Ophthalmology Diagnostics Market Report

First published: 08 October 2024 | Last updated: 25 May 2026 | Report Code: ophthalmology-diagnostics

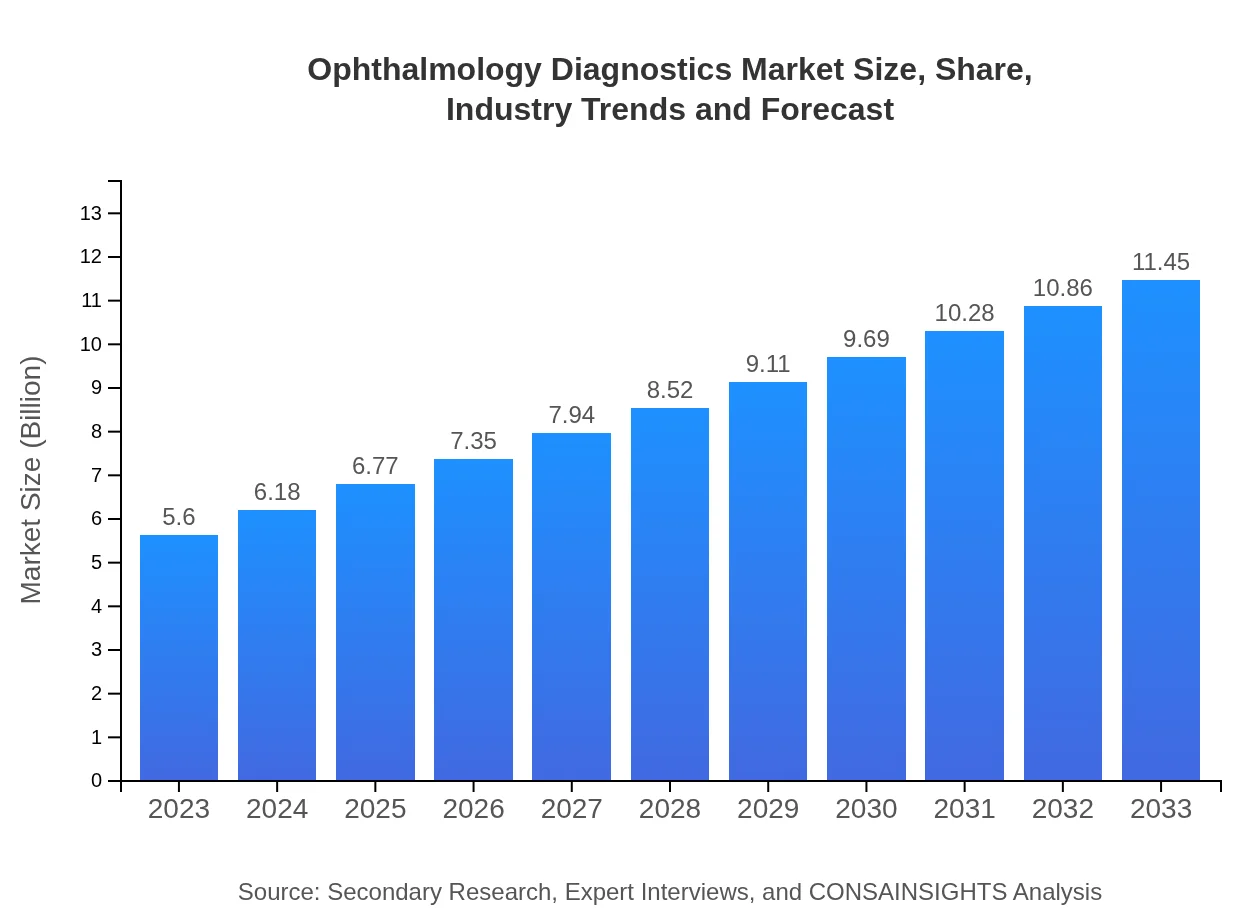

Ophthalmology Diagnostics Market — USD 5.6 billion in 2023, Growing to USD 11.45B by 2033 at 7.2% CAGR

This report provides comprehensive insights into the Ophthalmology Diagnostics market from 2023 to 2033, covering market size, growth trends, technological advancements, competitive landscape, and forecasts derived from detailed industry analysis.

