Corrugated Bulk Bins Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: corrugated-bulk-bins

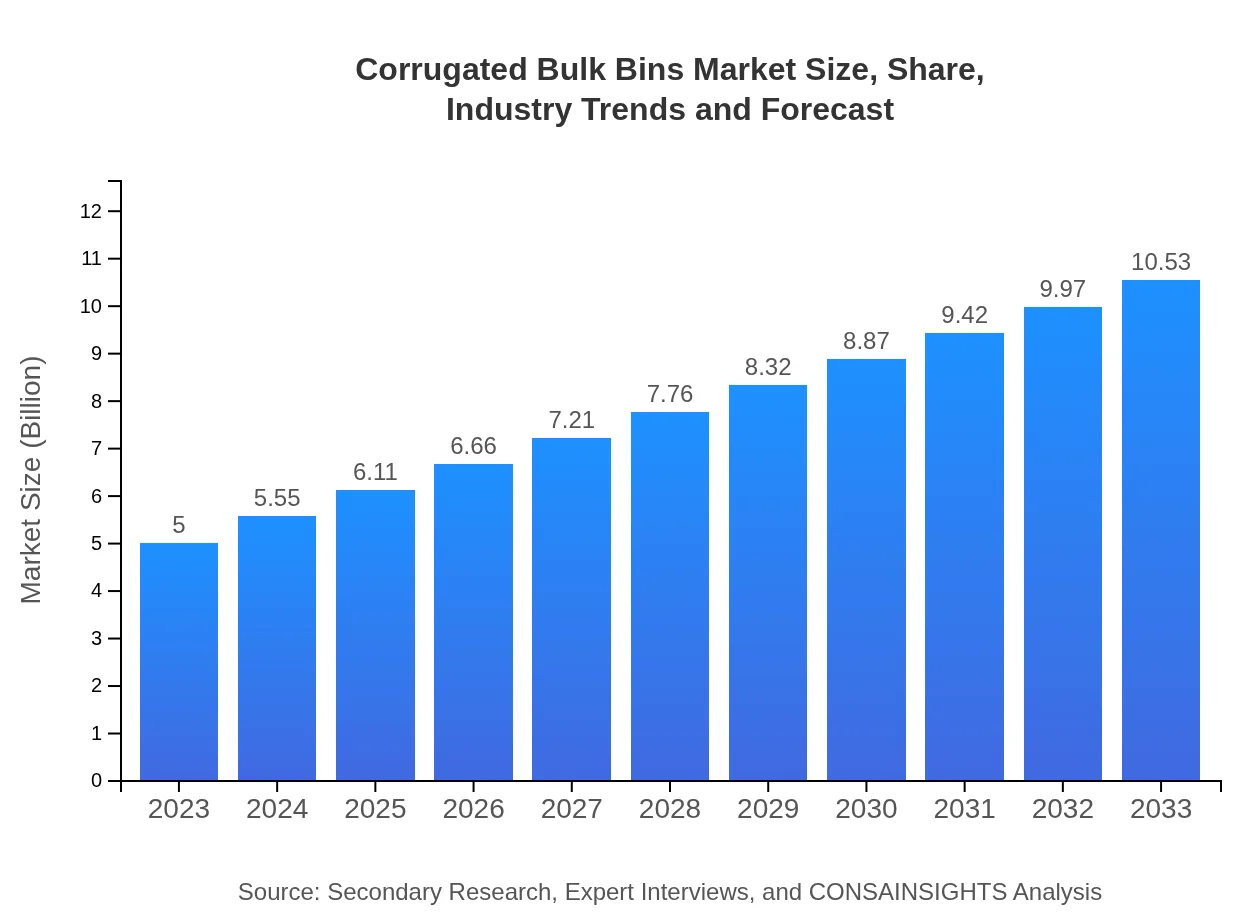

Corrugated Bulk Bins Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report offers a comprehensive analysis of the Corrugated Bulk Bins market, covering forecasts from 2023 to 2033. It includes insights on market size, trends, regional analysis, and key market players, providing a valuable resource for stakeholders in the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | International Paper Company, WestRock Company, Smurfit Kappa Group, DS Smith, Sealed Air |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Corrugated Bulk Bins Market Overview

Customize Corrugated Bulk Bins Market Report market research report

- ✔ Get in-depth analysis of Corrugated Bulk Bins market size, growth, and forecasts.

