Motor Monitoring Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: motor-monitoring

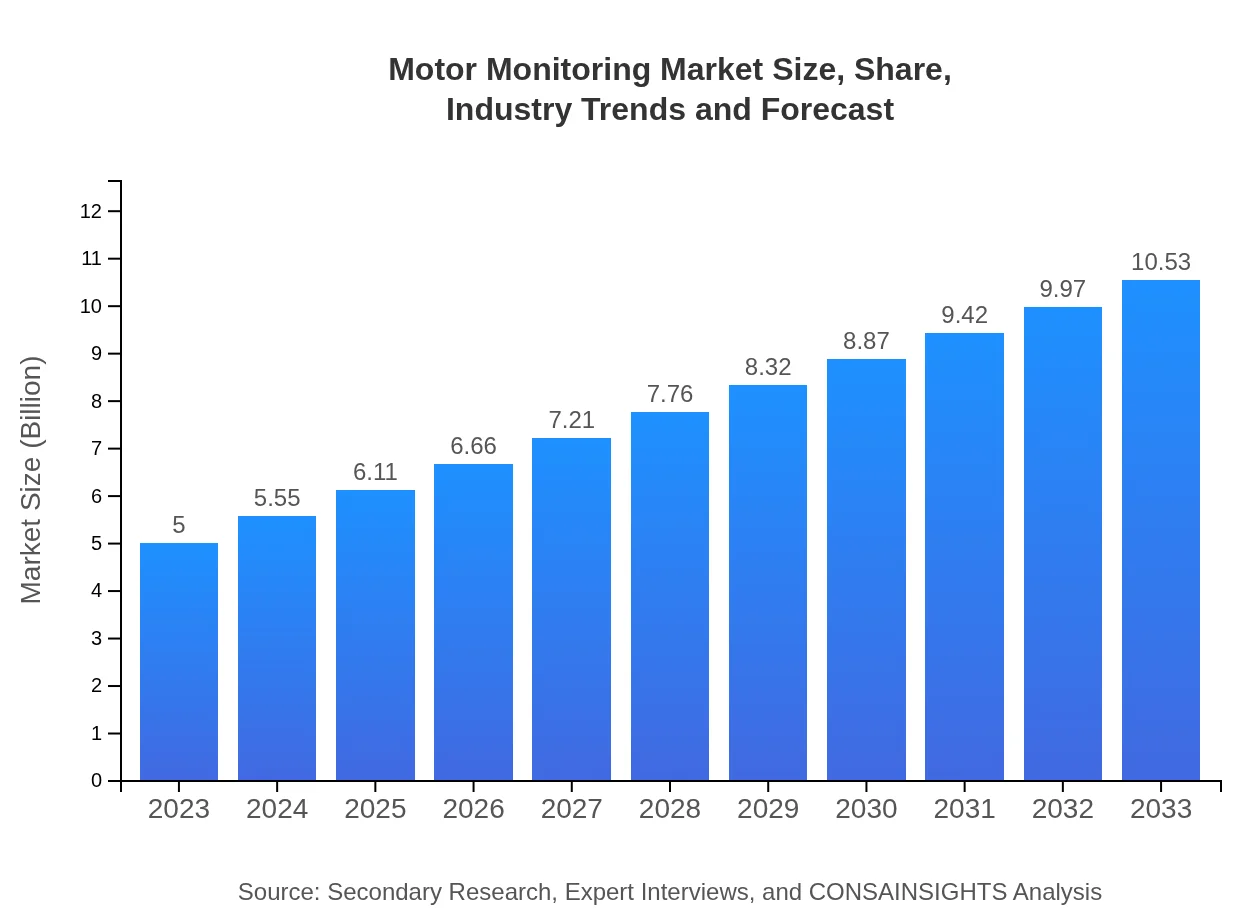

Motor Monitoring Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report covers the comprehensive analysis of the Motor Monitoring market, including market dynamics, segmentation, regional insights, and forecasts for the period from 2023 to 2033, providing valuable data for stakeholders.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Rockwell Automation, ABB, Siemens AG, Schneider Electric |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Motor Monitoring Market Overview

Customize Motor Monitoring Market Report market research report

- ✔ Get in-depth analysis of Motor Monitoring market size, growth, and forecasts.

