Pregnancy Detection Kits Market Report

First published: 11 October 2024 | Last updated: 25 May 2026 | Report Code: pregnancy-detection-kits

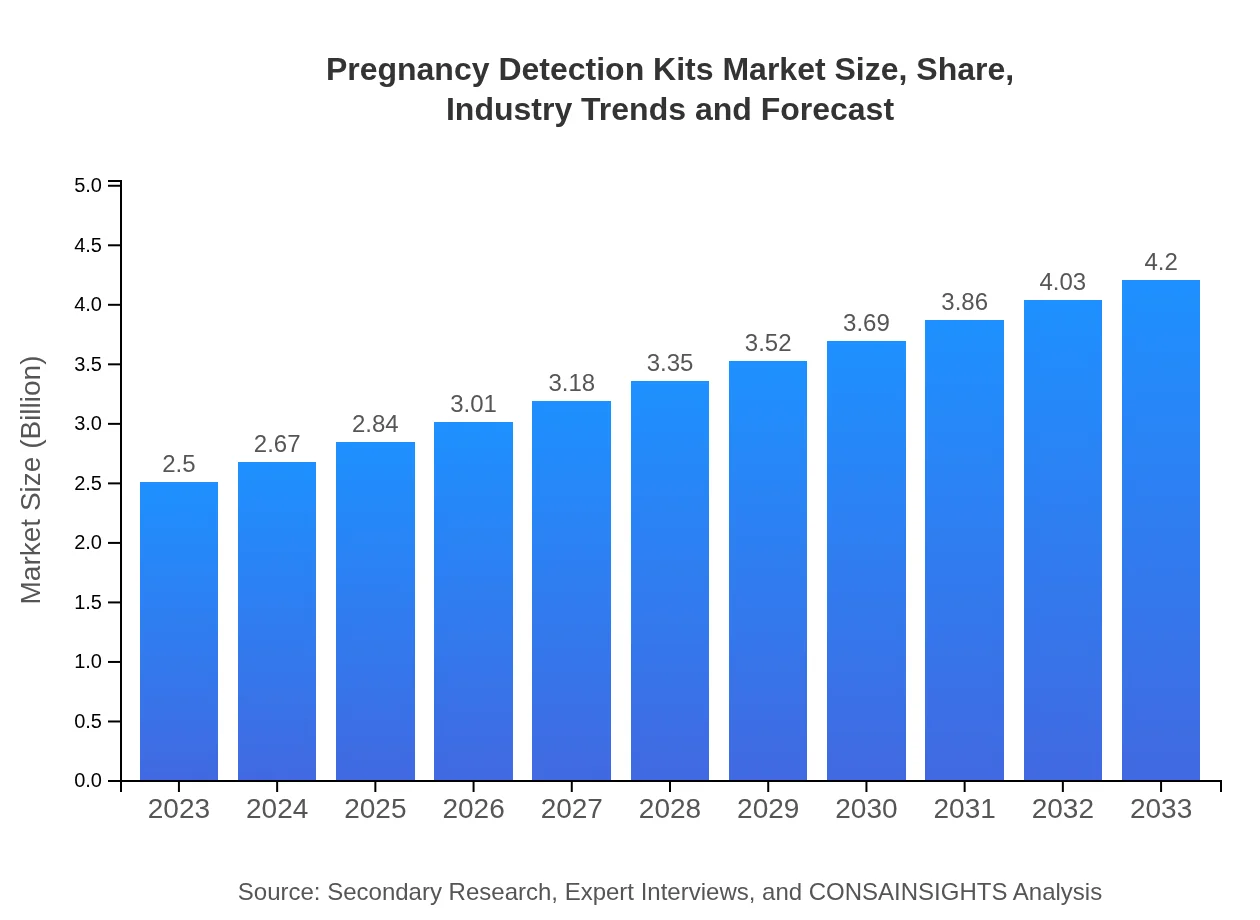

Pregnancy Detection Kits Market — USD 2.5 billion in 2023, Growing to USD 4.20B by 2033 at 5.2% CAGR

This report provides a comprehensive analysis of the Pregnancy Detection Kits market from 2023 to 2033, including market size, segmentation, regional insights, and future forecasts aimed at stakeholders for strategic decision-making.

Key Takeaways

- Global market value increases from $2.50 Billion in 2023 to $4.20 Billion in 2033 with a 5.2% CAGR over 2023 to 2033.

- North America is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- Europe grows from $0.76 Billion in 2023 to $1.27 Billion in 2033, while Asia Pacific reaches $0.79 Billion by 2033.

