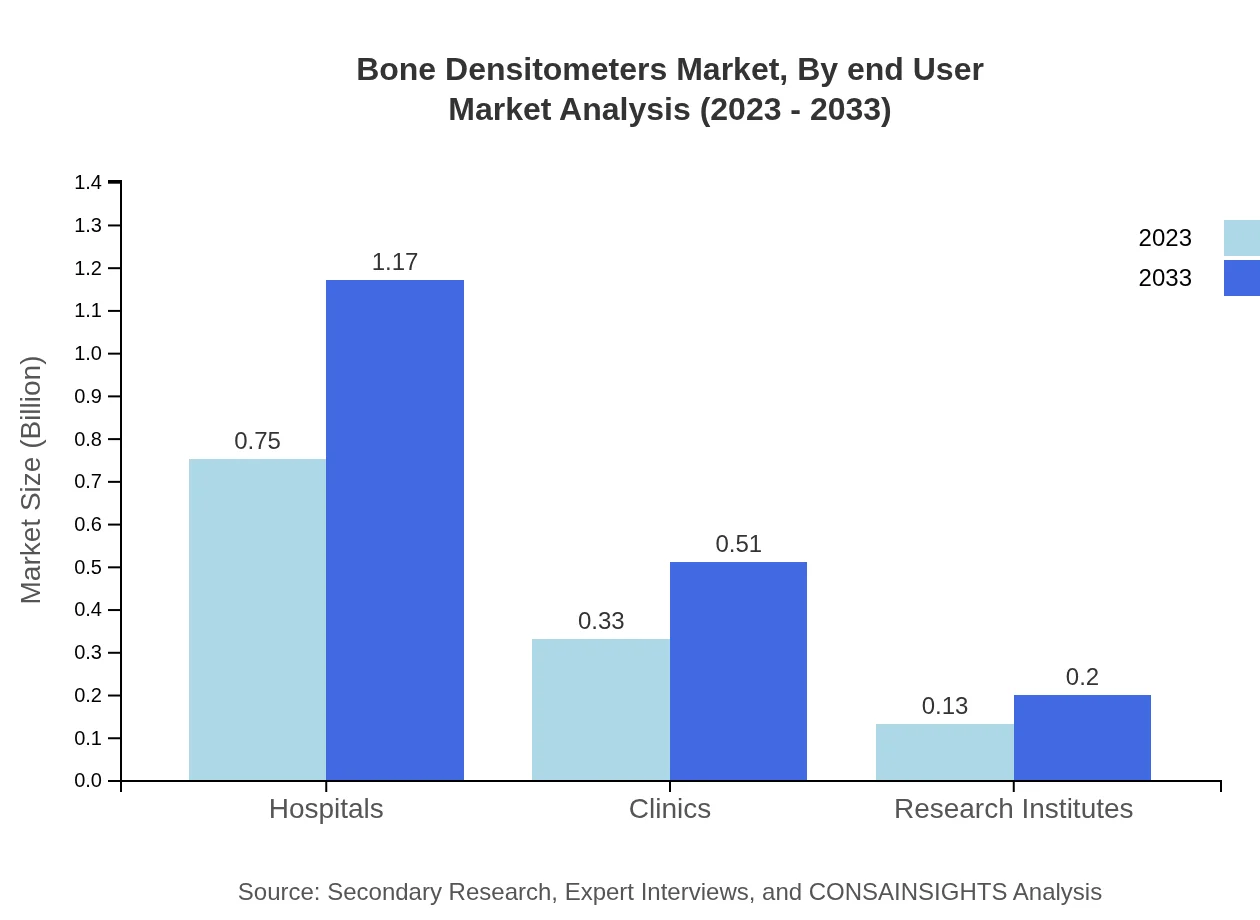

Hospitals, clinics, and research institutes are the primary end-users of Bone Densitometers. Hospitals account for a substantial 62.29% market share in 2023, expected to grow to 62.29% by 2033. Clinics and research institutes follow at 27.2% and 10.51%, respectively, reflecting their integral roles in patient care and research advancements.