- ✔ Understand Corrugated Bulk Bins's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Corrugated Bulk Bins

What is the Market Size & CAGR of Corrugated Bulk Bins market in 2023 and 2033?

Corrugated Bulk Bins Industry Analysis

Corrugated Bulk Bins Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Corrugated Bulk Bins Market Analysis Report by Region

Europe Corrugated Bulk Bins Market Report:

Europe's market for Corrugated Bulk Bins is expected to expand from $1.28 billion in 2023 to $2.69 billion by 2033. The region has stringent environmental regulations, prompting manufacturers to focus on eco-friendly products and driving the growth of recycled corrugated bulk bins.Asia Pacific Corrugated Bulk Bins Market Report:

The Asia Pacific region, estimated at $1.08 billion in 2023 and projected to grow to $2.26 billion by 2033, is expected to dominate the market due to rapid industrialization and expanding retail sectors. Countries like China and India are leading the demand for sustainable packaging solutions, significantly contributing to market growth.North America Corrugated Bulk Bins Market Report:

North America, with a market size of $1.89 billion in 2023 projected to reach $3.97 billion by 2033, is witnessing a strong demand driven by the robust e-commerce sector and advances in sustainable packaging practices. Key players in the U.S. are investing heavily in corrugated packaging technologies.South America Corrugated Bulk Bins Market Report:

In South America, the Corrugated Bulk Bins market is predicted to grow from $0.41 billion in 2023 to $0.87 billion by 2033. This growth is fueled by increasing adoption of e-commerce practices and a growing emphasis on reducing carbon footprints in packaging solutions.Middle East & Africa Corrugated Bulk Bins Market Report:

The Middle East and Africa region is anticipated to grow from $0.35 billion in 2023 to $0.73 billion by 2033. Growth in this region is primarily driven by increasing urbanization and the expansion of retail and logistics sectors, which are adopting bulk bins for efficiency.Tell us your focus area and get a customized research report.

