Reports >

Chemicals And Materials

>

Polysilicon Market Report

Polysilicon Market Report

First published: 03 October 2024 | Last updated: 02 February 2026 | Report Code: polysilicon

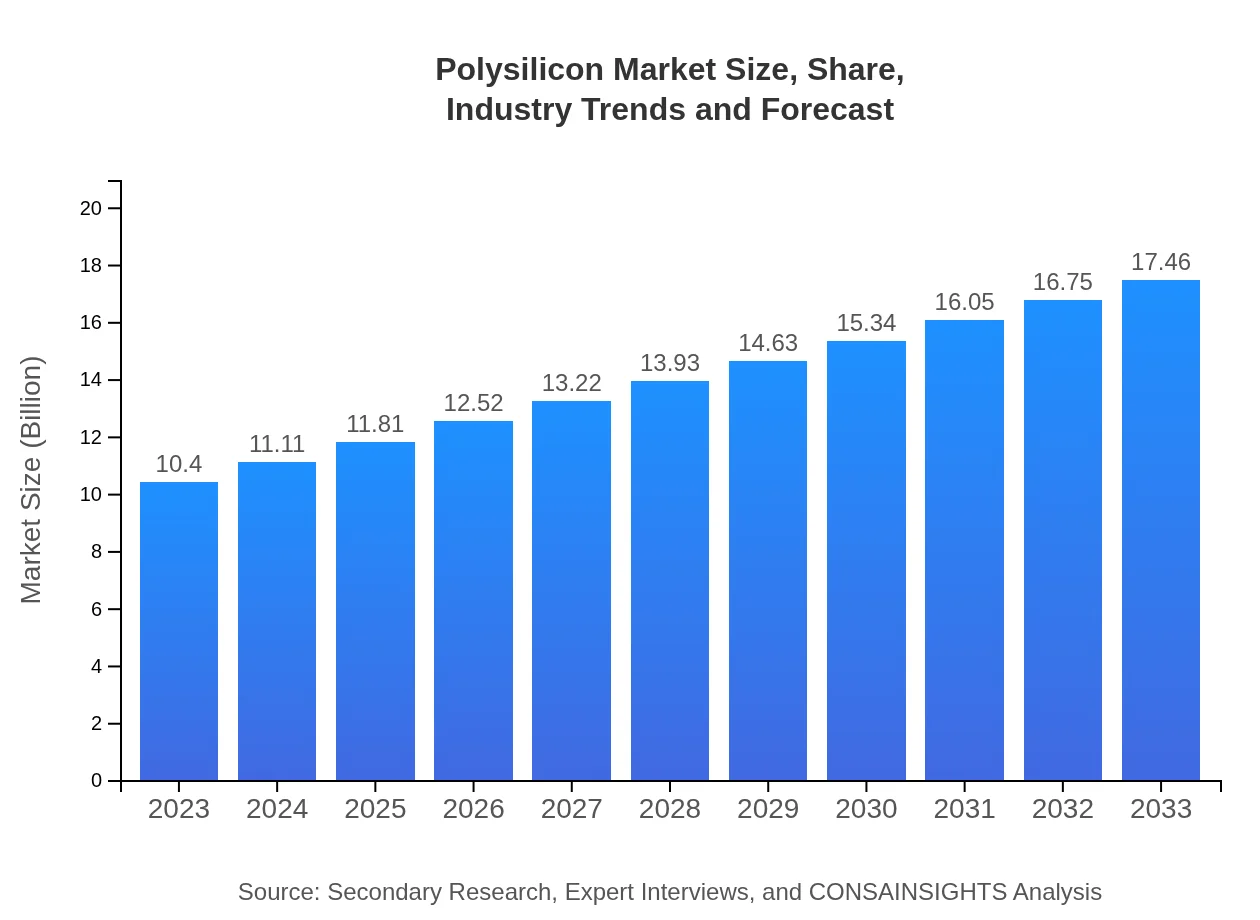

Polysilicon Market — USD 10.4 billion in 2023, Growing to USD 17.46B by 2033 at 5.2% CAGR

This report provides an in-depth analysis of the Polysilicon market, focusing on market dynamics, trends, forecasts, and regional insights for the period 2023 to 2033. It covers market size, CAGR, industry segments, and key players shaping the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $10.40 Billion |

| CAGR (2023-2033) | 5.2% |

| 2033 Market Size | $17.46 Billion |

| Top Companies | Wacker Chemie AG, GCL-Poly Energy Holdings Limited, OCI Company Ltd., REC Silicon |

| Published Date | 03 October 2024 |

| Last Modified Date | 02 February 2026 |

Polysilicon Market Overview

Customize Polysilicon Market Report market research report

- ✔ Get in-depth analysis of Polysilicon market size, growth, and forecasts.

