Agricultural Robots Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: agricultural-robots

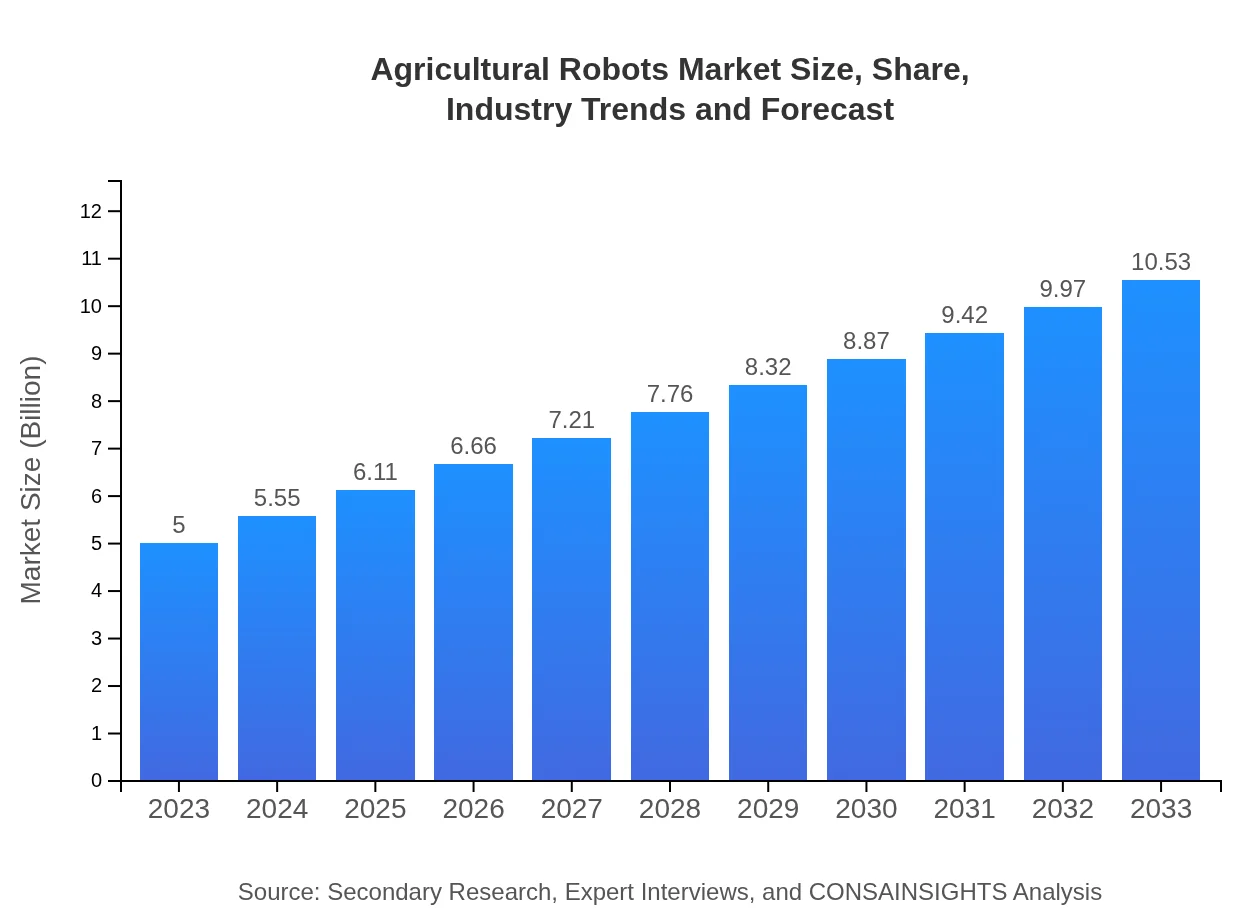

Agricultural Robots Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides an in-depth analysis of the Agricultural Robots market, including insights into market size, growth trends, regional performance, technologies, and forecasts for 2023 to 2033.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | John Deere, Trimble Inc., AG Leader Technology, Intuitive Surgical |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Agricultural Robots Market Overview

Customize Agricultural Robots Market Report market research report

- ✔ Get in-depth analysis of Agricultural Robots market size, growth, and forecasts.