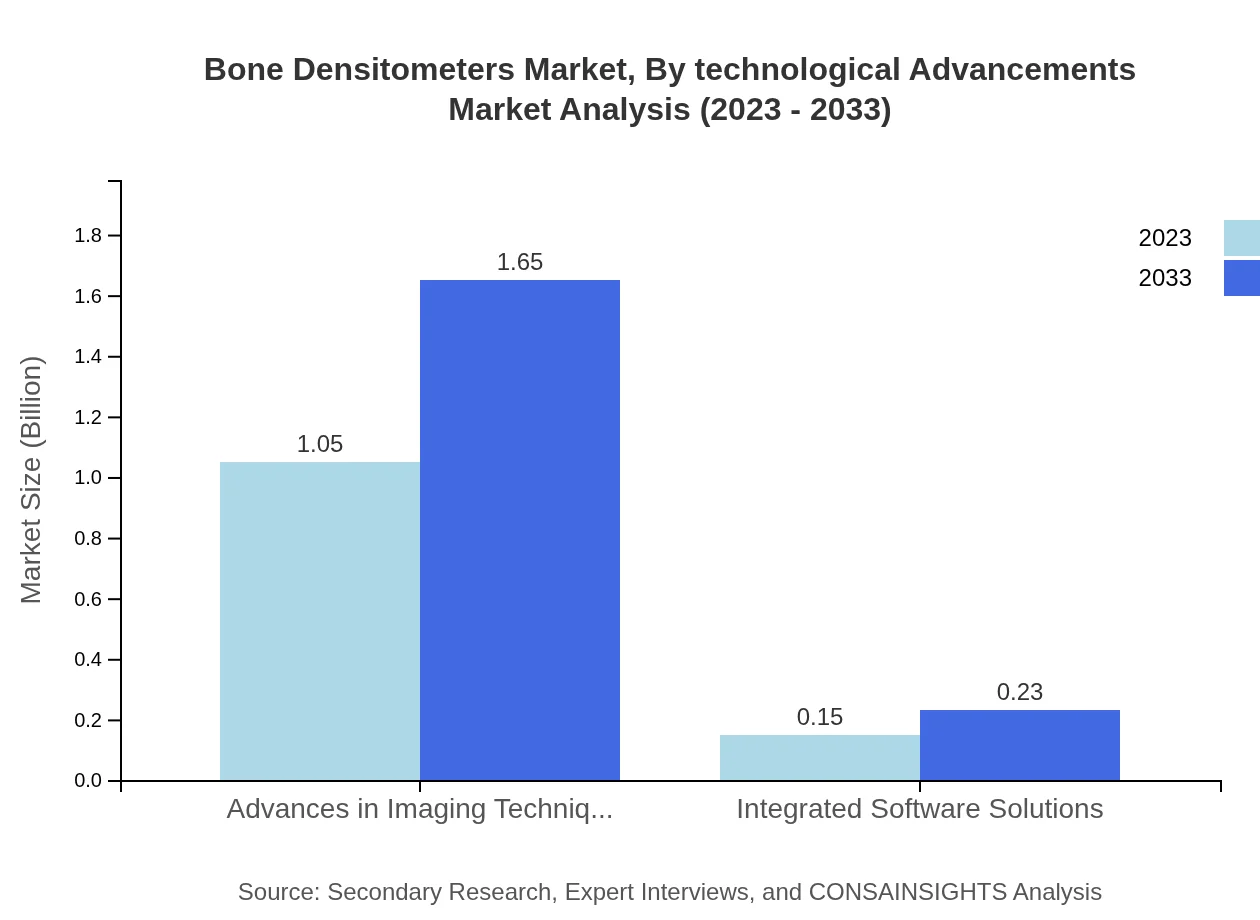

Bone Densitometers Market Analysis By Technological Advancements

Technological advancements such as integrated software solutions and improved imaging techniques are vital in enhancing the functionality and efficiency of Bone Densitometers. In 2023, solutions contributing to this segment capture 87.74% market share with a forecasted increase leading to similar shares in 2033.

