Frequency Converter Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: frequency-converter

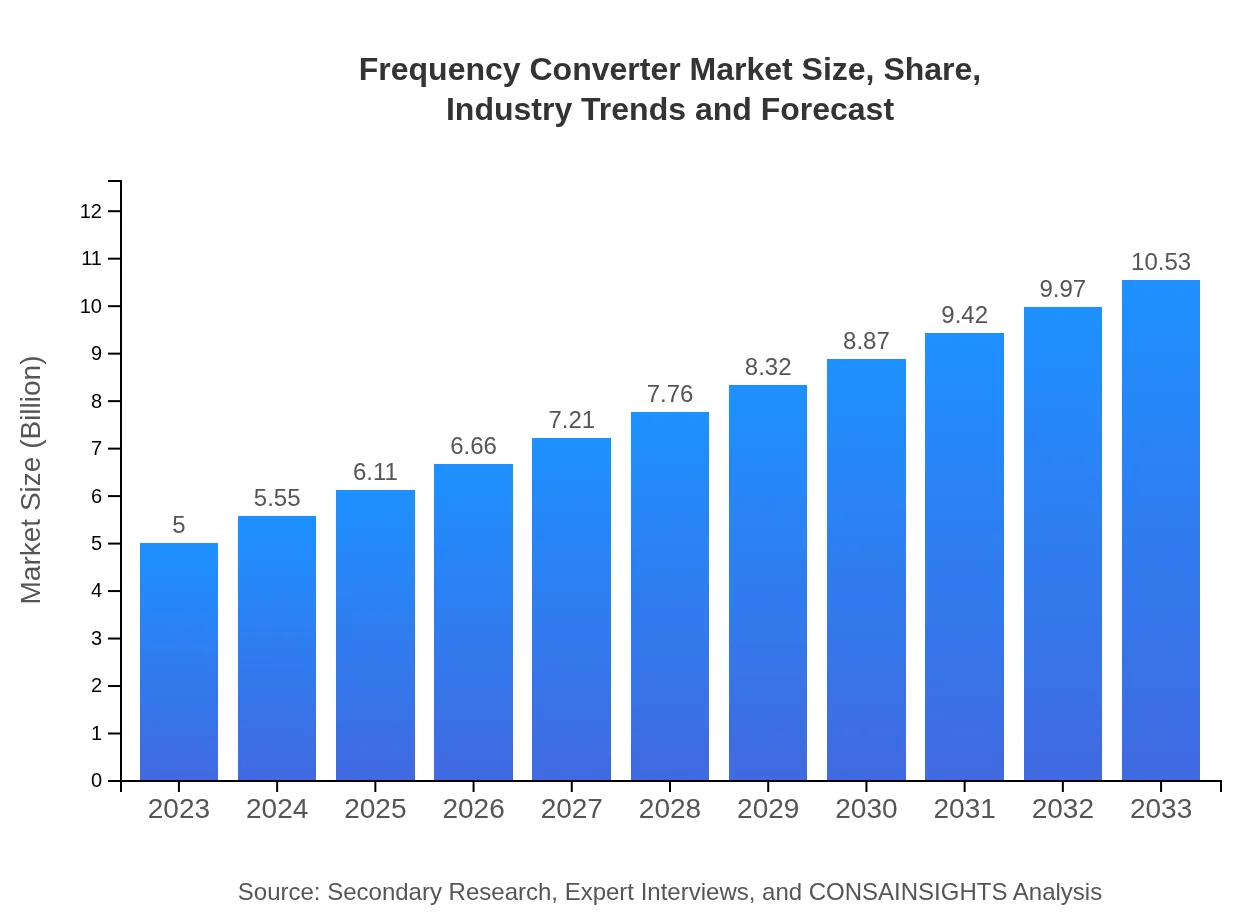

Frequency Converter Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides an in-depth analysis of the Frequency Converter market, examining its current status, trends, growth opportunities, and future forecasts from 2023 to 2033. Insights include market size, segmentation by type and application, regional dynamics, technology advancements, and contributions of leading companies.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Schneider Electric, Siemens AG, ABB Ltd., General Electric, Mitsubishi Electric |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Frequency Converter Market Overview

Customize Frequency Converter Market Report market research report

- ✔ Get in-depth analysis of Frequency Converter market size, growth, and forecasts.

