Reports >

Automotive And Mobility

>

Gdi System Market Report

Gdi System Market Report

First published: 27 September 2024 | Last updated: 02 February 2026 | Report Code: gdi-system

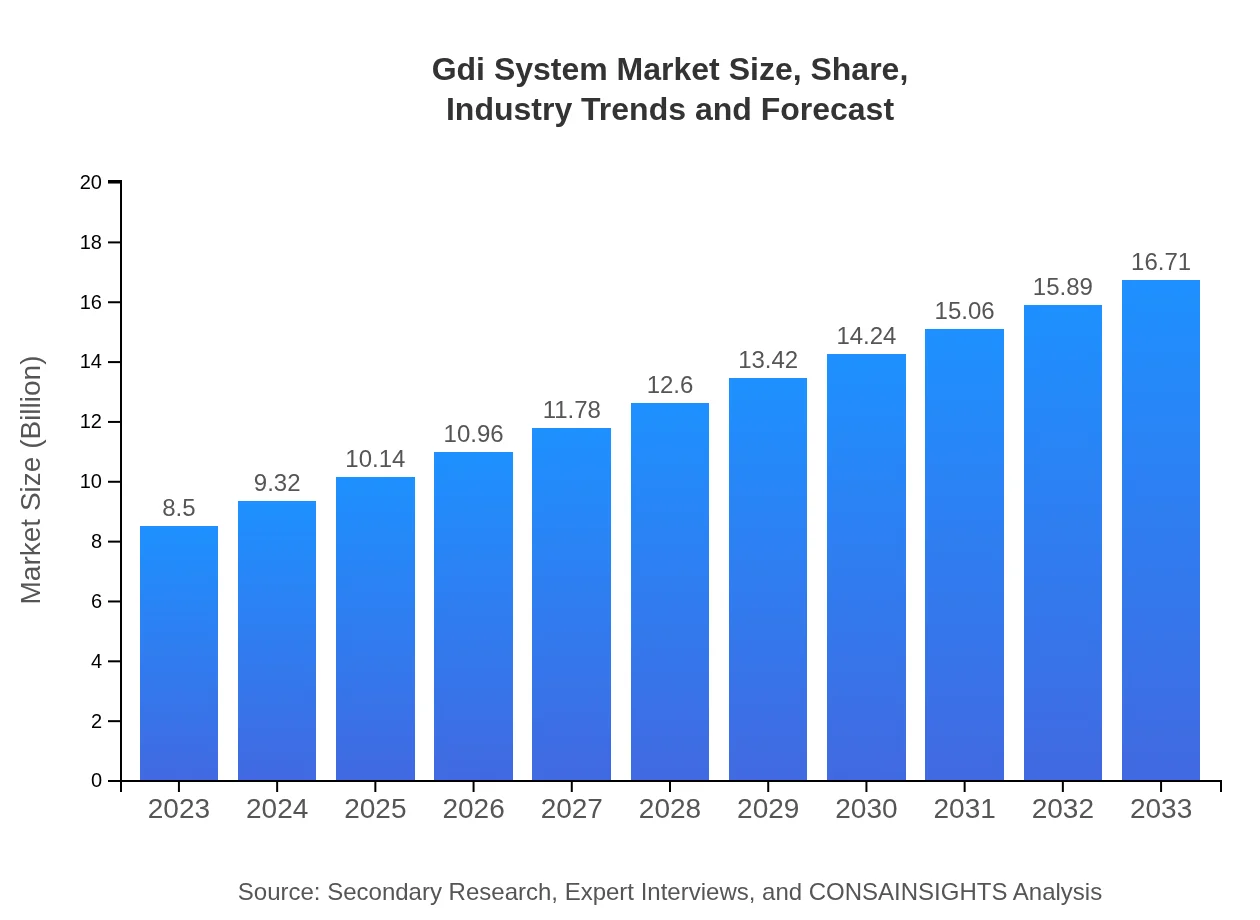

Gdi System Market — USD 8.5 billion in 2023, Growing to USD 16.71B by 2033 at 6.8% CAGR

This report provides an in-depth analysis of the Gdi System market, covering market size, growth trends, regional insights, and future forecasts for the period 2023 to 2033. It offers a comprehensive overview of industry dynamics and key players shaping the market landscape.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $8.50 Billion |

| CAGR (2023-2033) | 6.8% |

| 2033 Market Size | $16.71 Billion |

| Top Companies | Siemens AG, IBM Corporation, Schneider Electric, Honeywell International Inc. |

| Published Date | 27 September 2024 |

| Last Modified Date | 02 February 2026 |

Gdi System Market Overview

Customize Gdi System Market Report market research report

- ✔ Get in-depth analysis of Gdi System market size, growth, and forecasts.

