Intumescent Coatings Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: intumescent-coatings

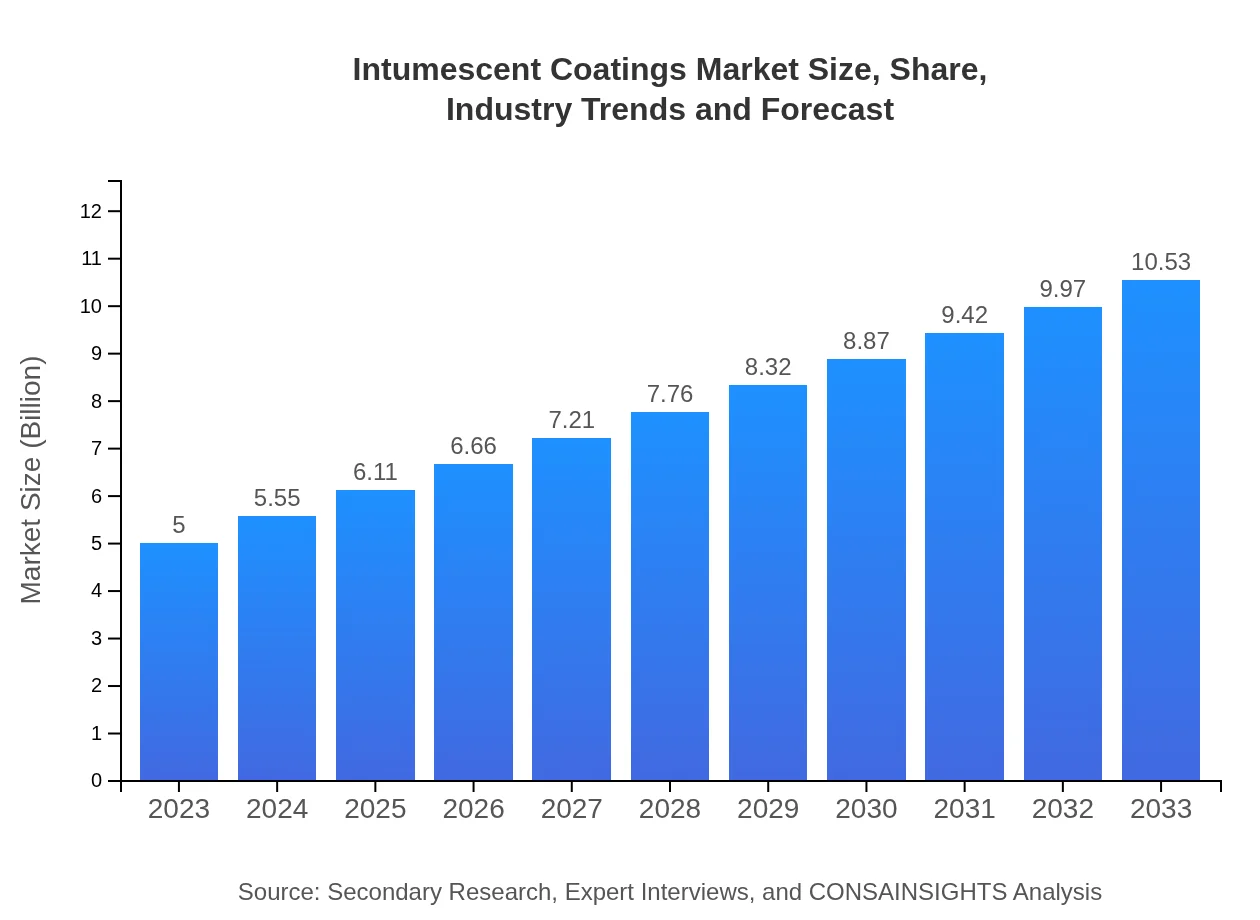

Intumescent Coatings Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides an in-depth analysis of the Intumescent Coatings market, offering insights on market size, growth trends, regional analysis, and future forecasts from 2023 to 2033.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | AkzoNobel N.V., Sherwin-Williams Company, BASF SE, Jotun Group |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Intumescent Coatings Market Overview

Customize Intumescent Coatings Market Report market research report

- ✔ Get in-depth analysis of Intumescent Coatings market size, growth, and forecasts.