- ✔ Understand Polysilicon's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Polysilicon

What is the Market Size & CAGR of Polysilicon market in 2023?

Polysilicon Industry Analysis

Polysilicon Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Polysilicon Market Analysis Report by Region

Europe Polysilicon Market Report:

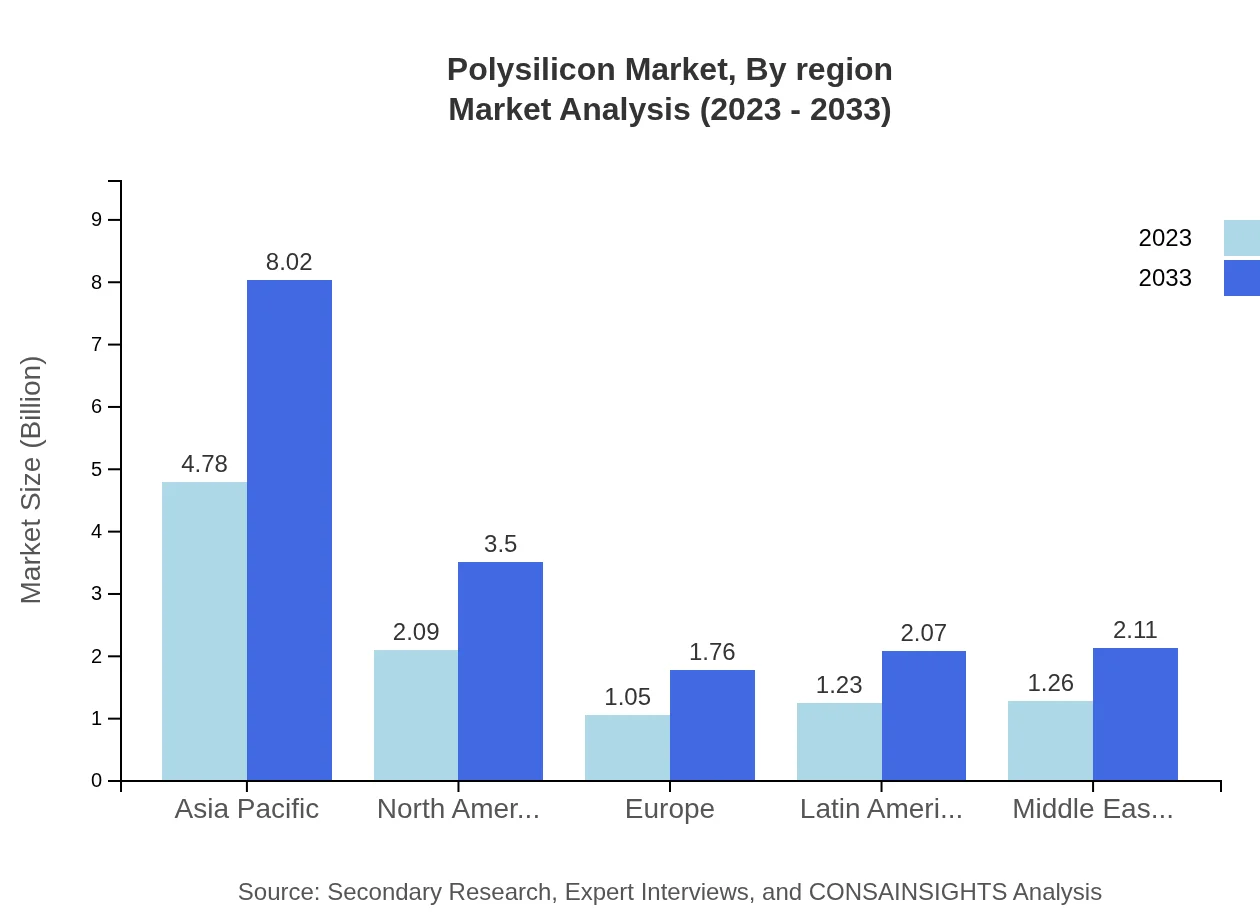

In Europe, the market is expected to expand from $2.98 billion in 2023 to about $4.99 billion by 2033. European countries are aggressively enhancing their solar capabilities, spurred by ambitious renewable energy targets and subsidies that encourage solar installations.Asia Pacific Polysilicon Market Report:

In 2023, Asia Pacific dominates the Polysilicon market, accounting for approximately $2.25 billion, with projections to reach $3.77 billion by 2033. The region is a leader in solar panel production and technological advancements, driven by countries like China, leading in polysilicon manufacturing capacity. The strong governmental support for renewable energy contributes significantly to this growth.North America Polysilicon Market Report:

North America is projected to grow from $3.40 billion in 2023 to approximately $5.70 billion by 2033. The increase is driven by a shift towards renewable energy sources, with substantial investments in solar energy infrastructure and technology, alongside stringent regulations aimed at reducing carbon emissions.South America Polysilicon Market Report:

The South American Polysilicon market is valued at $0.69 billion in 2023, with an anticipated growth to $1.15 billion by 2033. Countries such as Brazil and Chile are increasingly investing in solar energy projects, which is expected to boost the demand for polysilicon as a critical component.Middle East & Africa Polysilicon Market Report:

The Middle East and Africa region's Polysilicon market is valued at $1.10 billion in 2023, growing to $1.84 billion by 2033. The region is increasingly exploring solar energy as a viable power source, particularly in the Gulf Cooperation Council (GCC) nations, which are focusing on diversifying their energy sources.Tell us your focus area and get a customized research report.