- ✔ Understand Gdi System's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Gdi System

What is the Market Size & CAGR of Gdi System market in 2023?

Gdi System Industry Analysis

Gdi System Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Gdi System Market Analysis Report by Region

Europe Gdi System Market Report:

Europe's Gdi System market is forecasted to grow from $2.90 billion in 2023 to $5.70 billion by 2033. The region's commitment to sustainability and digital transformation in industries such as manufacturing and energy drives investment in Gdi Systems.Asia Pacific Gdi System Market Report:

The Asia-Pacific region is expected to experience significant growth, with the market projected to reach $2.70 billion by 2033, up from $1.37 billion in 2023. This growth is driven by increasing industrial automation and government initiatives promoting smart manufacturing and smart city solutions.North America Gdi System Market Report:

North America leads in the Gdi System market with a projected increase from $2.99 billion in 2023 to $5.87 billion by 2033. The presence of key technology players, coupled with a strong focus on innovation and advanced infrastructure, continues to fuel market expansion.South America Gdi System Market Report:

In South America, the Gdi System market is poised for a gradual increase from $0.65 billion in 2023 to $1.28 billion by 2033. The growth will be supported by investments in infrastructure and digital technologies aimed at improving operational efficiencies across various industries.Middle East & Africa Gdi System Market Report:

In the Middle East and Africa, the market is estimated to increase from $0.59 billion in 2023 to $1.16 billion by 2033, as improving economic conditions and technological adoption accelerate growth in key sectors.Tell us your focus area and get a customized research report.