- ✔ Understand Intumescent Coatings's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Intumescent Coatings

What is the Market Size & CAGR of Intumescent Coatings market in 2023?

Intumescent Coatings Industry Analysis

Intumescent Coatings Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Intumescent Coatings Market Analysis Report by Region

Europe Intumescent Coatings Market Report:

Europe is anticipated to grow from $1.43 billion in 2023 to $3.01 billion by 2033. The region’s rigorous fire safety regulations and the presence of major manufacturers enhance market growth opportunities, particularly in urban areas.Asia Pacific Intumescent Coatings Market Report:

In the Asia Pacific region, the Intumescent Coatings market is forecasted to grow from $1.08 billion in 2023 to $2.27 billion by 2033. Rapid urbanization, industrialization, and increasing investments in infrastructure development are driving this growth. Major economies like China and India are significant contributors.North America Intumescent Coatings Market Report:

In North America, the market is expected to expand from $1.71 billion in 2023 to $3.60 billion by 2033. The stringent fire codes, coupled with the substantial investment in infrastructure and commercial buildings, are key growth drivers in this region.South America Intumescent Coatings Market Report:

The South America market for Intumescent Coatings, albeit smaller, is predicted to grow from $0.09 billion in 2023 to $0.19 billion by 2033. The growth is attributed to rising construction activities and increasing awareness regarding fire safety standards.Middle East & Africa Intumescent Coatings Market Report:

The Middle East and Africa market will likely see growth from $0.69 billion in 2023 to $1.46 billion by 2033, primarily driven by infrastructural developments and increasing awareness of fire safety regulations in construction projects.Tell us your focus area and get a customized research report.