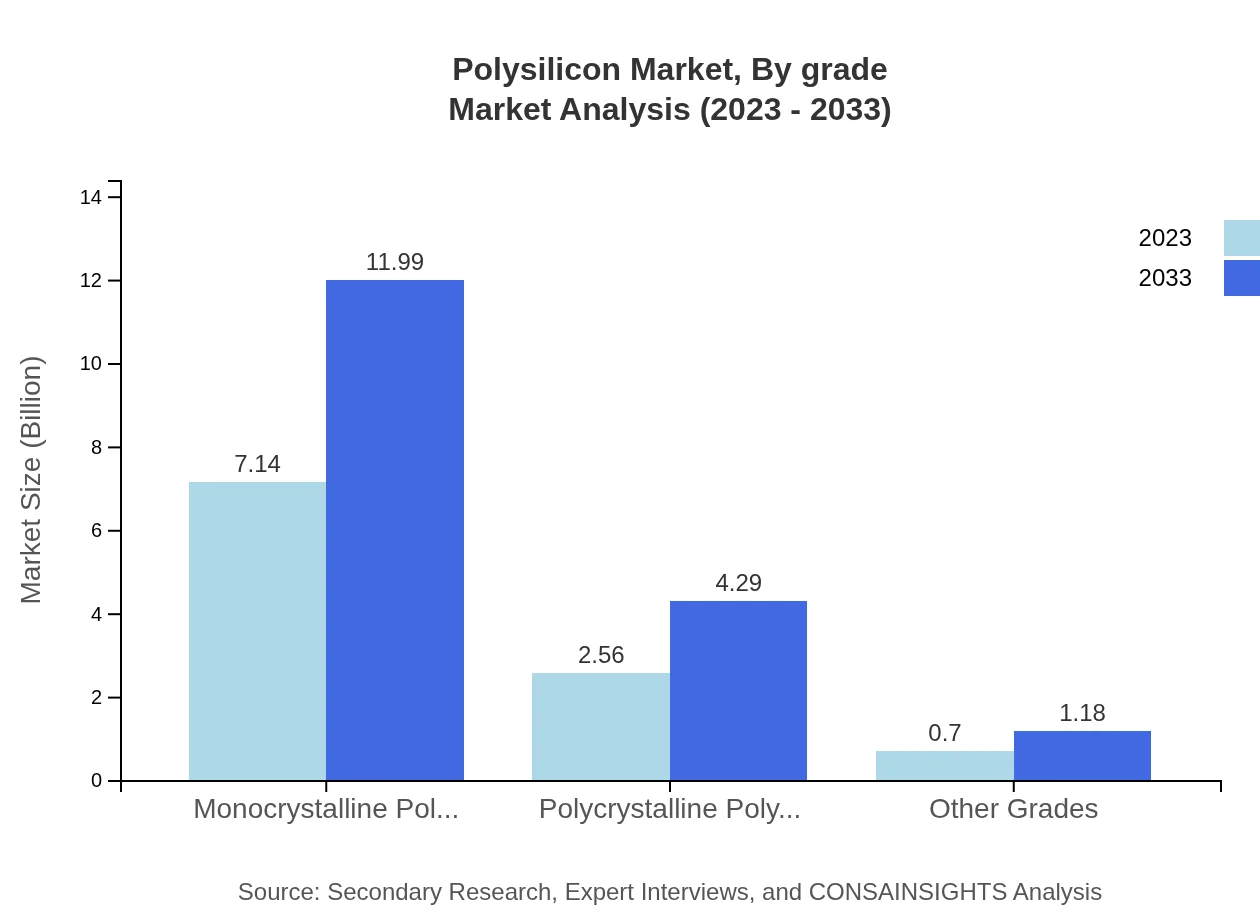

Polysilicon Market Analysis By Grade

The polysilicon market by grade shows that Monocrystalline polysilicon dominates, with a market size of $7.14 billion in 2023, expected to reach $11.99 billion by 2033. This segment represents 68.66% of the market share throughout the forecast period. In contrast, Polycrystalline polysilicon, valued at $2.56 billion in 2023, is projected to rise to $4.29 billion by 2033, holding a share of 24.59%.