- ✔ Understand Motor Monitoring's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Motor Monitoring

What is the Market Size & CAGR of Motor Monitoring market in 2023?

Motor Monitoring Industry Analysis

Motor Monitoring Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Motor Monitoring Market Analysis Report by Region

Europe Motor Monitoring Market Report:

The European Motor Monitoring market is valued at $1.32 billion in 2023, expected to double to $2.78 billion by 2033. The emphasis on digital transformation in industries and stringent regulations regarding energy efficiency are driving significant demand for smart monitoring solutions. Countries like Germany and France are at the forefront of adopting innovative technologies.Asia Pacific Motor Monitoring Market Report:

In the Asia Pacific region, the Motor Monitoring market is expected to grow from $1.00 billion in 2023 to $2.10 billion by 2033, exhibiting robust growth fueled by rapid industrialization and increased demand for automation in countries like China and India. Enhanced emphasis on resource optimization and energy efficiency in manufacturing is propelling the adoption of motor monitoring solutions across the region.North America Motor Monitoring Market Report:

North America leads this market with a size of $1.90 billion in 2023, anticipated to rise to $4.01 billion by 2033, indicating a strong CAGR. The region’s growth is driven by advanced technological adoption and extensive investments in automation across various industries, including manufacturing and energy, showcasing a robust inclination towards preventive maintenance solutions.South America Motor Monitoring Market Report:

South America shows a slower growth trajectory, with market values reaching $0.15 billion in 2023 and projected to be $0.31 billion by 2033. The region's growth is hampered by economic fluctuations but supported by increased industrial activity and investments in natural resources, notably in the oil and gas sector, which are expected to drive motor monitoring demand.Middle East & Africa Motor Monitoring Market Report:

In the Middle East and Africa, the motor monitoring market is valued at $0.63 billion in 2023 and projected to grow to $1.33 billion by 2033. The growth in this region is propelled by ongoing infrastructural development and an increase in oil and gas activities, where monitoring solutions are critical for ensuring operational safety and efficiency.Tell us your focus area and get a customized research report.