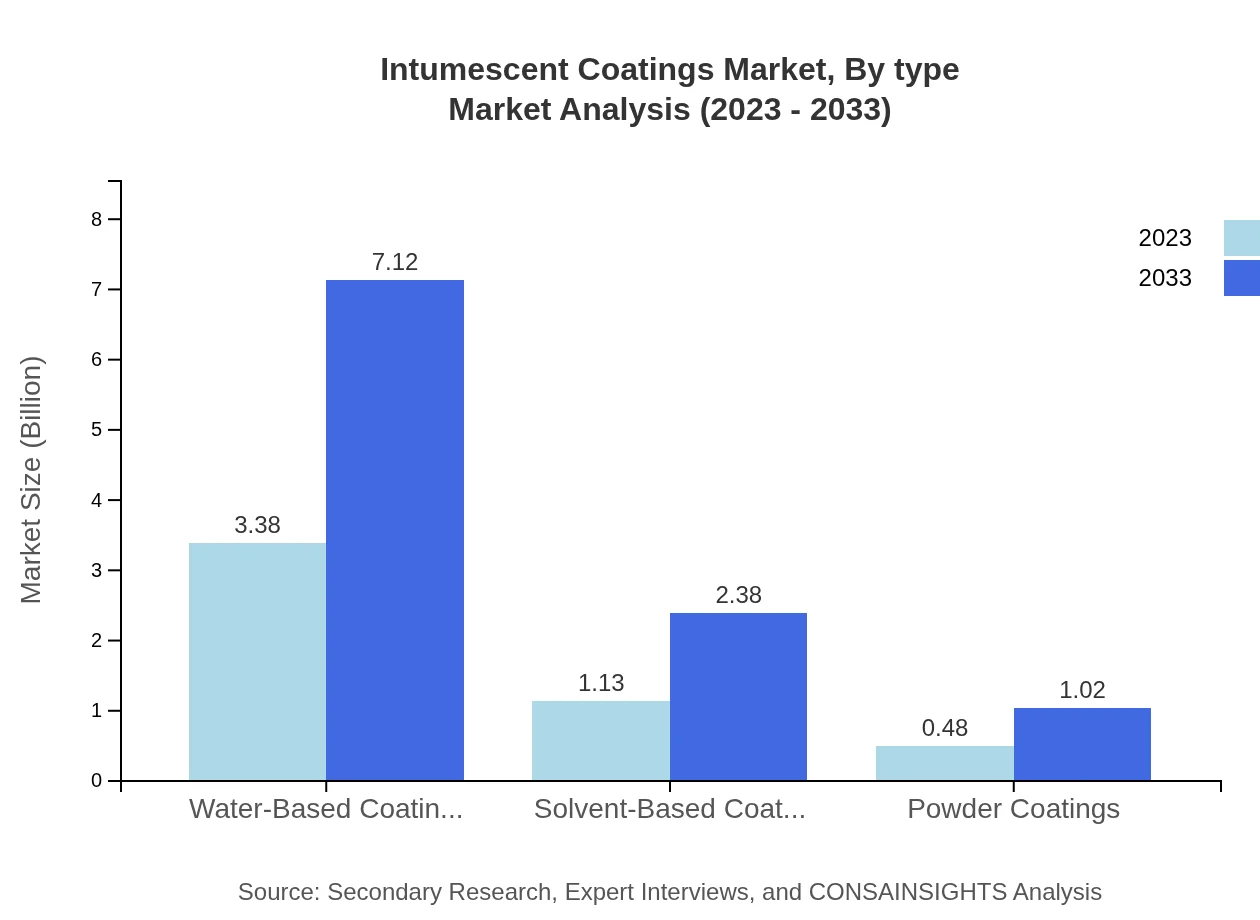

Intumescent Coatings Market Analysis By Type

Water-Based Coatings dominate the market with a significant size increase from $3.38 billion in 2023 to $7.12 billion by 2033, holding a 67.65% market share. In contrast, Solvent-Based Coatings are projected to increase from $1.13 billion in 2023 to $2.38 billion by 2033, maintaining a 22.65% market share. Powder Coatings are forecasted to grow from $0.48 billion to $1.02 billion, accounting for 9.7% of the market by 2033.