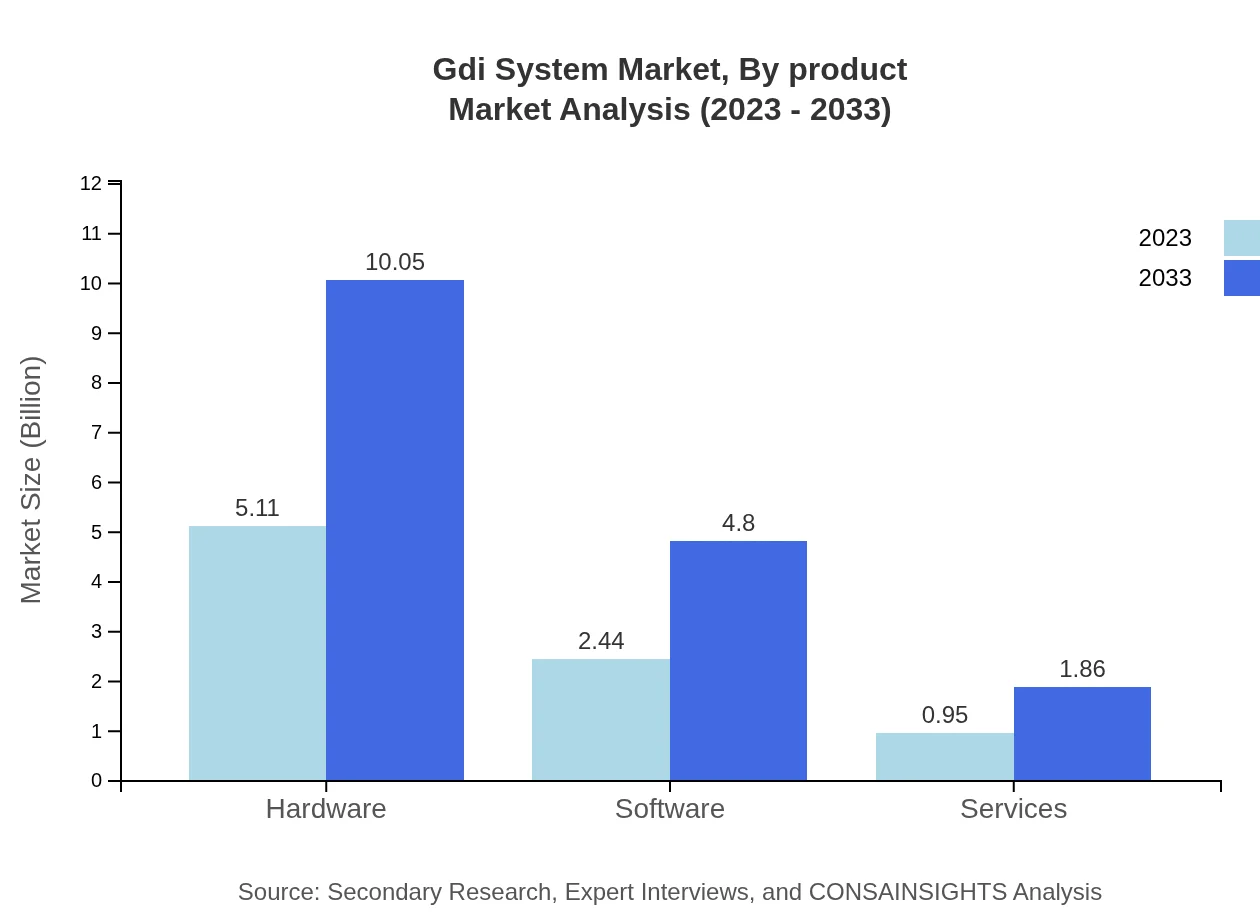

Gdi System Market Analysis By Product

The GDI system market is heavily dominated by hardware, which accounts for a substantial market share of 60.16% in 2023. The hardware market size is expected to grow from $5.11 billion in 2023 to $10.05 billion by 2033, indicating robust demand. Software solutions, critical for data management and analysis, will expand from $2.44 billion to $4.80 billion, maintaining a market share of 28.71%. Services provided alongside these products, growing from $0.95 billion to $1.86 billion, represent 11.13% of the market.

