Membrane Contactor Market Report

First published: 07 October 2024 | Last updated: 22 January 2026 | Report Code: membrane-contactor

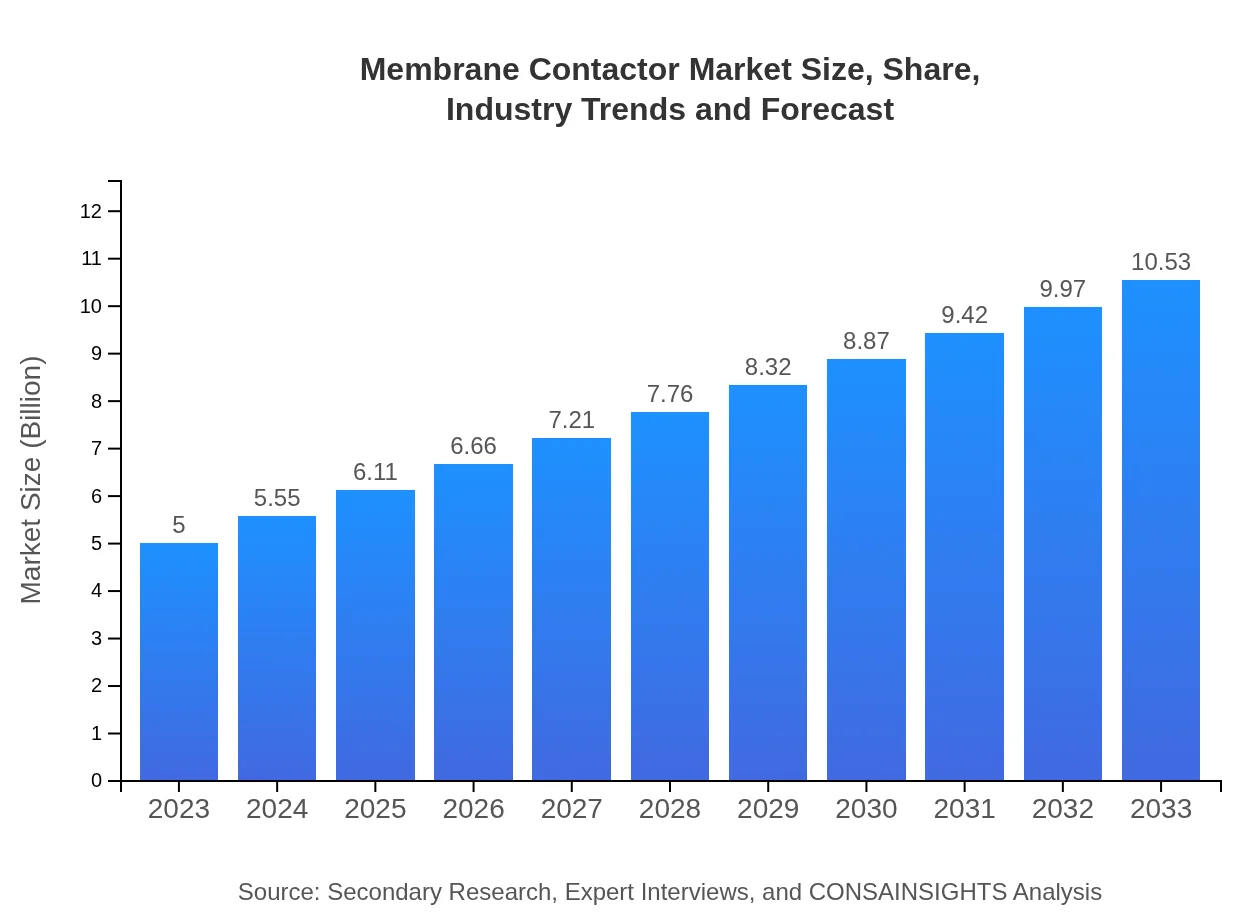

Membrane Contactor Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides an in-depth analysis of the Membrane Contactor market, identifying trends, market size, regional insights, and future growth forecasts up to 2033. Key segments and industry dynamics are explored to assist stakeholders in making informed decisions.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Pall Corporation, Suez Water Technologies & Solutions, Membrane Technology and Research, Inc. |

| Published Date | 07 October 2024 |

| Last Modified Date | 22 January 2026 |

Membrane Contactor Market Overview

Customize Membrane Contactor Market Report market research report

- ✔ Get in-depth analysis of Membrane Contactor market size, growth, and forecasts.