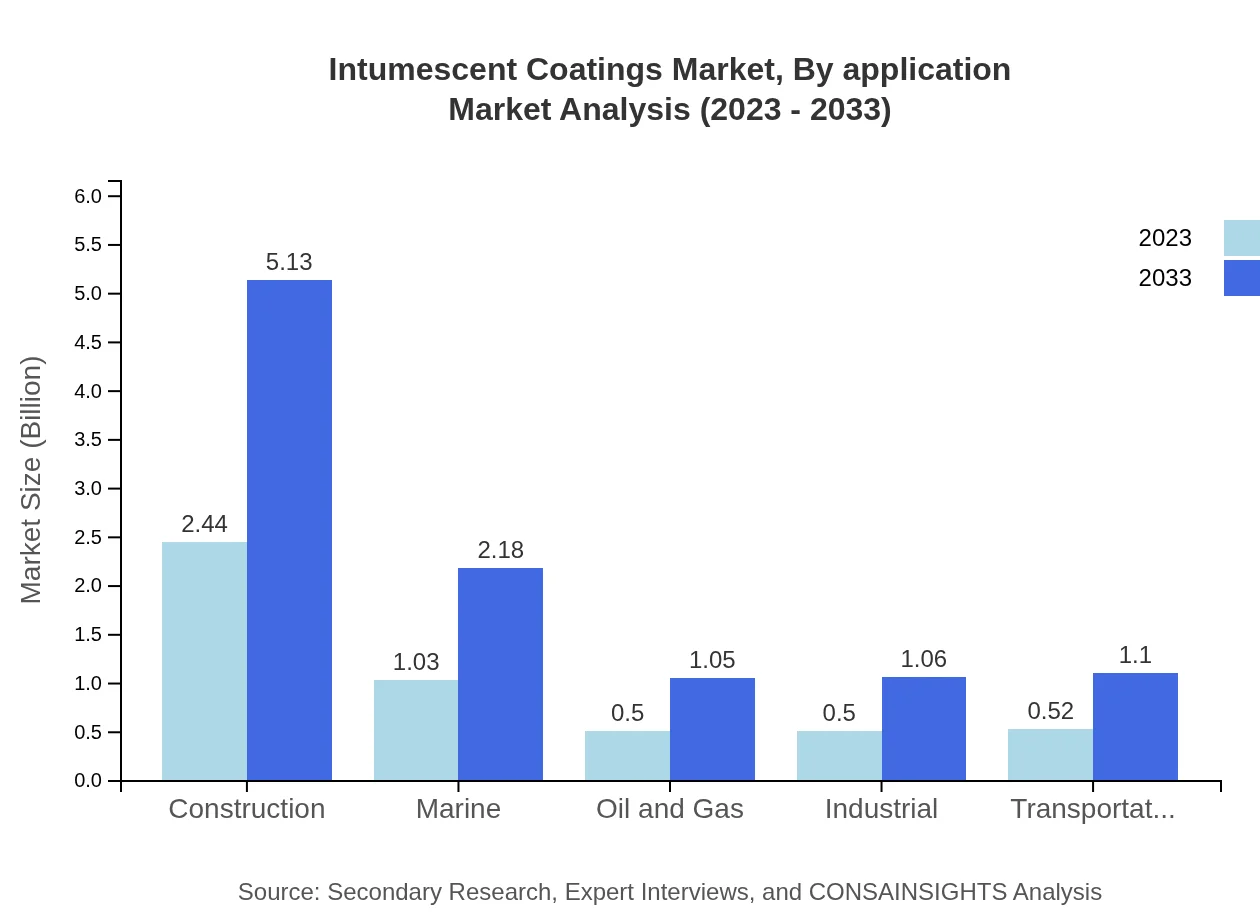

Intumescent Coatings Market Analysis By Application

The construction segment is significant, expected to grow from $2.44 billion in 2023 to $5.13 billion, holding 48.72% of the market share. Marine applications are also notable, expanding from $1.03 billion to $2.18 billion. Oil and gas applications and industrial sectors are expected to increase moderately, reflecting stable growth trends.

