Reports >

Chemicals And Materials

>

Geocells Market Report

Geocells Market Report

First published: 04 October 2024 | Last updated: 02 February 2026 | Report Code: geocells

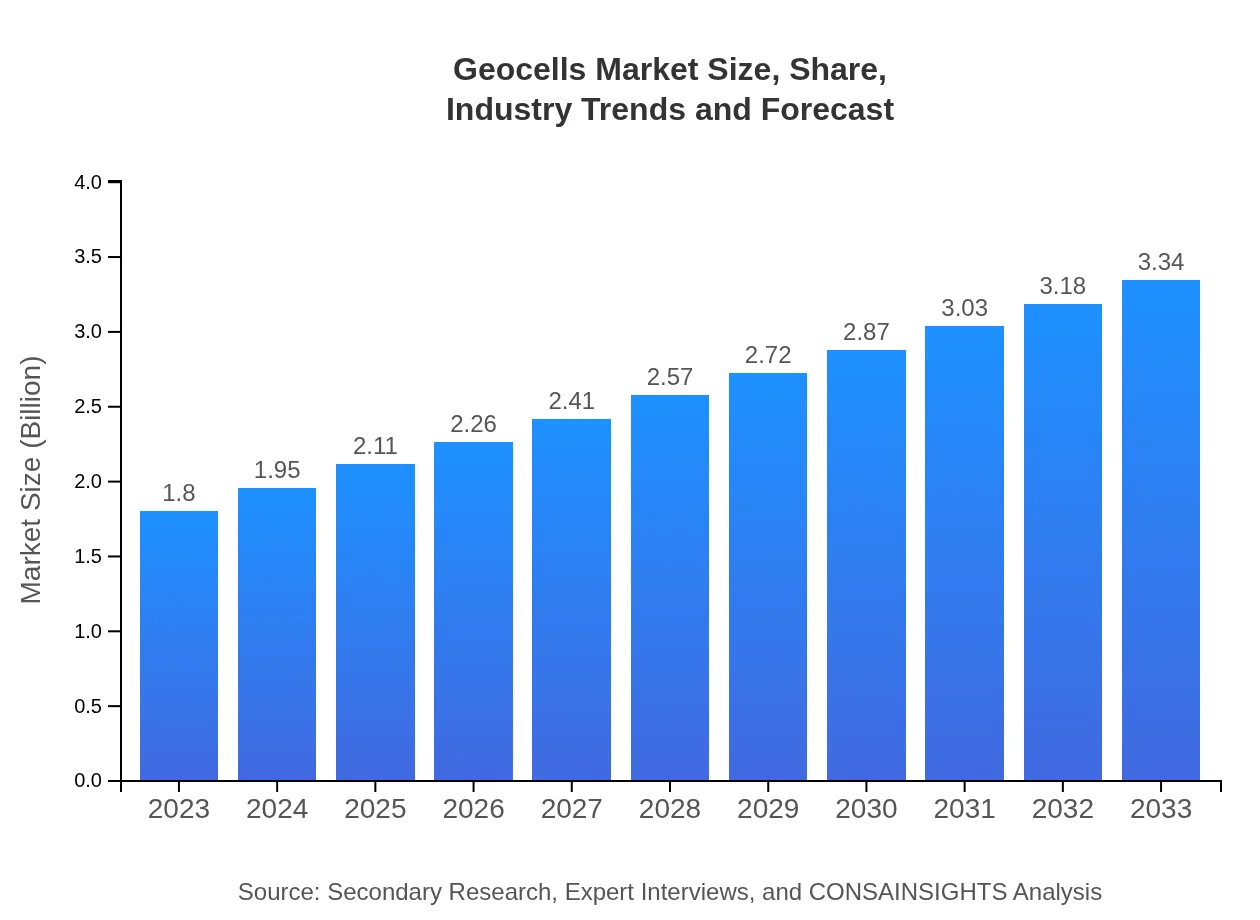

Geocells Market — USD $1.8 Billion in 2023, Growing to USD 3.34null by 2033 at 6.2% CAGR

This report provides a comprehensive analysis of the Geocells market, including insights on market trends, size, growth potential, and regional dynamics from 2023 to 2033.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $1.80 Billion |

| CAGR (2023-2033) | 6.2% |

| 2033 Market Size | $3.34 Billion |

| Top Companies | Presto Geosystems, Geosynthetics Engineering, Tensar Corporation, ABG Geosynthetics |

| Published Date | 04 October 2024 |

| Last Modified Date | 02 February 2026 |

Geocells Market Overview

Customize Geocells Market Report market research report

- ✔ Get in-depth analysis of Geocells market size, growth, and forecasts.