Corrugated Bulk Bins Market Analysis By Material

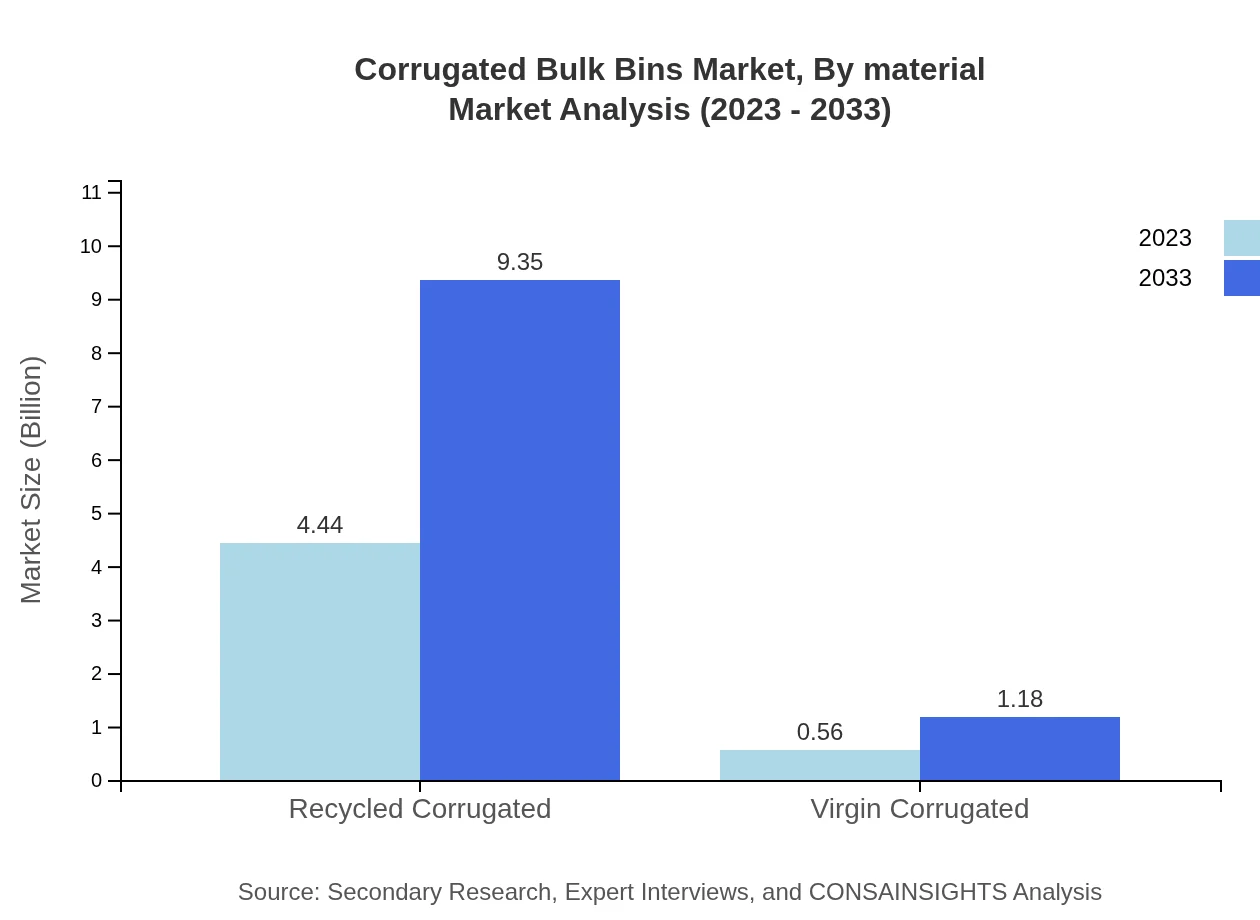

The Corrugated Bulk Bins market, segmented by material, shows a strong inclination towards recycled corrugated solutions, which accounted for 88.8% of the market share in 2023, equating to a size of $4.44 billion, and is projected to rise to $9.35 billion by 2033. Virgin corrugated products, while accounting for 11.2% of the market, are also projected to grow significantly, underlining the industry's shift towards sustainable practices.

