High Temperature Fiber Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: high-temperature-fiber

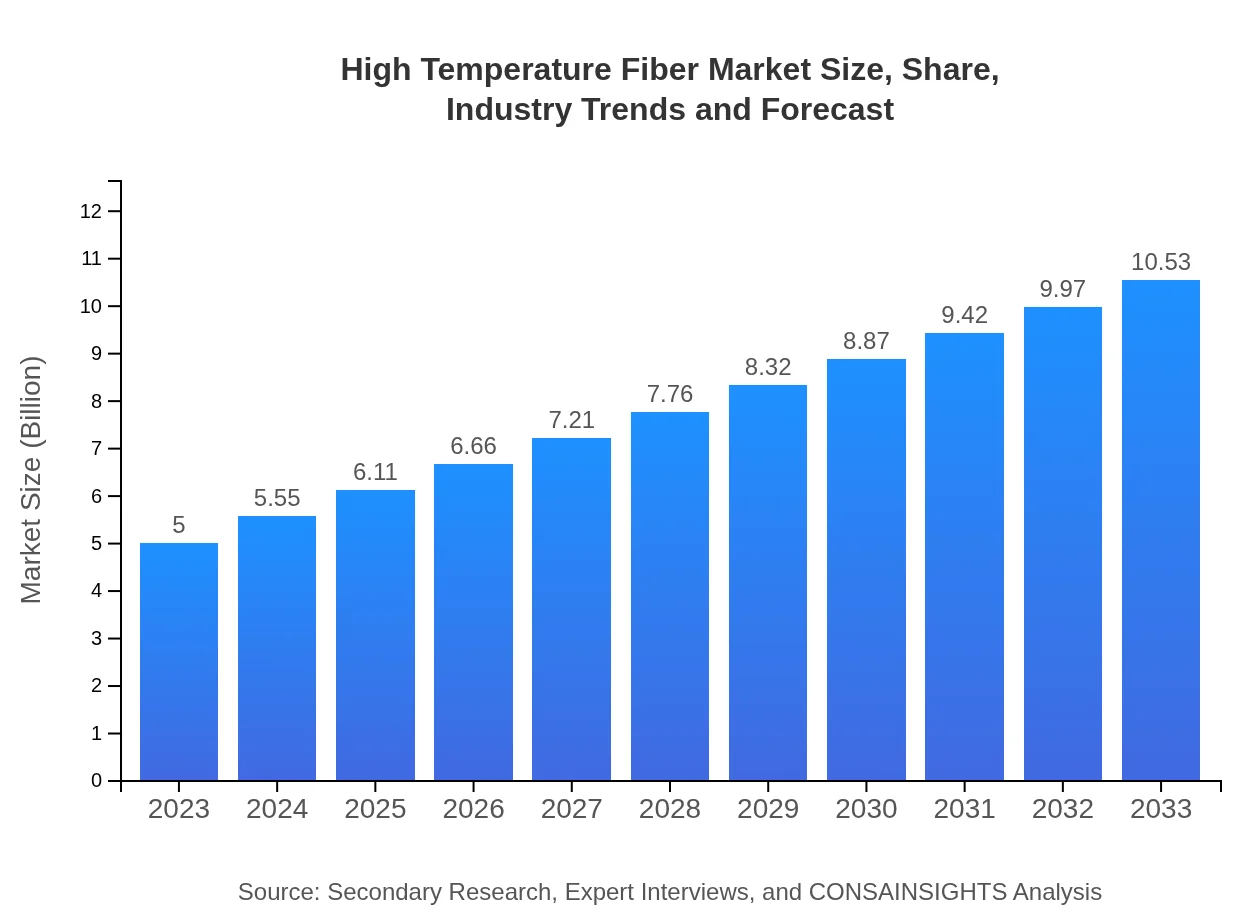

High Temperature Fiber Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides a comprehensive analysis of the High Temperature Fiber market, examining trends, market size, and growth forecasts from 2023 to 2033. Insights include segmentation, regional dynamics, industry leaders, and technology advancements influencing the market.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | DuPont, Teijin Limited, TenCate, Honeywell |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

High Temperature Fiber Market Overview

Customize High Temperature Fiber Market Report market research report

- ✔ Get in-depth analysis of High Temperature Fiber market size, growth, and forecasts.