- ✔ Understand Geocells's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Geocells

What is the Market Size & CAGR of Geocells market in 2023?

Geocells Industry Analysis

Geocells Market Segmentation and Scope

Tell us your focus area and get a customized research report.

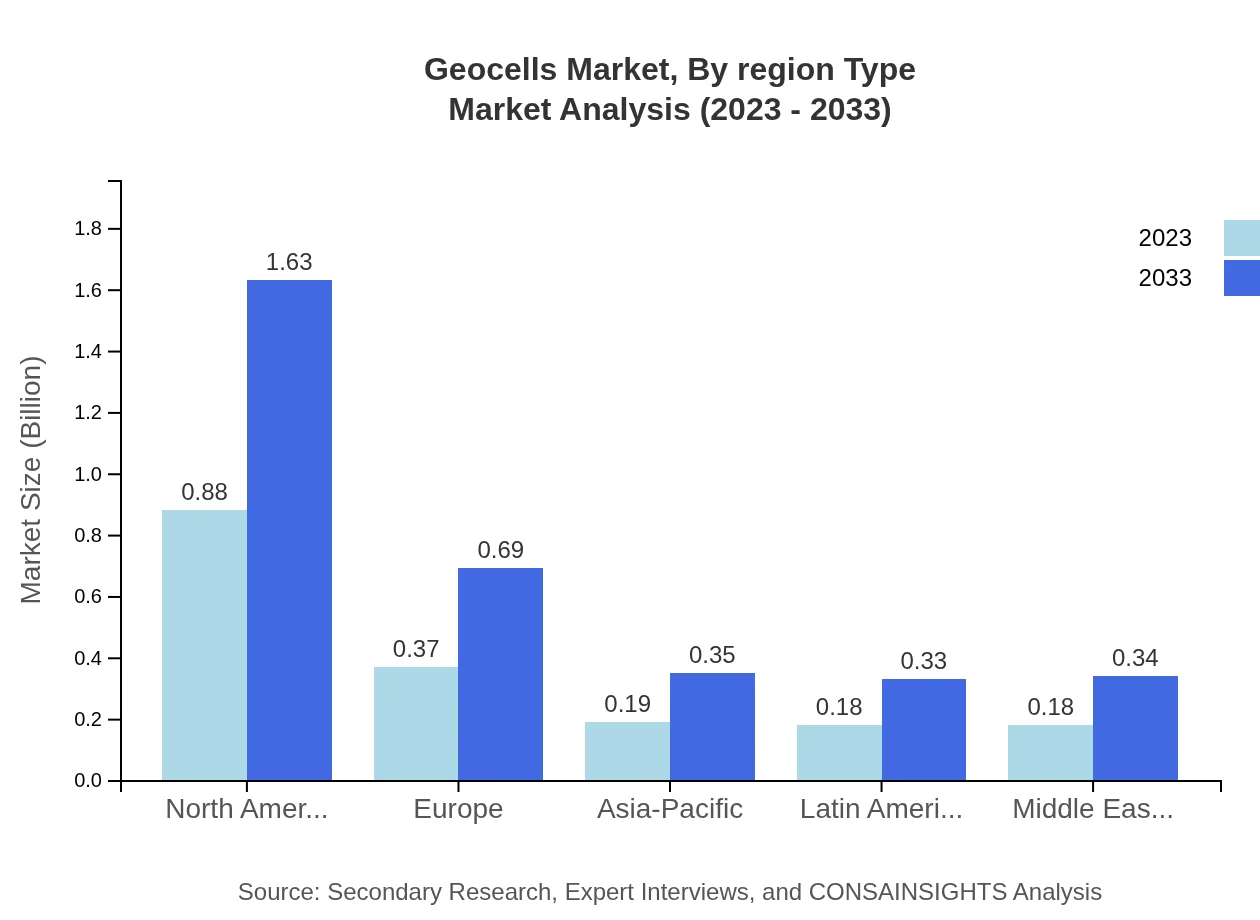

Geocells Market Analysis Report by Region

Europe Geocells Market Report:

Europe’s geocells market is forecasted to expand from $0.48 billion in 2023 to $0.90 billion by 2033. This growth is attributed to the region's focus on sustainability and the adoption of innovative solutions in civil engineering projects to combat soil erosion and enhance structural integrity.Asia Pacific Geocells Market Report:

The Asia Pacific region is expected to witness substantial growth, with the market anticipated to increase from $0.37 billion in 2023 to $0.69 billion by 2033. This growth is fueled by rapid urbanization and increasing infrastructural development across countries like China and India, where geocells are utilized for several applications including road construction and soil erosion control.North America Geocells Market Report:

North America leads the market with an expected growth from $0.65 billion in 2023 to $1.20 billion in 2033. The emphasis on sustainable construction practices and infrastructure renewal, alongside regulatory support for environmentally friendly technologies, is significantly boosting demand for geocells in the US and Canada.South America Geocells Market Report:

In South America, the geocells market is projected to grow from $0.08 billion in 2023 to $0.15 billion by 2033. The increasing need for sustainable solutions in response to environmental challenges, combined with investments in infrastructure, is aiding market growth particularly in Brazil and Argentina.Middle East & Africa Geocells Market Report:

The Middle East and Africa are projected to increase from $0.21 billion in 2023 to $0.40 billion by 2033. The growth in this region is primarily driven by the expanding construction activities and increased investments in infrastructure, especially in Gulf Cooperation Council (GCC) countries.Tell us your focus area and get a customized research report.