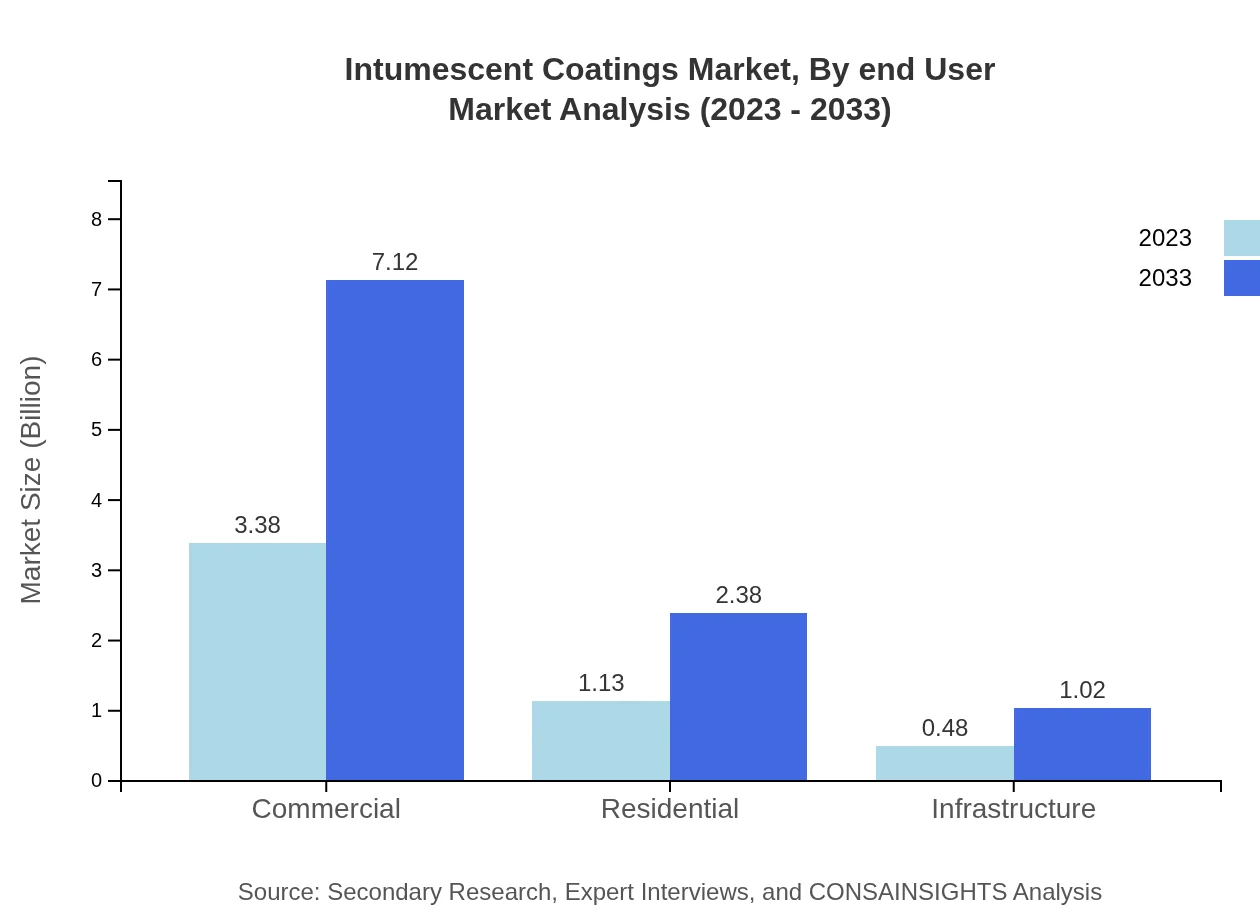

Intumescent Coatings Market Analysis By End User

Commercial and residential segments are pivotal in the end-user analysis. In 2023, commercial use is projected to dominate at $3.38 billion and is expected to grow to $7.12 billion by 2033. In comparison, residential usage will grow from $1.13 billion to $2.38 billion. Emerging sectors in infrastructure are also essential for future growth.

