Industrial Centrifuge Market Report

First published: 07 October 2024 | Last updated: 22 January 2026 | Report Code: industrial-centrifuge

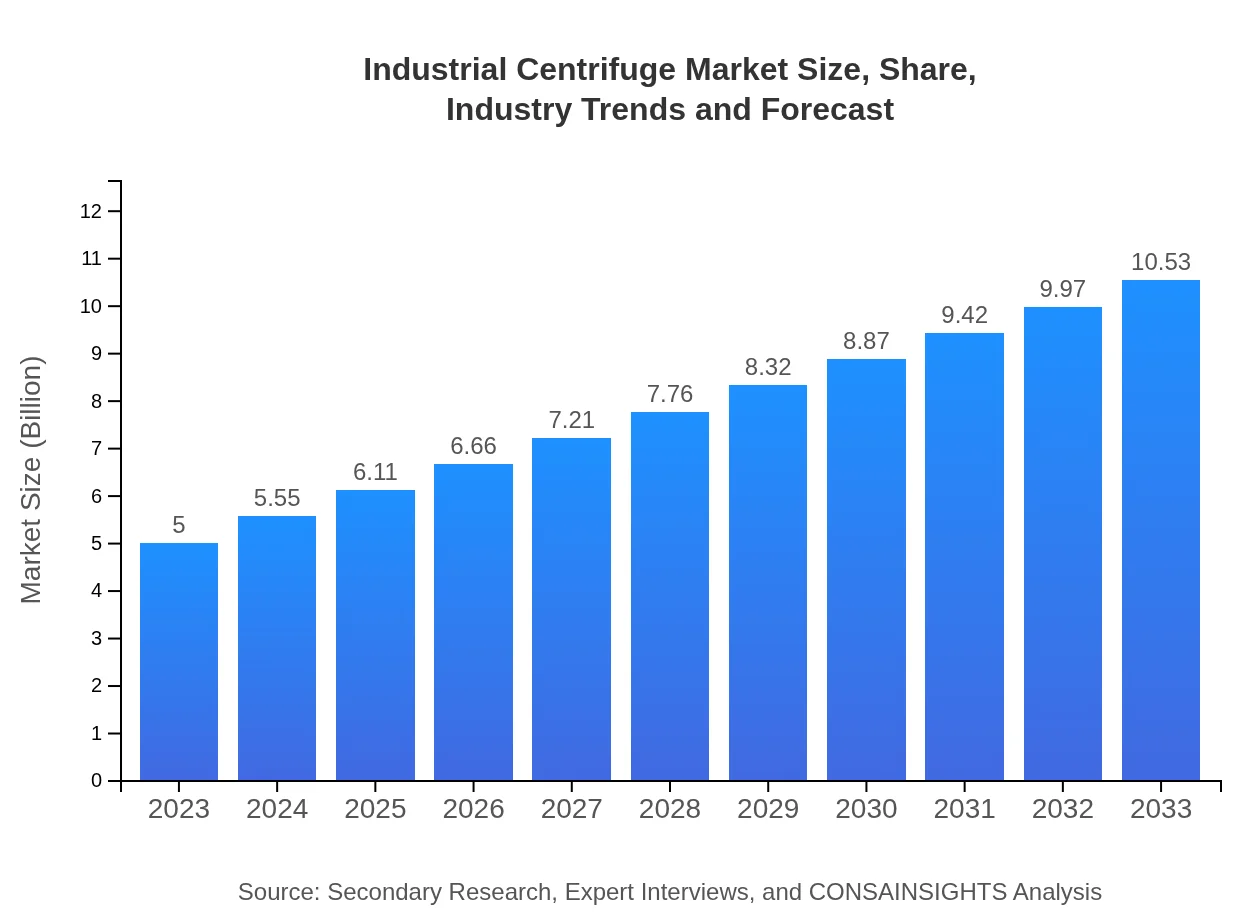

Industrial Centrifuge Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides a comprehensive analysis of the Industrial Centrifuge market, focusing on market dynamics, recent trends, segmentation, and regional performance. It covers forecasts from 2023 to 2033, providing data-driven insights for stakeholders.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Alfa Laval, GEA Group, ANDRITZ, Pieralisi |

| Published Date | 07 October 2024 |

| Last Modified Date | 22 January 2026 |

Industrial Centrifuge Market Overview

Customize Industrial Centrifuge Market Report market research report

- ✔ Get in-depth analysis of Industrial Centrifuge market size, growth, and forecasts.