- ✔ Understand High Temperature Fiber's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in High Temperature Fiber

What is the Market Size & CAGR of High Temperature Fiber market in 2023?

High Temperature Fiber Industry Analysis

High Temperature Fiber Market Segmentation and Scope

Tell us your focus area and get a customized research report.

High Temperature Fiber Market Analysis Report by Region

Europe High Temperature Fiber Market Report:

The European High Temperature Fiber market is projected to grow from $1.23 billion in 2023 to $2.58 billion by 2033. The region’s regulatory compliance on material safety and sustainability practices fuels demand for advanced fibers across various applications.Asia Pacific High Temperature Fiber Market Report:

The Asia Pacific region is anticipated to witness significant growth, with a market size of $1.00 billion in 2023, projected to reach $2.10 billion by 2033. Key factors include increased industrial activity, particularly in manufacturing and automotive sectors, driving demand for high temperature fibers.North America High Temperature Fiber Market Report:

North America holds a significant portion of the market, with an estimated value of $1.91 billion in 2023, expected to grow to approximately $4.01 billion by 2033. The region benefits from robust aerospace and defense industries that utilize high temperature fibers for safety applications.South America High Temperature Fiber Market Report:

In South America, the High Temperature Fiber market is expected to expand from $0.21 billion in 2023 to $0.45 billion by 2033. This growth is attributed to the region's increasing focus on industrial safety and technological incorporation in the extraction and production sectors.Middle East & Africa High Temperature Fiber Market Report:

The market in the Middle East and Africa is set to grow from $0.66 billion in 2023 to $1.38 billion by 2033, driven by advancements in oil and gas exploration and increasing adoption of high temperature resistant materials in construction and defense.Tell us your focus area and get a customized research report.