- ✔ Understand Frequency Converter's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Frequency Converter

What is the Market Size & CAGR of Frequency Converter market in 2023 and 2033?

Frequency Converter Industry Analysis

Frequency Converter Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Frequency Converter Market Analysis Report by Region

Europe Frequency Converter Market Report:

Europe's market is projected to rise from $1.72 billion in 2023 to $3.63 billion by 2033. The push for green technologies and stringent energy regulations drive the demand for efficient electrical power solutions across various industries.Asia Pacific Frequency Converter Market Report:

The Asia-Pacific region is projected to witness significant growth in the Frequency Converter market, expanding from $0.90 billion in 2023 to $1.89 billion by 2033. This growth is driven by increasing industrial activities, government initiatives to boost renewable energy, and the rapid urbanization of emerging economies.North America Frequency Converter Market Report:

North America is anticipated to grow from $1.63 billion in 2023 to $3.44 billion by 2033, supported by technological advancements and an increasing shift to renewable energy sources. The presence of major players in the region contributes significantly to market dynamics.South America Frequency Converter Market Report:

In South America, the Frequency Converter market is set to grow from $0.05 billion in 2023 to $0.10 billion by 2033. The development of infrastructure projects and increased investments in mining and energy sectors are expected to fuel market growth in the region.Middle East & Africa Frequency Converter Market Report:

The Middle East and Africa market will also experience growth, increasing from $0.70 billion in 2023 to $1.47 billion by 2033. The expansion of various sectors, coupled with investments in renewable energy infrastructure, fuels market growth in this region.Tell us your focus area and get a customized research report.

