Glass Curtain Wall Market Report

First published: 07 October 2024 | Last updated: 22 January 2026 | Report Code: glass-curtain-wall

Glass Curtain Wall Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides a comprehensive analysis of the Glass Curtain Wall market from 2023 to 2033, including market trends, growth forecasts, key market players, and segmentation insights across various regions and product types.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Schüco International KG, Kawneer Company, Inc., Saint-Gobain, BASF SE |

| Published Date | 07 October 2024 |

| Last Modified Date | 22 January 2026 |

Glass Curtain Wall Market Overview

Customize Glass Curtain Wall Market Report market research report

- ✔ Get in-depth analysis of Glass Curtain Wall market size, growth, and forecasts.

- ✔ Understand Glass Curtain Wall's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Glass Curtain Wall

What is the Market Size & CAGR of Glass Curtain Wall market in 2023?

Glass Curtain Wall Industry Analysis

Glass Curtain Wall Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Glass Curtain Wall Market Analysis Report by Region

Europe Glass Curtain Wall Market Report:

The European market for Glass Curtain Walls is expected to see its size surge from $1.58 billion in 2023 to $3.32 billion by 2033, led by stringent building regulations focused on energy efficiency and sustainability, and a growing interest in modern architectural designs.Asia Pacific Glass Curtain Wall Market Report:

The Asia Pacific region is anticipated to exhibit significant growth in the Glass Curtain Wall market, with a market size expected to increase from $0.89 billion in 2023 to $1.87 billion by 2033. Key factors include rapid urbanization, substantial investments in infrastructure projects, and a rising number of skyscrapers in countries like China and India.North America Glass Curtain Wall Market Report:

In North America, the Glass Curtain Wall market is set to grow from $1.86 billion in 2023 to around $3.91 billion by 2033. The region's advanced construction practices, along with a high demand for energy-efficient building solutions, significantly contribute to this expansion.South America Glass Curtain Wall Market Report:

The South American market is projected to grow from $0.34 billion in 2023 to $0.72 billion by 2033. This growth is driven by increasing governmental infrastructure projects and the need for modern commercial buildings that utilize efficient façade systems.Middle East & Africa Glass Curtain Wall Market Report:

The Middle Eastern and African market is projected to expand from $0.34 billion in 2023 to $0.72 billion by 2033. The growth is attributed to increased construction activities in the commercial sector to support growing populations and tourism.Tell us your focus area and get a customized research report.