Corrugated Bulk Bins Market Analysis By Industry

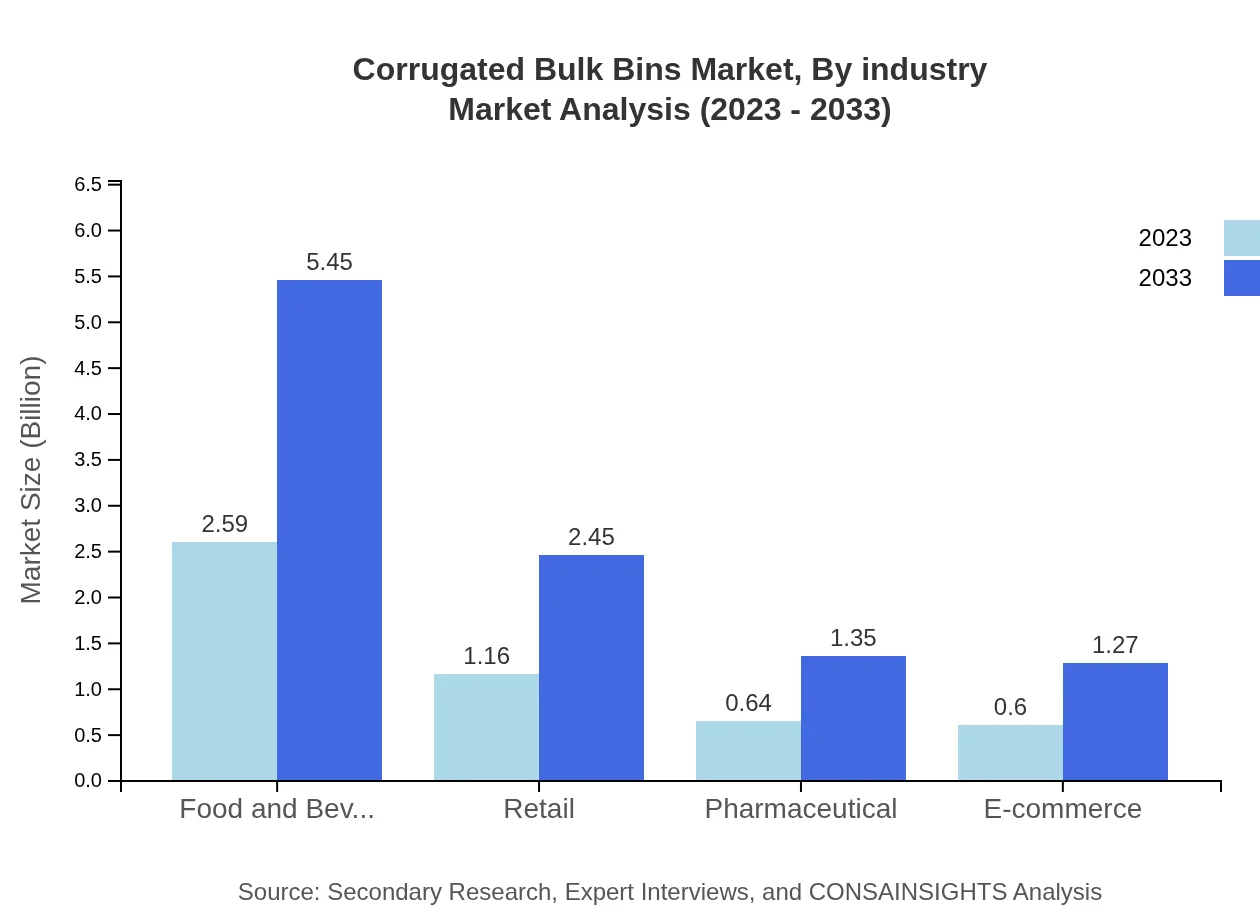

In terms of industry usage, the food and beverage sector dominates, representing 51.82% of the market with a size of $2.59 billion in 2023, anticipated to grow to $5.45 billion by 2033. Retail follows, accounting for 23.27% with projected growth from $1.16 billion to $2.45 billion, reflecting the strong demand driven by e-commerce.