- ✔ Understand Membrane Contactor's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Membrane Contactor

What is the Market Size & CAGR of Membrane Contactor market in 2023?

Membrane Contactor Industry Analysis

Membrane Contactor Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Membrane Contactor Market Analysis Report by Region

Europe Membrane Contactor Market Report:

Europe's Membrane Contactor market is anticipated to flourish, increasing from $1.55 billion in 2023 to $3.27 billion by 2033. The region's focus on green technologies and robust environmental laws fosters advancements in membrane technologies.Asia Pacific Membrane Contactor Market Report:

In the Asia Pacific region, the Membrane Contactor market is set to grow from $0.84 billion in 2023 to $1.77 billion by 2033. This growth is driven by increasing urbanization and industrialization, coupled with rising environmental concerns prompting governments and industries to invest in water purification technologies.North America Membrane Contactor Market Report:

North America will experience significant growth, with the market size expected to increase from $1.95 billion in 2023 to $4.10 billion by 2033. The region's expansion is largely due to stringent water quality regulations and a push for sustainable water management practices.South America Membrane Contactor Market Report:

South America is projected to see its market size grow from $0.32 billion in 2023 to $0.67 billion in 2033. Key drivers include agricultural demand for water efficiency and various municipal initiatives aimed at improving waste management systems.Middle East & Africa Membrane Contactor Market Report:

The Middle East and Africa region's market is expected to rise from $0.34 billion in 2023 to $0.72 billion by 2033, driven by the need for water scarcity solutions and industrial wastewater management, along with increasing investments in infrastructure.Tell us your focus area and get a customized research report.