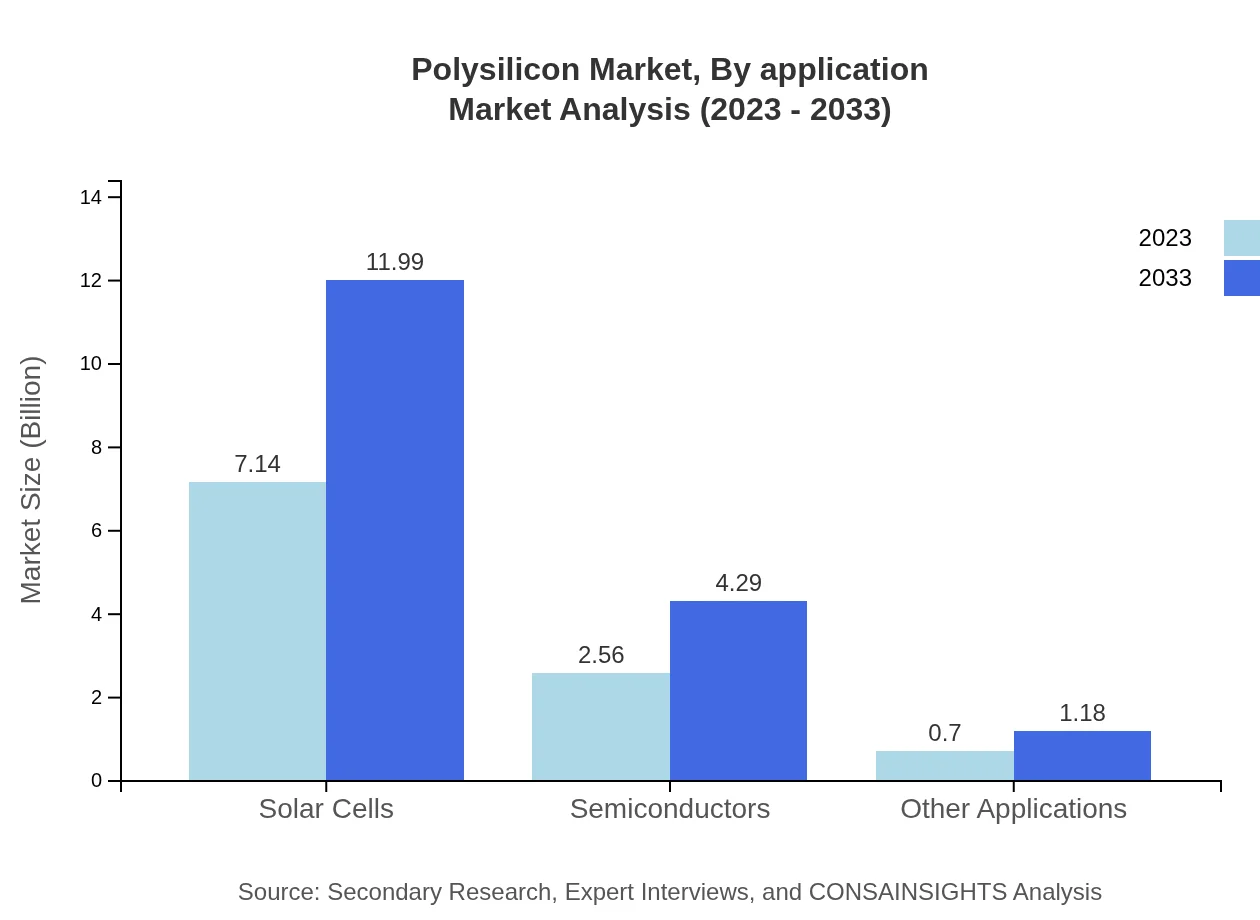

Polysilicon Market Analysis By Application

The application of polysilicon predominantly lies within the solar industry, comprising 68.66% of the market share. The solar cells segment alone is anticipated to grow from $7.14 billion in 2023 to approximately $11.99 billion by 2033. Other applications like electronics manufacturing and semiconductors also represent significant shares of 24.59% and are expected to grow steadily in tandem with advances in technology.