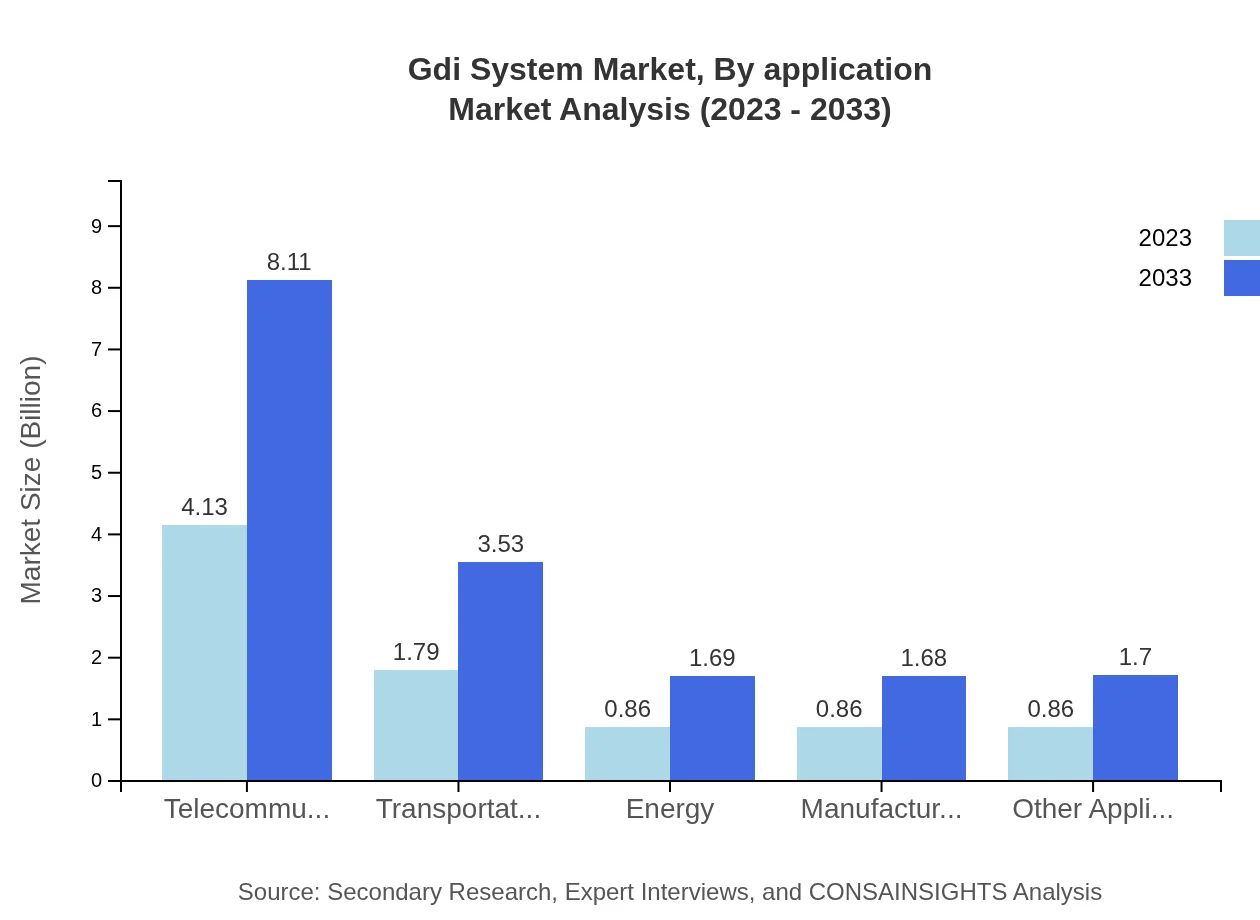

Gdi System Market Analysis By Application

The telecom industry remains the largest application segment within the GDI system market, increasing from $4.13 billion in 2023 to $8.11 billion in 2033. Logistics and transportation applications also show growth potential, anticipated to rise from $1.79 billion to $3.53 billion. The energy sector, while smaller, is expected to see consistent growth driven by renewable energy initiatives, increasing from $0.86 billion to $1.69 billion.