- ✔ Understand Industrial Centrifuge's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Industrial Centrifuge

What is the Market Size & CAGR of Industrial Centrifuge market in 2023?

Industrial Centrifuge Industry Analysis

Industrial Centrifuge Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Industrial Centrifuge Market Analysis Report by Region

Europe Industrial Centrifuge Market Report:

Europe is one of the leading markets for Industrial Centrifuges, with a market size of $1.74 billion expected to grow to $3.66 billion by 2033. The region benefits from a mature industrial base and increasing technological innovations, driven by a stringent regulatory environment promoting efficient waste management and industrial processes.Asia Pacific Industrial Centrifuge Market Report:

The Asia Pacific region is experiencing notable growth in the Industrial Centrifuge market, driven by rapid industrialization, especially in China and India. In 2023, the market size is estimated at $0.83 billion, expected to reach $1.75 billion by 2033, with a CAGR of 7.7%. The increasing focus on wastewater treatment and food processing industries is anticipated to fuel this growth.North America Industrial Centrifuge Market Report:

North America represents a significant share of the Industrial Centrifuge market, with a size of $1.74 billion in 2023, expected to double to $3.66 billion by 2033. This growth can be attributed to stringent regulations regarding environmental sustainability and advancements in technology across various sectors, particularly in pharmaceuticals and wastewater treatment.South America Industrial Centrifuge Market Report:

In South America, the Industrial Centrifuge market is projected to grow from $0.33 billion in 2023 to $0.69 billion by 2033, reflecting a CAGR of 7.5%. The growth is attributed to rising investments in the mining and food industries, as well as an emphasis on efficient waste management practices.Middle East & Africa Industrial Centrifuge Market Report:

The Middle East and Africa market for Industrial Centrifuges is experiencing gradual growth, expected to increase from $0.36 billion in 2023 to $0.76 billion by 2033, at a CAGR of 7.7%. The growth is driven by investments in oil and gas industries and enhanced wastewater management systems across the region.Tell us your focus area and get a customized research report.

