Scr Power Controller Market Report

First published: 07 October 2024 | Last updated: 22 January 2026 | Report Code: scr-power-controller

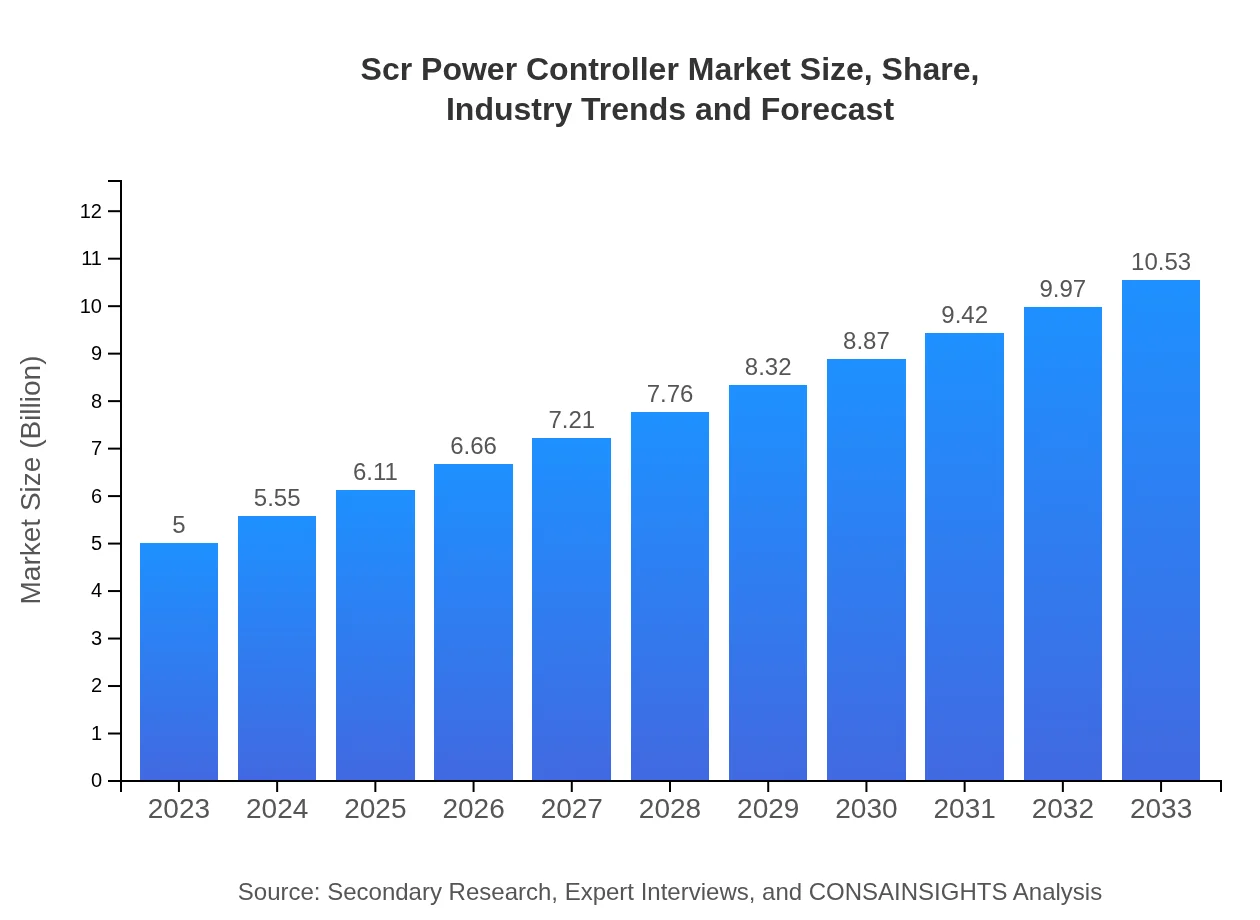

Scr Power Controller Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides a comprehensive analysis of the SCR Power Controller market from 2023 to 2033, including market trends, size, segmentation, regional analysis, key players, and forecasts to help stakeholders make informed decisions.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Siemens AG, ABB Ltd., Schneider Electric |

| Published Date | 07 October 2024 |

| Last Modified Date | 22 January 2026 |

SCR Power Controller Market Overview

Customize Scr Power Controller Market Report market research report

- ✔ Get in-depth analysis of Scr Power Controller market size, growth, and forecasts.

