Continuous Manufacturing Market Report

First published: 07 October 2024 | Last updated: 22 January 2026 | Report Code: continuous-manufacturing

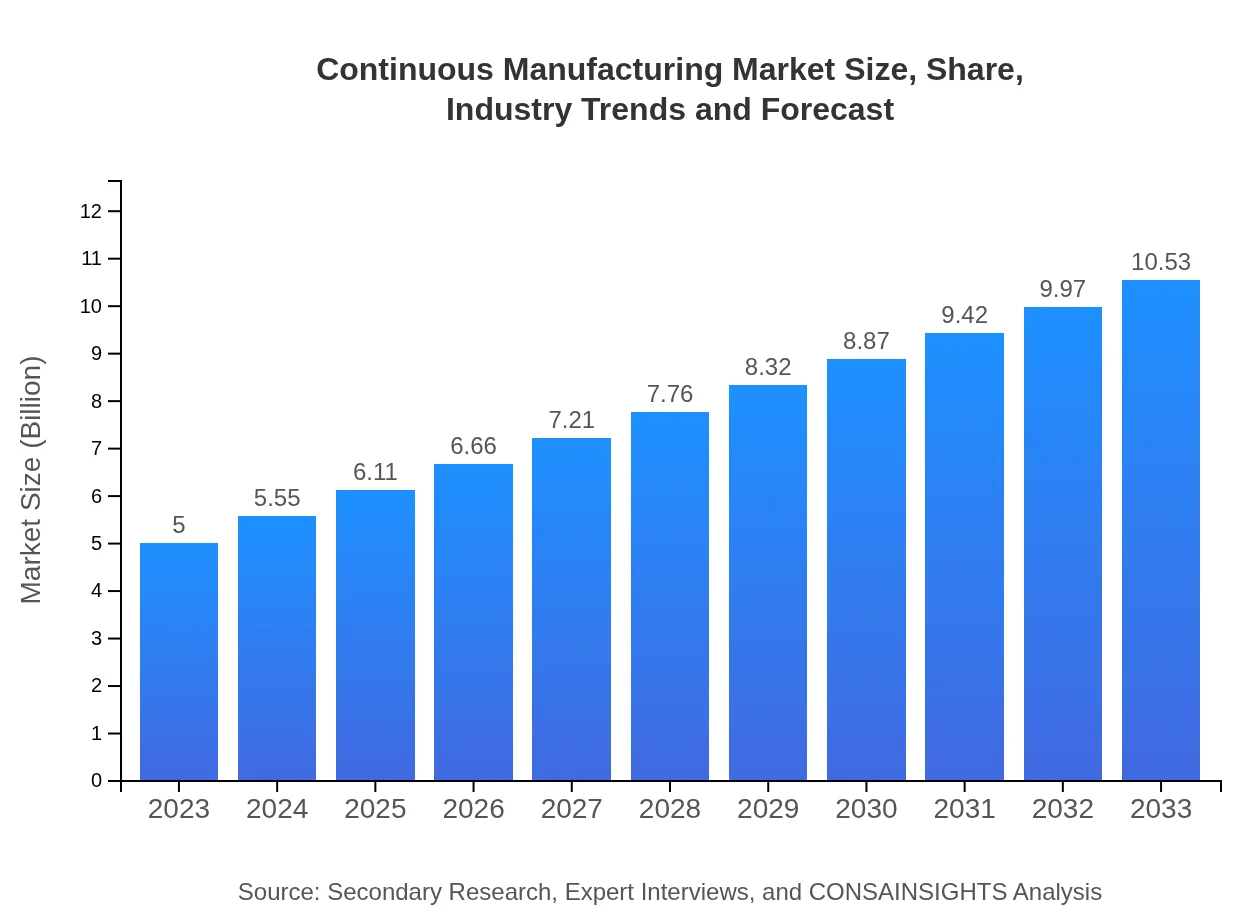

Continuous Manufacturing Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides a comprehensive analysis of the Continuous Manufacturing market, covering key insights, market size, growth trends, and forecasts from 2023 to 2033. It aims to equip stakeholders with data-driven insights to navigate this evolving industry landscape.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Siemens AG, Emerson Electric Co., Rockwell Automation, Honeywell International Inc., ABB Ltd. |

| Published Date | 07 October 2024 |

| Last Modified Date | 22 January 2026 |

Continuous Manufacturing Market Overview

Customize Continuous Manufacturing Market Report market research report

- ✔ Get in-depth analysis of Continuous Manufacturing market size, growth, and forecasts.