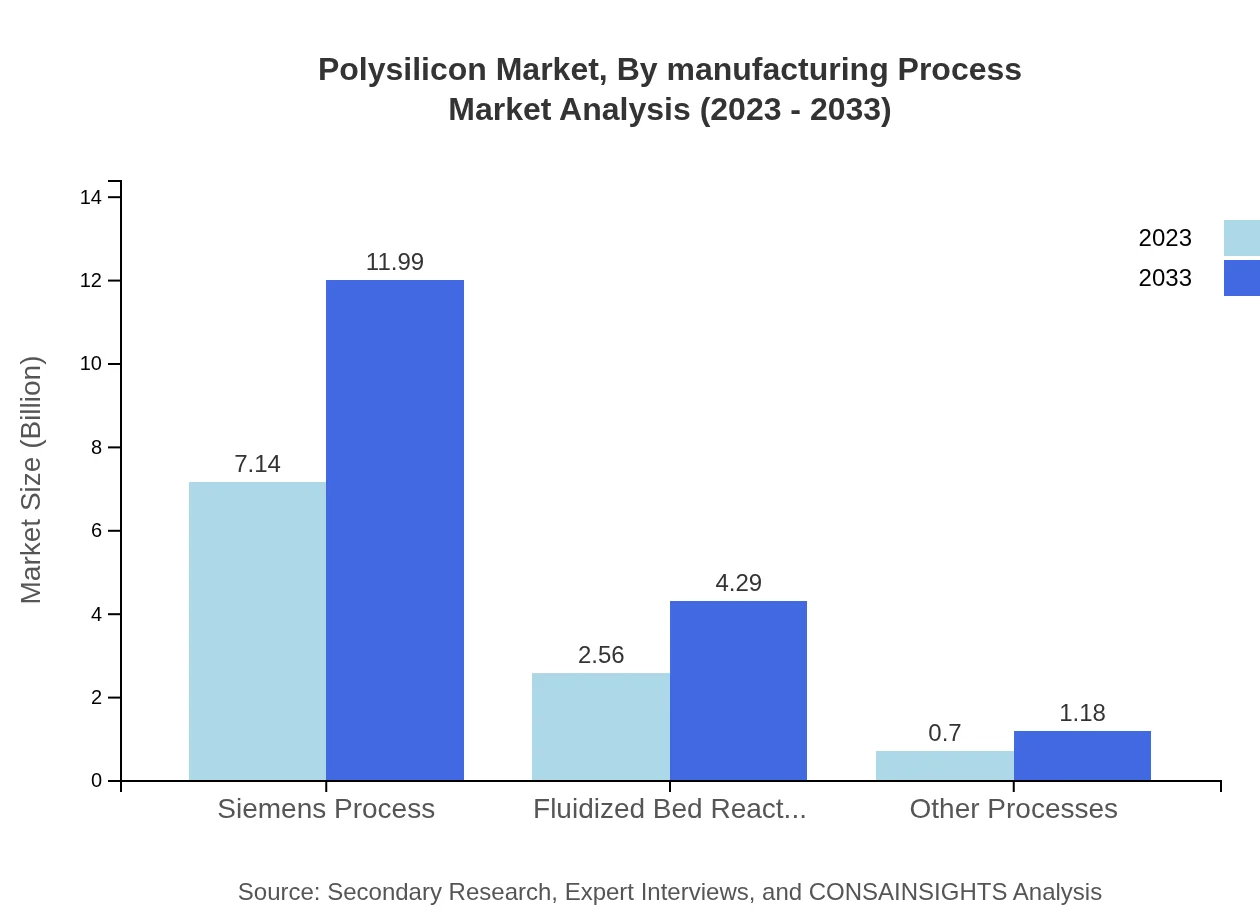

Polysilicon Market Analysis By Manufacturing Process

Manufacturing processes significantly impact the quality and pricing of polysilicon. The Siemens Process, accounting for 68.66% of the market share, is deemed the most established and effective technique for high purity. Newer methods, such as Fluidized Bed Reactor, are becoming more popular, enabling efficiency improvements but are currently at a smaller scale.