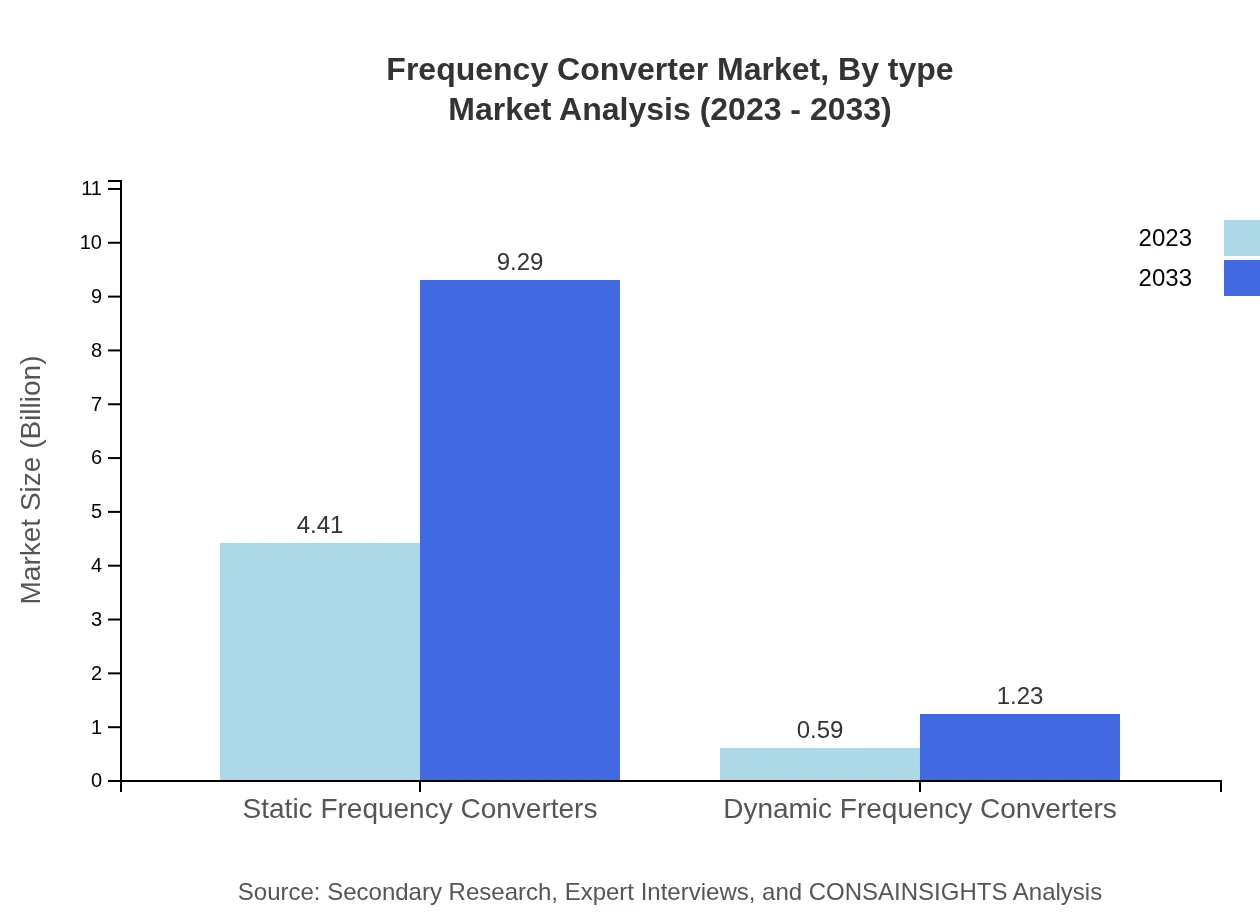

Frequency Converter Market Analysis By Type

The market is categorized into Static Frequency Converters and Dynamic Frequency Converters. In 2023, the Static Frequency Converter segment is valued at $4.41 billion, accounting for 88.28% of the market share, and is projected to grow to $9.29 billion by 2033. Conversely, Dynamic Frequency Converters represent 11.72% of the market share in 2023 and are expected to rise from $0.59 billion to $1.23 billion over the same period.