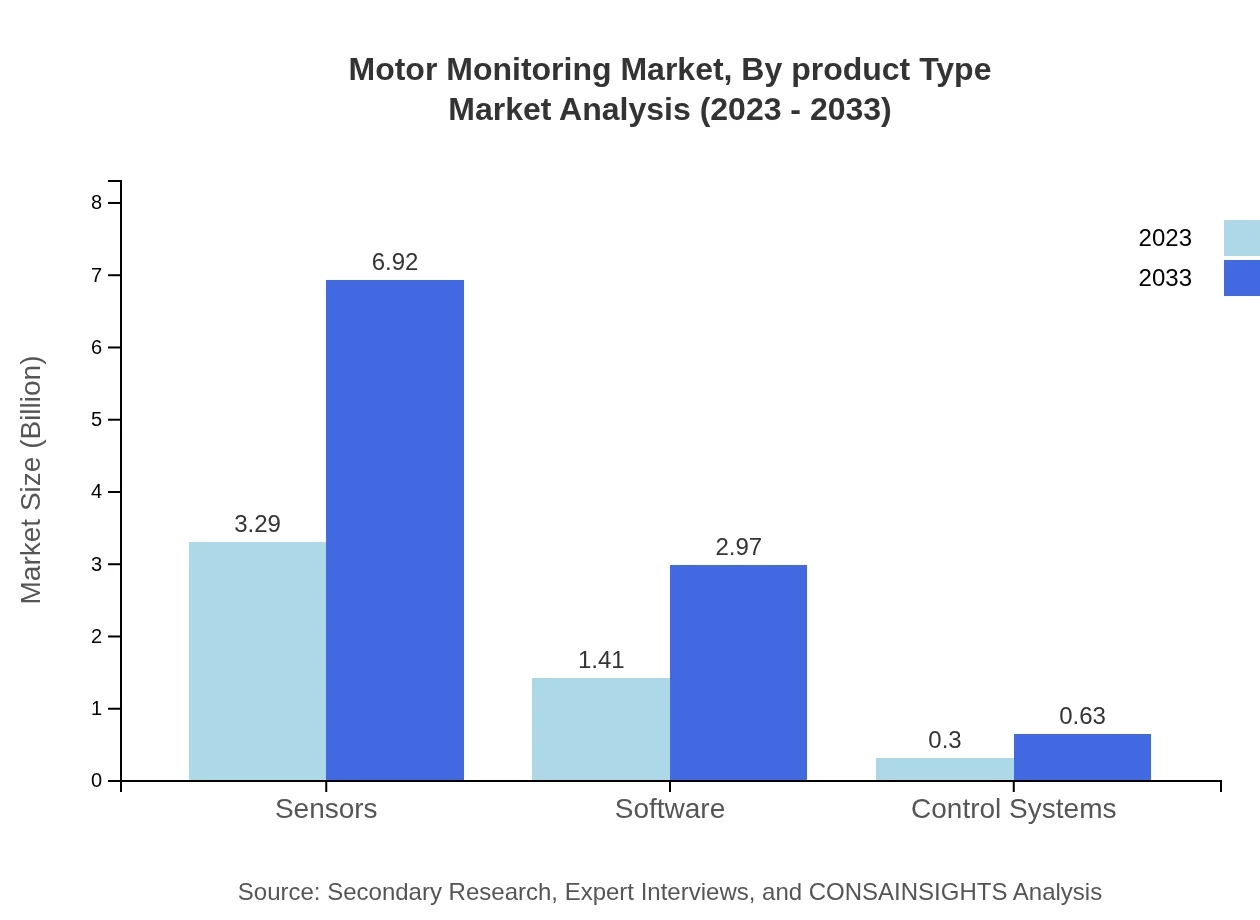

Motor Monitoring Market Analysis By Product Type

The Motor Monitoring market by product type is predominantly shaped by sensors, which held a market size of $3.29 billion in 2023 and are expected to reach $6.92 billion in 2033, maintaining an 83.78% market share. The software segment follows closely, driving additional features like data analytics and visualization for predictive maintenance. Control systems and maintenance services are also critical segments, underscoring their roles in functional efficiency.