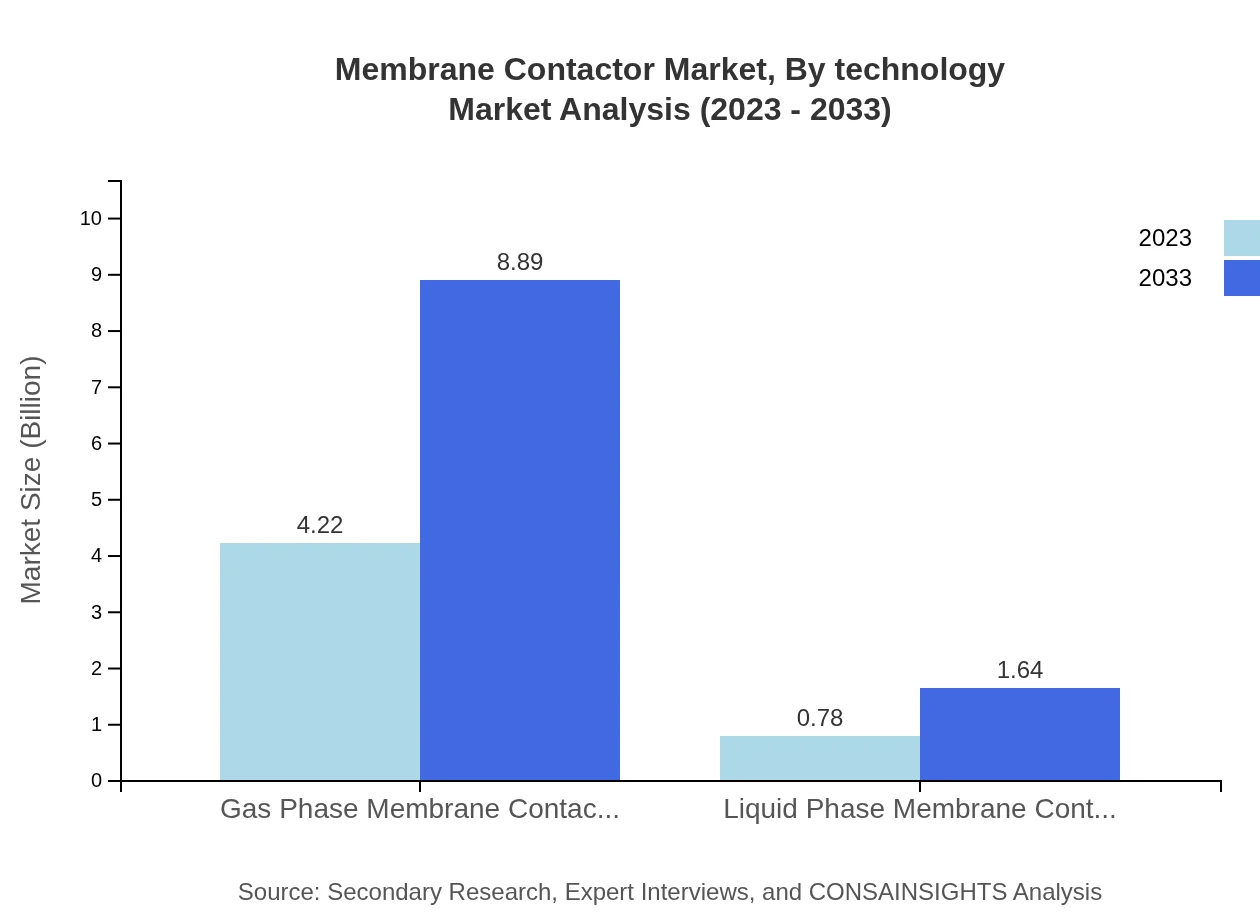

Membrane Contactor Market Analysis By Technology

The Membrane Contactor market is segmented into Gas Phase and Liquid Phase technologies. Gas Phase contactors represent a significant share due to their efficiency in gas absorption and removal applications. In 2023, the Gas Phase segment generates approximately $4.22 billion, with growth expected to reach $8.89 billion by 2033, maintaining an 84.46% market share. Liquid Phase contactors, while smaller in size, are essential for various water treatment applications, starting at $0.78 billion in 2023 and projected to grow to $1.64 billion by 2033, reflecting a continuous demand for efficient liquid separation processes.