Key Takeaways

- Global market projected from $5.60 Billion in 2023 to $11.45 Billion in 2033 at a 7.2% CAGR.

- North America is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- Europe and Asia Pacific show significant growth: Europe from $1.44 Billion to $2.94 Billion; Asia Pacific from $1.12 Billion to $2.29 Billion.

- Top firms active in the space include Carl Zeiss AG, Johnson & Johnson Vision, Alcon Inc., Bausch + Lomb, and Topcon Corporation.

Ophthalmology Diagnostics Market Report — Executive Summary

North America remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. This report provides a data-driven assessment of the ophthalmology diagnostics sector across product types, technologies, applications, and end users. Key demand drivers include demographic shifts, rising prevalence of ocular conditions, and continuous product innovation in diagnostic instruments and supplies. Advances in non-invasive methods and telemedicine integration are reshaping service delivery, while established companies and new entrants pursue R&D and strategic partnerships. The analysis covers market size, regional trajectories, segmentation by product and end user, and profiles of leading players, offering practical insight for stakeholders planning investments, product launches, or market entry strategies.

Key Growth Drivers

- Aging populations increasing prevalence of vision disorders, driving demand for diagnostic services and devices.

- Technological improvements in non-invasive diagnostic instruments improving diagnostic accuracy and patient comfort.

- Integration of telemedicine expands remote screening and monitoring capabilities for ophthalmic conditions.

- Rising investments by leading companies in research and development to introduce advanced solutions and broaden product portfolios.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.60 Billion |

| CAGR (2023-2033) | 7.2% |

| 2033 Market Size | $11.45 Billion |

| Top Companies | Carl Zeiss AG, Johnson & Johnson Vision, Alcon Inc., Bausch + Lomb, Topcon Corporation |

| Published Date | 08 October 2024 |

| Last Modified Date | 25 May 2026 |

Ophthalmology Diagnostics Market Overview

Customize Ophthalmology Diagnostics Market Report market research report

- ✔ Get in-depth analysis of Ophthalmology Diagnostics market size, growth, and forecasts.

- ✔ Understand Ophthalmology Diagnostics's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Ophthalmology Diagnostics

What is the Market Size & CAGR of Ophthalmology Diagnostics Market Report market in 2023?

Ophthalmology Diagnostics Industry Analysis

Ophthalmology Diagnostics Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Ophthalmology Diagnostics Market Report Market Analysis Report by Region

Europe Ophthalmology Diagnostics Market Report:

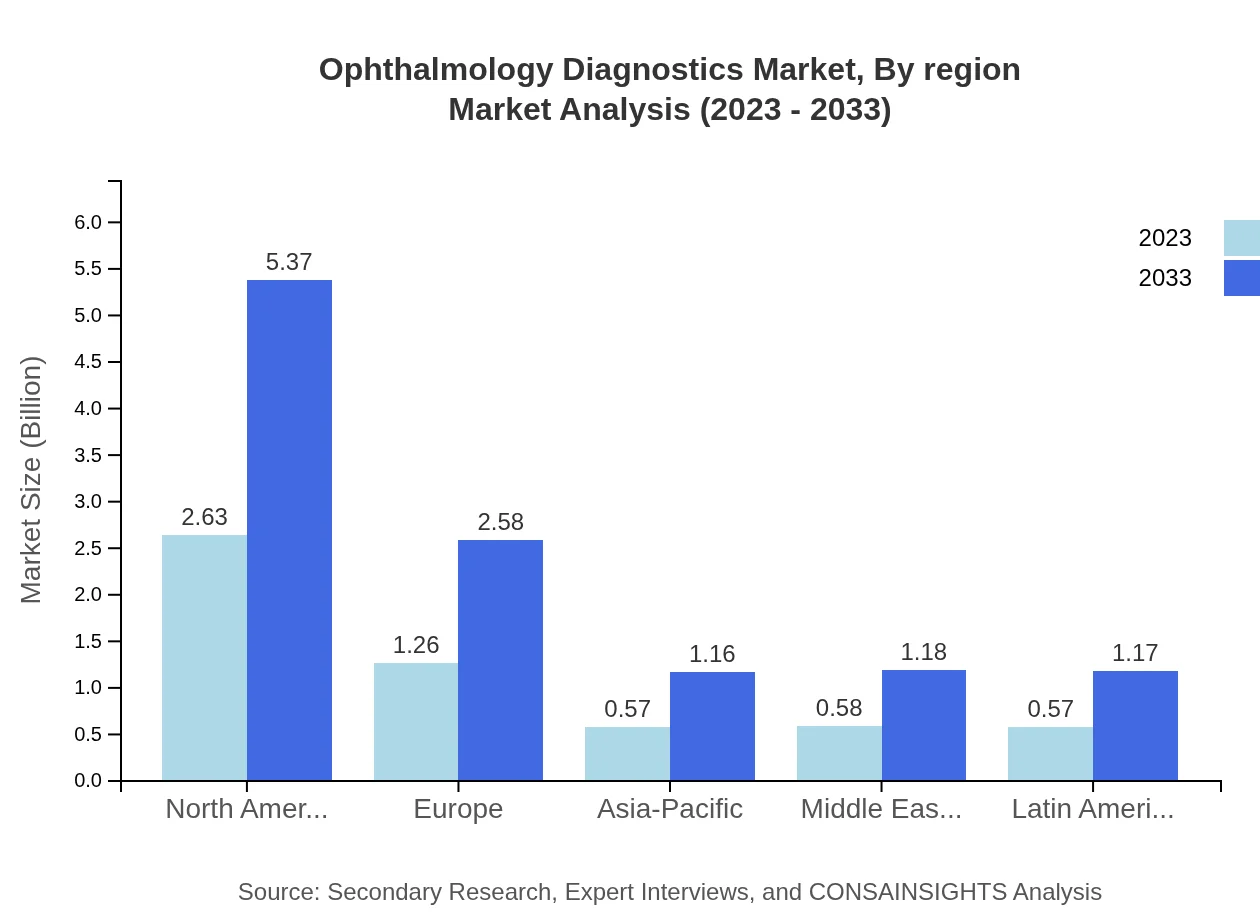

Europe grows from $1.44 Billion in 2023 to $2.94 Billion in 2033. Market movement in the region is supported by aging populations, reimbursement frameworks that facilitate diagnostic services, and ongoing adoption of improved non-invasive diagnostic techniques.Asia Pacific Ophthalmology Diagnostics Market Report:

Asia Pacific grows from $1.12 Billion in 2023 to $2.29 Billion in 2033. Regional dynamics include growing healthcare access, increased screening initiatives, and technology adoption that enhance diagnostic capacity across urban and emerging markets.North America Ophthalmology Diagnostics Market Report:

North America is largest regional market, rising from $1.96 Billion in 2023 to $4 Billion in 2033. Regional expansion reflects high uptake of advanced diagnostic instruments, strong healthcare infrastructure, and significant investment by established device manufacturers.South America Ophthalmology Diagnostics Market Report:

Latin America grows from $0.41 Billion in 2023 to $0.84 Billion in 2033. Market gains are linked to rising awareness of eye health, incremental improvements in diagnostic infrastructure, and gradual uptake of modern diagnostic instruments and supplies.Middle East & Africa Ophthalmology Diagnostics Market Report:

Middle East and Africa grows from $0.67 Billion in 2023 to $1.37 Billion in 2033. Growth drivers include expanding healthcare services, investments in diagnostic capabilities, and a growing focus on early detection and management of ocular conditions.Tell us your focus area and get a customized research report.