- ✔ Understand Continuous Manufacturing's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Continuous Manufacturing

What is the Market Size & CAGR of Continuous Manufacturing market in 2023?

Continuous Manufacturing Industry Analysis

Continuous Manufacturing Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Continuous Manufacturing Market Analysis Report by Region

Europe Continuous Manufacturing Market Report:

Europe's market for Continuous Manufacturing is projected to grow from $1.65 billion in 2023 to $3.48 billion by 2033. Strong regulatory frameworks and a focus on innovation in pharmaceuticals and chemicals are key trends in this region.Asia Pacific Continuous Manufacturing Market Report:

The Asia Pacific region is projected to witness substantial growth, with the market size expected to rise from $0.93 billion in 2023 to $1.96 billion by 2033, driven by the increasing industrialization and demand for process efficiency in countries like China and India.North America Continuous Manufacturing Market Report:

In North America, particularly in the U.S., the market is expected to expand from $1.82 billion in 2023 to $3.82 billion by 2033. The early adoption of advanced manufacturing technologies is a significant driver in this region.South America Continuous Manufacturing Market Report:

In South America, the Continuous Manufacturing market is estimated at $0.32 billion in 2023, growing to $0.68 billion by 2033. The demand for improved production methods in the chemical and food industries is fueling this growth.Middle East & Africa Continuous Manufacturing Market Report:

The Middle East and Africa market is anticipated to grow from $0.28 billion in 2023 to $0.59 billion by 2033, with increasing investments in manufacturing infrastructure and technology enhancements in various sectors.Tell us your focus area and get a customized research report.