Intumescent Coatings Market Analysis By Region

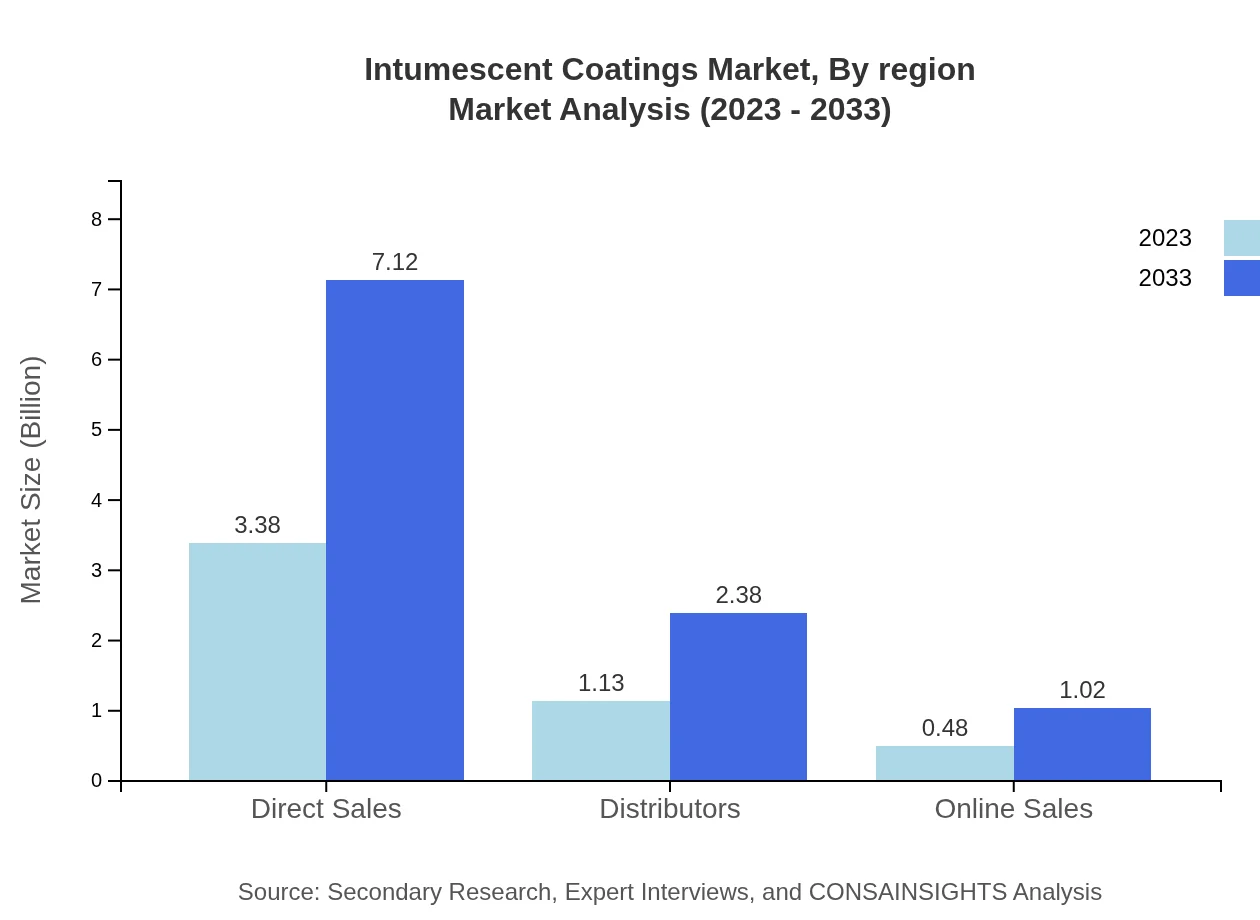

Distribution channels are crucial for market success. Direct sales dominate with $3.38 billion projected in 2023 growing to $7.12 billion by 2033. Distributor channels are expected to rise from $1.13 billion to $2.38 billion, while online sales will likely grow from $0.48 billion to $1.02 billion, reflecting the digital shift in sales.