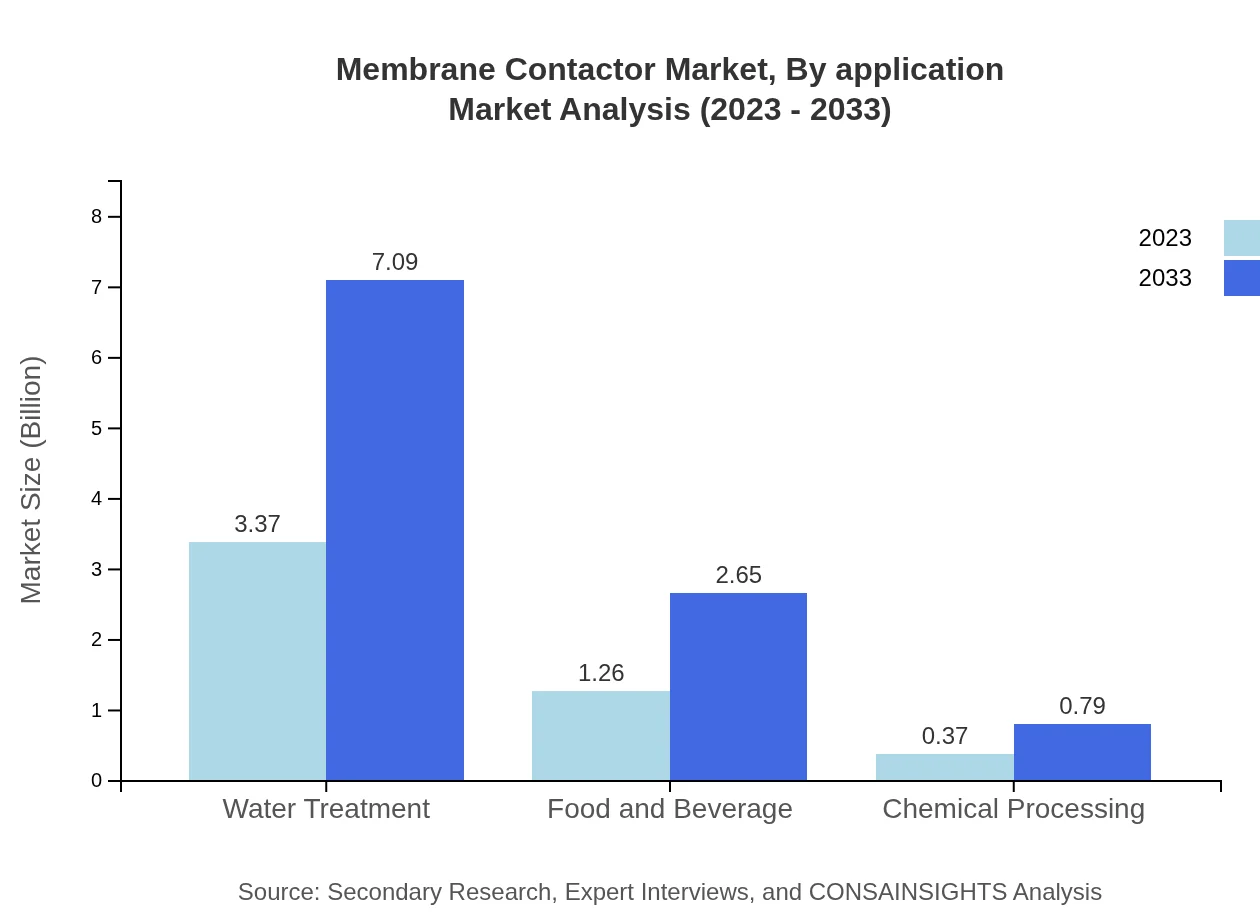

Membrane Contactor Market Analysis By Application

The market is divided into Municipal, Industrial, Energy, Food and Beverage, Chemical Processing, and Water Treatment applications. The Municipal sector is the largest, valued at $3.37 billion in 2023 and expected to grow to $7.09 billion by 2033, maintaining a 67.38% market share. Industrial applications follow, starting at $1.26 billion and set to reach $2.65 billion. The Food and Beverage sector, crucial for quality control, is valued at $1.26 billion and expected to escalate to $2.65 billion, driven by rigorous food safety standards. Energy applications also show promise, with a steady rise anticipated.