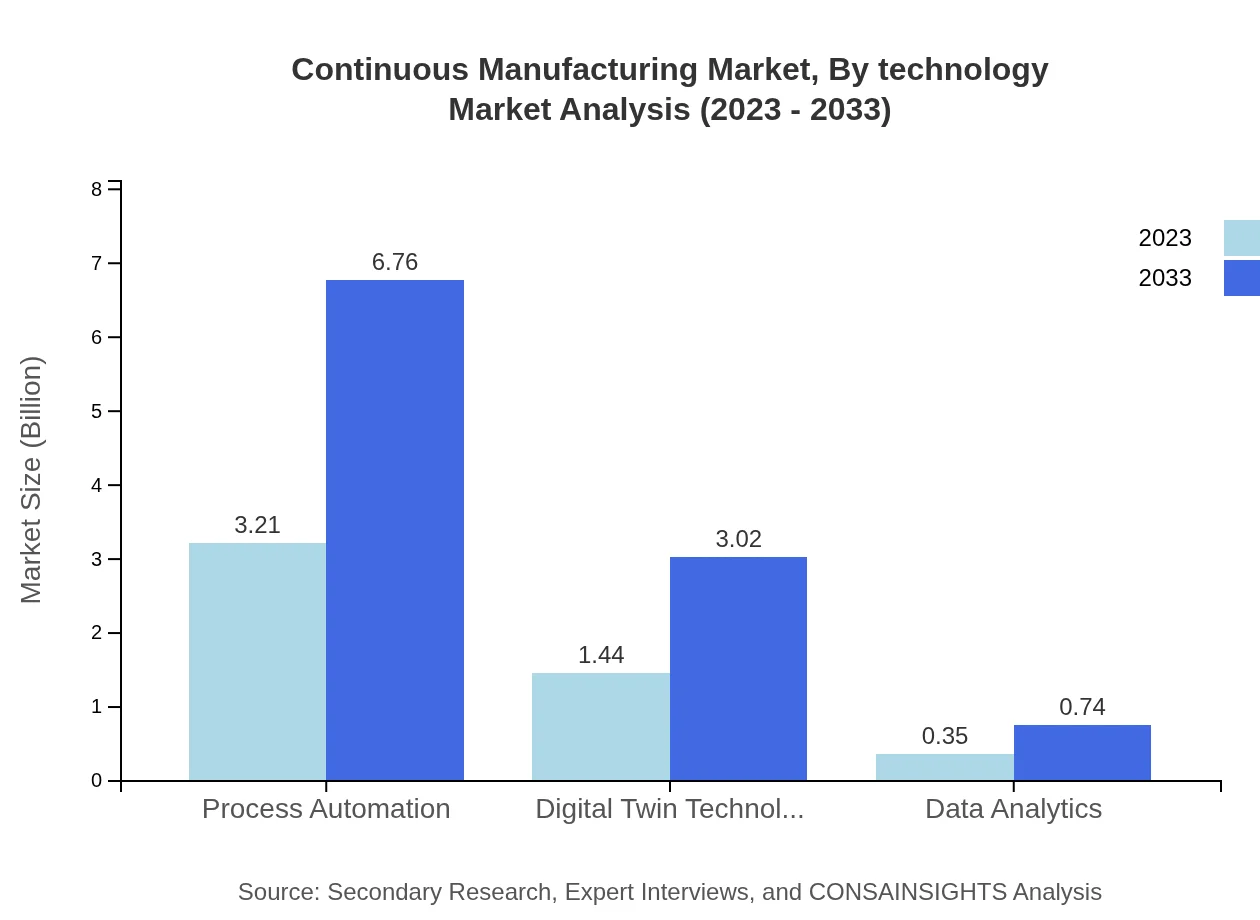

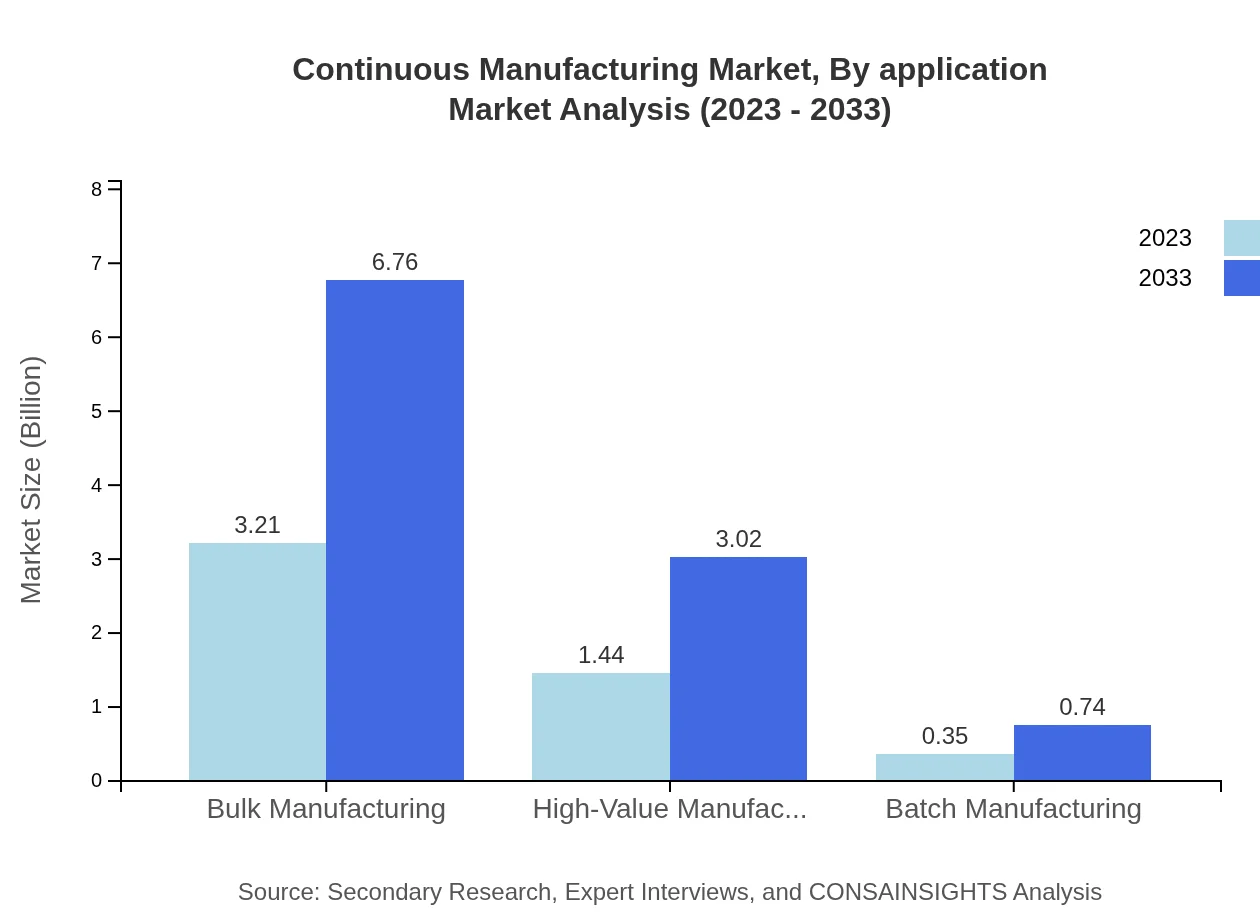

Continuous Manufacturing Market Analysis By Technology

Key technologies in the continuous manufacturing market include process automation, digital twin technology, and data analytics. Process automation is pivotal, with a market size of $3.21 billion in 2023, expected to grow to $6.76 billion by 2033, capturing 64.23% market share. Digital twin technology is also gaining momentum, growing from $1.44 billion to $3.02 billion during the same period, holding 28.72% share. Data analytics, while smaller, is crucial for optimizing operations and is expected to increase from $0.35 billion to $0.74 billion.