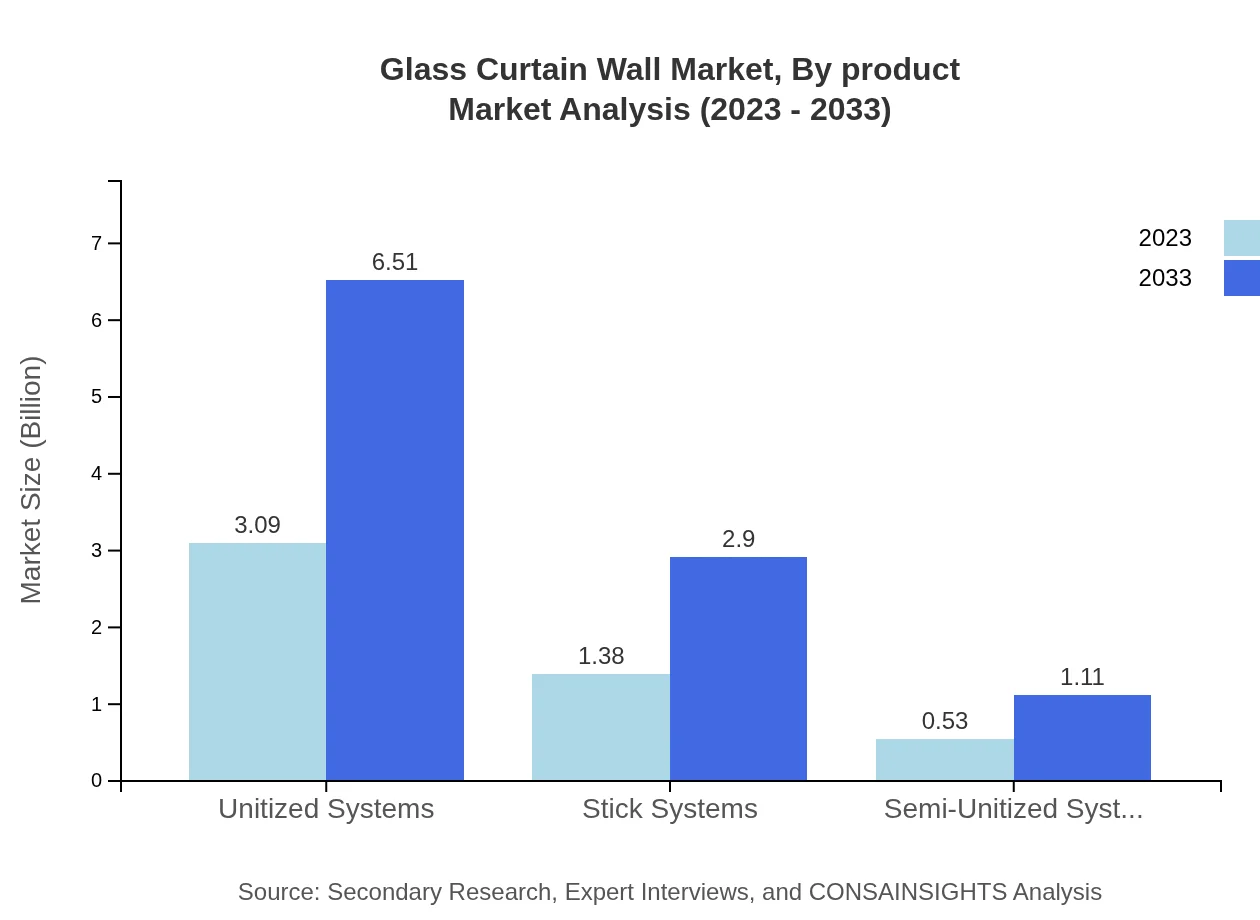

Glass Curtain Wall Market Analysis By Product

The product segmentation reveals unitized systems to be the largest segment, valued at $3.09 billion in 2023 and projected to reach $6.51 billion by 2033, representing 61.88% market share throughout the period. Stick systems follow, with a size of $1.38 billion in 2023, expected to grow significantly. Semi-unitized systems also display promising growth, while the trends highlight a notable preference towards innovations in system designs that improve installation efficiency.