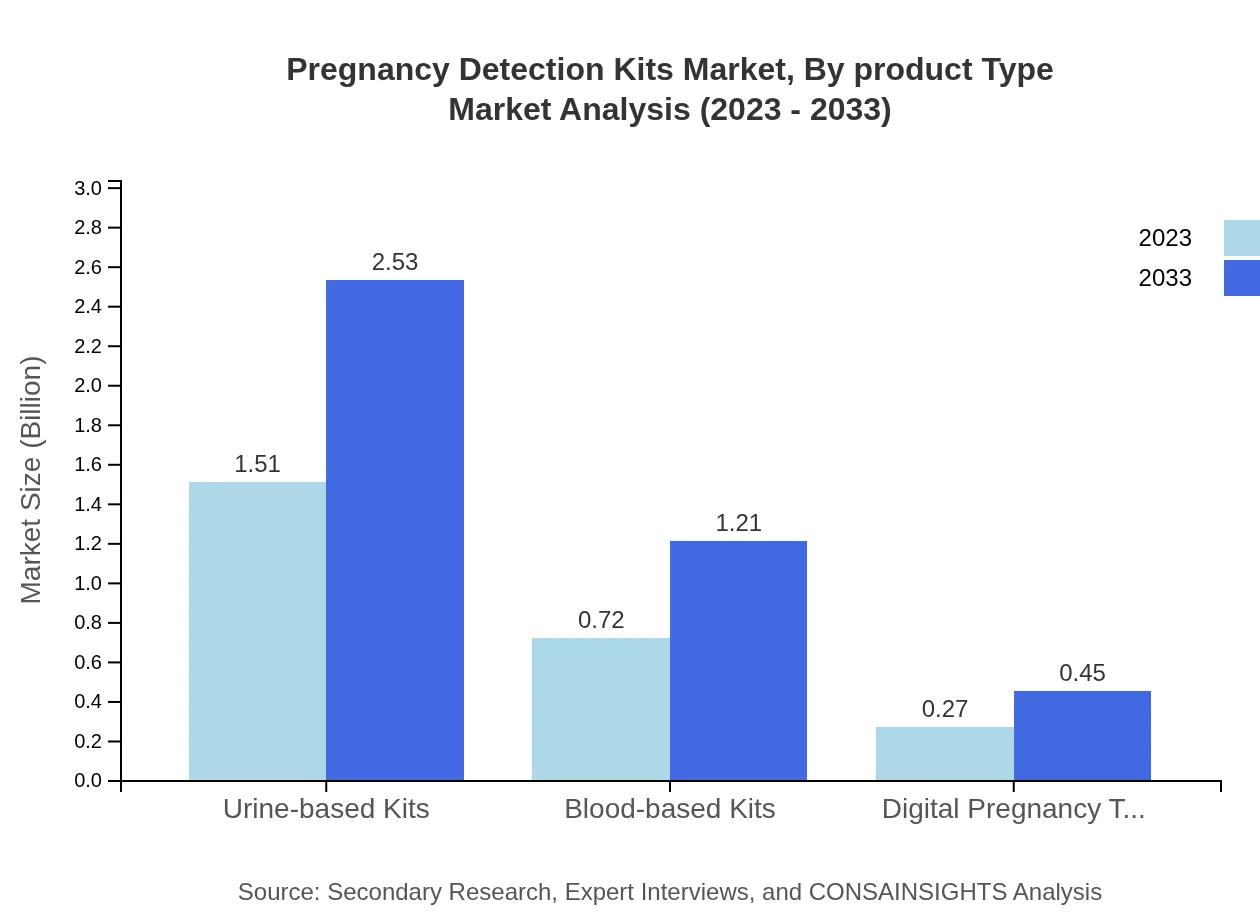

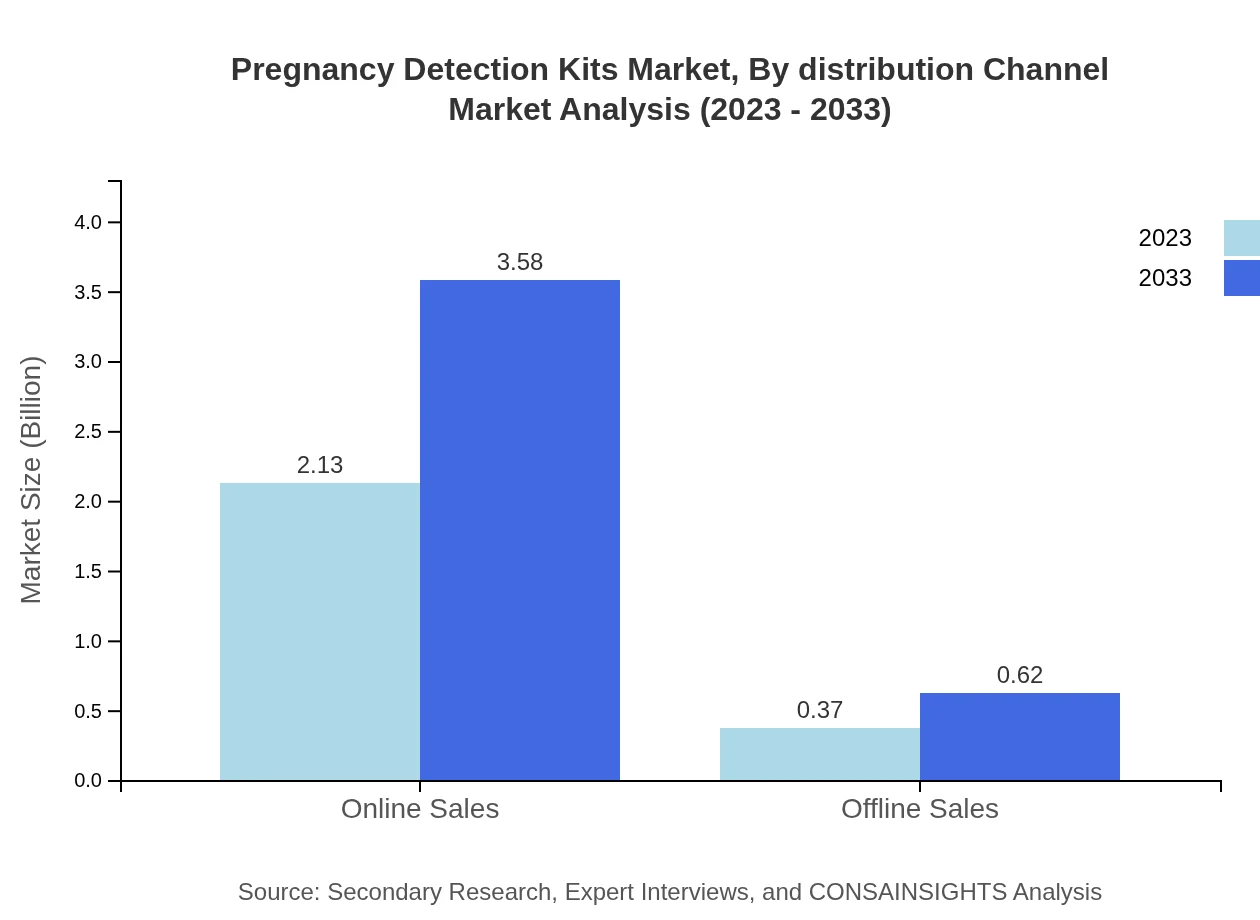

- Product mix includes urine-based, blood-based and digital kits; distribution shifts toward online and offline channels.

- Leading companies identified: Procter & Gamble, Church & Dwight, First Response, Clearblue, driving product innovation and distribution reach.

Pregnancy Detection Kits Market Report — Executive Summary

North America remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. This report examines the Pregnancy Detection Kits market, which moves from $2.50 Billion in 2023 to $4.20 Billion by 2033, reflecting a 5.2% CAGR across 2023 to 2033. Growth is driven by heightened reproductive health awareness, broader availability through online channels, and ongoing product innovation including digital and urine-based formats. Industry structure covers end users from individuals to clinical settings, technologies such as immunoassay and molecular biology, and distribution via online and offline sales. Regional footprints show North America as the largest market, with Europe and Asia Pacific making notable gains. The competitive landscape highlights established consumer health and diagnostic brands, and the analysis emphasizes regulatory quality, consumer preference for self-testing, and technology-led usability improvements as prevailing themes shaping strategic decisions through 2033.

Key Growth Drivers

- Rising consumer interest in self-testing and reproductive health awareness increasing demand for at-home pregnancy tests.