- ✔ Understand Agricultural Robots's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Agricultural Robots

What is the Market Size & CAGR of Agricultural Robots market in 2033?

Agricultural Robots Industry Analysis

Agricultural Robots Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Agricultural Robots Market Analysis Report by Region

Europe Agricultural Robots Market Report:

The European market for Agricultural Robots is set to see growth from $1.41 billion in 2023 to $2.97 billion by 2033. This growth is fostered by stringent regulations on sustainable farming practices and increasing investment in agricultural innovations among European countries.Asia Pacific Agricultural Robots Market Report:

Asia-Pacific is anticipated to be a key region for the Agricultural Robots market, with a market size of $1.10 billion in 2023 projected to increase to $2.31 billion by 2033. The growth is driven by increasing investments in agricultural technology, government support for modern farming practices, and the significant expansion of the agricultural sector in countries like China and India.North America Agricultural Robots Market Report:

North America occupies a significant share of the Agricultural Robots market, with a market value of $1.68 billion in 2023 anticipated to rise to $3.53 billion by 2033. The strong emphasis on technological advancements and high adoption rates of automation practices in the U.S. contribute to this market's expansion.South America Agricultural Robots Market Report:

The South American market for Agricultural Robots is expected to grow from $0.32 billion in 2023 to $0.67 billion by 2033. The booming agricultural sector across Brazil and Argentina, along with rising farm mechanization, are key growth drivers in this region.Middle East & Africa Agricultural Robots Market Report:

The Middle East and Africa region's Agricultural Robots market, valued at $0.50 billion in 2023, is expected to grow to $1.04 billion by 2033. Factors such as improving agricultural practices and increasing investments in food security play crucial roles in this growth.Tell us your focus area and get a customized research report.