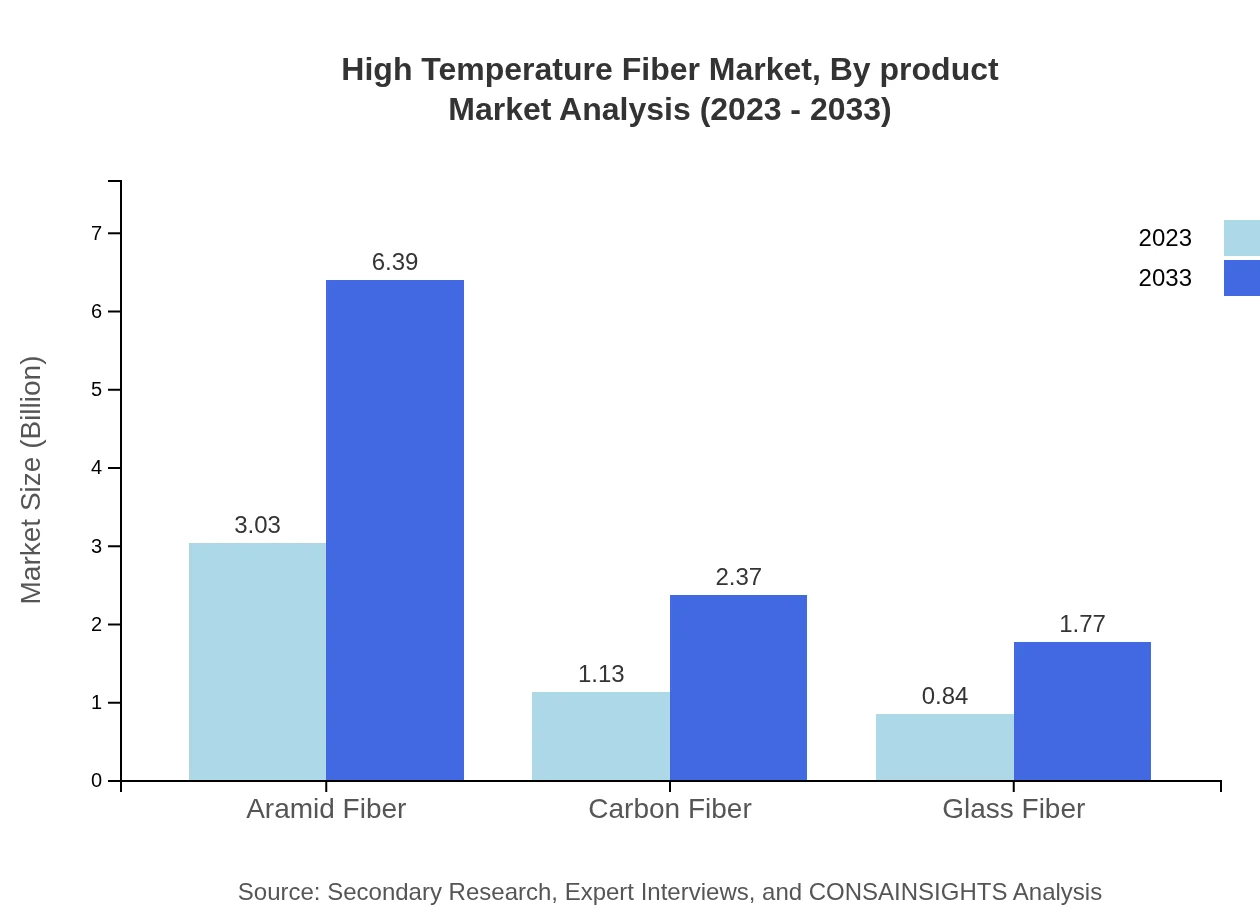

High Temperature Fiber Market Analysis By Product

The High Temperature Fiber market is predominantly driven by woven fabrics, which accounted for a market size of $3.03 billion in 2023, expected to grow to $6.39 billion by 2033. Non-woven fabrics follow, starting at $1.13 billion and predicted to expand to $2.37 billion. Composite materials represent a smaller share but are emerging as crucial components in lightweight applications, with growth from $0.84 billion to $1.77 billion during the same period.