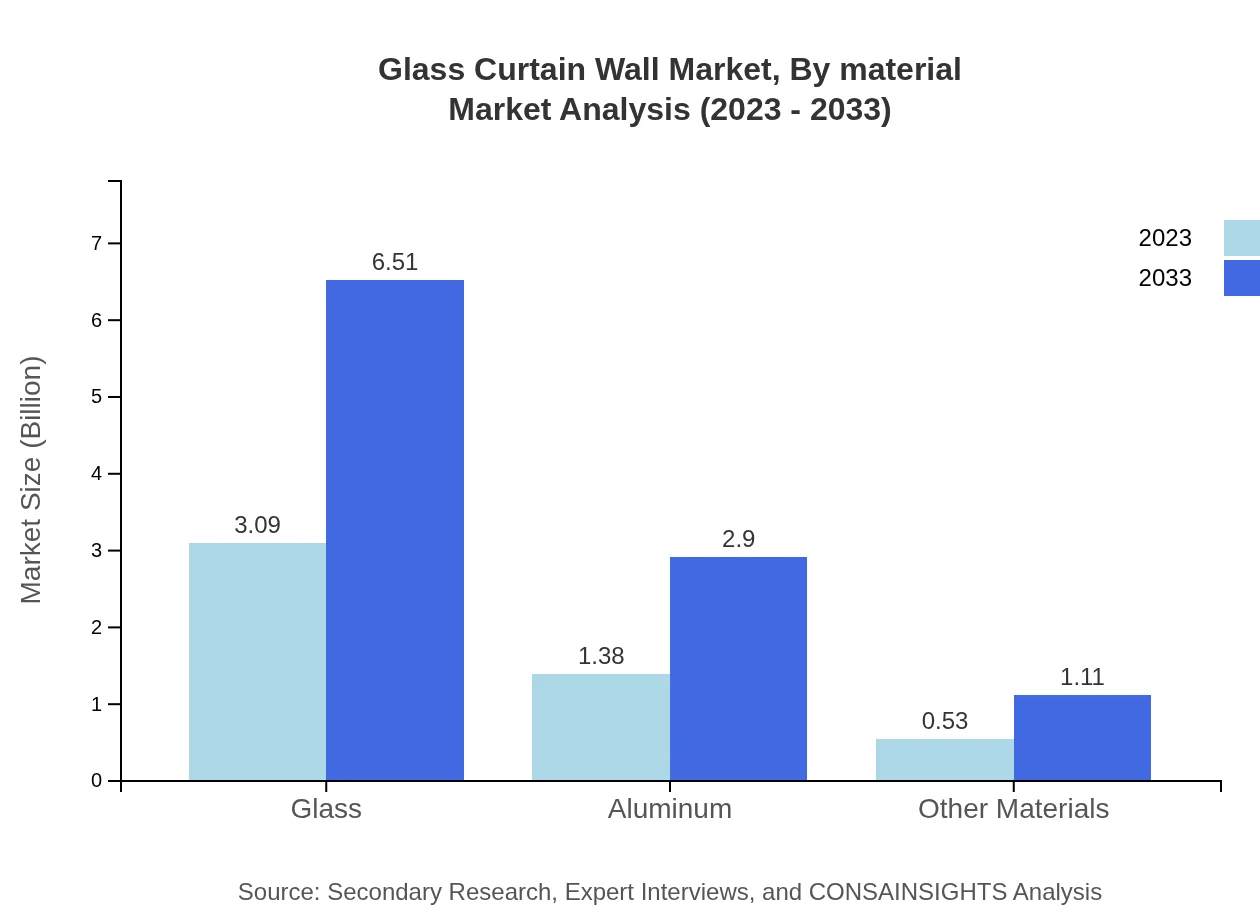

Glass Curtain Wall Market Analysis By Material

In terms of materials, glass dominates the segment, capturing a market size of $3.09 billion in 2023 and anticipated to reach $6.51 billion by 2033, holding a significant share due to its aesthetic and thermal properties. Aluminum remains a crucial material, contributing to $1.38 billion in 2023, with increasing demand for lightweight yet strong building materials. Other materials like polymers and composites are also gaining traction as technology evolves.