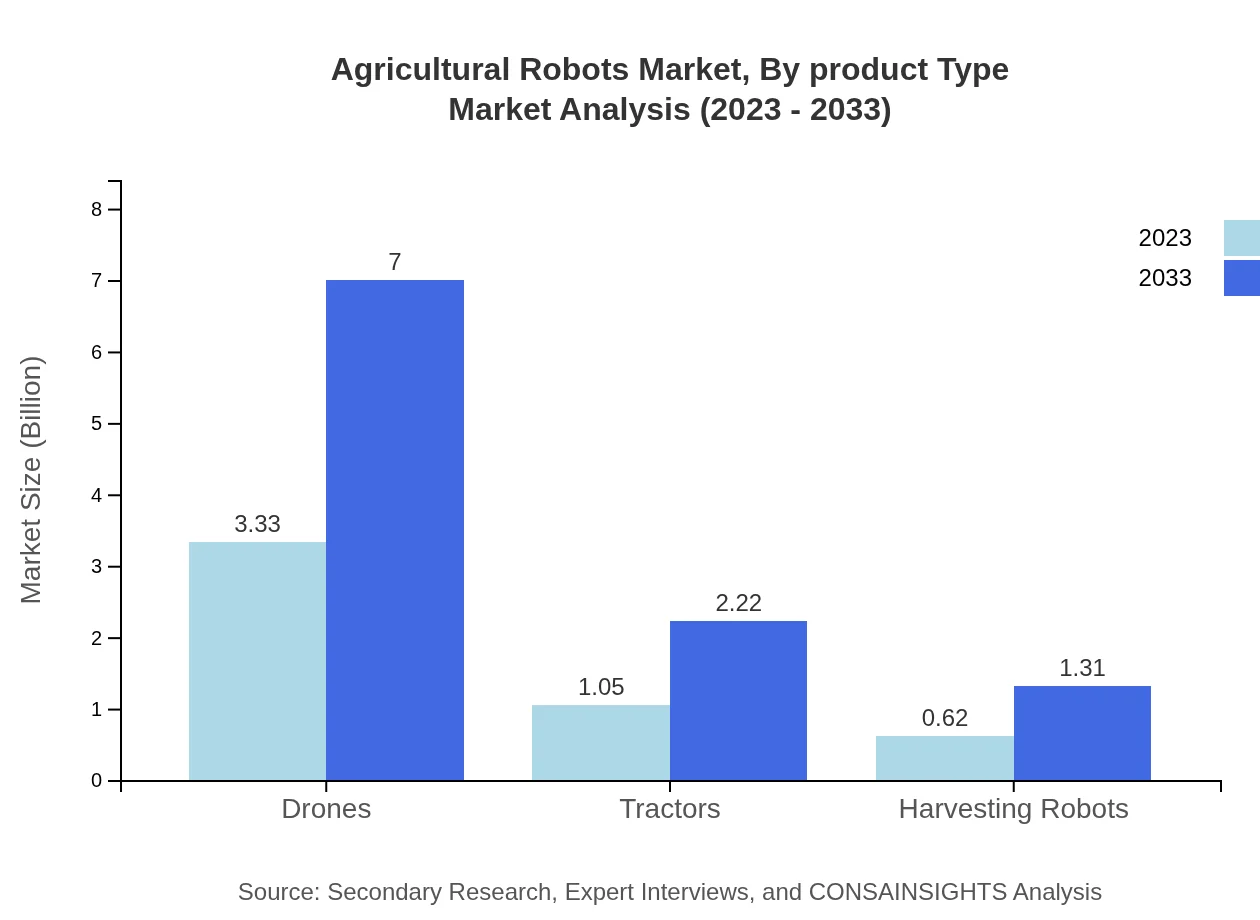

Agricultural Robots Market Analysis By Product Type

The Agricultural Robots market is dominated by various product types such as tractors, drones, harvesting robots, and autonomous robots. These products play a significant role in enhancing productivity and operational efficiency. For instance, the market size for drones is anticipated to reach $3.33 billion by 2033 from $1.68 billion in 2023, showing a strong inclination towards aerial solutions in agriculture. Each technology contributes uniquely to agricultural efforts, be it crop management or livestock operations.