Research Methodology

Ophthalmology Diagnostics Market Analysis By Product

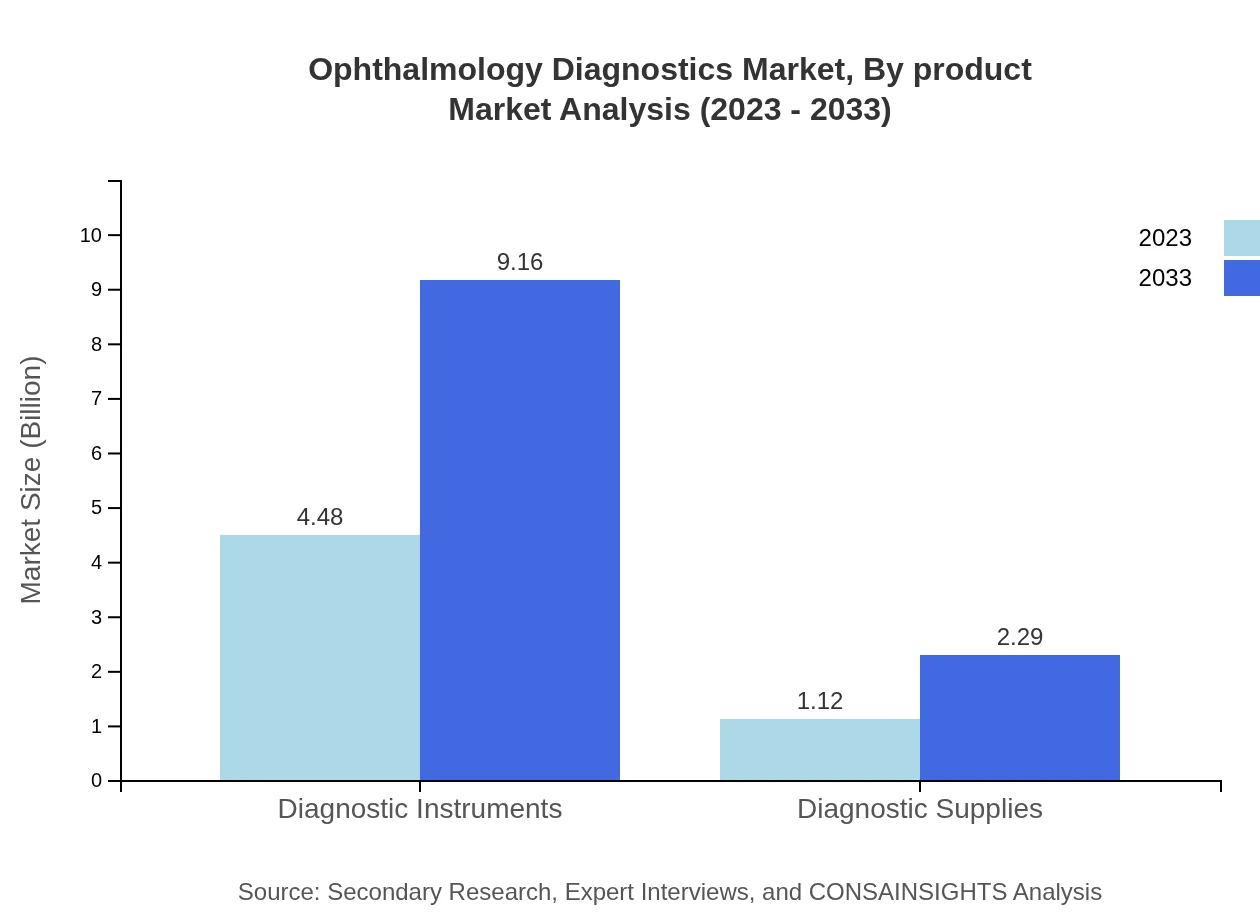

The ophthalmology diagnostics market primarily consists of diagnostic instruments and diagnostic supplies. Diagnostic instruments, which include imaging systems and refractive instruments, accounted for 80.01% market share in 2023, with a projection of significant growth to USD 9.16 billion by 2033. Conversely, diagnostic supplies, including consumables and reagents, hold a 19.99% share, expected to grow to USD 2.29 billion over the same period.