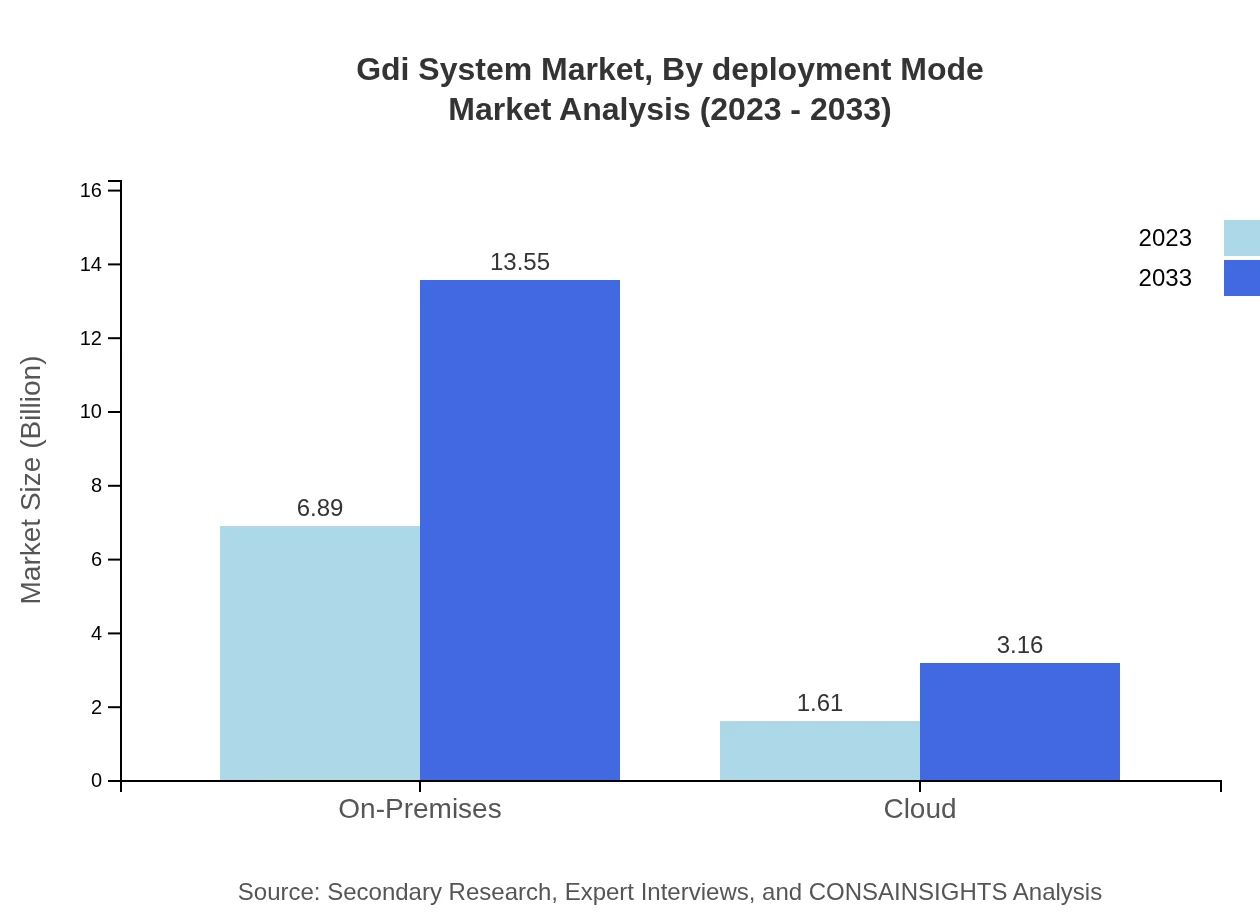

Gdi System Market Analysis By Deployment Mode

In terms of deployment modes, on-premises solutions currently dominate the market, representing 81.09% with a market size of $6.89 billion in 2023. However, cloud-based deployments are growing, anticipated to increase from $1.61 billion to $3.16 billion, capturing the shift toward flexible and scalable IT infrastructures.