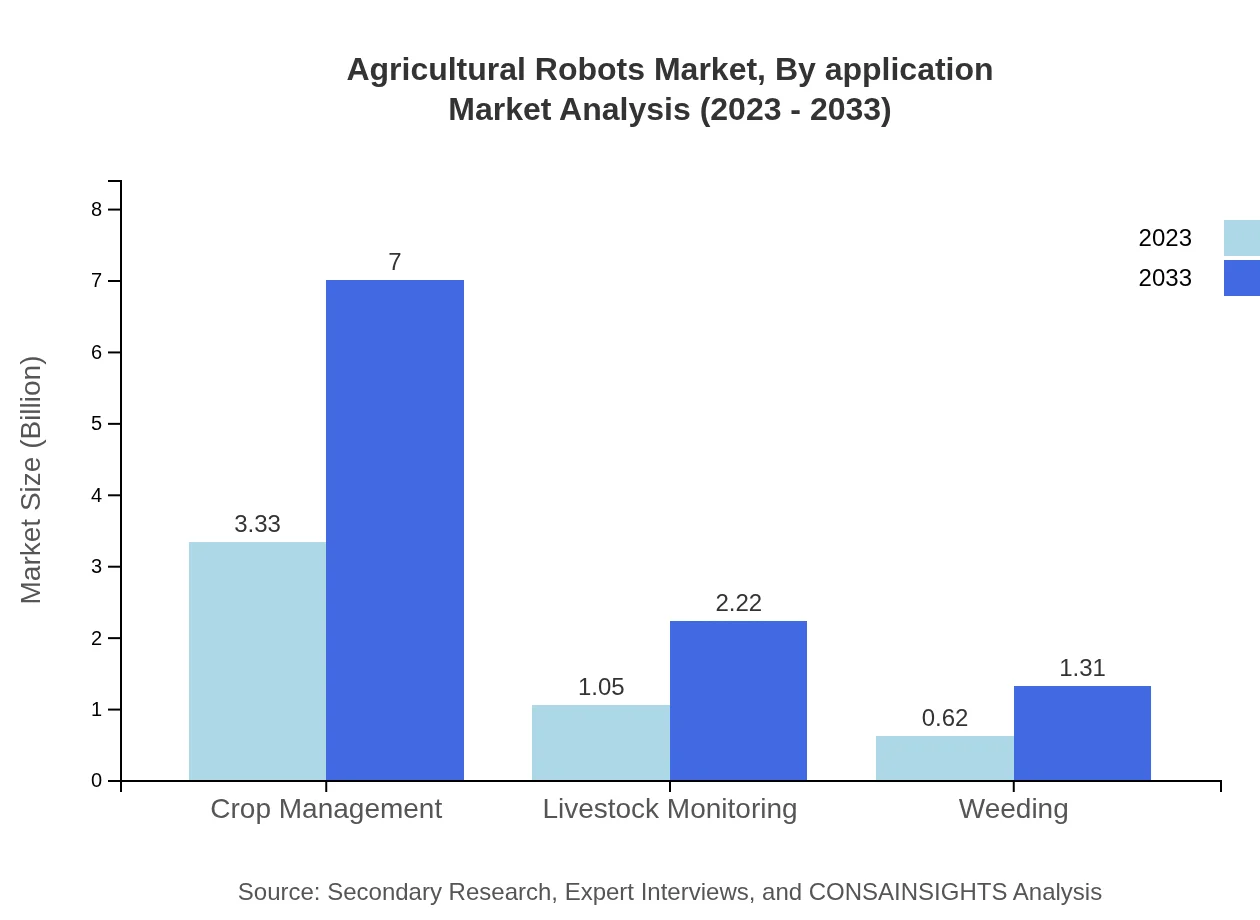

Agricultural Robots Market Analysis By Application

In terms of application, the Agricultural Robots market is heavily influenced by crop management and livestock monitoring, which together are expected to account for a significant share of the market. The market size for crop management applications is expected to grow proportionately from $3.33 billion in 2023 to about $7.00 billion by 2033, as more farmers adopt technologies for precision agriculture.