Ophthalmology Diagnostics Market Analysis By Technology

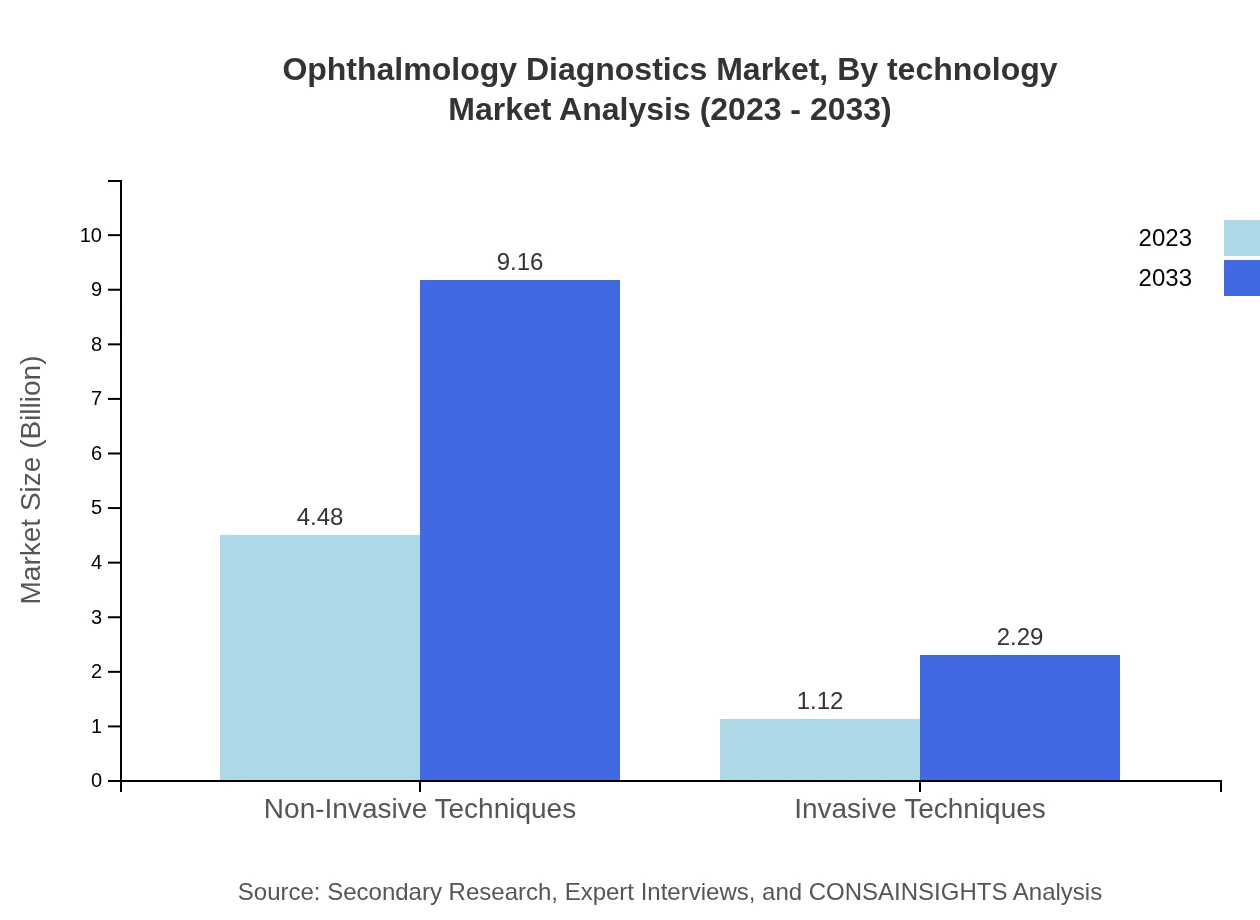

Technology in the ophthalmology diagnostics sector is largely characterized by non-invasive techniques, which dominate the market with an 80.01% share in size as of 2023, projected to reach USD 9.16 billion by 2033. In contrast, invasive techniques, representing a 19.99% share, are also growing due to their necessity in certain diagnostic scenarios. Innovative imaging technologies and telehealth solutions are also gaining traction.