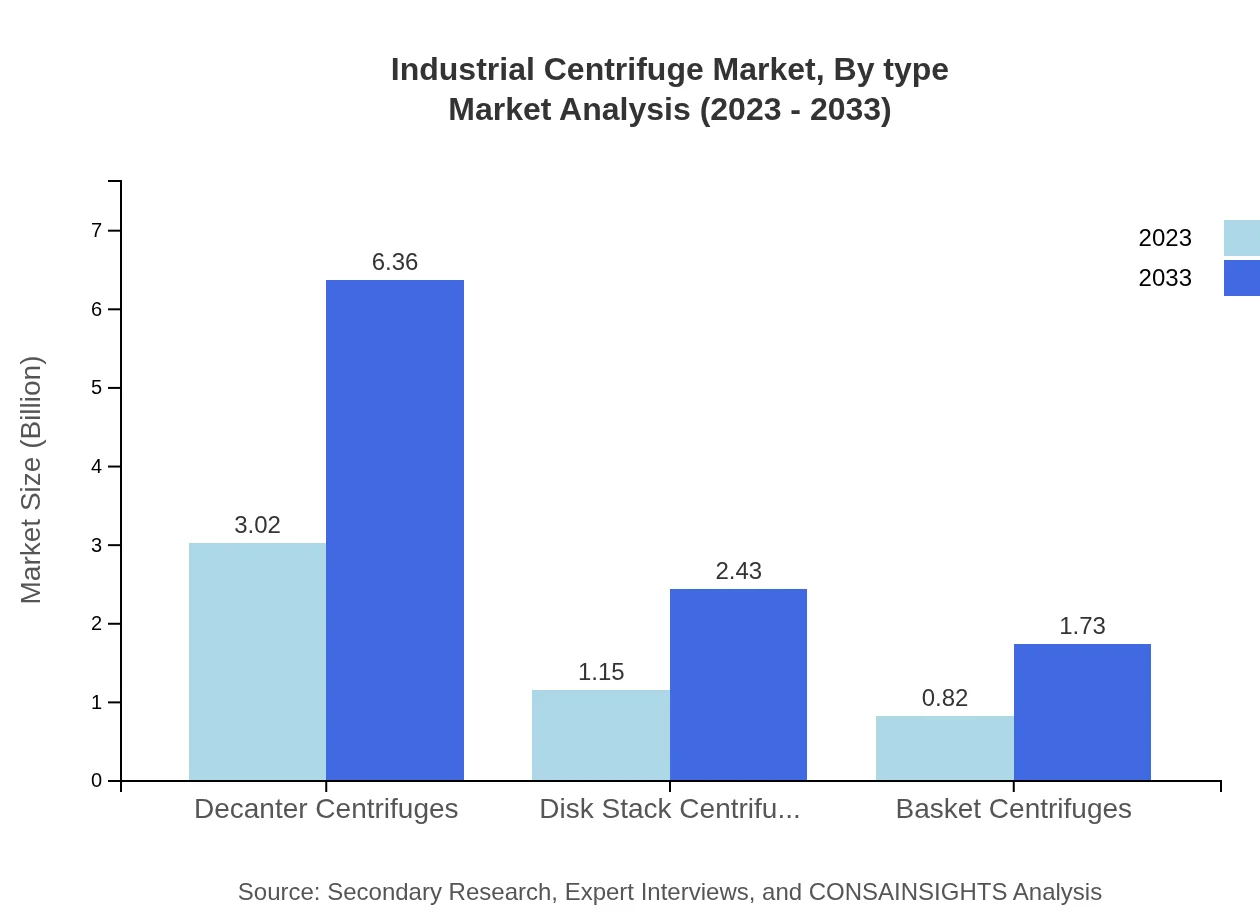

Industrial Centrifuge Market Analysis By Type

In 2023, Decanter Centrifuges dominate the market with a size of $3.02 billion, projected to grow to $6.36 billion by 2033 (60.44% share). Disk Stack Centrifuges follow, starting at $1.15 billion in 2023 and expected to reach $2.43 billion by 2033 (23.08% share). Basket Centrifuges are also notable, moving from $0.82 billion in 2023 to $1.73 billion by 2033 (16.48% share). This indicates a solid demand for advanced separation technologies in various applications.