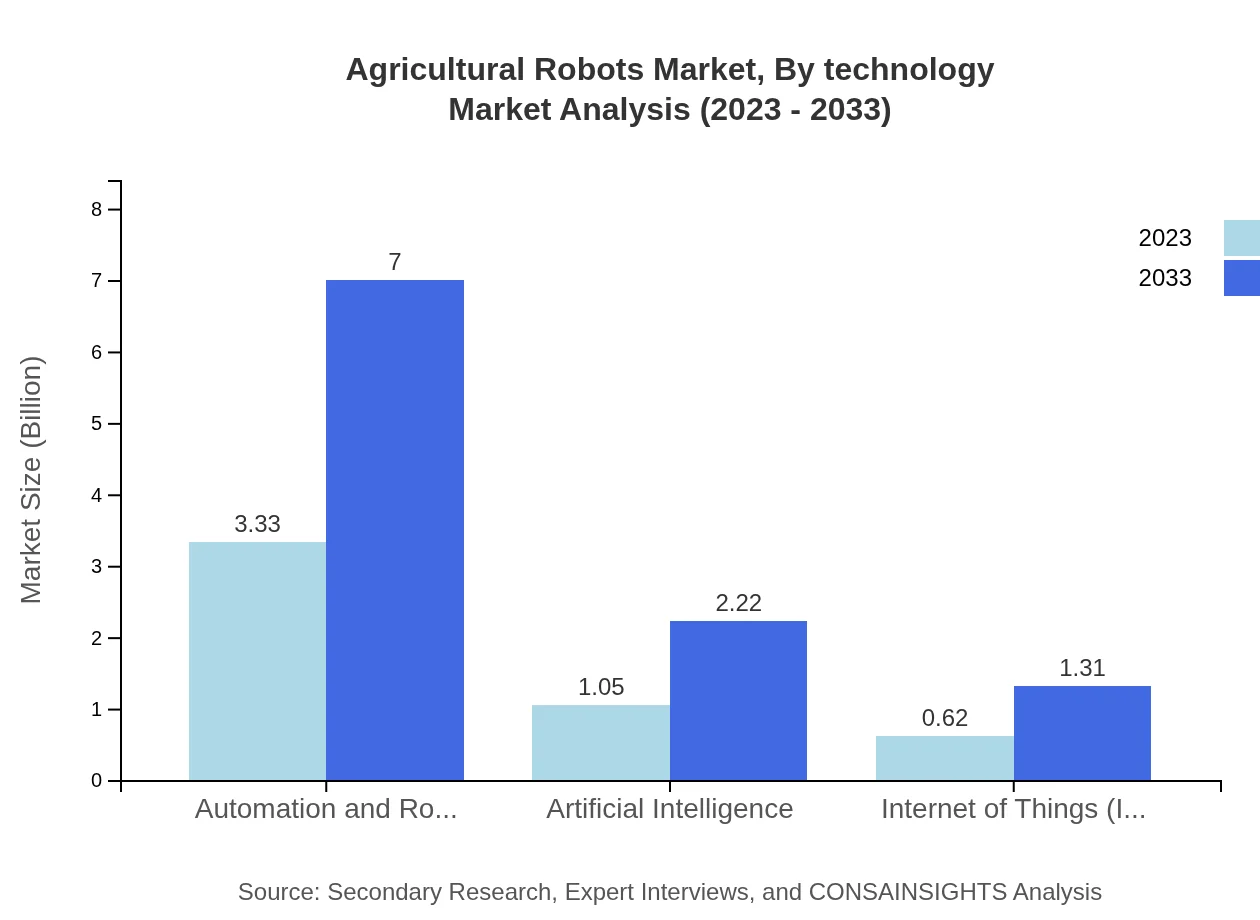

Agricultural Robots Market Analysis By Technology

The segment dedicated to technology highlights the importance of innovations such as AI, IoT, and robotics in transforming agricultural practices. AI-enabled robots are expected to dominate, significantly influencing the productivity of farms and yielding better crop results with minimal resources. The market for AI technologies in agriculture is expected to grow from $1.05 billion in 2023 to $2.22 billion by 2033.