Ophthalmology Diagnostics Market Analysis By Application

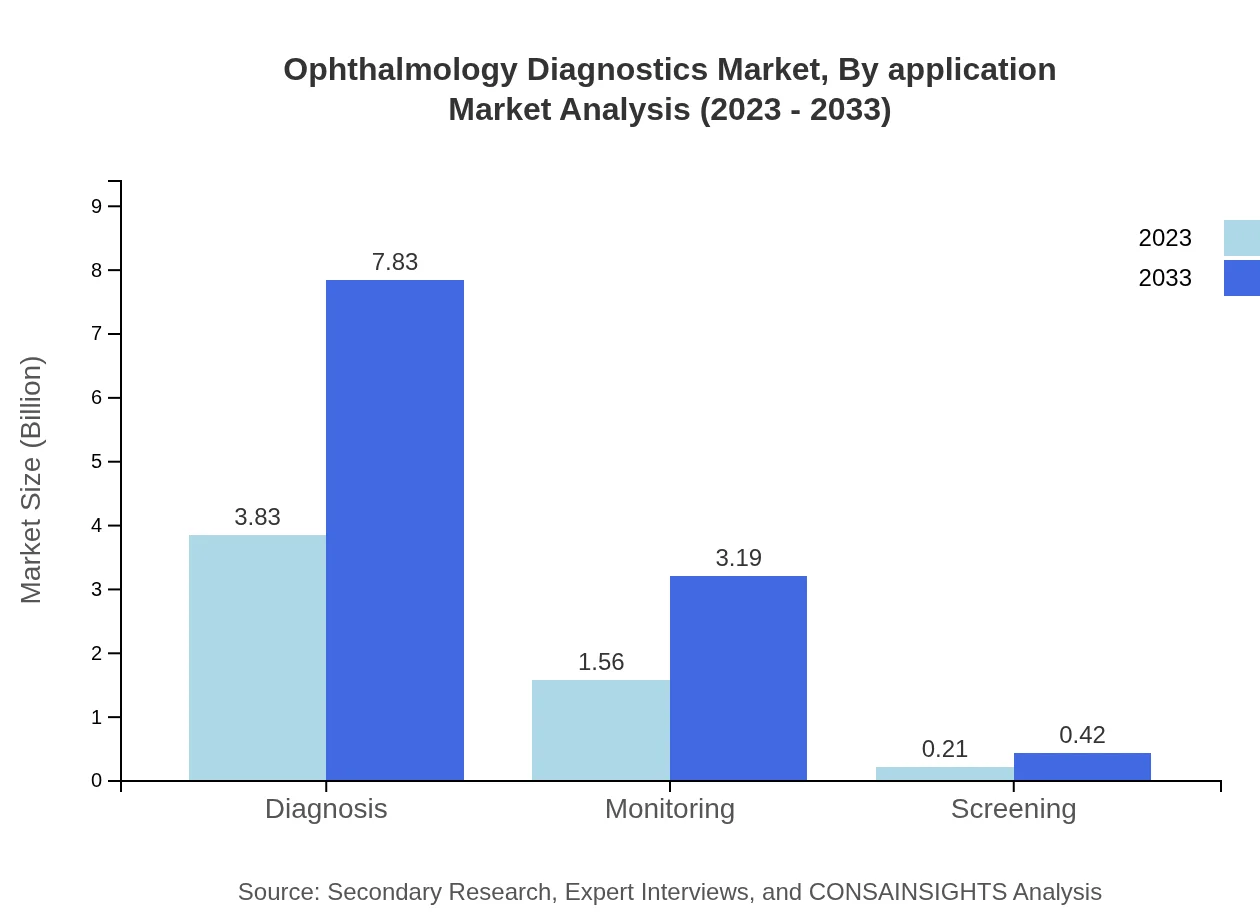

The primary applications for ophthalmology diagnostics include diagnosis, monitoring, and screening. Diagnosis accounts for 68.41% of the market share in 2023, expected to maintain growth dynamics as the primary focus area of ophthalmologists. Monitoring activities, making up 27.91% of the market, are equally essential for ongoing patient care, with a project to double in size by 2033. Meanwhile, screening, though smaller at a 3.68% share, is critical for early detection initiatives.