- ✔ Understand Scr Power Controller's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Scr Power Controller

What is the Market Size & CAGR of SCR Power Controller market in 2023 and 2033?

SCR Power Controller Industry Analysis

SCR Power Controller Market Segmentation and Scope

Tell us your focus area and get a customized research report.

SCR Power Controller Market Analysis Report by Region

Europe Scr Power Controller Market Report:

The European SCR Power Controller market is slated for growth from $1.54 billion in 2023 to $3.23 billion by 2033, driven by stringent regulations on energy consumption and significant investments in renewable energy initiatives.Asia Pacific Scr Power Controller Market Report:

In the Asia Pacific region, the SCR Power Controller market is forecasted to grow from $0.94 billion in 2023 to $1.99 billion by 2033. Factors such as rapid industrialization, increasing energy demands, and government incentives for renewable energy are driving this growth.North America Scr Power Controller Market Report:

North America displays a robust SCR Power Controller market, projected to grow from $1.78 billion in 2023 to $3.75 billion by 2033. The region's strong regulatory frameworks favoring energy efficiency and the increasing adoption of automation technologies in industries are pivotal factors.South America Scr Power Controller Market Report:

South America is expected to see growth from $0.21 billion in 2023 to $0.45 billion in 2033. Continuous development in infrastructure and increasing energy investments are supporting the expansion of the SCR Power Controller market in this region.Middle East & Africa Scr Power Controller Market Report:

The Middle East and Africa market is projected to increase from $0.52 billion in 2023 to $1.10 billion by 2033, supported by ongoing industrial development and a focus on enhancing energy efficiency across the region.Tell us your focus area and get a customized research report.