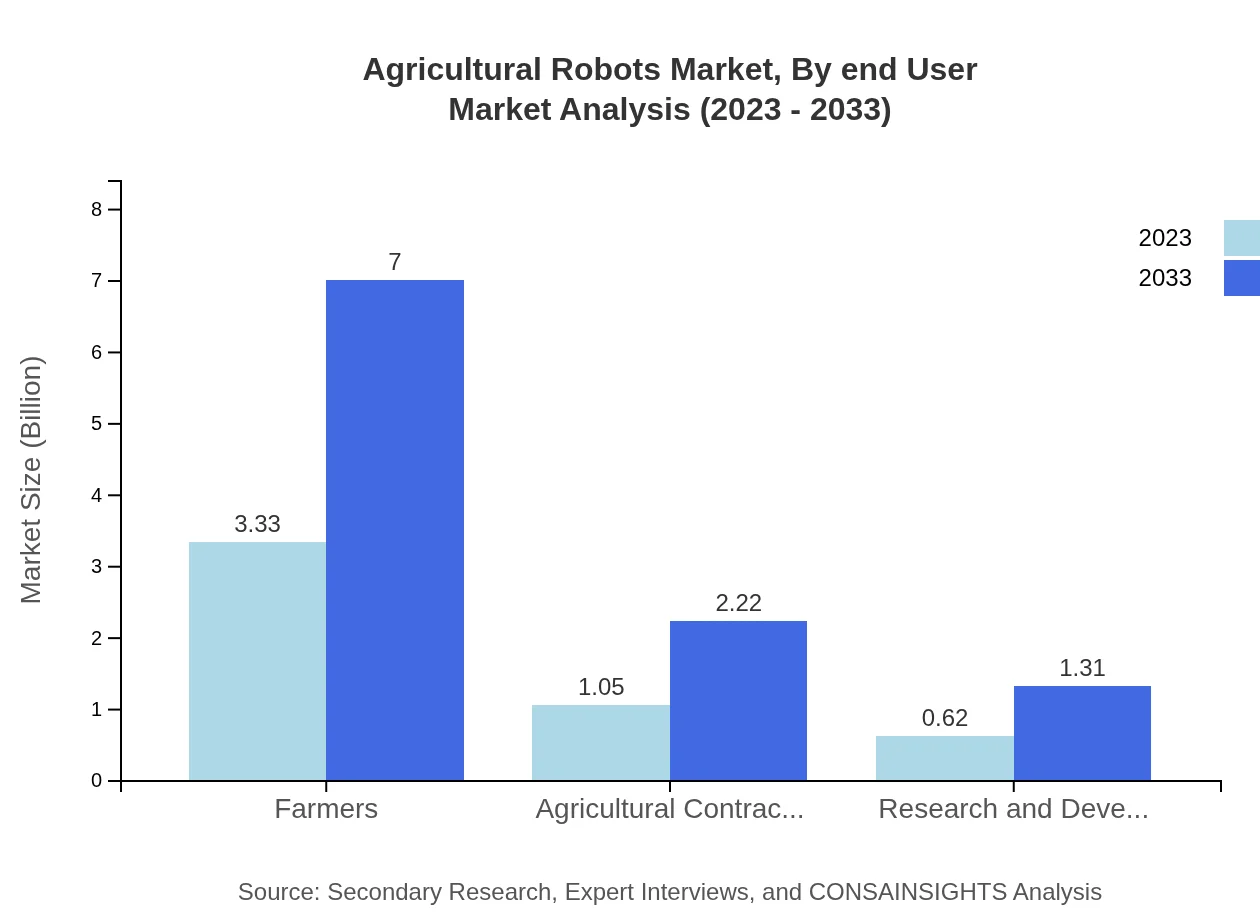

Agricultural Robots Market Analysis By End User

Farmers continue to be the largest end-user segment in the Agricultural Robots market, with their market share predicted to remain stable at 66.53% throughout the forecast period. This segment's growth underscores the importance of providing solutions that cater specifically to the agricultural workforce, improving efficiency and outputs decisively.