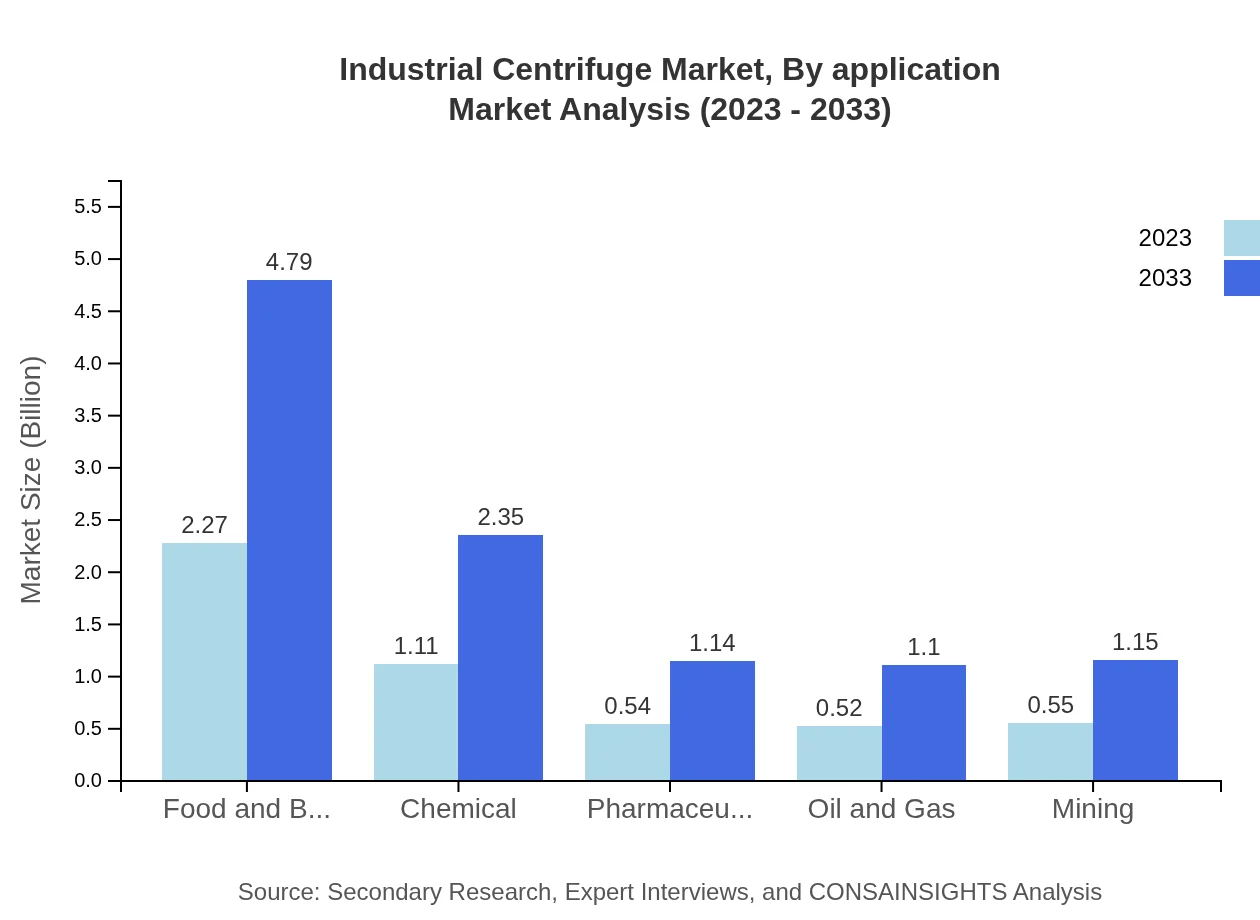

Industrial Centrifuge Market Analysis By Application

The primary applications of Industrial Centrifuges include wastewater treatment, food and beverage, pharmaceuticals, and oil and gas. In 2023, wastewater treatment dominates the application landscape, followed by the food and beverage sector, which reflects a growing trend toward efficient separation technologies within these fields.