Scr Power Controller Market Analysis By Application

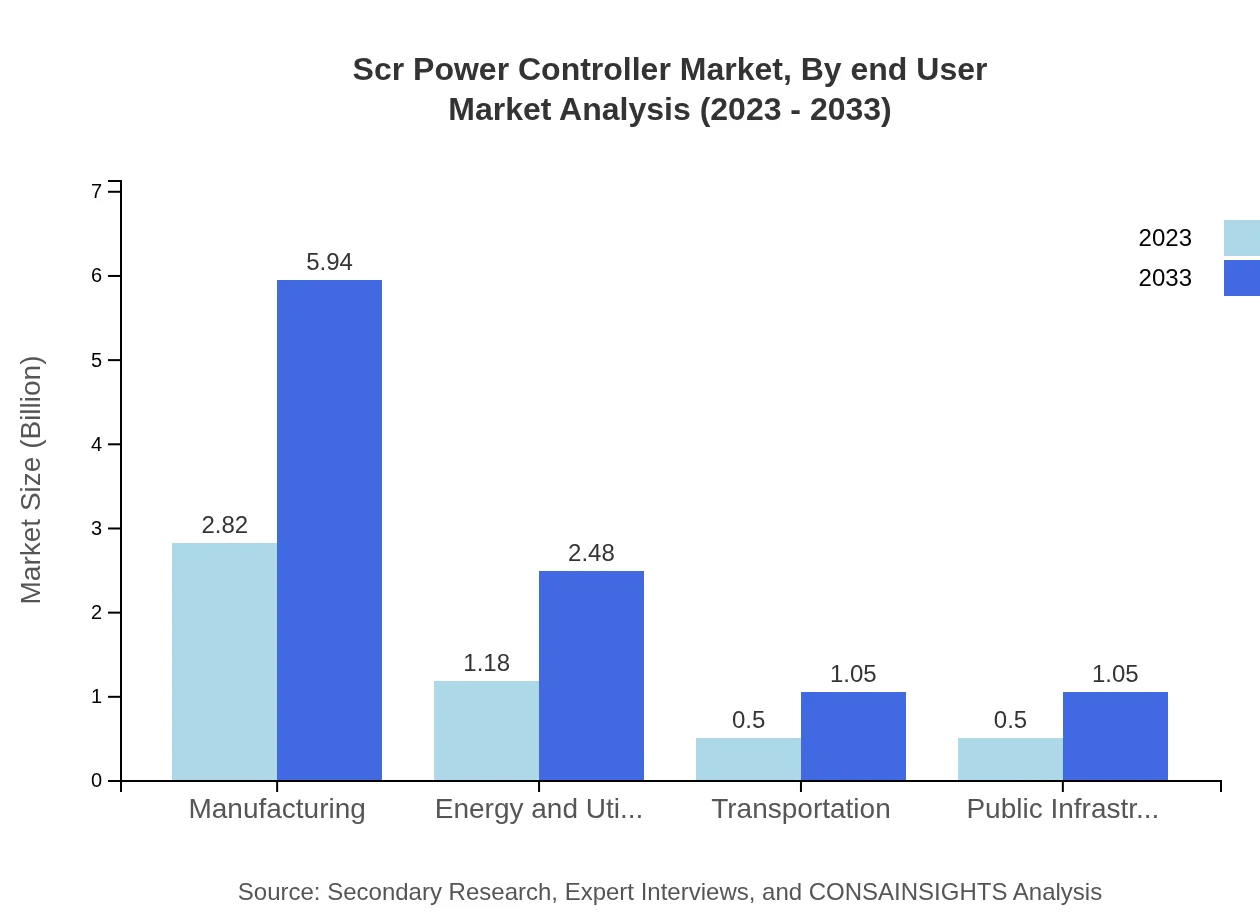

The SCR Power Controller market segmented by application features key segments: Manufacturing, Energy and Utilities, Transportation, and Public Infrastructure. Manufacturing holds the largest share, representing approximately $2.82 billion in 2023, expected to increase to $5.94 billion by 2033. Energy and Utilities follow, increasing from $1.18 billion to $2.48 billion, while Transportation and Public Infrastructure are emerging segments, each growing from $0.50 billion to $1.05 billion over the same period.