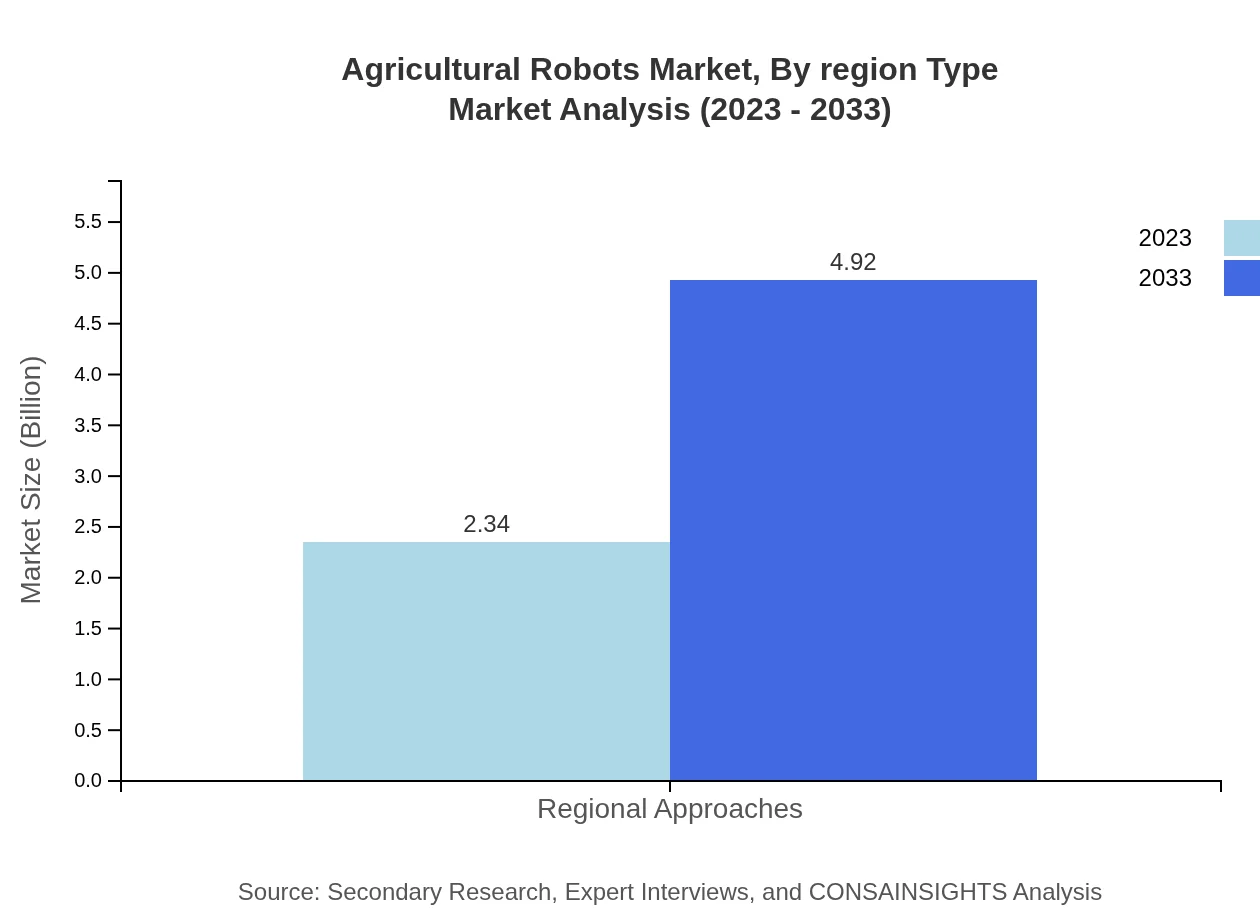

Agricultural Robots Market Analysis By Region Type

Each regional market presents unique opportunities and challenges, reflecting the varying levels of technology adoption and agricultural practices. Europe and North America lead in technological advancement and market share, while regions like Asia Pacific and South America exhibit rapid growth potential due to increasing agricultural needs and investments in farming technologies.

Agricultural Robots Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Agricultural Robots Industry

John Deere:

John Deere is a leading player in the agricultural machinery sector, recognized for its advanced autonomous tractors and precision farming technologies that significantly enhance farming operations worldwide.Trimble Inc.:

Trimble Inc. specializes in agricultural solutions, including precision farming and farm management software, offering robust technological advancements for efficiency and data-driven farming.AG Leader Technology:

AG Leader Technology has become a significant player in the automation and agricultural technology field, providing advanced tools for data collection and precision application.Intuitive Surgical:

Although primarily focused on healthcare, Intuitive Surgical has ventured into agricultural robotics, leveraging surgical robots’ precise control for applications in high-tech farming processes.We're grateful to work with incredible clients.

FAQs

What is the market size of the Agricultural Robots industry?

The agricultural robots market is currently valued at approximately $5 billion and is projected to grow with a CAGR of 7.5% from 2023 to 2033, showcasing substantial growth in the sector.

What are the key market players or companies in the Agricultural Robots industry?

Key players in the agricultural robots market include companies specializing in automation and robotics technologies. Their contributions significantly influence market dynamics and advancements in agricultural practices.

What are the primary factors driving the growth in the Agricultural Robots industry?

Growth is primarily driven by technological advancements in automation, increasing labor costs, and a rising demand for efficient farming solutions. Sustainability practices also encourage the integration of robots in agriculture.

Which region is the fastest Growing in the Agricultural Robots industry?

North America is the fastest-growing region in the agricultural robots market, expanding from $1.68 billion in 2023 to $3.53 billion by 2033, reflecting high adoption rates and innovation in agricultural practices.

Does ConsaInsights provide customized market report data for the Agricultural Robots industry?

Yes, ConsaInsights offers customized market report data tailored to specific client needs in the agricultural robots sector, facilitating in-depth analysis and strategic decision-making.

What deliverables can I expect from this Agricultural Robots market research project?

Deliverables include detailed market analysis, growth forecasts, competitive landscape insights, and actionable recommendations tailored to the agricultural robots industry.

What are the market trends of the Agricultural Robots industry?

Trends include increased automation, the integration of AI and IoT technologies, and greater emphasis on sustainable farming practices, significantly shaping the agricultural robots sector.