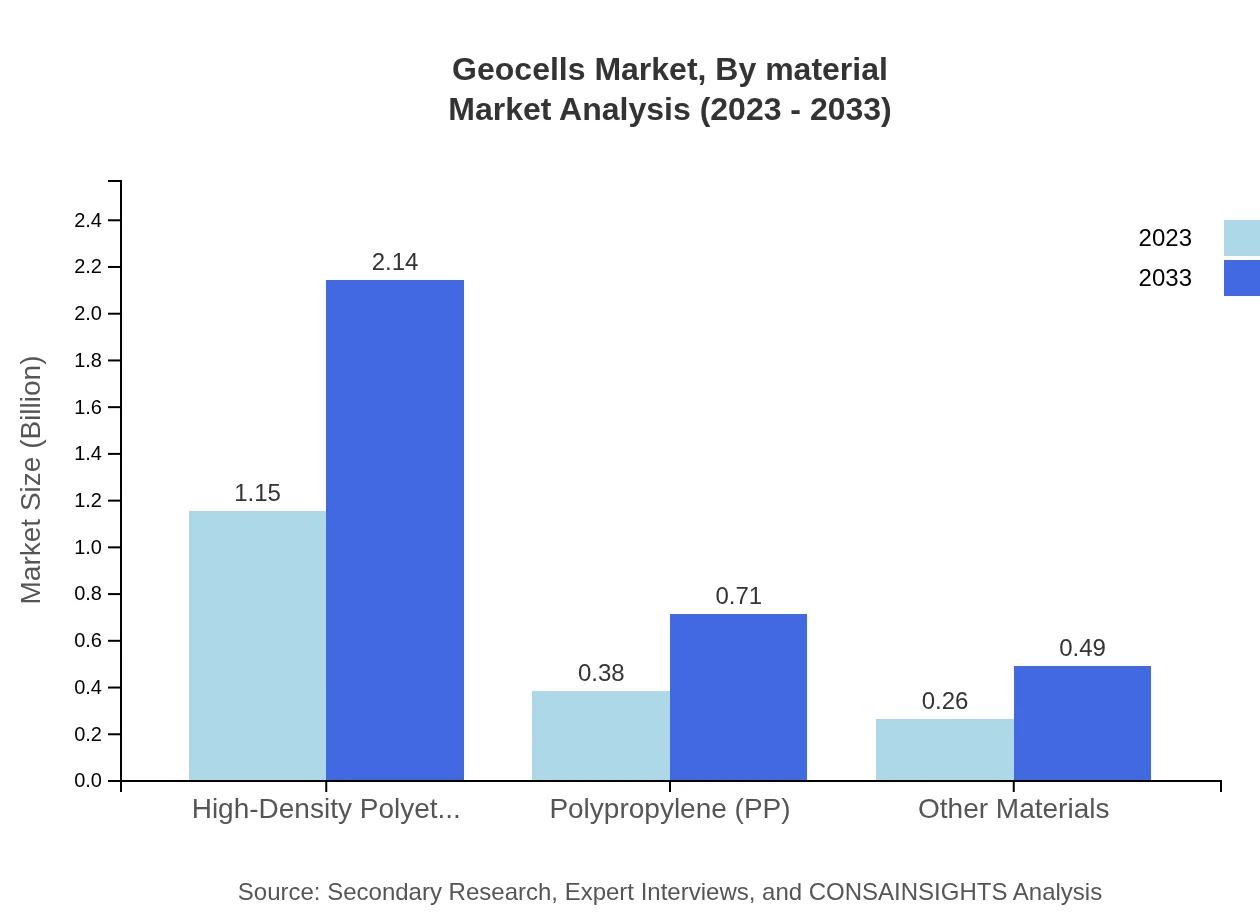

Geocells Market Analysis By Material

The market segmentation by material shows that High-Density Polyethylene (HDPE) remains the dominant material in the Geocells market, holding a 64.04% share in 2023. The market is expected to grow from $1.15 billion to $2.14 billion by 2033, highlighting its essential role due to durability and resistance to environmental factors. Polypropylene (PP) follows with a 21.31% share, projected to increase from $0.38 billion in 2023 to $0.71 billion by 2033, offering notable flexibility and strength.