Frequency Converter Market Analysis By Application

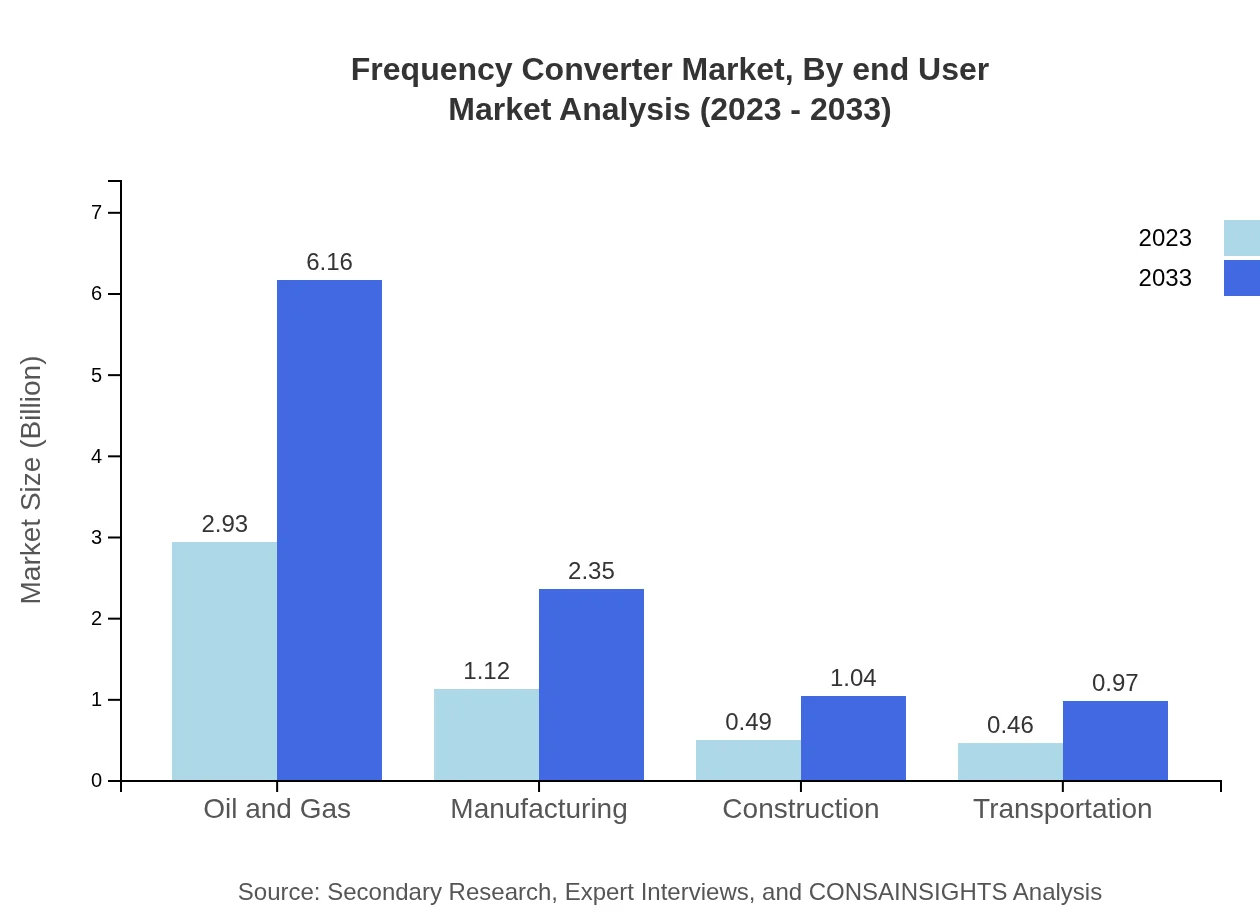

The Frequency Converter market is utilized across various applications such as Oil and Gas, Manufacturing, and Renewable Energy. The Oil and Gas segment is the largest, valued at $2.93 billion (58.55% share) in 2023, and expected to reach $6.16 billion by 2033. Manufacturing captures 22.34% of the market and is projected to grow from $1.12 billion to $2.35 billion in the forecasted period.