Corrugated Bulk Bins Market Analysis By Design

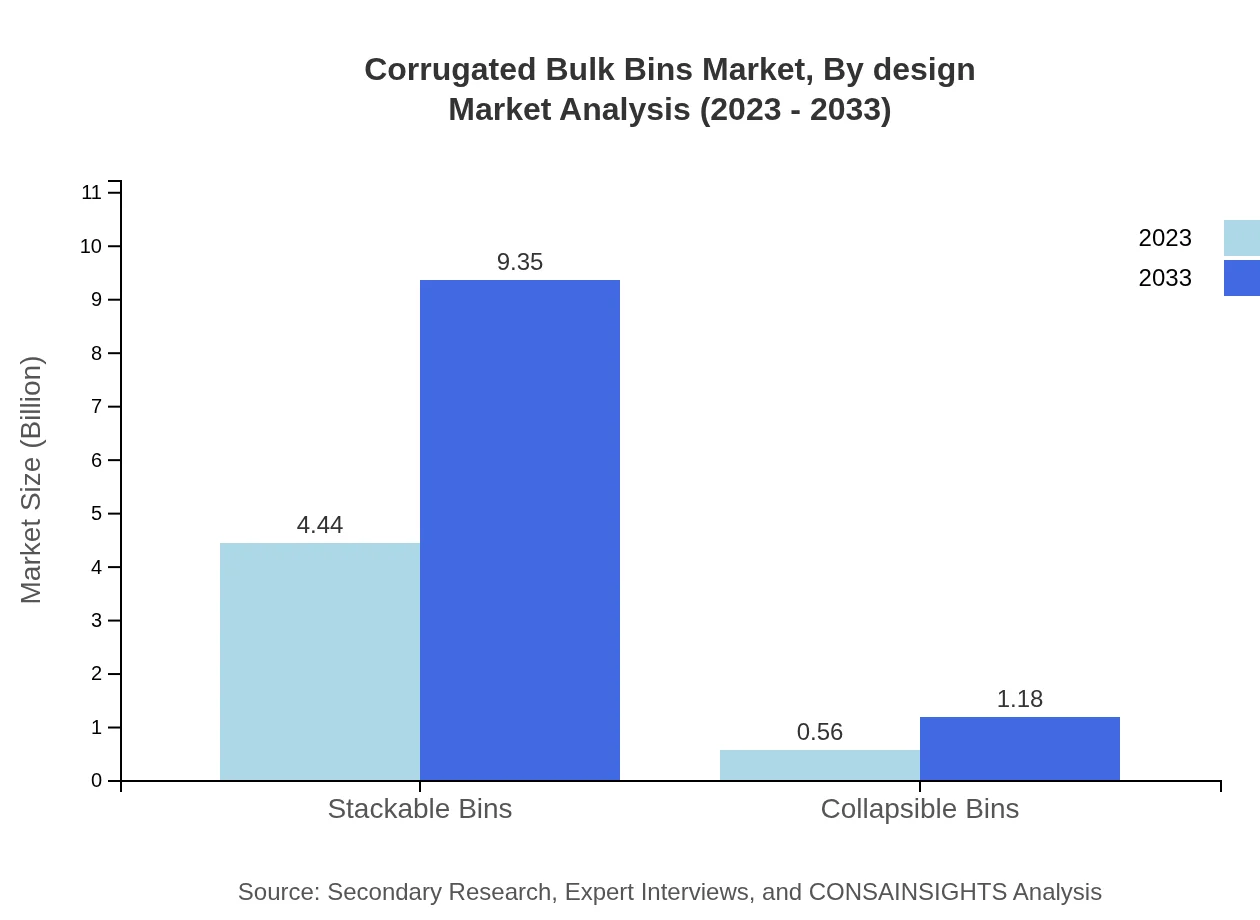

The leading design segment, Stackable Bins, holds a substantial share at 88.8% in 2023, estimated at $4.44 billion, expected to reach $9.35 billion by 2033, indicating their favorable characteristics for warehouse operations. Meanwhile, collapsible bins, which currently account for 11.2%, portray promising growth potential driven by space-saving benefits.