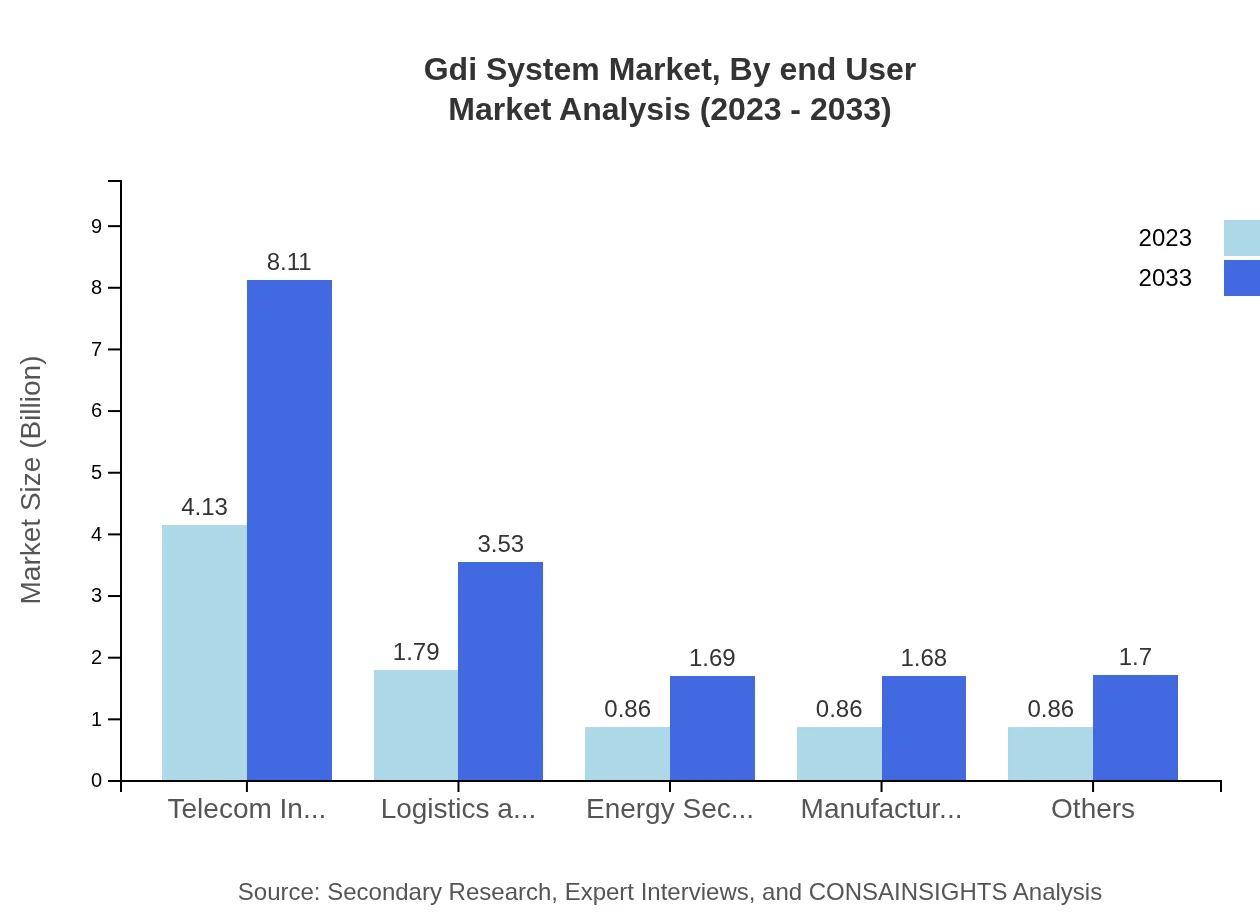

Gdi System Market Analysis By End User

The manufacturing sector is a significant user of GDI systems, projecting growth from $0.86 billion in 2023 to $1.68 billion by 2033. Other key industries include energy, healthcare, and transportation, which are increasingly adopting GDI systems for improved efficiency and data management.