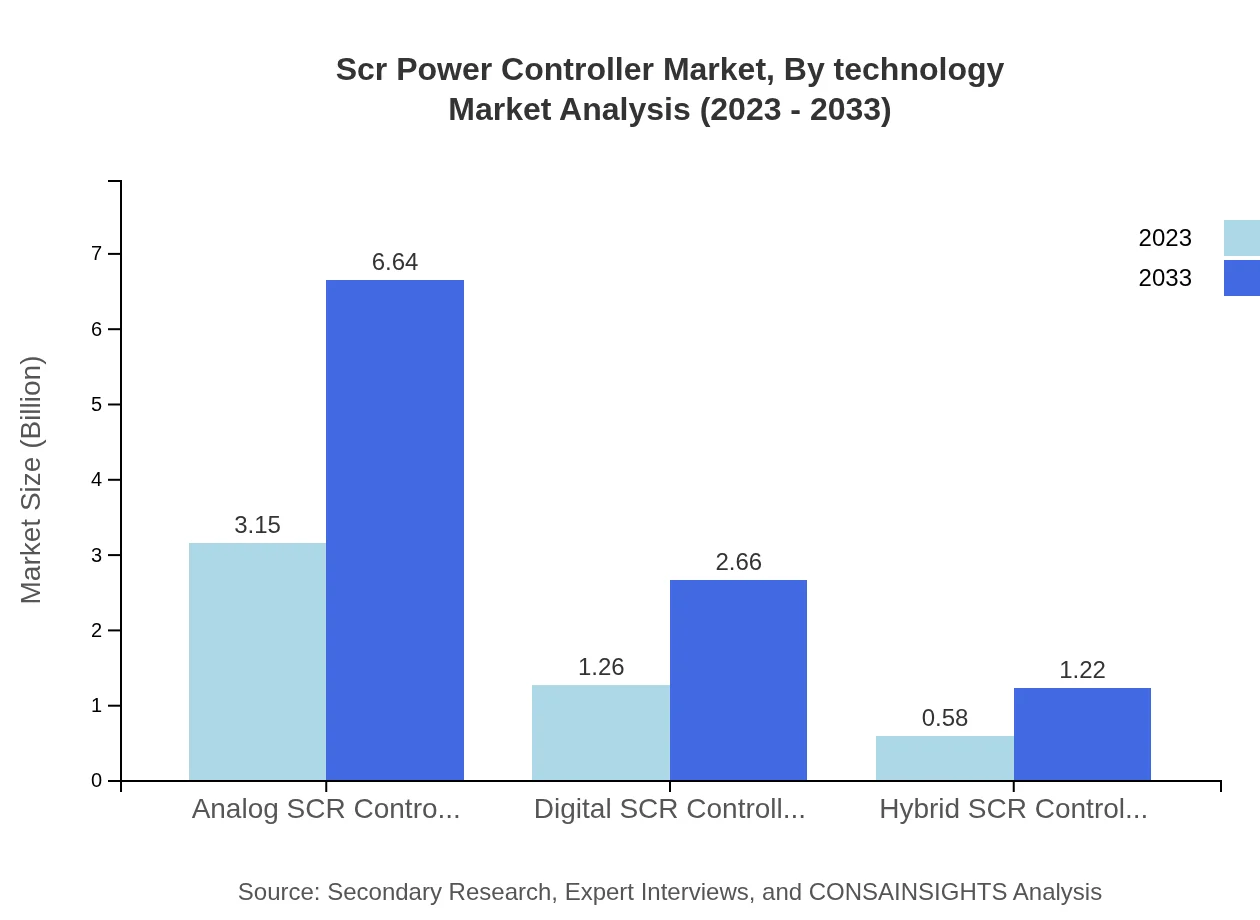

Scr Power Controller Market Analysis By Technology

The market's technology segment includes Analog, Digital, and Hybrid SCR Controllers. Analog SCR Controllers dominate with a market size of $3.15 billion in 2023 and forecasted to reach $6.64 billion by 2033. Digital SCR Controllers are also expanding, projected to grow from $1.26 billion to $2.66 billion, while Hybrid controllers are positioned for growth from $0.58 billion to $1.22 billion, reflecting trends toward more sophisticated control systems.