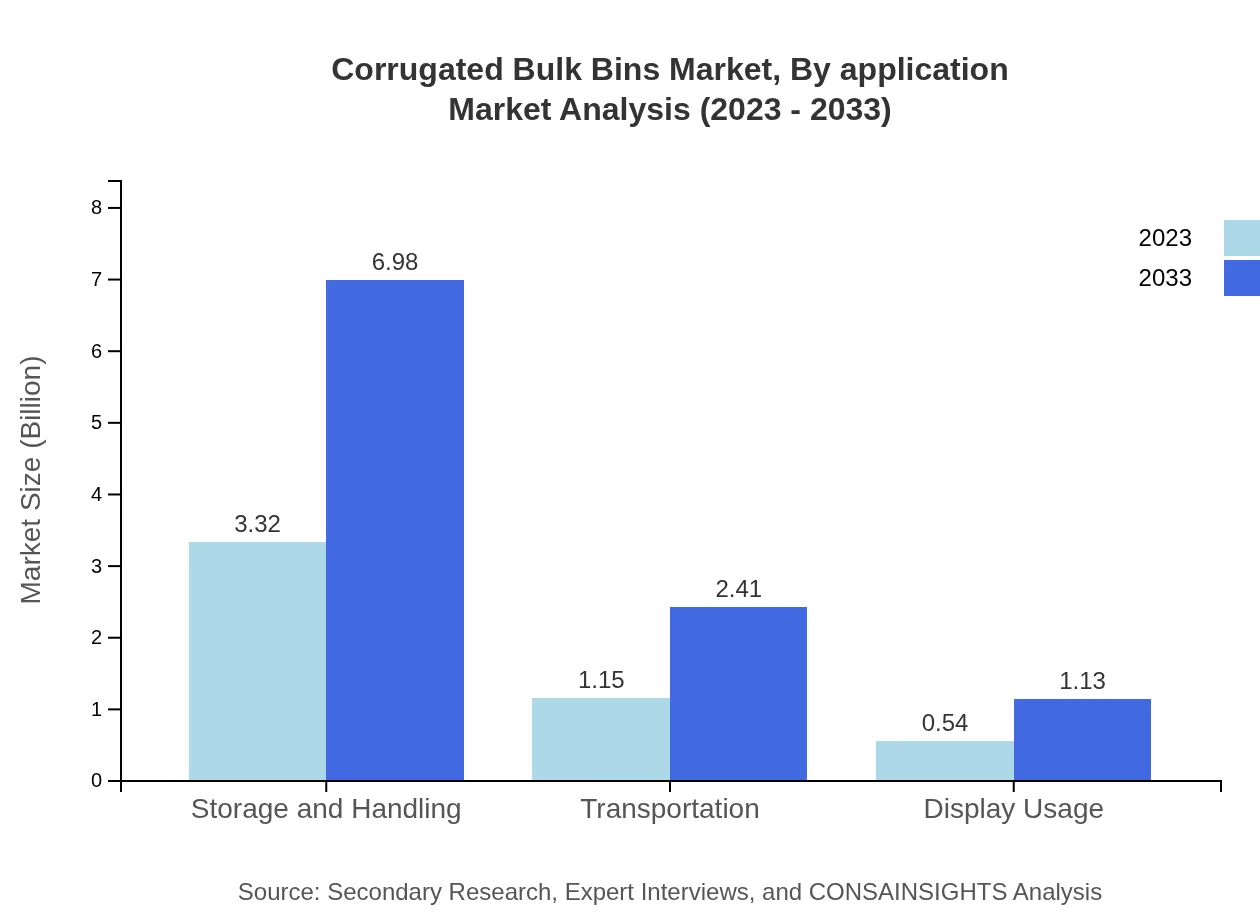

Corrugated Bulk Bins Market Analysis By Application

The storage and handling application represents a majority share of 66.36% in 2023 with a market size of $3.32 billion, anticipated to grow to $6.98 billion by 2033. Transportation and display usage applications follow, showing significant growth patterns driven by enhanced logistics strategies and retail display needs.

Corrugated Bulk Bins Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Corrugated Bulk Bins Industry

International Paper Company:

A major player in the corrugated packaging market, known for innovative and sustainable bulk bin solutions.WestRock Company:

A leading provider of corrugated packaging solutions, emphasizing sustainable practices and customer-oriented designs.Smurfit Kappa Group:

Specializing in paper-based packaging, Smurfit Kappa is recognized for its environmentally friendly bulk bin products.DS Smith:

A prominent player in the corrugated packaging sector, known for its resource-efficient and recyclable bulk bins.Sealed Air:

A global leader in packaging solutions, offering innovative corrugated bins that cater to various industries.We're grateful to work with incredible clients.

FAQs

What is the market size of corrugated Bulk Bins?

The global market size for corrugated bulk bins is projected to reach $5 billion by 2033, exhibiting a CAGR of 7.5% during the forecast period. This growth is driven by increasing demand across various industries for effective bulk storage solutions.

What are the key market players or companies in this corrugated Bulk Bins industry?

Key players in the corrugated bulk bins market include major manufacturers and suppliers with established distribution networks. These companies are focused on innovation and sustainability to enhance market reach and customer satisfaction.

What are the primary factors driving the growth in the corrugated bulk bins industry?

Factors driving growth include increasing demand from the food and beverage sector, rising e-commerce activities, and the need for efficient storage solutions. Sustainability practices also encourage the use of recycled materials in production.

Which region is the fastest Growing in the corrugated bulk bins?

The fastest-growing region is North America, with a market size projected to grow from $1.89 billion in 2023 to $3.97 billion in 2033. This is attributed to the increasing adoption of sustainability practices and robust e-commerce growth.

Does ConsaInsights provide customized market report data for the corrugated bulk bins industry?

Yes, ConsaInsights offers customized market report data that caters to the specific needs and interests of businesses within the corrugated bulk bins industry, ensuring relevant insights for strategic decision-making.

What deliverables can I expect from this corrugated bulk bins market research project?

Deliverables include comprehensive market analysis reports, segmentation data, regional insights, and actionable strategies for market entry and expansion. Detailed forecasts and trend analysis will also be provided.

What are the market trends of corrugated bulk bins?

Current trends indicate a shift towards stackable and collapsible bin designs, increasing use of recycled materials, and growing demand in sectors like food & beverage and e-commerce, reflecting adaptability in the market.