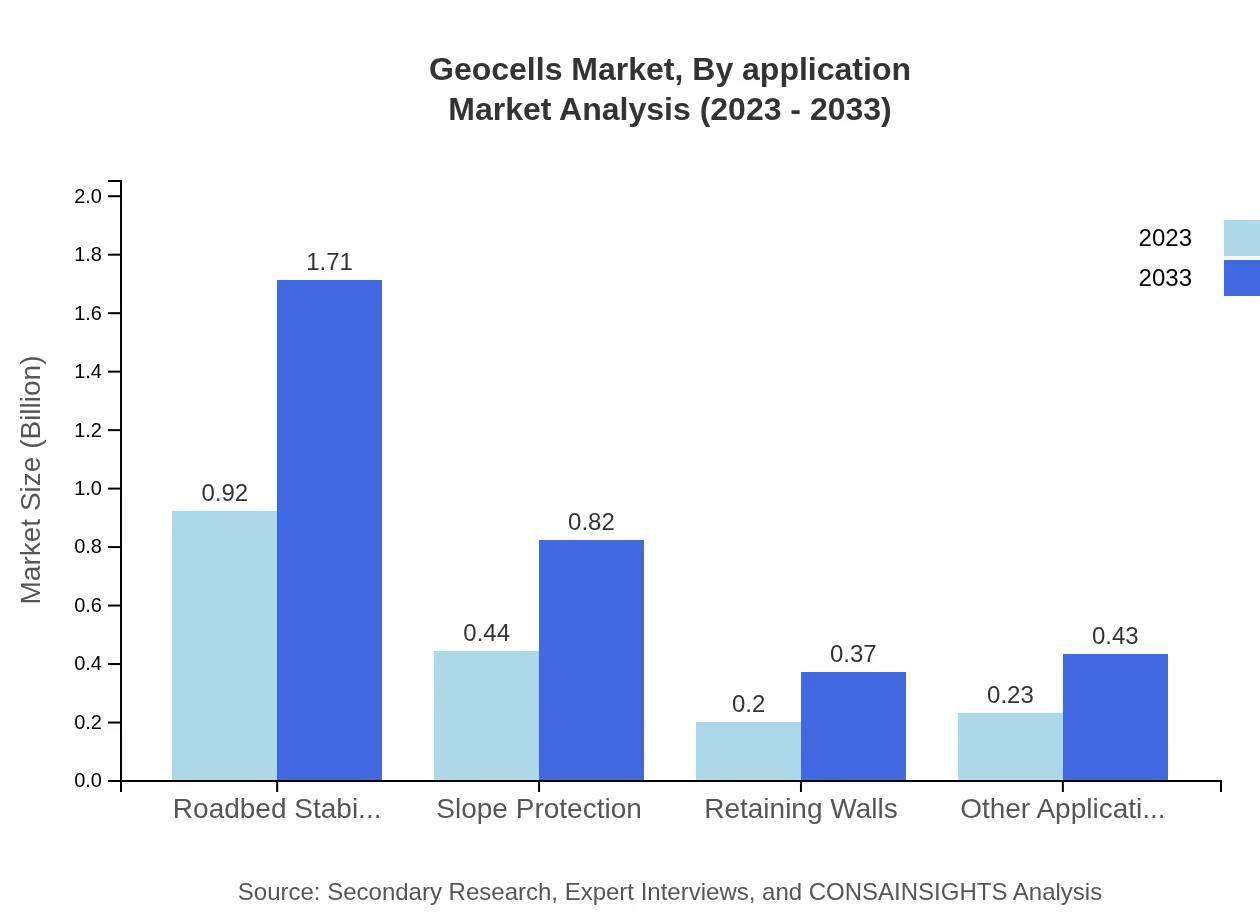

Geocells Market Analysis By Application

By application, the geocells market in construction is anticipated to command 51.34% market share for the forecasted period, expanding from $0.92 billion to $1.71 billion by 2033. Transportation applications also hold substantial importance, projected to grow from $0.44 billion to $0.82 billion, showcasing their significant role in roadbed stabilization and slope protection.