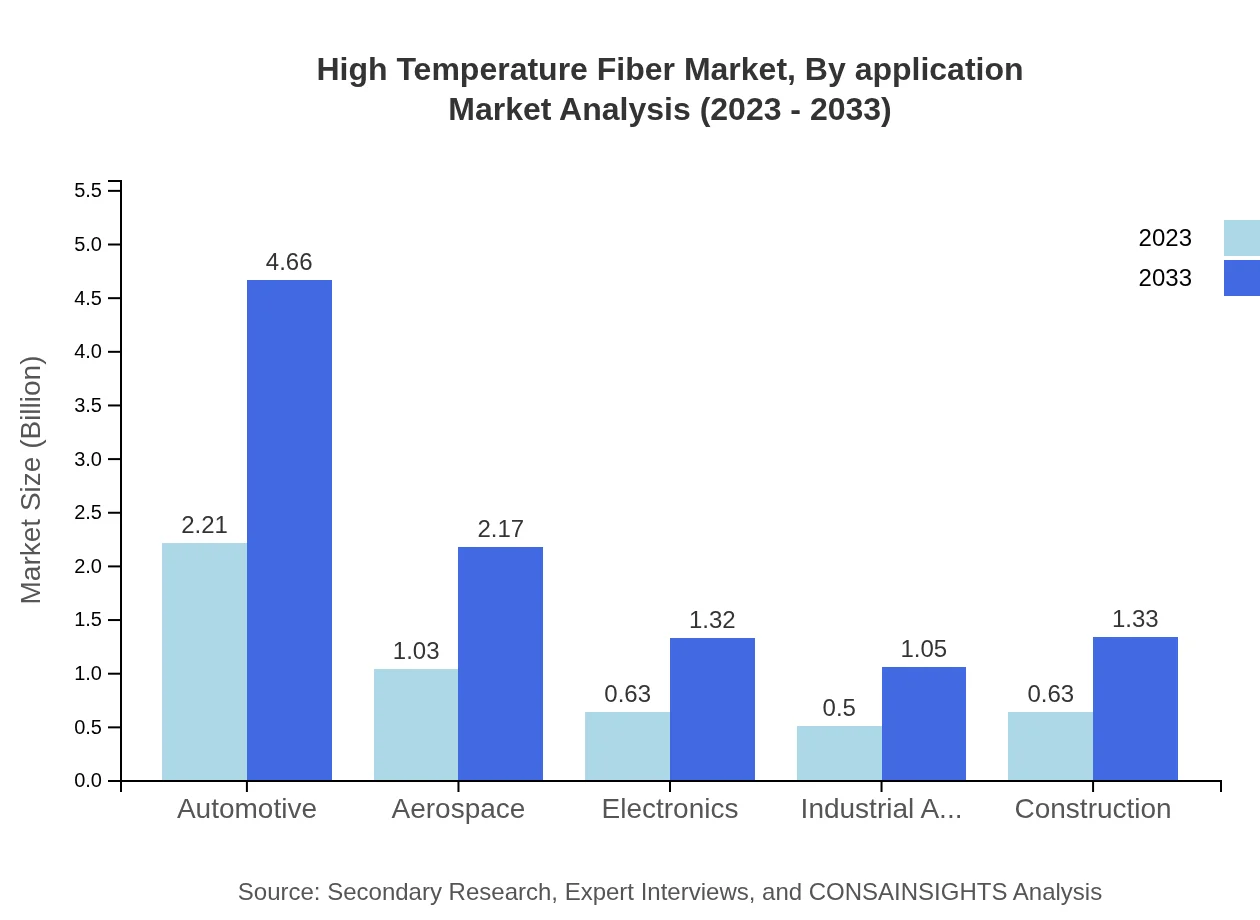

High Temperature Fiber Market Analysis By Application

The automotive sector remains a leading application area, expected to grow from $2.21 billion in 2023 to $4.66 billion by 2033, while the aerospace sector will increase from $1.03 billion to $2.17 billion, highlighting the trend of incorporating advanced materials in high-demand environments.