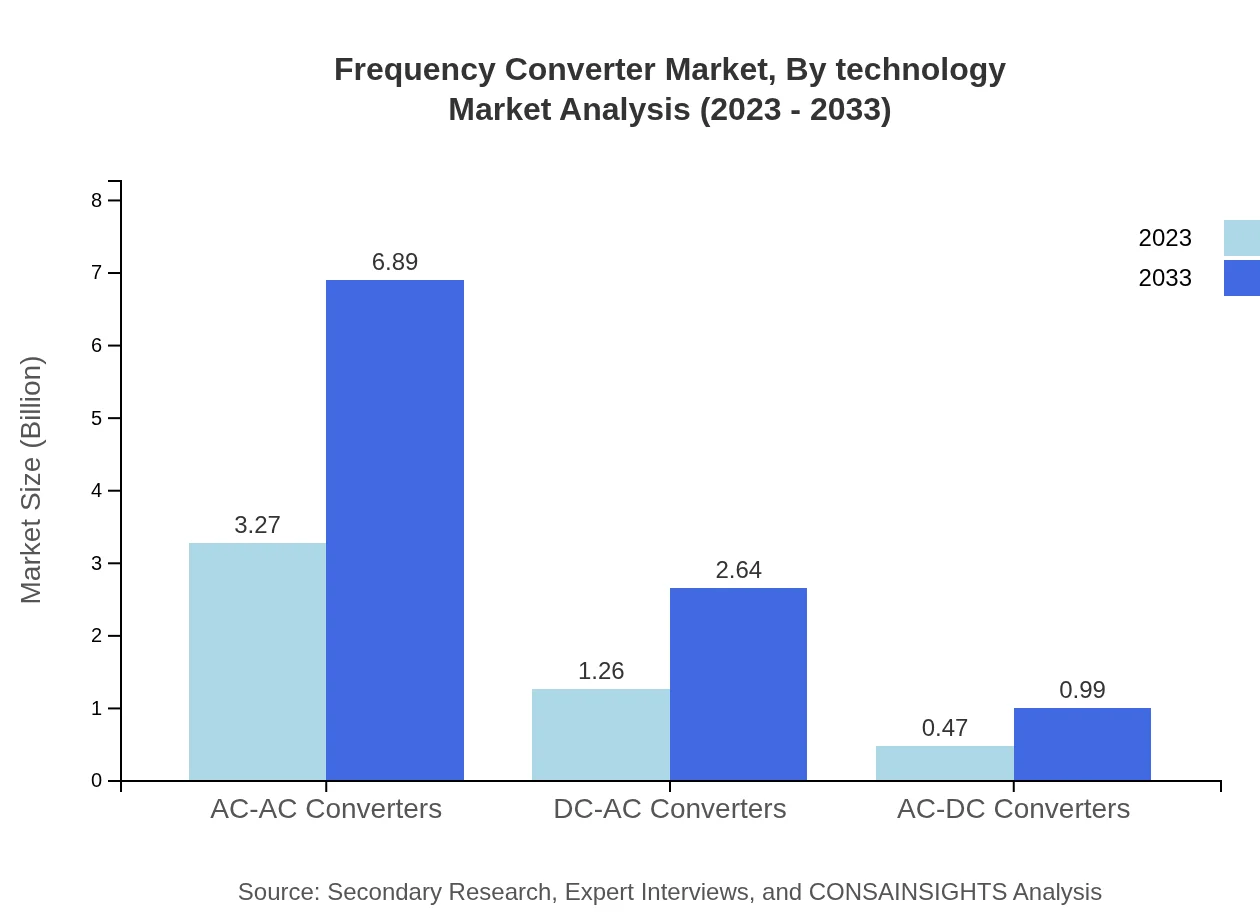

Frequency Converter Market Analysis By Technology

The Frequency Converter market is segmented by technology into AC-AC, DC-AC, and AC-DC converters. AC-AC Converters hold the largest share at 65.45% in 2023, growing from $3.27 billion to $6.89 billion by 2033. DC-AC converters account for 25.11% of the share and are set to increase from $1.26 billion to $2.64 billion, while AC-DC converters cover 9.44% with growth from $0.47 billion to $0.99 billion.