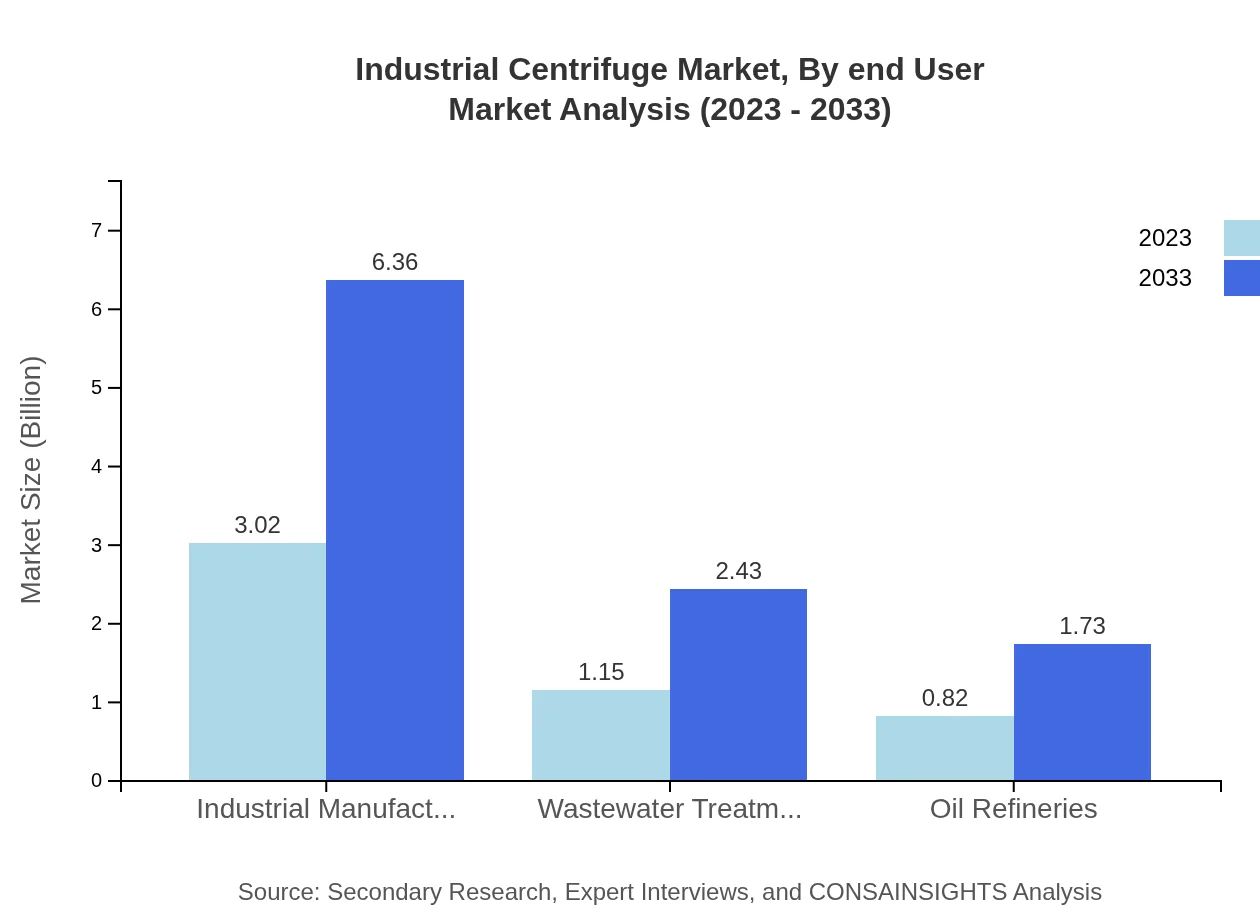

Industrial Centrifuge Market Analysis By End User

Key end-user industries for Industrial Centrifuges include chemical, pharmaceutical, and oil refining industries. The pharmaceutical segment is expected to witness significant growth, driven by increasing investments in healthcare and biopharma sectors aimed at improving production efficiencies.