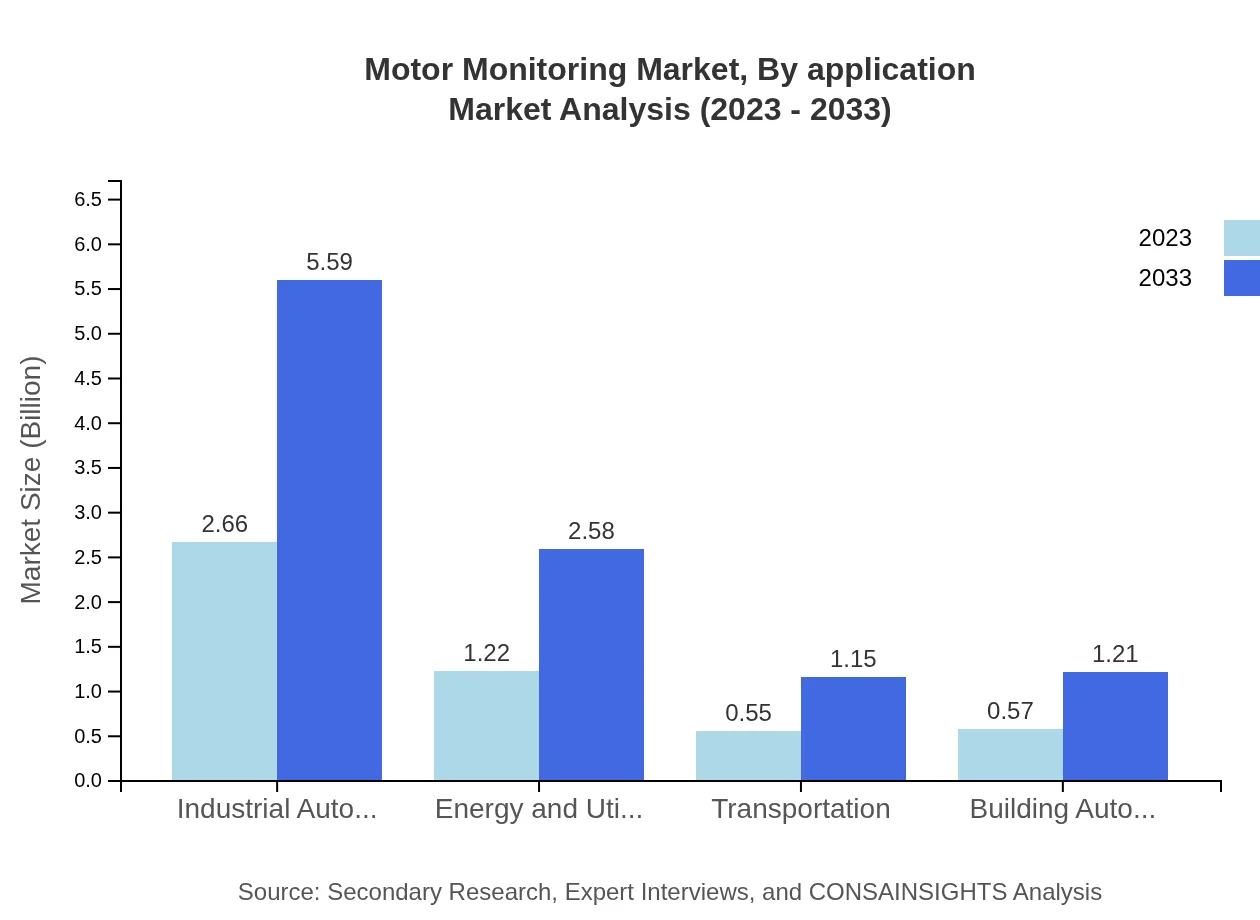

Motor Monitoring Market Analysis By Application

The primary applications of motor monitoring include manufacturing, oil and gas, mining, and chemical processing, with manufacturing leading the segment with $2.66 billion in 2023 postulated to expand to $5.59 billion by 2033. The demand for motor monitoring solutions across these applications is amplified by increasing automation and the need for operational reliability.