Intumescent Coatings Market Analysis By Technology

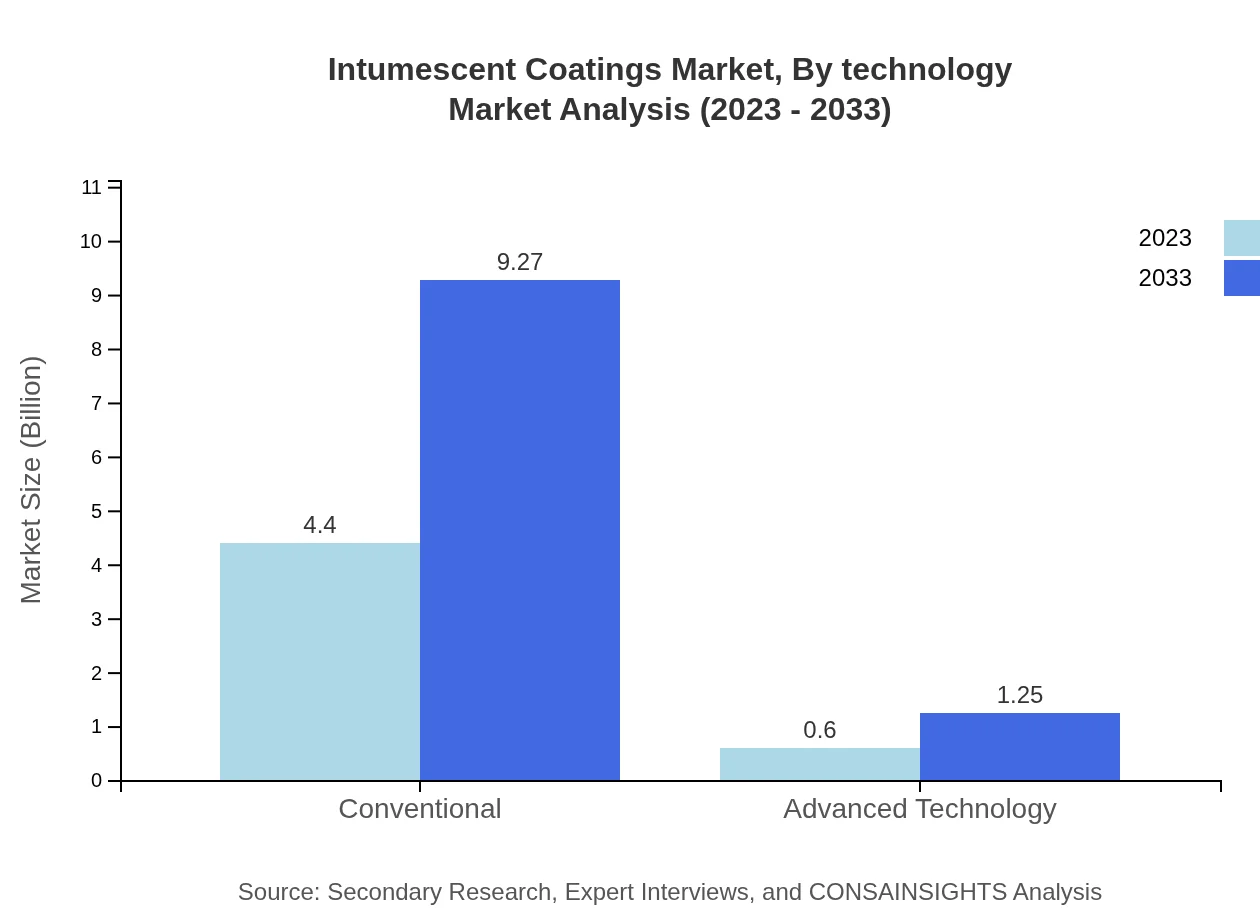

The market analysis by technology will focus on Conventional and Advanced Technology coatings. Conventional coatings hold a significant share with sizes projected to rise from $4.40 billion to $9.27 billion by 2033, while Advanced Technology coatings are expected to grow from $0.60 billion to $1.25 billion, affirming innovative trends.

Intumescent Coatings Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Intumescent Coatings Industry

AkzoNobel N.V.:

A leading global producer of paints and coatings, AkzoNobel provides a wide range of innovative intumescent coating solutions known for their fireproofing capabilities.Sherwin-Williams Company:

Sherwin-Williams is a major player in protective coatings, offering high-quality intumescent coatings for industrial and commercial applications.BASF SE:

BASF is one of the world’s largest chemical producers, known for its advanced formulation technologies in intumescent coatings that enhance safety and environmental sustainability.Jotun Group:

The Jotun Group specializes in decorative paints and performance coatings, providing intumescent coatings that meet stringent industry standards across various sectors.We're grateful to work with incredible clients.

FAQs

What is the market size of intumescent coatings?

The global intumescent coatings market is valued at approximately $5 billion in 2023 and is projected to grow with a CAGR of 7.5%, reaching a considerably larger market size by 2033.

What are the key market players or companies in the intumescent coatings industry?

Key players in the intumescent coatings industry include Sherwin-Williams, AkzoNobel, Jotun, RPM International, and Hempel, all of which are recognized for their innovative product offerings and significant market presence.

What are the primary factors driving the growth in the intumescent coatings industry?

The growth of the intumescent coatings industry is driven by increasing regulations for fire safety, rising construction activities, advancements in coating technologies, and growing awareness of fire-resistant materials among consumers.

Which region is the fastest Growing in the intumescent coatings market?

The Asia-Pacific region is projected to be the fastest-growing market for intumescent coatings from 2023 to 2033, expanding from a market size of $1.08 billion to $2.27 billion, fueled by rapid urbanization and industrialization.

Does ConsaInsights provide customized market report data for the intumescent coatings industry?

Yes, ConsaInsights offers customized market report data tailored to specific needs in the intumescent coatings industry, including in-depth analyses and sector-specific insights to help businesses make informed decisions.

What deliverables can I expect from this intumescent coatings market research project?

Deliverables from the intumescent coatings market research project include comprehensive reports, market segmentation analysis, trend forecasting, competitive landscape evaluations, and actionable insights actionable for strategic planning.

What are the market trends of intumescent coatings?

Current trends in the intumescent coatings market include the increasing demand for water-based coatings, technological advancements in fire protection, and a shift towards sustainable and eco-friendly materials, all shaping the industry's future directions.