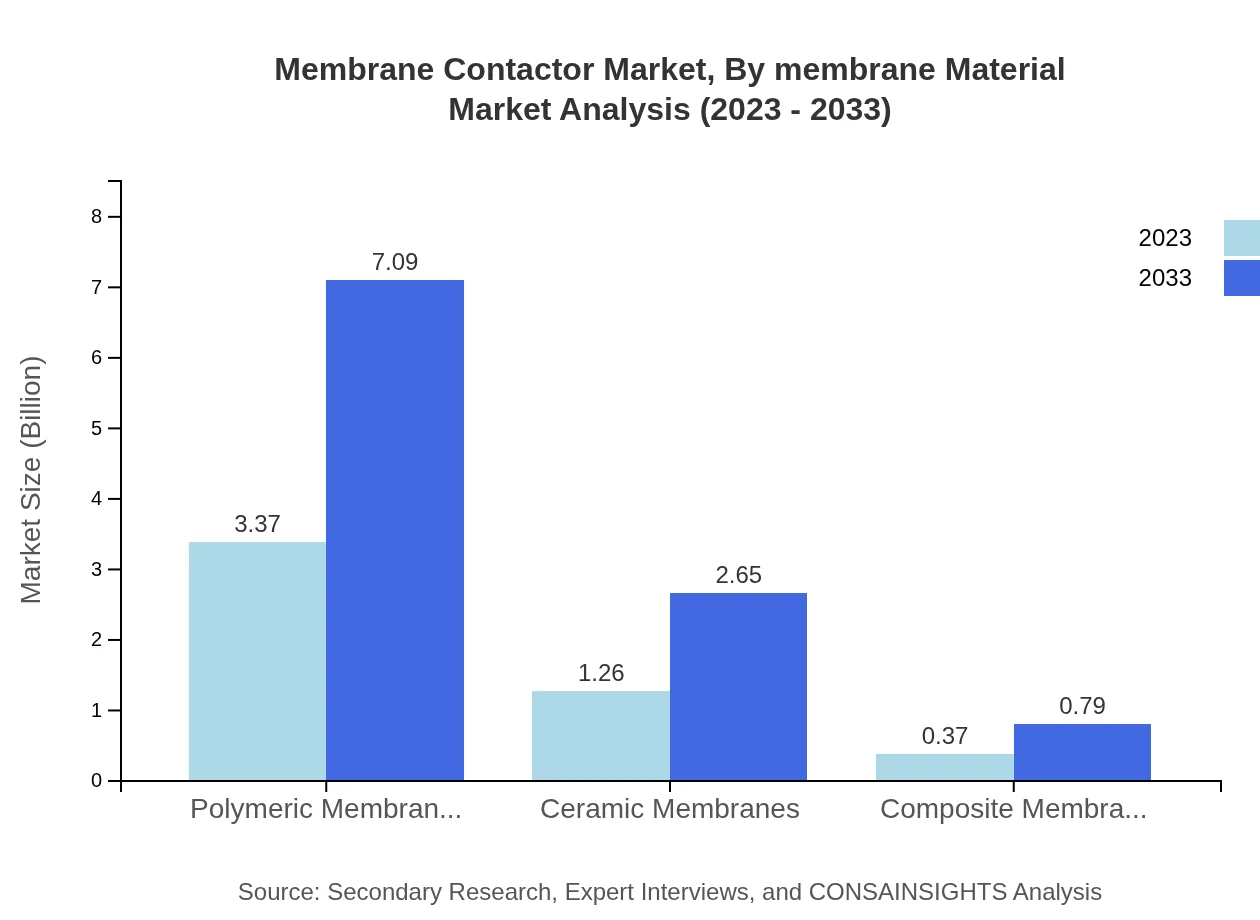

Membrane Contactor Market Analysis By Membrane Material

Membrane materials are categorized into Polymeric, Ceramic, and Composite. Polymeric membranes account for the largest share, with a market size of $3.37 billion in 2023 growing to $7.09 billion by 2033. This is followed by Ceramic membranes, set to increase from $1.26 billion to $2.65 billion, as these materials are increasingly preferred for their durability and resistance to fouling. Composite membranes are emerging due to their ability to combine properties for improved performance, projected to rise from $0.37 billion to $0.79 billion.