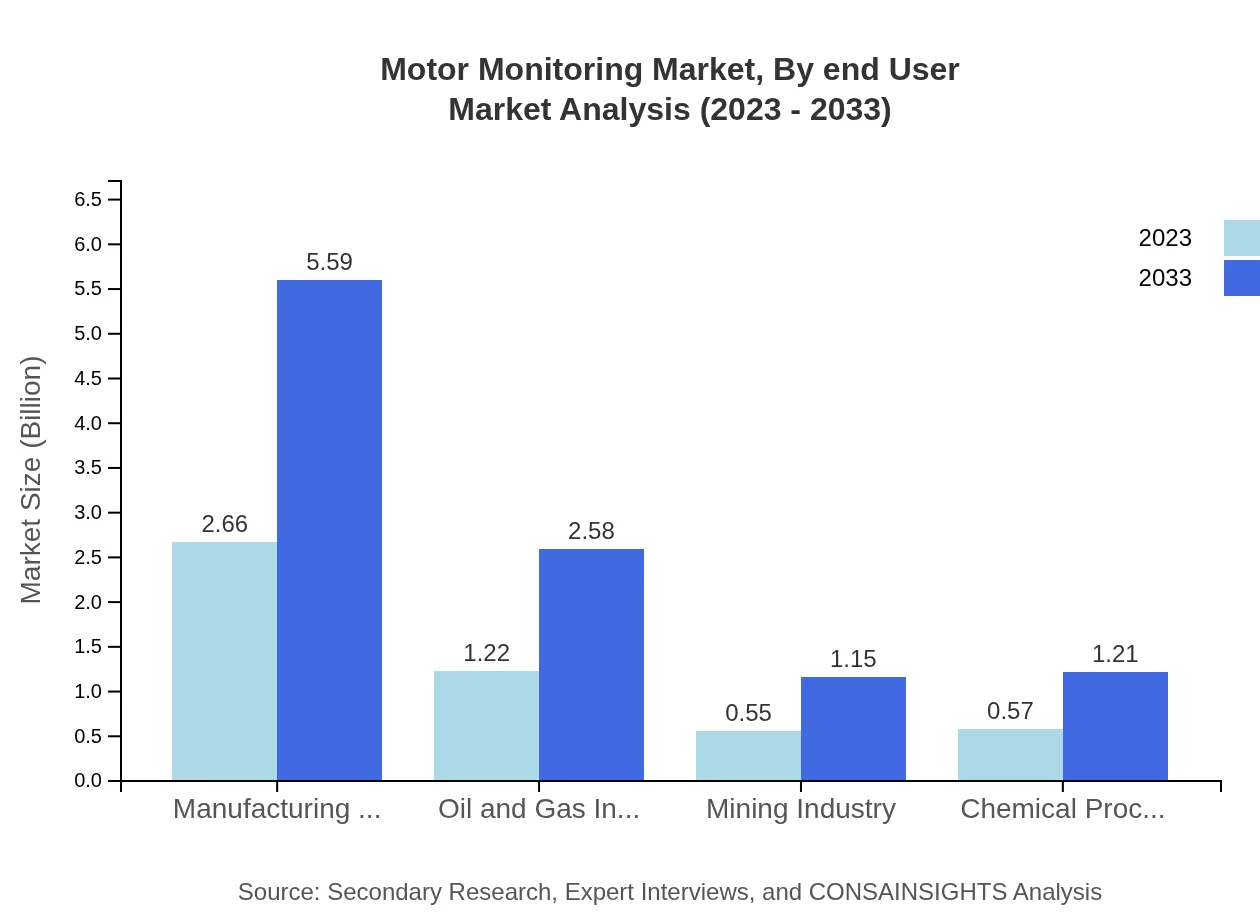

Motor Monitoring Market Analysis By End User

The end-users of motor monitoring technology span various sectors, with the manufacturing industry commanding the largest share at 53.1%, valued at $2.66 billion in 2023. The oil and gas segment follows, illustrating the critical nature of real-time monitoring in these high-value industries.