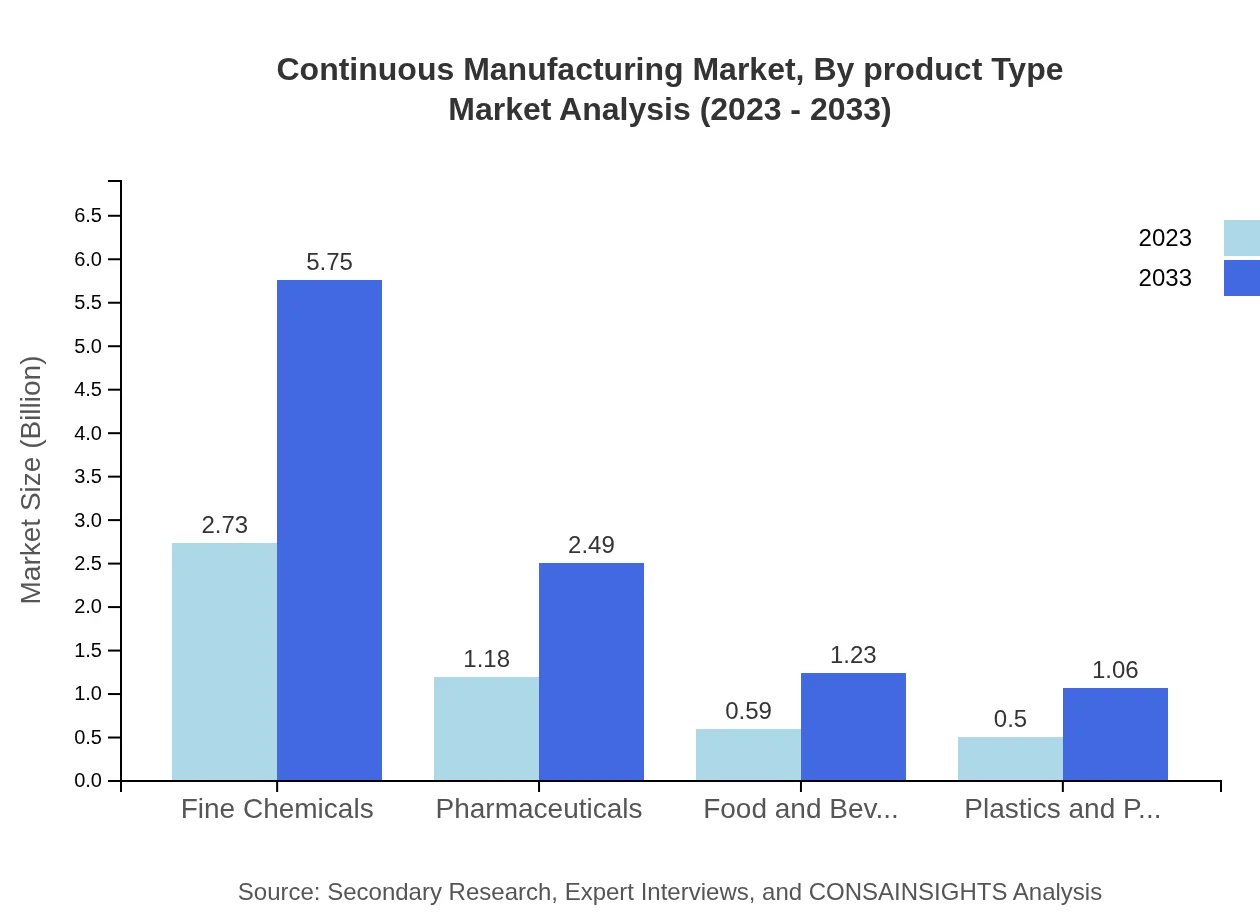

Continuous Manufacturing Market Analysis By Product Type

Different product types significantly influence the continuous manufacturing landscape. Fine chemicals have substantial market presence, starting at $2.73 billion in 2023 and expected to reach $5.75 billion by 2033, representing 54.62% of the market. The pharmaceutical industry also shows promise, with anticipated growth from $1.18 billion to $2.49 billion, comprising 23.62%. Other industries such as food & beverages and plastics & polymers, while smaller, are expected to increase steadily due to growing consumer demand.