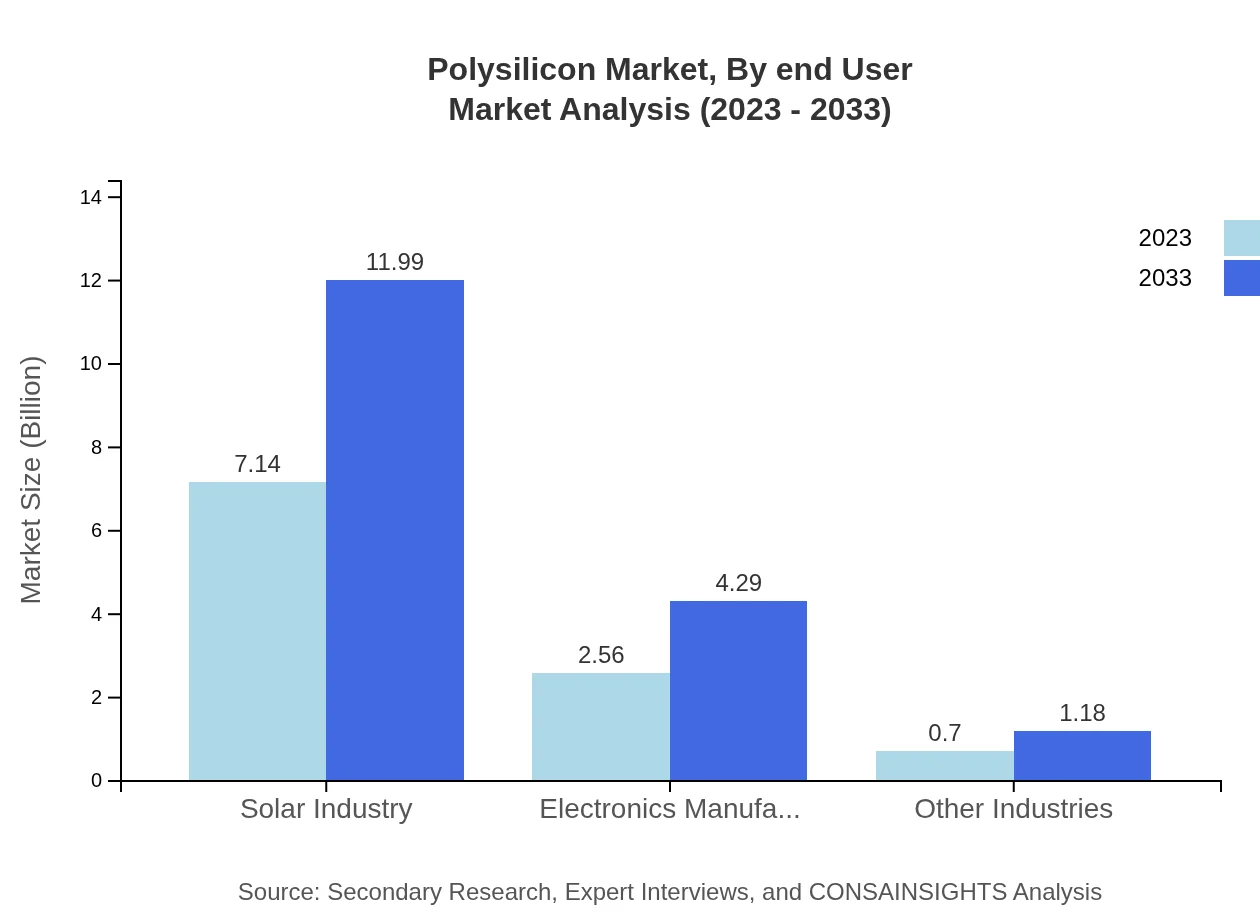

Polysilicon Market Analysis By End User

The primary end-user of polysilicon is the solar energy sector, which is expected to maintain a major focus resulting in a market size of $7.14 billion in 2023, surging to $11.99 billion by 2033. Other significant end-users include electronics manufacturing and semiconductors, which are increasingly integrating polysilicon into their manufacturing processes.

Polysilicon Market Analysis By Region

Regional analysis highlights that Asia Pacific leads with a market share of 45.95%, followed by North America at 20.05%, Europe at 10.06%, and South America at 11.85%. Each region shows distinct growth patterns influenced by local energy policies, market demand, and investment in renewable energy technologies.

Polysilicon Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Polysilicon Industry

Wacker Chemie AG:

A leading global supplier of polysilicon, Wacker Chemie is recognized for high-quality production techniques and extensive R&D efforts aimed at improving polysilicon production efficiency.GCL-Poly Energy Holdings Limited:

One of the largest producers in the world, GCL-Poly is instrumental in advancing polysilicon manufacturing technologies and expanding their presence in international markets.OCI Company Ltd.:

OCI specializes in producing solar-grade polysilicon and contributes significantly to the market through technological innovations and strategic partnerships.REC Silicon:

With a focus on sustainability, REC is a key player in polysilicon production and is known for its efforts to integrate cleaner processes in its manufacturing.We're grateful to work with incredible clients.

FAQs

What is the market size of polysilicon?

The global polysilicon market is valued at approximately $10.4 billion in 2023 and is expected to grow at a CAGR of 5.2% over the next decade, potentially reaching significant growth in 2033.