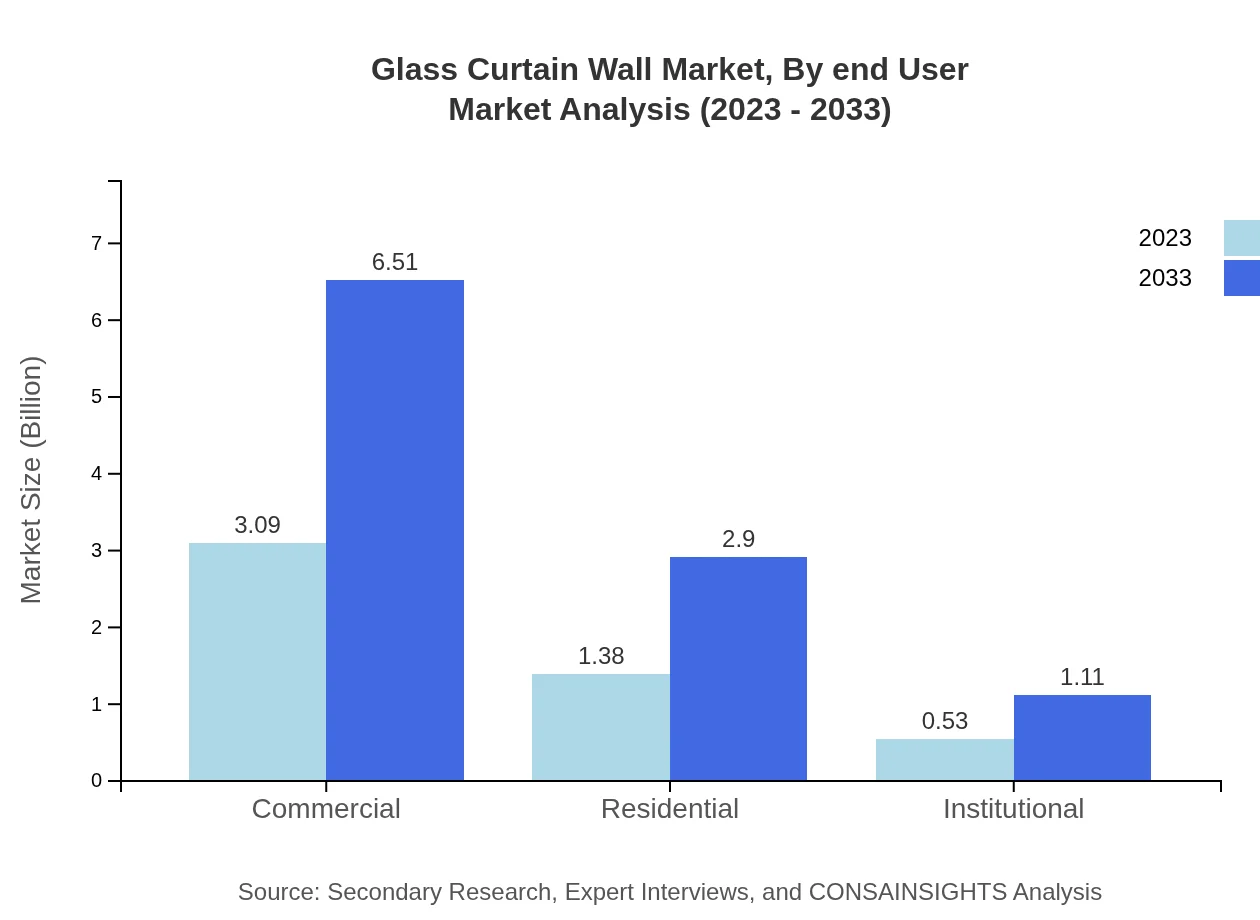

Glass Curtain Wall Market Analysis By End User

The commercial sector is a primary driver of the Glass Curtain Wall market, with a share of 61.88% in 2023, representing a market value of $3.09 billion, expected to grow to $6.51 billion in 2033. The residential and institutional sectors are also vital, contributing substantially to market dynamics driven by modernization and the necessity for energy-efficient structures in housing and education facilities.