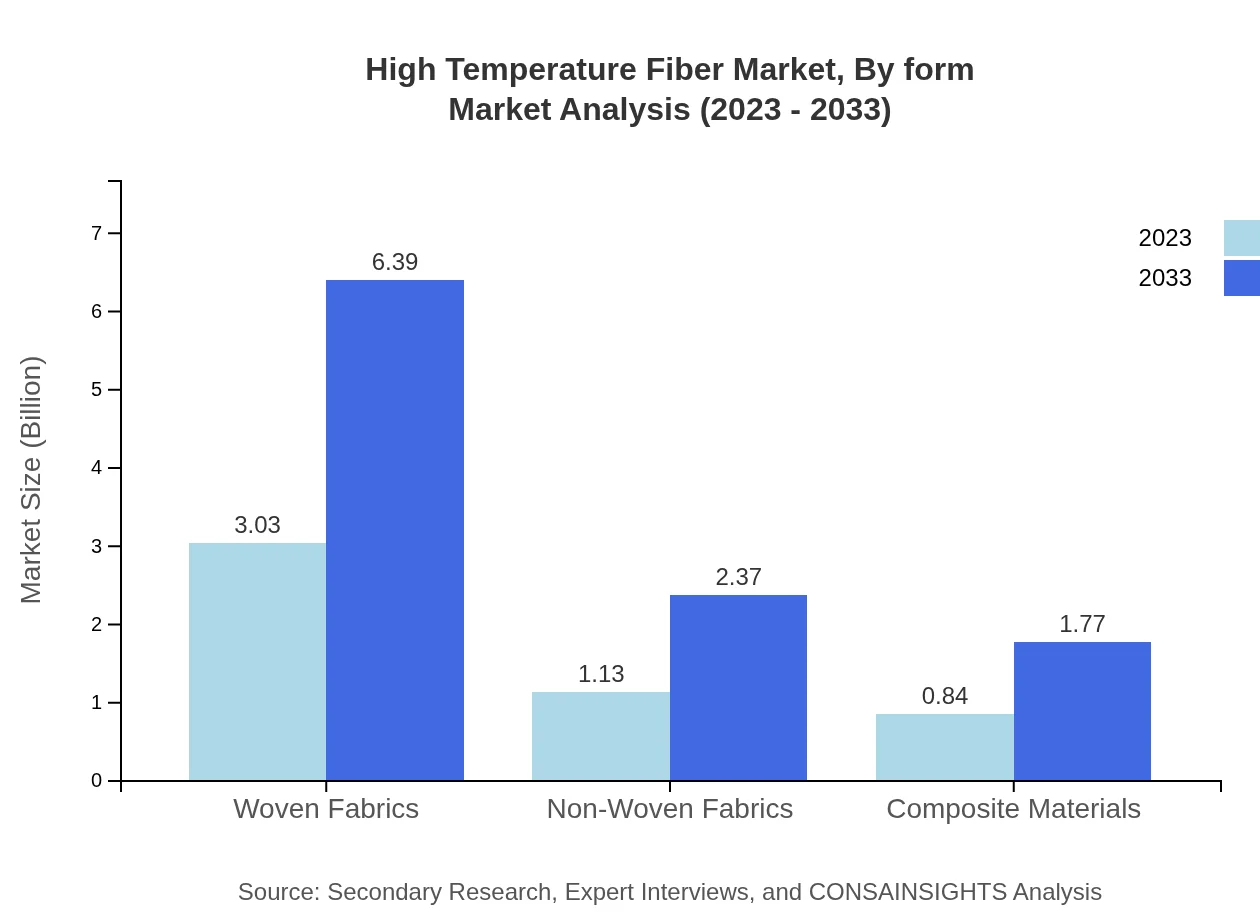

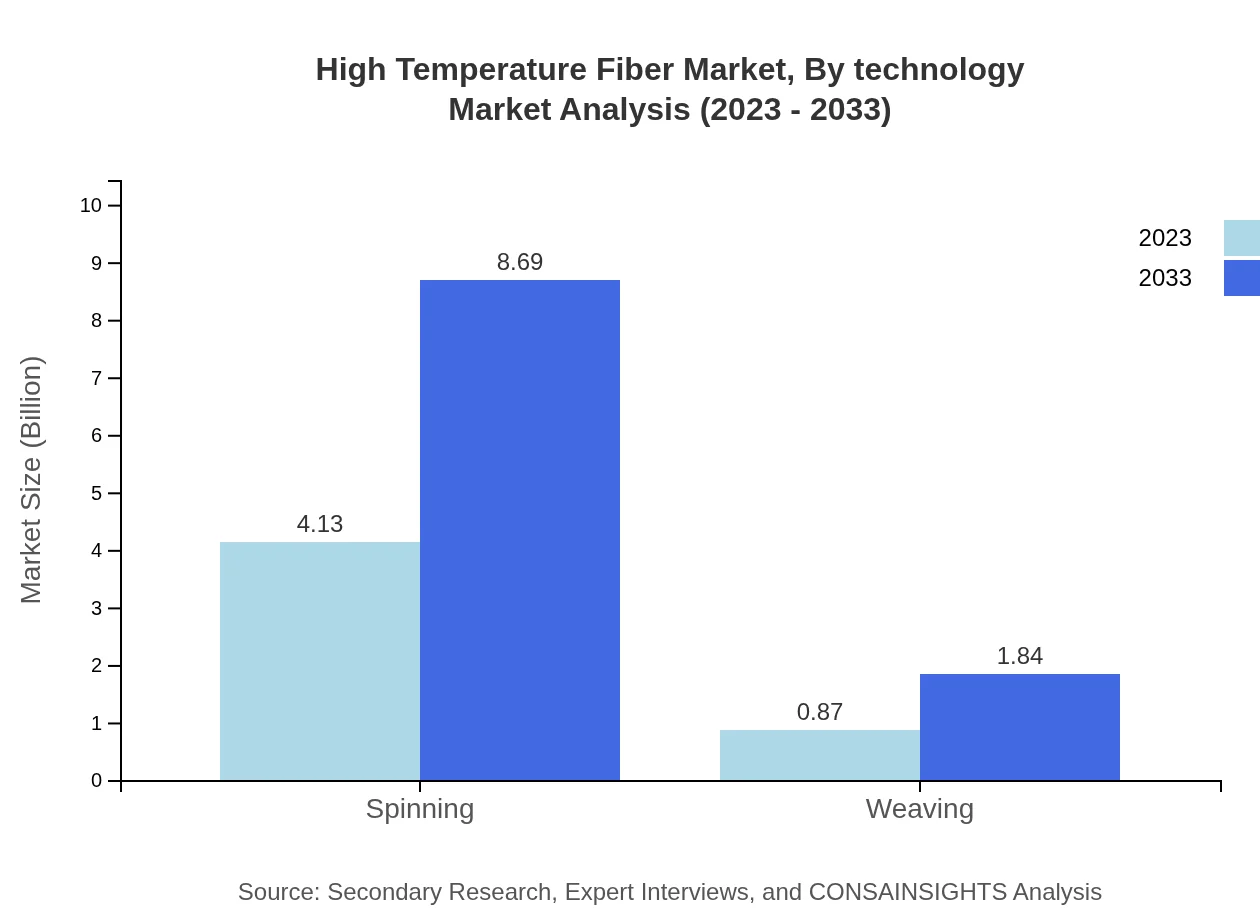

High Temperature Fiber Market Analysis By Form

Spinning processes currently dominate the market with a share of 82.52% and are projected to grow, while weaving, although smaller, shows promise with applications in specialized areas. Expectations for spin-off technologies in processing are driving innovation.