What are the key market players or companies in the polysilicon industry?

Key players in the polysilicon market include major manufacturers like Wacker Chemie AG, GCL-Poly Energy Holdings, and OCI Company. These companies dominate the market through innovative processes, sustainable practices, and extensive distribution networks.

What are the primary factors driving the growth in the polysilicon industry?

The growth in the polysilicon industry is driven by increasing demand for solar energy, governmental support for renewable energy projects, advancements in production technology, and the growing electronics market requiring high-purity silicon.

Which region is the fastest Growing in the polysilicon market?

The Asia-Pacific region is the fastest-growing market for polysilicon, projected to expand from $2.25 billion in 2023 to $3.77 billion by 2033, driven by rising solar power deployment across countries like China and India.

Does ConsaInsights provide customized market report data for the polysilicon industry?

Yes, ConsaInsights offers tailored market report data for the polysilicon industry, allowing clients to access specific insights and analytics that meet their unique business needs and objectives.

What deliverables can I expect from this polysilicon market research project?

Delivables from the polysilicon market research project include detailed market analysis, forecasts, competitive landscape assessment, regional insights, and segmented data reports that inform strategic decisions.

What are the market trends of polysilicon?

Current market trends in the polysilicon industry include an increased focus on sustainability, technological advancements in production processes, higher efficiency solar panels, and a shift towards more renewable-centric energy policies.