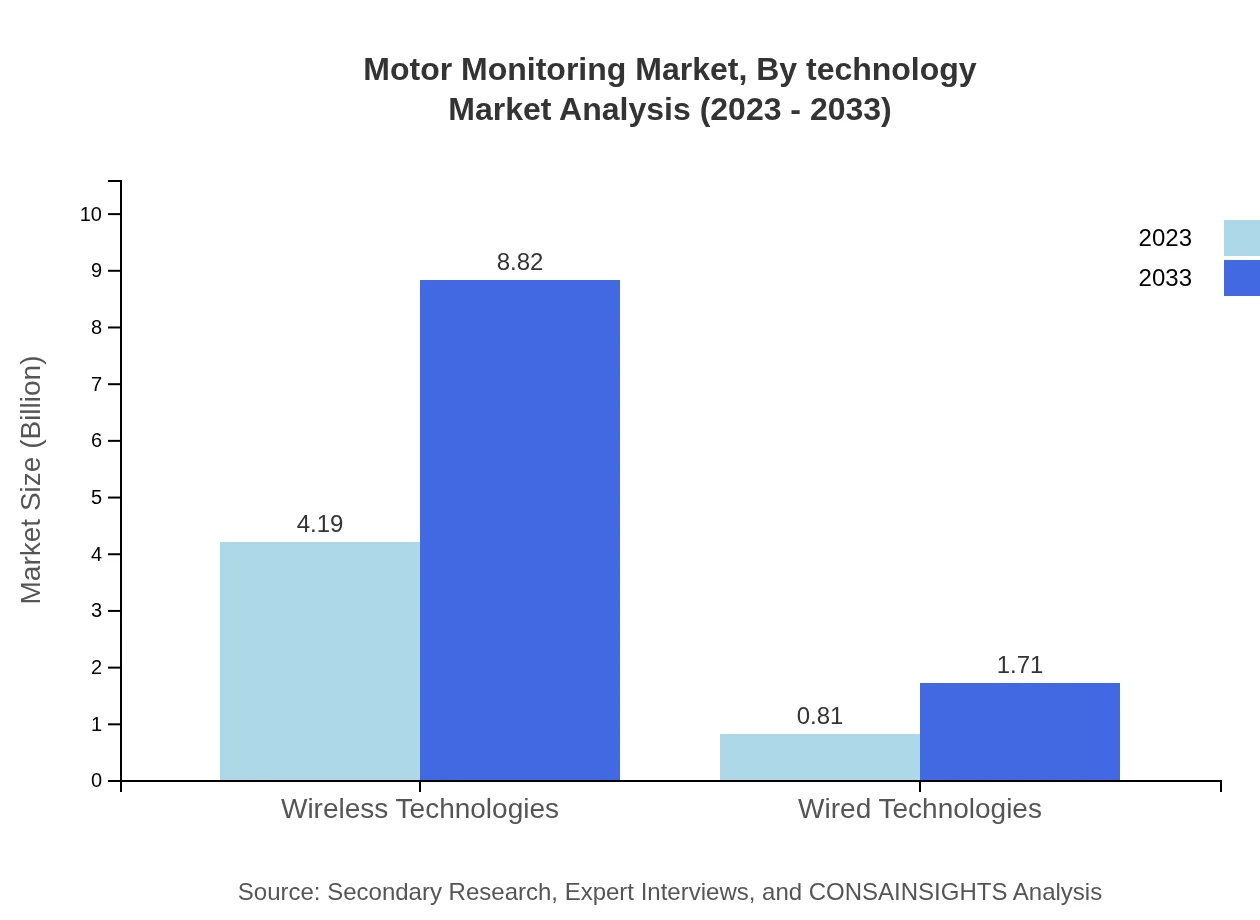

Motor Monitoring Market Analysis By Technology

The increasing adoption of wireless technologies is evident as they capture the majority share of 83.78% in the Motor Monitoring market. Wireless sensors enhance flexibility in monitoring operations, leading to better data acquisition. Wired technologies, while holding a smaller market share of 16.22%, continue to be relevant where physical connections are preferred for reliability.