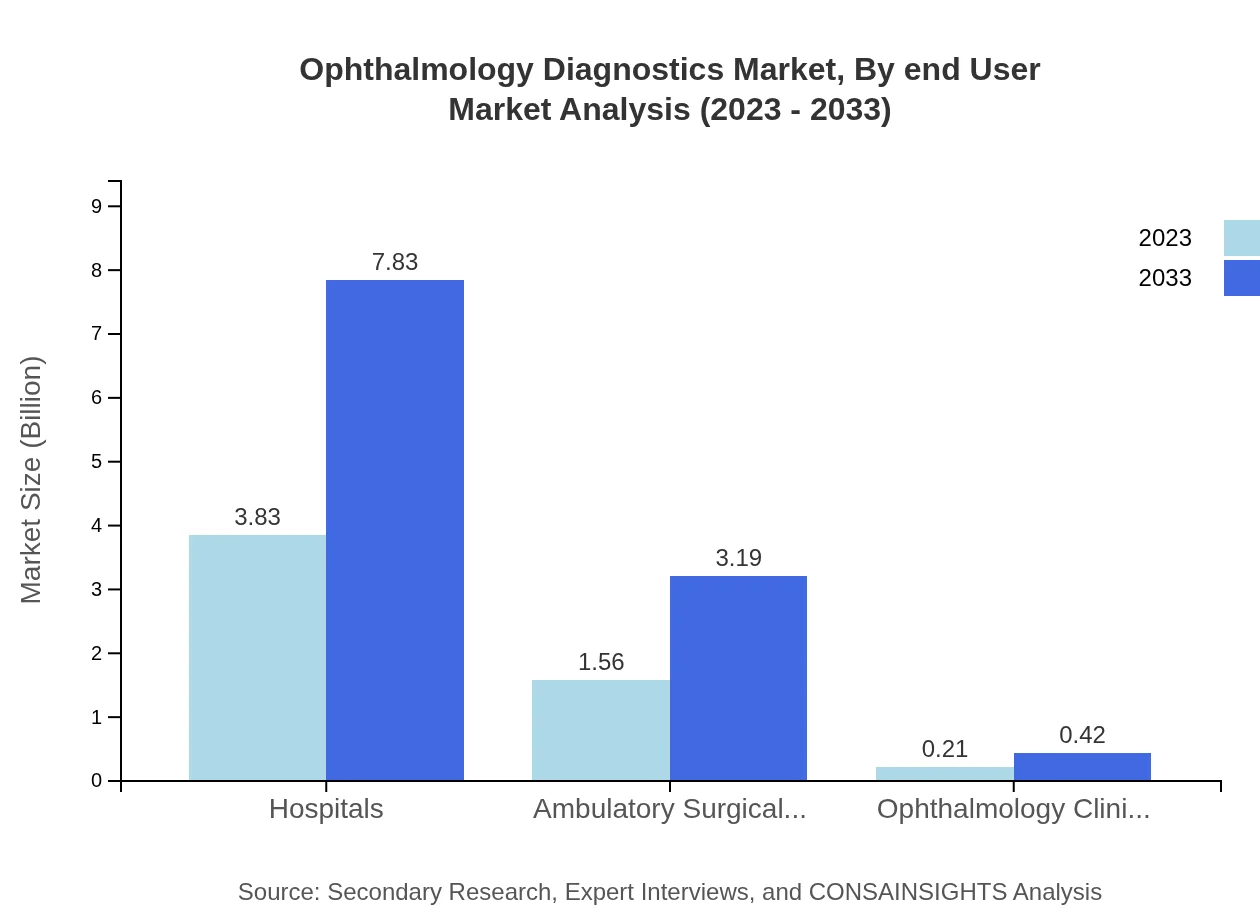

Ophthalmology Diagnostics Market Analysis By End User

Hospitals dominate the ophthalmology diagnostics market, holding a significant share of 68.41% in 2023, and projected to grow steadily. Ambulatory surgical centers also play an important role, holding a 27.91% share and expected to see increased demand for outpatient eye care services. Conversely, ophthalmology clinics, albeit smaller at just 3.68%, contribute to niche services and specialized care.

Ophthalmology Diagnostics Market Analysis By Region

Regional dynamics indicate North America leads the market, attributed to advanced infrastructure and high healthcare spending. Europe follows closely, while the Asia Pacific displays rapid growth potential driven by population health initiatives. The Middle East and Africa, along with South America, are gradually increasing their market shares through improving healthcare conditions and investments in technology.

Ophthalmology Diagnostics Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Ophthalmology Diagnostics Industry

Carl Zeiss AG:

Specializes in optics and optoelectronics, offering advanced diagnostic and surgical solutions in ophthalmology.Johnson & Johnson Vision:

Focuses on innovative eye health products, including surgical instruments and diagnostics devices for eye care professionals.Alcon Inc.:

A global leader in eye care, providing a range of surgical and vision care products, focusing on diagnostics and treatment.Bausch + Lomb:

Engaged in manufacturing eye health products, including diagnostic instruments and solutions for eye care specialists.Topcon Corporation:

Offers a wide range of ophthalmic equipment with a focus on diagnostic imaging and surgical solutions.We're grateful to work with incredible clients.