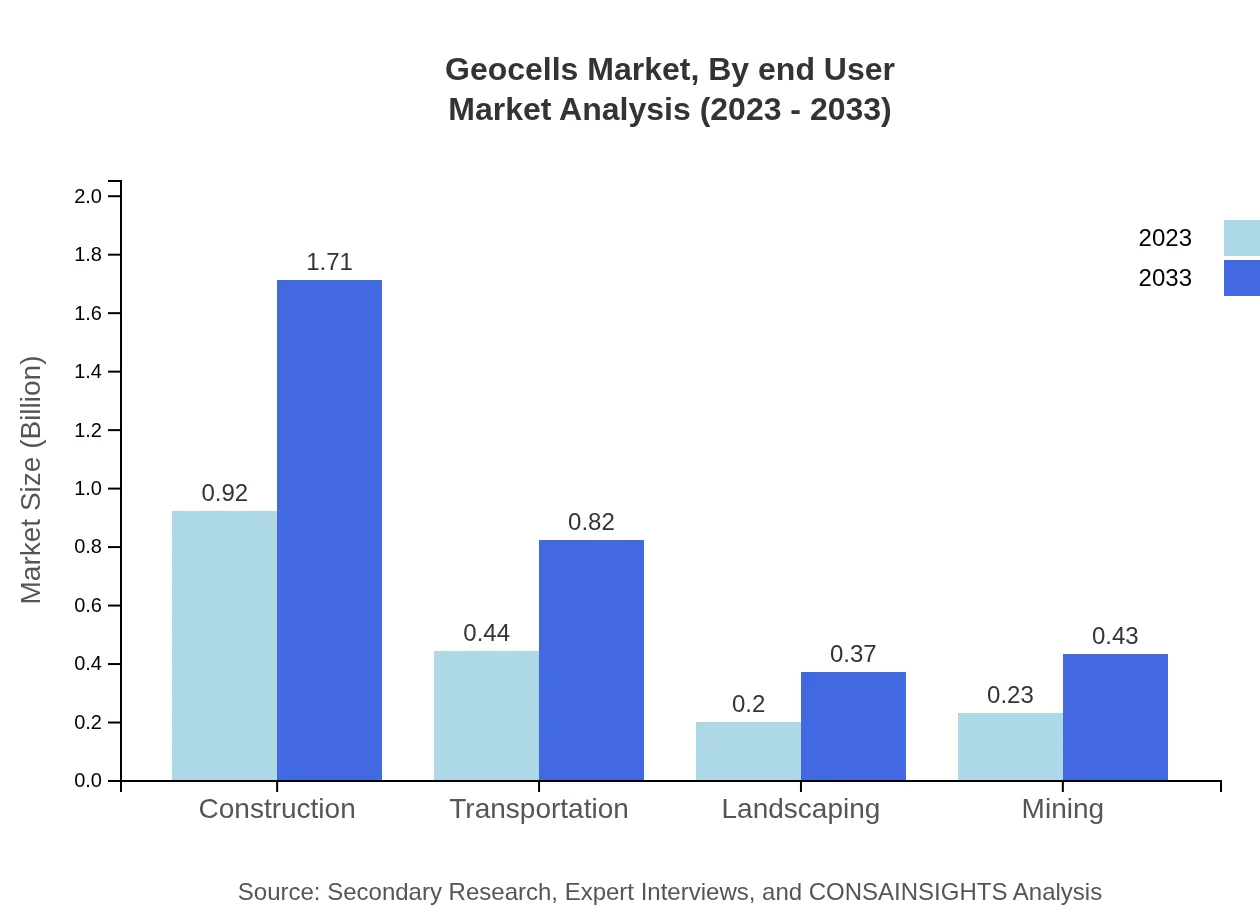

Geocells Market Analysis By End User

The end-user analysis reveals that civil engineering projects are the primary consumers of geocells, emphasizing durability and reliability. Additionally, landscaping and mining applications are rapidly gaining traction, particularly with the increasing necessity for soil stabilization and erosion control, marking growth opportunities in varied sectors.

Geocells Market Analysis By Region Type

The regional segmentation indicates North America as an emerging giant in the geocells market due to its significant infrastructure development projects. Europe follows closely, driven by environmental policies. The Asia Pacific region displays rapid growth potential with urbanization, while South America and Africa are also expanding, albeit at varying rates due to regional economic development.

Geocells Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Geocells Industry

Presto Geosystems:

A pioneer in products related to soil stabilization and erosion control, known for its innovation in geocell technologies.Geosynthetics Engineering:

Renowned for providing geocell solutions tailored to the specific needs of construction and civil engineering projects across various climates.Tensar Corporation:

A major player specializing in geosynthetic technology, contributing to the advancement of geocell applications in transportation and site development.ABG Geosynthetics:

Focused on sustainable geotechnical solutions, providing high-quality geocell products for construction and environmental projects.We're grateful to work with incredible clients.

FAQs

What is the market size of geocells?

The global geocells market is valued at approximately $1.8 billion in 2023, with a projected compound annual growth rate (CAGR) of 6.2% through 2033, highlighting strong growth potential in construction, transportation, and landscaping sectors.

What are the key market players or companies in the geocells industry?

Key players in the geocells market include companies like GeoProducts, Nilex, and Presto Geosystems, which lead in innovative solutions and production capabilities that meet the diverse needs of infrastructure and construction projects.

What are the primary factors driving the growth in the geocells industry?

Factors driving growth in the geocells industry include increased construction activity, a focus on sustainable practices, and the need for efficient soil stabilization solutions among various applications such as transportation and landscaping.

Which region is the fastest Growing in the geocells market?

Asia-Pacific is currently the fastest-growing region in the geocells market, with market size increasing from $0.37 billion in 2023 to $0.69 billion in 2033, driven by rapid urbanization and infrastructure development.

Does ConsaInsights provide customized market report data for the geocells industry?

Yes, ConsaInsights offers customized market report data tailored specifically for the geocells industry, accommodating various needs including regional analysis, competitive landscape, and growth forecasts.

What deliverables can I expect from this geocells market research project?

Expect comprehensive deliverables from the geocells market research project including detailed market analysis reports, segment insights, regional data breakdown, and strategic recommendations based on the latest trends.

What are the market trends of geocells?

Current trends in the geocells market include increased adoption of eco-friendly materials, advancements in technology for soil stabilization, and growing demand for geocells in landscaping and transportation applications.