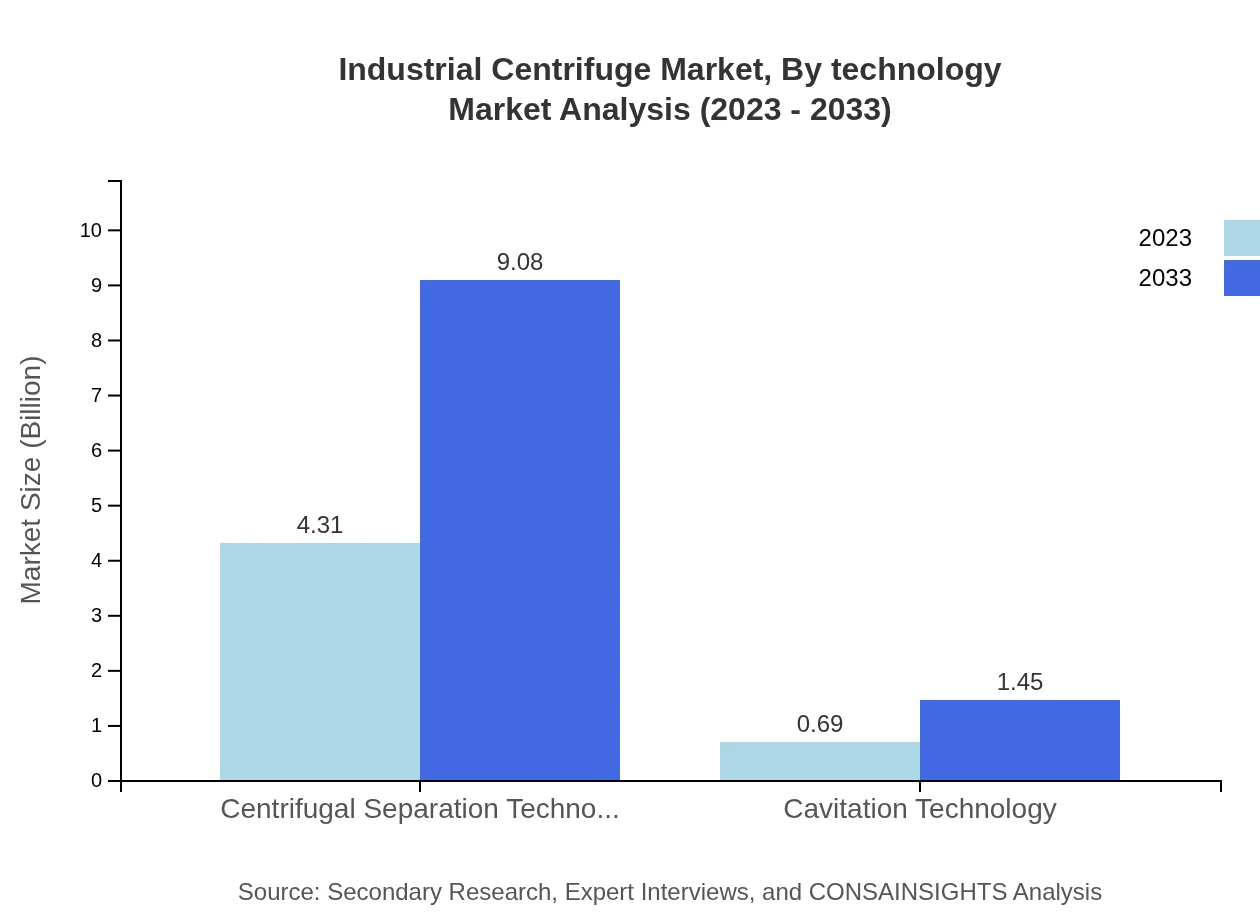

Industrial Centrifuge Market Analysis By Technology

Technology plays a crucial role in the Industrial Centrifuge market, with advanced centrifuge systems that utilize centrifugal separation technology leading the market with a size of $4.31 billion in 2023. The innovation around smart centrifuges is also expected to become a defining trend as industries seek automation and efficiency.