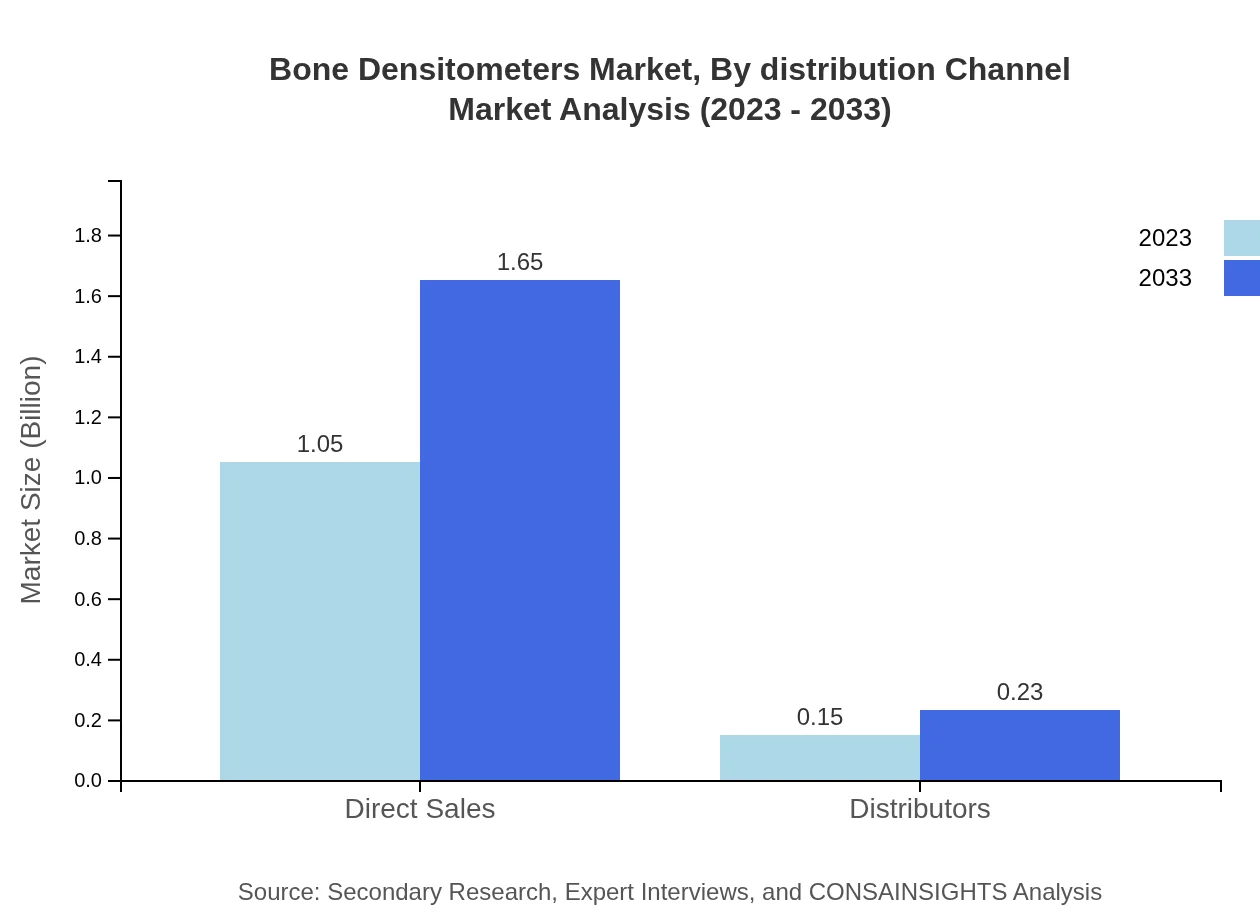

Bone Densitometers Market Analysis By Distribution Channel

The market’s distribution channels include direct sales and distributors. Direct sales dominate significantly, capturing about 87.74% in 2023, anticipated to retain this market share until 2033. The distributor channel remains crucial, holding 12.26% share as it offers access to broader healthcare facilities.

Bone Densitometers Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Bone Densitometers Industry

Hologic, Inc.:

Hologic is a leading manufacturer specializing in medical imaging and diagnostic products for women’s health. Known for its innovative DXA systems, Hologic drives advancements in bone health assessments.GE Healthcare:

GE Healthcare is a renowned provider of medical imaging equipment, including bone densitometers, with a strong focus on technology integration and enhancing patient care through innovative solutions.Siemens Healthineers:

Siemens Healthineers is a pioneer in imaging technologies and medical devices, producing advanced solutions that facilitate accurate bone density measurements for diagnosis and treatment.osteoporosis Diagnostics, Inc.:

Focused on osteoporosis diagnostic tools, this company is known for its advanced densitometry solutions tailored towards enhancing clinical outcomes.We're grateful to work with incredible clients.

FAQs

What is the market size of the Bone Densitometers Market Report in 2023?

The reported market size for 2023 is $1.20 Billion, representing the base-year valuation for the 2023 to 2033 forecast period.

What is the projected market size in 2033?

The market is projected to reach $1.88 Billion by 2033 according to the 2023 to 2033 forecast.

What is CAGR of the Bone Densitometers Market Report?

The Compound Annual Growth Rate (CAGR) for the forecast period 2023 to 2033 is 4.5% as provided in the report data.

Which region is the fastest Growing in the Bone Densitometers Market Report market?

Middle East and Africa is the fastest-growing region, projected to expand from $0.07 Billion in 2023 to $0.12 Billion in 2033, reflecting an implied 5.54% CAGR over the forecast period.

Why is Middle East and Africa noted in the report?

Middle East and Africa is specified as the regional market region, increasing from $0.07 Billion in 2023 to $0.12 Billion in 2033 with an implied 5.54% CAGR.

Which product types are included in the segmentation?

Product-type segmentation includes Dual-energy X-ray Absorptiometry (DXA), Ultrasound Bone Densitometers and Quantitative Computed Tomography (QCT) as listed subsegments.

Who are the top companies mentioned in the report?

Top firms cited in the market data include Hologic, Inc., GE Healthcare, Siemens Healthineers and osteoporosis Diagnostics, Inc.

What end users are covered in the market segmentation?

End-user segmentation includes Hospitals, Clinics and Research Institutes as the specified subsegments in the dataset.

How big is Europe in 2023 and 2033?

Europe is reported at $0.34 Billion in 2023 and is projected to reach $0.53 Billion by 2033 per the regional facts.

How big is Asia Pacific in 2023 and 2033?

Asia Pacific is noted at $0.24 Billion in 2023 and is forecast to grow to $0.38 Billion by 2033 according to the input data.