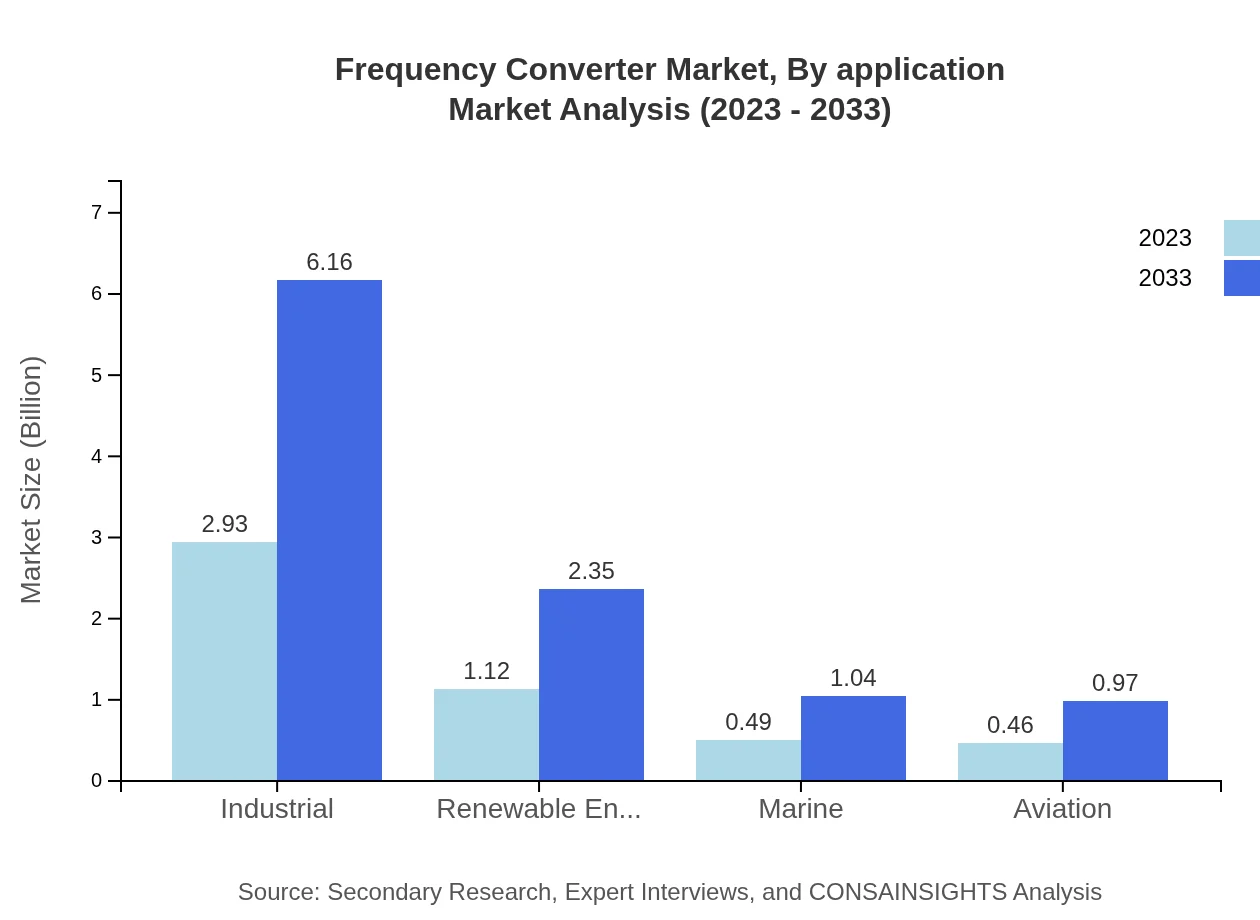

Frequency Converter Market Analysis By End User

End-user sectors for Frequency Converters include Industrial, Renewable Energy, and Marine. The Industrial segment represents the majority with 58.55% market share, forecast to grow from $2.93 billion to $6.16 billion. Renewable Energy comprises 22.34%, expanding from $1.12 billion to $2.35 billion, and the Marine sector follows with 9.85% share, from $0.49 billion to $1.04 billion.