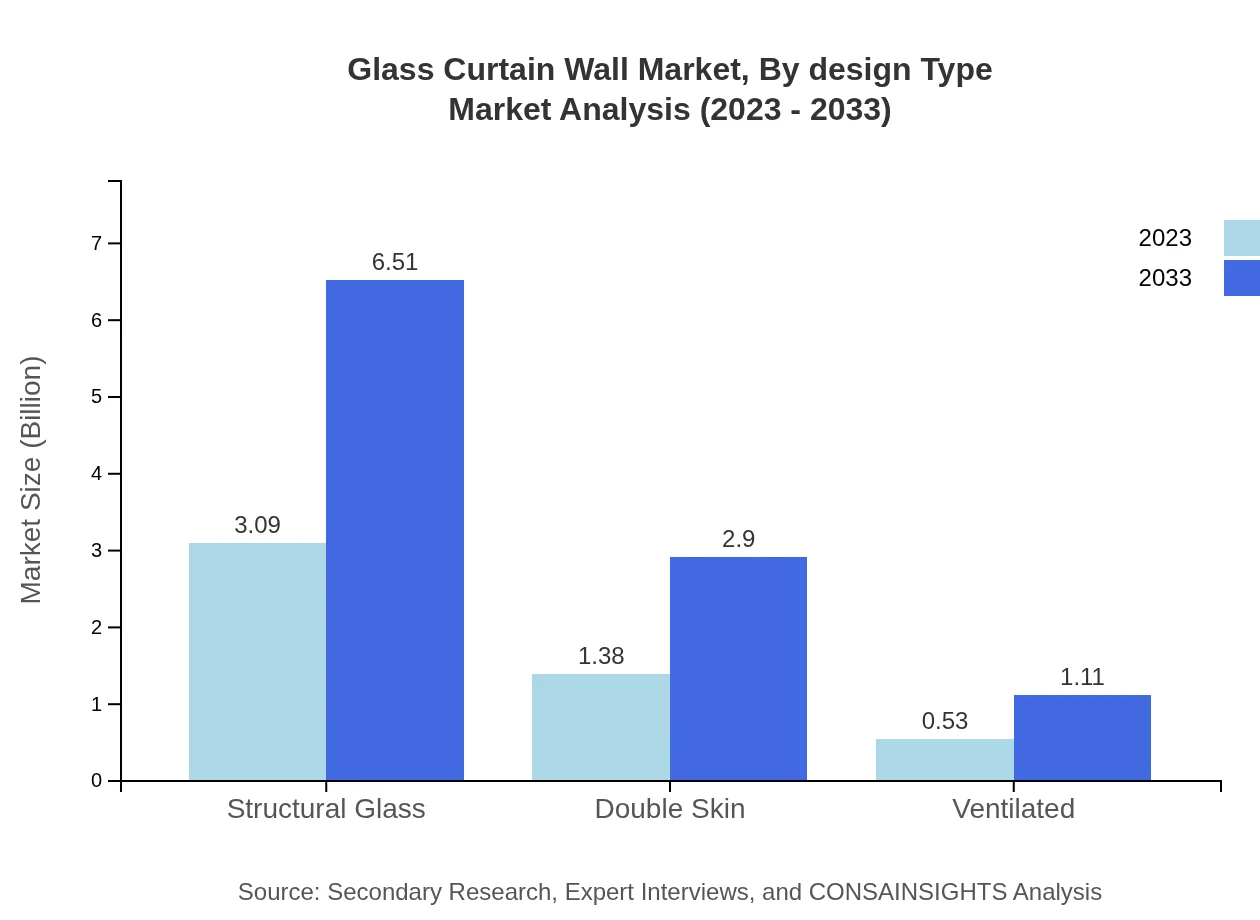

Glass Curtain Wall Market Analysis By Design Type

Design types play a vital role in market segmentation, with structural glass designs leading the market. The double skin design is also gaining traction due to its energy-efficient design. The ventilated systems are becoming increasingly popular, enhancing energy performance and indoor climate control, reflecting innovation in architectural aesthetics.

Glass Curtain Wall Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Glass Curtain Wall Industry

Schüco International KG:

A leading supplier of innovative building envelopes, Schüco specializes in high-performance façade systems and sustainable building solutions.Kawneer Company, Inc.:

Kawneer is renowned for its aluminum curtain wall systems and is a key player in providing robust, energy-efficient façades.Saint-Gobain:

A global leader in glass manufacturing and design, Saint-Gobain provides advanced solutions for curtain walls focusing on sustainability and innovation.BASF SE:

BASF is known for its specialty chemicals and solutions for construction materials, including advanced adhesives used in glass applications.We're grateful to work with incredible clients.

FAQs

What is the market size of glass Curtain Wall?

The glass curtain wall market is experiencing significant growth, projected to reach approximately $5 billion by 2033, with a compound annual growth rate (CAGR) of 7.5%. This indicates a robust demand for these architectural elements globally.

What are the key market players or companies in the glass Curtain Wall industry?

Key players in the glass curtain wall industry include major construction and architectural firms, manufacturers specializing in glass and aluminum systems, and technology innovators focused on sustainable materials and designs, contributing to the market's dynamic landscape.

What are the primary factors driving the growth in the glass Curtain Wall industry?

Growth in the glass curtain wall market is driven by urbanization, the demand for energy-efficient buildings, architectural innovations, and increasing investments in commercial construction projects that prioritize aesthetics and sustainability.

Which region is the fastest Growing in the glass Curtain Wall?

The fastest-growing regions for glass curtain walls include North America and Europe, with North America projected to grow from $1.86 billion in 2023 to $3.91 billion by 2033, reflecting strong infrastructure development and architectural trends.

Does ConsaInsights provide customized market report data for the glass Curtain Wall industry?

Yes, ConsaInsights offers customizable market reports tailored to specific client needs in the glass curtain wall industry, allowing stakeholders to access relevant data and insights that suit their strategic objectives and market focus.

What deliverables can I expect from this glass Curtain Wall market research project?

Deliverables include comprehensive market analysis reports, segmentation insights, growth forecasts, regional trends, competitive landscape review, and actionable recommendations that inform decision-making for stakeholders in the glass curtain wall market.

What are the market trends of glass Curtain Wall?

Current trends in the glass curtain wall market focus on sustainability, with innovations in energy-efficient materials, smart glass technologies, and increased demand for unitized systems, driving a shift towards more efficient architectural solutions.