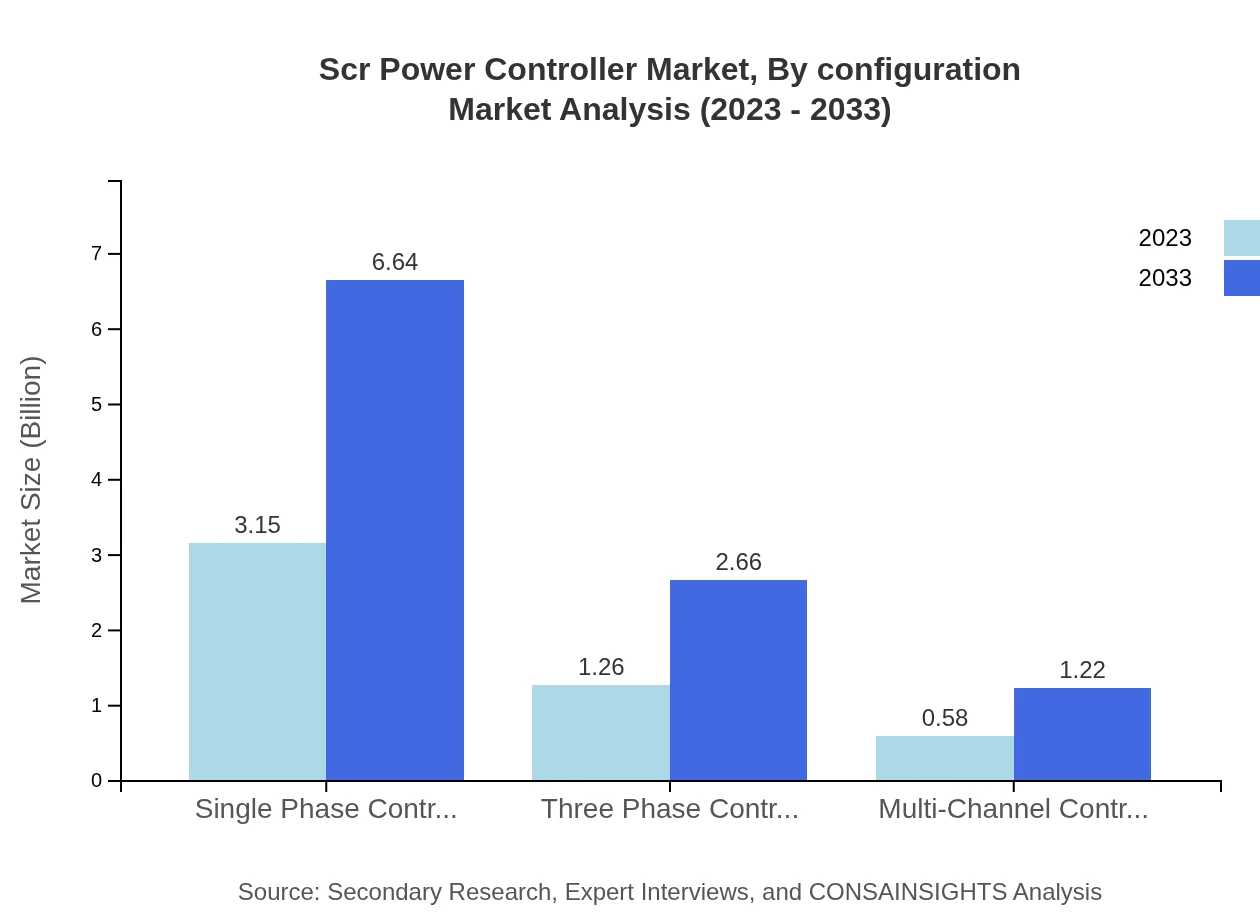

Scr Power Controller Market Analysis By Configuration

Configuration-wise, the market is divided into Single Phase, Three Phase, and Multi-Channel Controllers. Single Phase Controllers lead the market with a size of $3.15 billion in 2023, expected to reach $6.64 billion by 2033. Three Phase Controllers also show potential growth from $1.26 billion to $2.66 billion, whereas Multi-Channel Controllers are projected to grow from $0.58 billion to $1.22 billion, underscoring their relevance in complex applications.