Frequency Converter Market Analysis By Power Rating

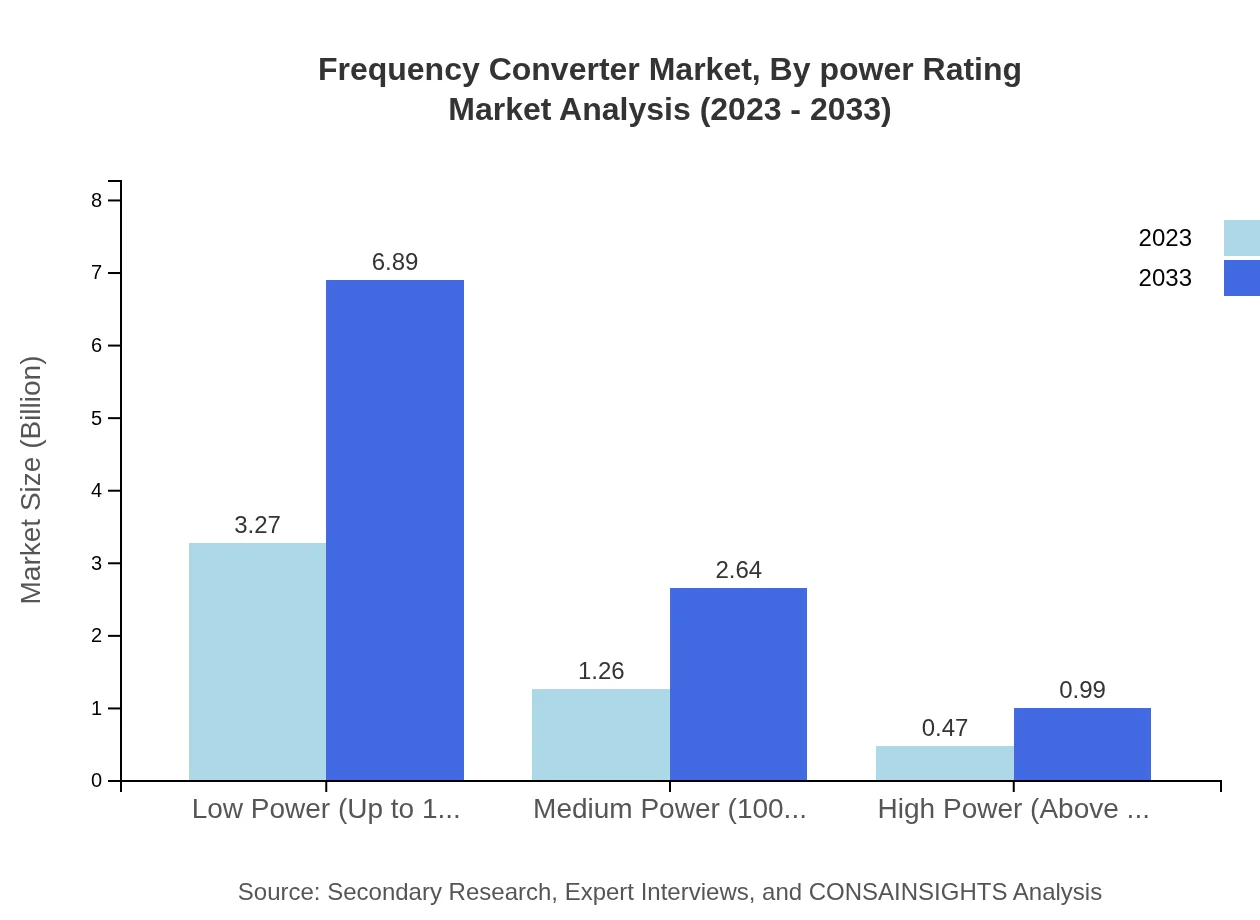

By power rating, the market is divided into Low Power (Up to 100 kVA), Medium Power (100 kVA - 1 MVA), and High Power (Above 1 MVA). Low Power converters dominate both the size and share categories, anticipated to increase from $3.27 billion (65.45%) to $6.89 billion over the next decade. Medium Power is projected to expand from $1.26 billion (25.11%) to $2.64 billion, while High Power may rise from $0.47 billion (9.44%) to $0.99 billion.

Frequency Converter Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Frequency Converter Industry

Schneider Electric:

A leader in energy management and automation solutions, Schneider Electric offers a wide range of frequency converters that enhance energy efficiency in various applications.Siemens AG:

Siemens is a global powerhouse in electrical engineering, providing advanced frequency converters to optimize performance and energy use across industries.ABB Ltd.:

ABB is known for its pioneering technologies in electric and automation, including innovative frequency converter solutions that cater to both standard and specialized applications.General Electric:

With a strong focus on innovation, GE epitomizes strength in the Frequency Converter market, producing solutions that boost operational efficiency in industrial settings.Mitsubishi Electric:

Mitsubishi Electric provides advanced frequency converter technologies, emphasizing energy-saving features and compatibility with modern industrial applications.We're grateful to work with incredible clients.

FAQs

What is the market size of frequency Converter?

The frequency converter market is estimated to reach $5 billion by 2033, growing at a CAGR of 7.5% from its current size. This growth is driven by increasing demand across various industries for efficient power management and conversion solutions.

What are the key market players or companies in the frequency Converter industry?

Key players in the frequency converter industry include notable manufacturers and solution providers that specialize in power electronic products. Their innovations and competitive strategies significantly impact the market's development and growth trajectory.

What are the primary factors driving the growth in the frequency Converter industry?

The growth drivers for the frequency converter market include increasing demand for energy efficiency, the rise of renewable energy sources, and expansion in industrial automation. Automation and modernization across various sectors are significantly contributing to this market's expansion.

Which region is the fastest Growing in the frequency Converter market?

Europe is the fastest-growing region in the frequency converter market, projecting growth from $1.72 billion in 2023 to $3.63 billion in 2033. Other regions, like North America and Asia-Pacific, also show strong growth potential.

Does ConsaInsights provide customized market report data for the frequency Converter industry?

Yes, ConsaInsights offers customized market report data tailored to the frequency converter industry. Clients can request specific insights and analysis to meet their unique business needs and strategic goals.

What deliverables can I expect from this frequency Converter market research project?

Deliverables from the frequency converter market research project include comprehensive reports, market size analysis, competitive landscape assessments, and future trend predictions, providing actionable insights for stakeholders.

What are the market trends of frequency Converter?

Current trends in the frequency converter market include increased adoption of static and dynamic converters, a shift towards more energy-efficient solutions, and growth in sectors like renewable energy and industrial automation.