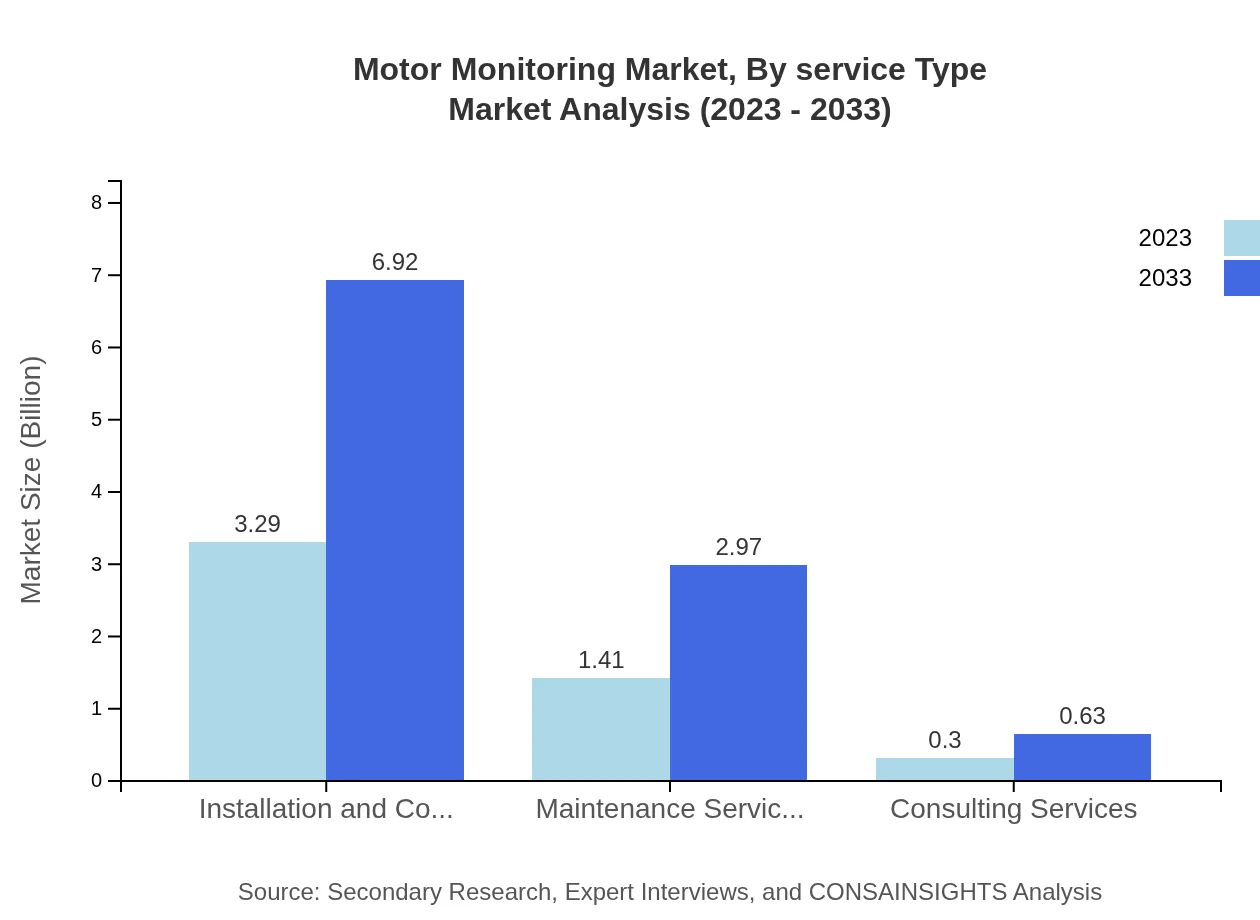

Motor Monitoring Market Analysis By Service Type

Service types within the Motor Monitoring market cover installation, maintenance, and consulting services, with installation and commissioning holding a significant segment share of 65.74%. These services are crucial for ensuring effective deployment and continuous performance optimization of monitoring systems across various industrial applications.

Motor Monitoring Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Motor Monitoring Industry

Rockwell Automation:

Rockwell Automation provides integrated control and information solutions that optimize energy efficiency and operational productivity across various industries.ABB:

ABB offers a wide range of motor monitoring solutions, focusing on industrial automation, robotics, and digitalization to enhance production efficiency and reduce downtime.Siemens AG:

Siemens is a global leader in electric engineering and electronics, providing innovative motor monitoring solutions that integrate IoT capabilities for smart manufacturing.Schneider Electric:

Schneider Electric specializes in energy management and automation solutions, delivering advanced motor monitoring systems designed to optimize performance and reduce operational costs.We're grateful to work with incredible clients.

FAQs

What is the market size of motor Monitoring?

The motor-monitoring market is valued at approximately $5 billion in 2023, with a projected compound annual growth rate (CAGR) of 7.5%. This growth reflects the increasing demand for motor monitoring solutions across various industries.

What are the key market players or companies in this motor Monitoring industry?

The motor-monitoring industry is significantly influenced by key players such as Siemens, Rockwell Automation, Schneider Electric, ABB, and Honeywell. These companies contribute innovative technologies and solutions to enhance motor efficiency and reliability.

What are the primary factors driving the growth in the motor Monitoring industry?

Key growth drivers for the motor-monitoring industry include the rise in industrial automation, increasing demand for energy-efficient systems, and the adoption of predictive maintenance techniques. Additionally, regulatory standards are pushing industries to invest in smart monitoring solutions.

Which region is the fastest Growing in the motor Monitoring?

North America is poised to be the fastest-growing region in the motor-monitoring market, expected to rise from $1.90 billion in 2023 to $4.01 billion by 2033. This growth is fueled by advancements in industrial automation and IoT technologies.

Does ConsaInsights provide customized market report data for the motor Monitoring industry?

Yes, ConsaInsights offers customized market report data specifically tailored to the motor-monitoring industry. Clients can expect detailed analyses that align with their specific business needs and objectives.

What deliverables can I expect from this motor Monitoring market research project?

Typical deliverables from a motor-monitoring market research project include comprehensive market analysis reports, segmentation studies, competitive landscape insights, and forecasts of industry trends up to the year 2033.

What are the market trends of motor Monitoring?

Market trends in motor monitoring include the rising integration of AI and IoT technologies, a shift towards wireless monitoring solutions, and an increasing emphasis on preventive maintenance to reduce operational downtime and enhance efficiency.