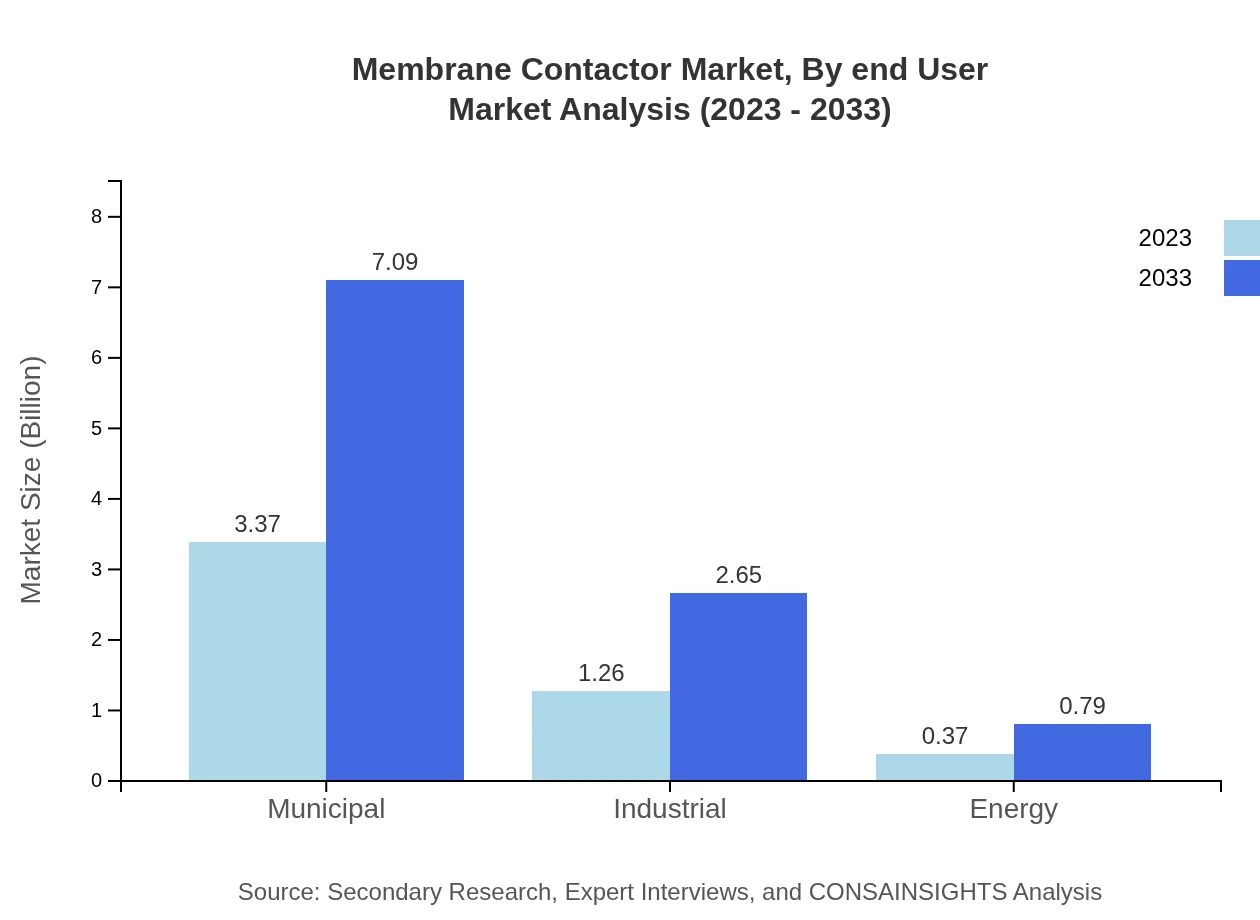

Membrane Contactor Market Analysis By End User

End-user segments include Water Treatment, Food and Beverage, and Chemical Processing industries. Water Treatment holds the largest market share, projected at $3.37 billion in 2023 and expected to grow to $7.09 billion by 2033. The Food and Beverage industry is also significant, with a market evolution from $1.26 billion to $2.65 billion, reflecting increased focus on quality and safety. Chemical Processing continues to enhance operational efficiency through membrane contactors, beginning at $0.37 billion and anticipated to grow to $0.79 billion.

Membrane Contactor Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Membrane Contactor Industry

Pall Corporation:

Pall Corporation specializes in filtration, separation, and purification technologies, providing advanced membrane solutions that enhance operational efficiency across various industries.Suez Water Technologies & Solutions:

Suez offers innovative water treatment solutions, including advanced membrane systems, to improve water quality while ensuring sustainable operations in municipal and industrial sectors.Membrane Technology and Research, Inc.:

Membrane Technology and Research focuses on membrane separation and providing leading-edge solutions for natural gas processing and other industries, leveraging advanced membrane contactor technologies.We're grateful to work with incredible clients.

FAQs

What is the market size of membrane Contactor?

The membrane contactor market was valued at approximately $5 billion in 2023 and is projected to grow at a CAGR of 7.5%. By 2033, the market size is expected to significantly increase, reflecting expanded utilization across various industries.

What are the key market players or companies in this membrane Contactor industry?

Key players in the membrane contactor industry include major companies specializing in filtration and separation technologies. These companies are continuously innovating to enhance performance, adding competitive pressure and driving advancements in membrane technology.

What are the primary factors driving the growth in the membrane Contactor industry?

Growth in the membrane contactor sector is primarily driven by increasing demand for water treatment, advancements in membrane technology, and rising industrial applications. The focus on sustainable solutions also supports market expansion as industries seek efficient separation processes.

Which region is the fastest Growing in the membrane Contactor?

In the membrane contactor market, North America is observed to be the fastest-growing region, with a market size of approximately $1.95 billion in 2023, projected to reach around $4.10 billion by 2033, showcasing robust demand and development in technology.

Does ConsaInsights provide customized market report data for the membrane Contactor industry?

Yes, ConsaInsights offers customized market reports tailored to clients' specific needs in the membrane contactor industry. This includes detailed analyses of market trends, competitive landscapes, and forecasting to aid strategic decision-making.

What deliverables can I expect from this membrane Contactor market research project?

Deliverables from the membrane contactor market research project include comprehensive reports featuring market size data, growth trends, competitive analysis, segment performance metrics, and detailed insights into regional dynamics and future forecasts.

What are the market trends of membrane Contactors?

Market trends for membrane contactors indicate a shift towards integrated applications in water treatment and gas separation technologies. Innovations in membrane materials and production techniques are enhancing efficiency and performance, aligning with industrial sustainability goals.