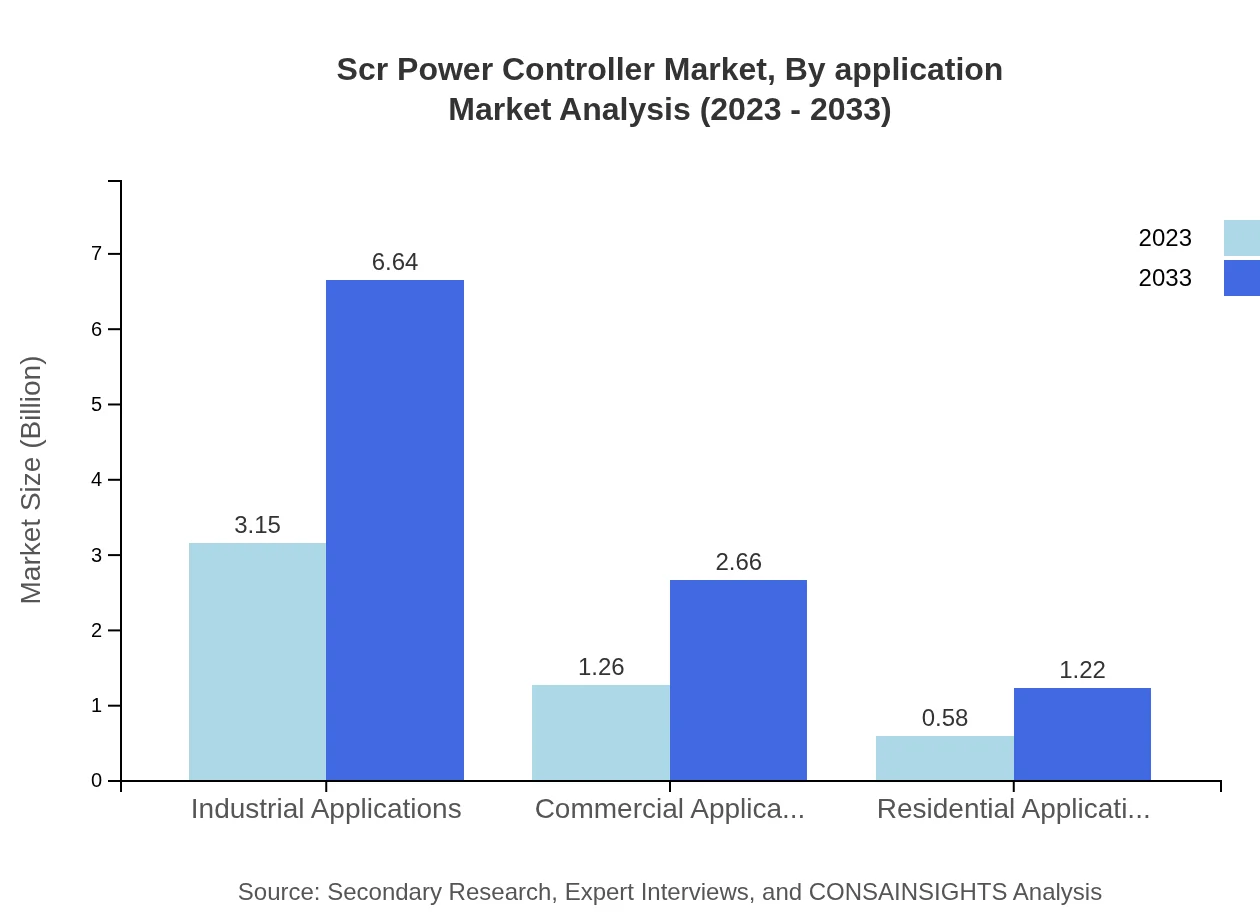

Scr Power Controller Market Analysis By End User

In terms of end-users, the market is segmented into Industrial Applications, Commercial Applications, and Residential Applications. Industrial Applications command the largest share, valued at $3.15 billion in 2023, growing to $6.64 billion by 2033. Commercial Applications follow, with an increase from $1.26 billion to $2.66 billion, while Residential Applications are also on the rise from $0.58 billion to $1.22 billion, as energy efficiency becomes crucial in homes.

SCR Power Controller Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in SCR Power Controller Industry

Siemens AG:

Siemens AG is a global leader in automation and digitalization, providing innovative SCR Power Controllers that enhance efficiency and performance across various sectors.ABB Ltd.:

ABB Ltd. is renowned for its advanced power and automation technologies, offering a comprehensive range of SCR Power Controllers that cater to industrial and commercial needs.Schneider Electric:

Schneider Electric is a prominent player in energy management, delivering SCR Power Controllers that focus on sustainability and efficiency in power generation and consumption.We're grateful to work with incredible clients.

FAQs

What is the market size of SCR Power Controller?

The global SCR Power Controller market is valued at approximately $5 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 7.5%, reaching around $11 billion by 2033.

What are the key market players or companies in this SCR Power Controller industry?

Key players in the SCR Power Controller industry include Schneider Electric, Siemens AG, ABB Ltd, Rockwell Automation, and General Electric. These companies are known for their innovative technologies and extensive product portfolios, driving significant market growth.

What are the primary factors driving the growth in the SCR Power Controller industry?

Growth in the SCR Power Controller market is driven by rising industrial automation, increasing demand for energy efficiency, and advancements in technology. The shift towards renewable energy sources also encourages investment in SCR controllers for better energy management.

Which region is the fastest Growing in the SCR Power Controller market?

The Asia Pacific region is expected to be the fastest-growing area for SCR Power Controllers, with a market size projected to grow from $0.94 billion in 2023 to $1.99 billion by 2033, indicating rising industrialization and infrastructure development.

Does ConsaInsights provide customized market report data for the SCR Power Controller industry?

Yes, ConsaInsights offers customized market report data tailored to specific needs in the SCR Power Controller industry, allowing businesses to access relevant insights that can drive strategic decision-making and competitive advantage.

What deliverables can I expect from this SCR Power Controller market research project?

Deliverables from the SCR Power Controller market research project include comprehensive market analysis reports, competitive landscape evaluations, trend identification, segmentation insights, and actionable recommendations to inform business strategies.

What are the market trends of SCR Power Controller?

Current market trends in SCR Power Controllers include enhanced energy efficiency, integration with smart grid technology, and a growing preference for digital and hybrid SCR controllers, reflecting innovations aimed at optimizing performance and reducing costs.