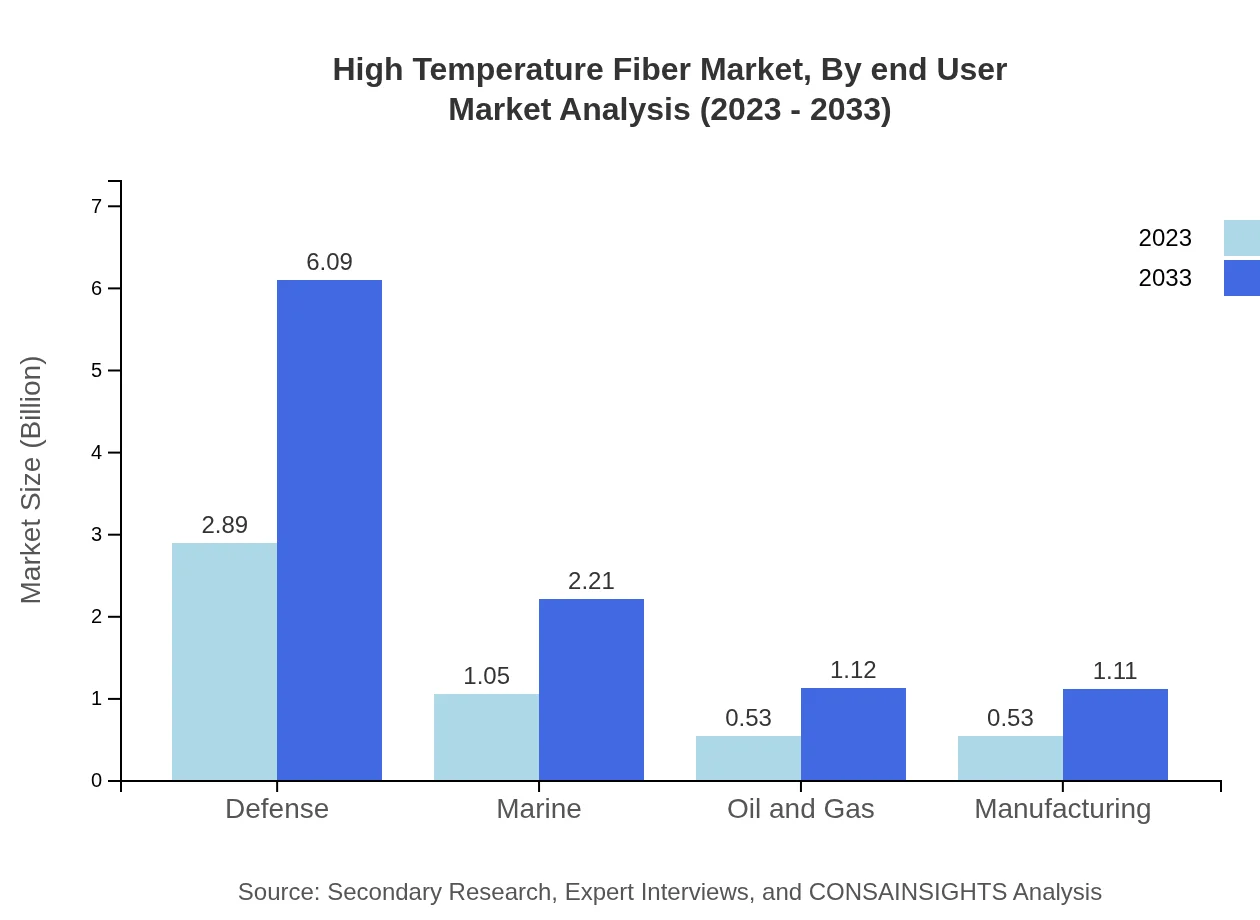

High Temperature Fiber Market Analysis By End User

Defense remains the largest segment with a share of 57.85%, increasing demand for protective clothing and equipment. The marine, oil and gas, and manufacturing sectors are also critical, reflecting a diversified application across industrial contexts.

High Temperature Fiber Market Analysis By Technology

Technological innovation plays a pivotal role in market dynamics, with advancements in fiber manufacturing techniques yielding enhanced thermal resistance and lightweight properties. Innovations in fiber treatments and coatings continue to expand applications in existing and emerging markets.

High Temperature Fiber Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in High Temperature Fiber Industry

DuPont:

DuPont is a pioneer in high temperature fiber technology, particularly known for its Nomex brand, widely used in personal protective equipment and industrial applications.Teijin Limited:

Teijin is known for its aramid fibers, particularly Twaron and Technora, utilized in various applications ranging from automotive to aerospace, emphasizing safety and heat resistance.TenCate:

TenCate is engaged in advanced textile solutions and is known for producing heat and flame-resistant fabrics used in military and firefighting applications.Honeywell :

Honeywell develops innovative materials in the heat-resistant fibers segment, including their Spectra product line, which showcases strength and thermal resistance.We're grateful to work with incredible clients.

FAQs

What is the market size of high Temperature Fiber?

The global high-temperature fiber market is projected to reach $5 billion by 2033, growing at a CAGR of 7.5% from its current valuation. This growth reflects the increasing demand for advanced materials in various industries.

What are the key market players or companies in the high Temperature Fiber industry?

Key players in the high-temperature fiber market include renowned manufacturers and innovators in material science. These companies are pivotal in advancing fiber technology and include leaders known for sustainable and high-performance solutions.

What are the primary factors driving the growth in the high Temperature Fiber industry?

Factors driving growth in the high-temperature fiber industry include rising demand for lightweight materials, advancements in manufacturing technologies, and increased applications in aerospace and automotive sectors, driving innovation and expanding markets.

Which region is the fastest Growing in the high Temperature Fiber market?

North America is the fastest-growing region in the high-temperature fiber market, projected to increase from $1.91 billion in 2023 to $4.01 billion by 2033, owing to strong industrial applications and technological advancements.

Does ConsaInsights provide customized market report data for the high Temperature Fiber industry?

Yes, ConsaInsights offers customized market report data tailored to specific client needs in the high-temperature fiber industry, allowing stakeholders to gain insights that suit their business strategies and operational requirements.

What deliverables can I expect from this high Temperature Fiber market research project?

Deliverables from the high-temperature fiber market research project include comprehensive data analysis, market forecasts, competitive landscape assessments, and actionable insights, designed to support strategic decision-making.

What are the market trends of high Temperature Fiber?

Current trends in the high-temperature fiber market include increasing usage in aerospace and defense, growth in emerging economies, and innovation in fiber technology, driving enhanced performance and sustainability metrics across various applications.