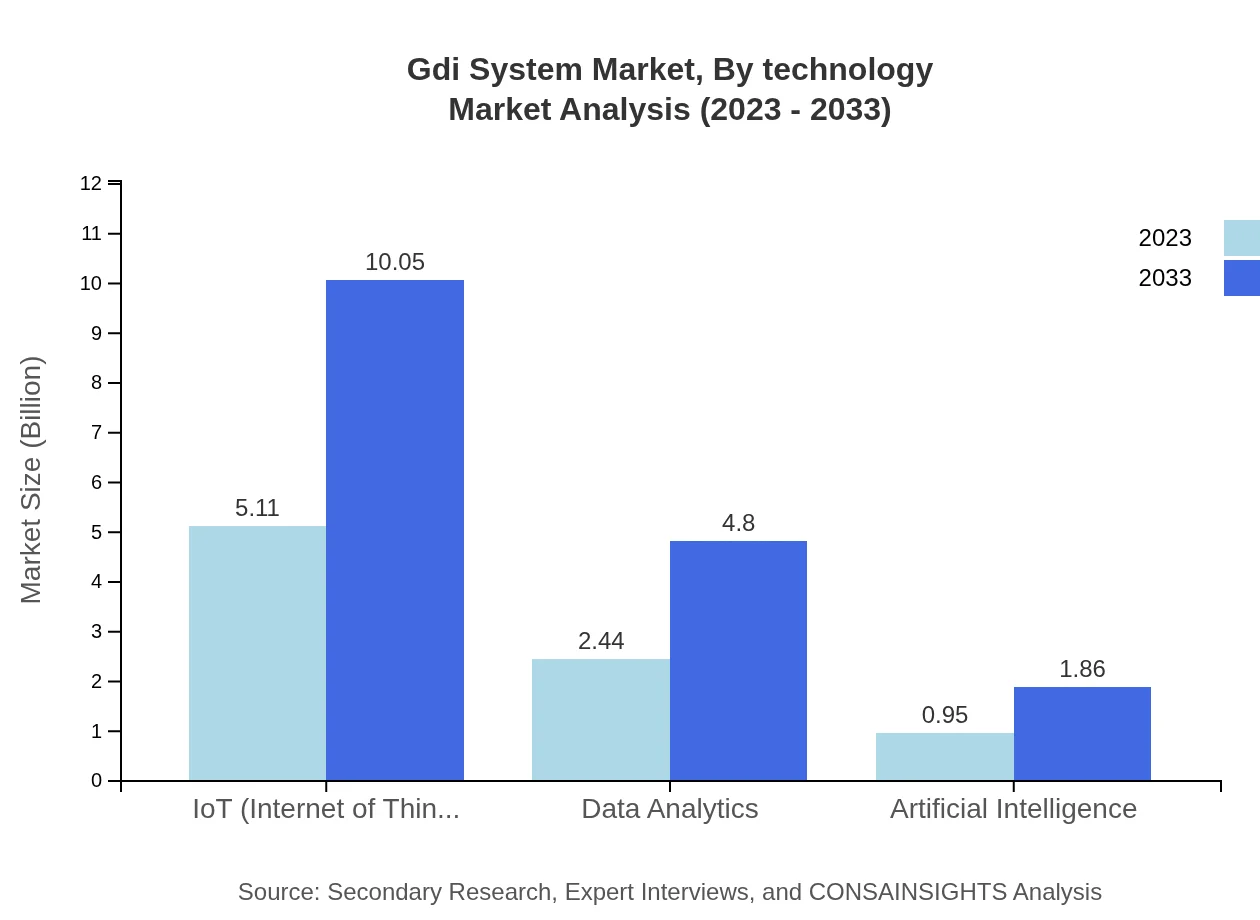

Gdi System Market Analysis By Technology

The integration of IoT technology has become crucial across various applications, representing a significant trend in the GDI system market. Increased connectivity and data collection capabilities are driving growth, with the IoT segment expected to grow from $5.11 billion to $10.05 billion over the forecast period.

Gdi System Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Gdi System Industry

Siemens AG:

Siemens AG is a leading global technology company that specializes in automation and digitalization in various industries, including manufacturing and energy.IBM Corporation:

IBM Corporation is recognized for its advanced data analytics and cloud solutions, playing a pivotal role in shaping the Gdi System landscape.Schneider Electric:

Schneider Electric focuses on energy management and automation solutions, driving sustainability and efficiency in various sectors.Honeywell International Inc.:

Honeywell International offers a wide array of solutions in automation and control, contributing significantly to advancements in the Gdi System market.We're grateful to work with incredible clients.

FAQs

What is the market size of gdi System?

The GDI System market size is projected to reach $8.5 billion by 2033, growing at a CAGR of 6.8%. This growth is driven by increasing demand across various sectors, enhanced by technological advancements and heightened awareness regarding efficient data systems.

What are the key market players or companies in this gdi System industry?

Key players in the GDI system industry include major technology companies that specialize in IoT, data analytics, and AI solutions, focusing on device integration and management, which are essential for fostering innovation and industry growth.

What are the primary factors driving the growth in the gdi System industry?

The growth in the GDI system industry is driven by technological advancements, increasing adoption of IoT, and rising demand for data analytics across sectors, improving operational efficiencies and decision-making processes.

Which region is the fastest Growing in the gdi System?

North America is the fastest-growing region for the GDI System, with a market size projected to reach $5.87 billion by 2033, followed closely by Europe, with significant investments in technological infrastructure.

Does ConsaInsights provide customized market report data for the gdi System industry?

Yes, ConsaInsights offers customized market report data tailored to specific needs within the GDI system industry, helping clients make informed strategic decisions based on personalized insights.

What deliverables can I expect from this gdi System market research project?

Deliverables include detailed market analysis, segmentation data, forecasts, trend insights, and competitive landscape assessments to support strategic planning and investment decisions in the GDI system industry.

What are the market trends of gdi System?

Market trends for the GDI System indicate a shift towards cloud-based solutions, increasing integration of AI and IoT technologies, and a focus on sustainability and efficiency in operations across various industries.