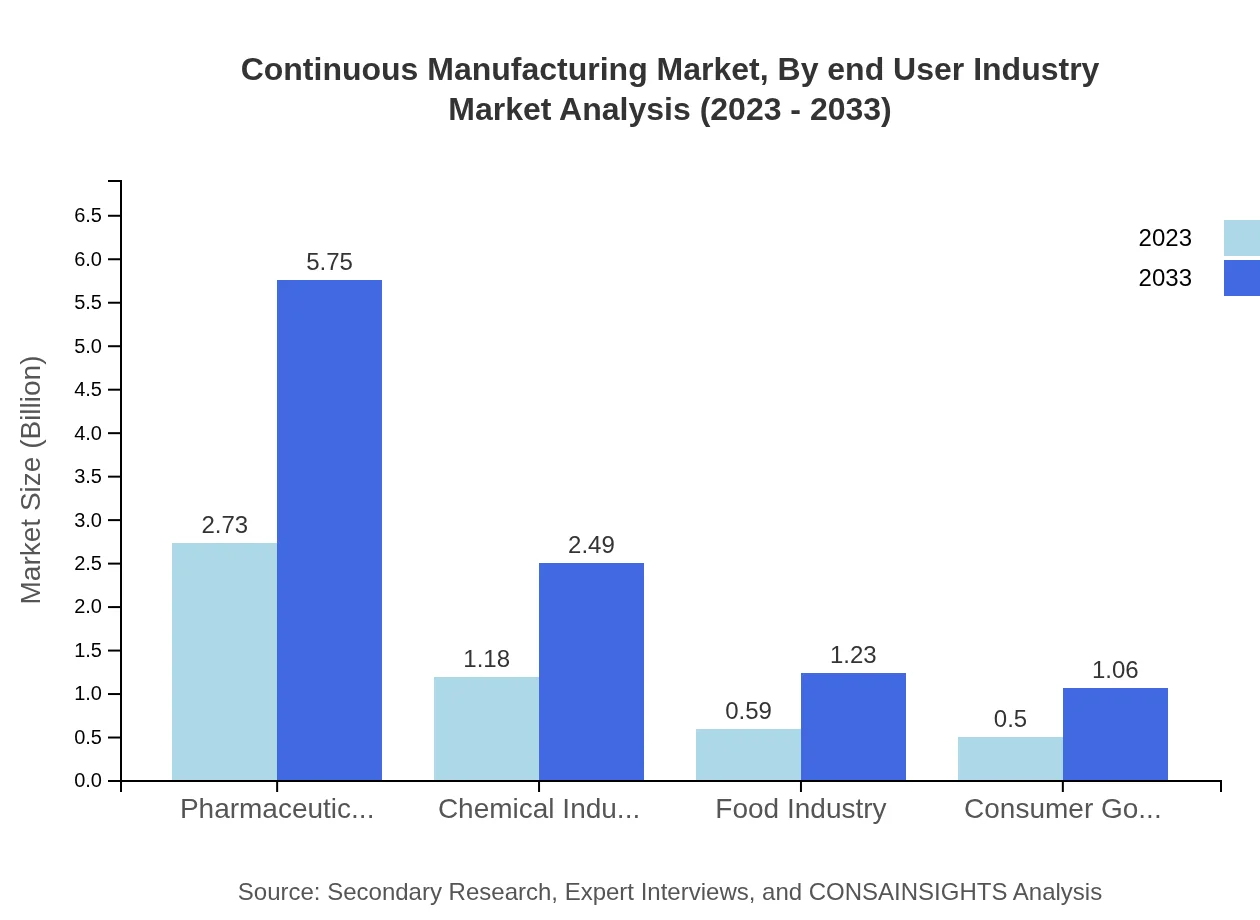

Continuous Manufacturing Market Analysis By End User Industry

The end-user industries for Continuous Manufacturing range from pharmaceuticals to consumer goods. The pharmaceutical sector dominates with a share of 54.62%, while the food industry and consumer goods segments hold 11.73% and 10.03%, respectively. Each industry demands specific manufacturing solutions and features unique challenges, contributing to the ongoing evolution of the continuous manufacturing processes.

Continuous Manufacturing Market Analysis By Application

Applications of Continuous Manufacturing span various sectors, enhancing flexibility and efficiency in production lines. Applications in the pharmaceutical sector are critical, given the stringent compliance requirements. Food and beverage applications are gaining traction, focusing on quality and safety. Digital technologies are increasingly integrated into these applications, driving further growth and innovation.

Continuous Manufacturing Market Analysis By Regulatory Compliance

Regulatory compliance is paramount in the Continuous Manufacturing market, particularly in pharmaceuticals and food production. Compliance with standards like Good Manufacturing Practices (GMP), ISO certifications, and CFR 21 Part 11 significantly influences manufacturing processes. The emphasis on regulatory compliance shapes market dynamics, pushing manufacturers to adopt continuous processes to facilitate adherence to these regulations.

Continuous Manufacturing Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Continuous Manufacturing Industry

Siemens AG:

A leader in automation and digitalization, Siemens plays a critical role in providing advanced technologies that facilitate continuous manufacturing processes.Emerson Electric Co.:

Specializes in process automation solutions, Emerson is influential in optimizing continuous manufacturing through innovative technology and ongoing support.Rockwell Automation:

Provides integrated control and information solutions that enhance continuous manufacturing efficiency and productivity.Honeywell International Inc.:

Offers a range of solutions for manufacturing across chemicals and pharmaceuticals, contributing to advancements in continuous manufacturing technologies.ABB Ltd.:

A global leader in industrial technology, ABB supports the continuous manufacturing market through automation and digitalization strategies.We're grateful to work with incredible clients.

FAQs

What is the market size of continuous Manufacturing?

The global continuous manufacturing market in 2023 is valued at $5 billion, with a projected growth rate (CAGR) of 7.5% over the next decade, indicating robust expansion in this sector.

What are the key market players or companies in the continuous Manufacturing industry?

Leading companies in the continuous manufacturing space include industry giants known for their innovative solutions in process automation, digital twin technology, and data analytics, driving advancements across various sectors.

What are the primary factors driving the growth in the continuous manufacturing industry?

Growth is being propelled by advancements in automation technology, increasing demand for efficiency and productivity, and the rising necessity for real-time data processing, making continuous manufacturing more appealing to industries.

Which region is the fastest Growing in continuous manufacturing?

North America is the fastest-growing region, with the market expected to grow from $1.82 billion in 2023 to $3.82 billion by 2033, reflecting a strong demand for advanced manufacturing technologies in the region.

Does ConsaInsights provide customized market report data for the continuous manufacturing industry?

Yes, ConsaInsights offers customized market report data tailored to specific needs in the continuous manufacturing sector, ensuring actionable insights and strategic recommendations for stakeholders.

What deliverables can I expect from this continuous manufacturing market research project?

Expect comprehensive deliverables, including detailed market analysis, forecasts, segmentation data, competitive landscape assessments, and insights into regulatory trends impacting the continuous manufacturing landscape.

What are the market trends of continuous manufacturing?

Current trends include increased adoption of process automation, integration of digital twin technologies, and a focus on sustainability, as companies seek ways to enhance efficiency and reduce waste in manufacturing processes.