FAQs

What is the market size of the ophthalmology diagnostics market in 2023?

The ophthalmology diagnostics market size for 2023 is $5.60 Billion as reported for the global market at the start of the forecast period.

How big will the market be by 2033?

By 2033 the market is projected to reach $11.45 Billion according to the report’s end‑period market size projection for the forecast horizon.

What is CAGR for the forecast period?

The reported compound annual growth rate (CAGR) for the 2023 to 2033 forecast period is 7.2% for the global ophthalmology diagnostics market.

Is there a single fastest Growing region in the Ophthalmology Diagnostics Market Report market?

No single fastest-growing region is stated for the Ophthalmology Diagnostics Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Which companies are leading the market?

Top companies noted in the report include Carl Zeiss AG, Johnson & Johnson Vision, Alcon Inc., Bausch + Lomb, and Topcon Corporation driving product and technology development.

What are primary technological trends in the sector?

Primary trends include adoption of non-invasive diagnostic techniques and expanded telemedicine integration, improving accessibility and diagnostic efficiency across care settings.

Who are the main end users for diagnostic products?

Main end users identified include hospitals, ambulatory surgical centers, and ophthalmology clinics, reflecting demand across inpatient and outpatient care environments.

How is regional growth characterized in the report?

Regional growth is presented with specific start and end market values; North America is largest, and the report does not designate a fastest‑growing region due to close regional growth rates.