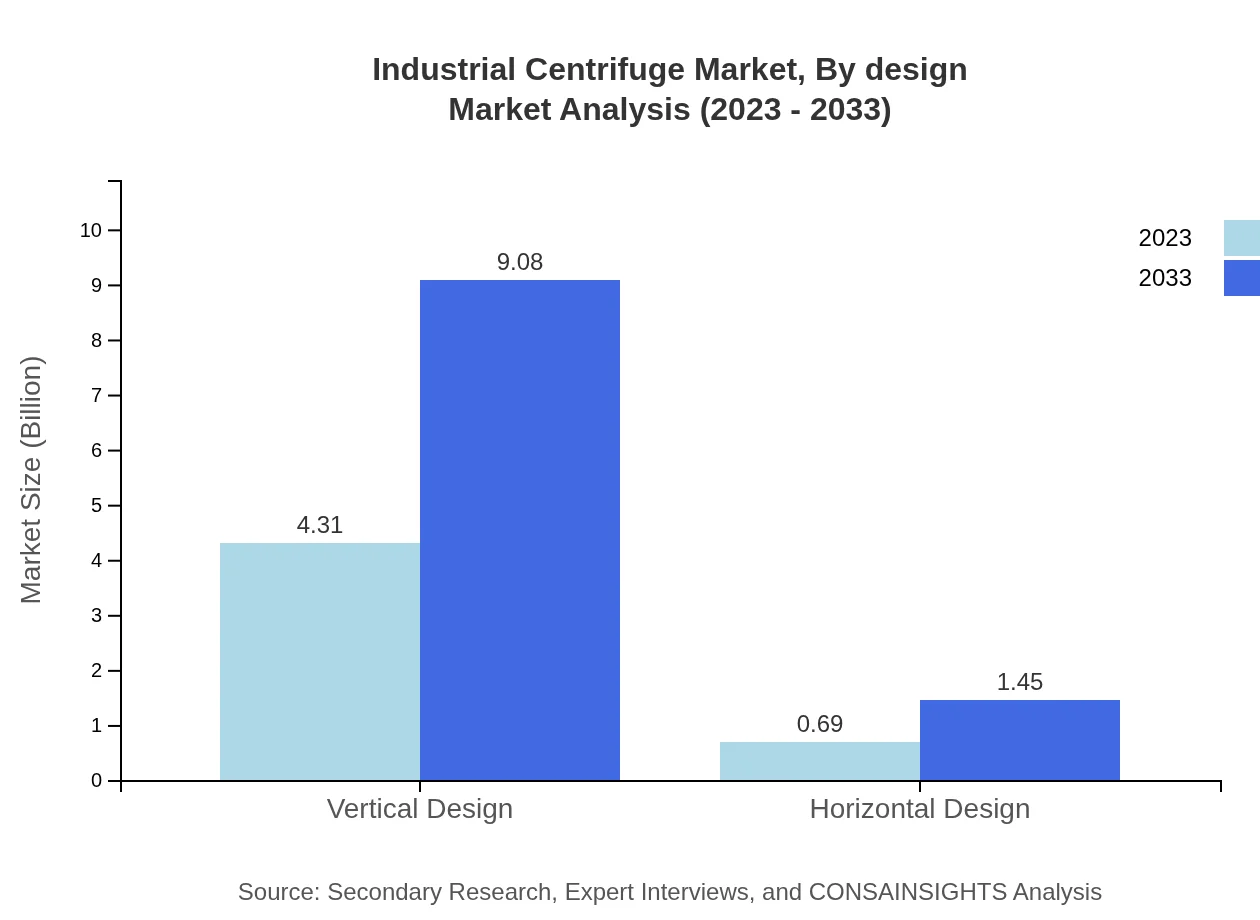

Industrial Centrifuge Market Analysis By Design

The design segment of Industrial Centrifuges includes vertical and horizontal designs. The vertical design currently dominates with a market share of 86.23%, indicating a preference for this format in various applications due to its space efficiency and operational effectiveness.

Industrial Centrifuge Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Industrial Centrifuge Industry

Alfa Laval:

A leading provider of centrifugal separation technology, known for innovative and cost-effective solutions across various industries.GEA Group:

A prominent manufacturer offering a wide range of industrial centrifuges tailored for multiple applications, including food processing and pharmaceuticals.ANDRITZ:

Specializes in separation technologies and equipment for various industries, boasting a comprehensive portfolio of high-performance centrifuges.Pieralisi:

Recognized for technological leadership in separation processes, delivering advanced centrifuge solutions predominantly in the food and beverage sector.We're grateful to work with incredible clients.

FAQs

What is the market size of industrial centrifuge?

The industrial centrifuge market is valued at approximately $5 billion in 2023 and is anticipated to grow at a CAGR of 7.5%, reaching significant market size by 2033, reflecting strong demand across various sectors.

What are the key market players or companies in the industrial centrifuge industry?

Key players in the industrial centrifuge market include established manufacturers and emerging players focusing on innovative technologies, enhancing production efficiency, and expanding their presence through strategic partnerships and acquisitions.

What are the primary factors driving the growth in the industrial centrifuge industry?

Growth in the industrial centrifuge market is driven by increasing demand in wastewater treatment, food and beverage processing, and pharmaceutical production. Technological advancements and the need for efficient separation processes further boost market expansion.

Which region is the fastest Growing in the industrial centrifuge?

The fastest-growing region for industrial centrifuges is Europe, where the market is projected to grow from $1.74 billion in 2023 to $3.66 billion by 2033, highlighting substantial investment and demand across various industries.

Does ConsInsights provide customized market report data for the industrial centrifuge industry?

Yes, ConsInsights provides tailored market report data for the industrial centrifuge sector, enabling clients to access specific insights and analysis based on their unique market needs and strategic objectives.

What deliverables can I expect from this industrial centrifuge market research project?

From the industrial centrifuge market research project, clients can expect comprehensive reports, detailed segment analysis, market forecasts, competitive landscape assessments, and actionable insights tailored to inform business strategies.

What are the market trends of industrial centrifuge?

Current trends in the industrial centrifuge market indicate a shift towards automation, sustainability, and energy efficiency. Moreover, technological innovations are shaping product offerings, catering to industries like pharmaceuticals, food, and chemicals.