- Expansion of e-commerce platforms improving access and anonymity for purchasers, boosting online distribution channels.

- Technological advancements, including digital test formats and enhanced immunoassay sensitivity, improving accuracy and user experience.

- Sustained product portfolio investment by major manufacturers like Procter & Gamble and Church & Dwight driving market availability.

- Healthcare facility demand sustaining clinical-use kits alongside consumer-focused offerings, supporting diversified end-user growth.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $2.50 Billion |

| CAGR (2023-2033) | 5.2% |

| 2033 Market Size | $4.20 Billion |

| Top Companies | Procter & Gamble, Church & Dwight, First Response, Clearblue |

| Published Date | 11 October 2024 |

| Last Modified Date | 25 May 2026 |

Pregnancy Detection Kits Market Overview

Customize Pregnancy Detection Kits Market Report market research report

- ✔ Get in-depth analysis of Pregnancy Detection Kits market size, growth, and forecasts.

- ✔ Understand Pregnancy Detection Kits's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Pregnancy Detection Kits

What is the Market Size & CAGR of Pregnancy Detection Kits Market Report market in 2023?

Pregnancy Detection Kits Industry Analysis

Pregnancy Detection Kits Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Pregnancy Detection Kits Market Report Market Analysis Report by Region

Europe Pregnancy Detection Kits Market Report:

Europe grows from $0.76 Billion in 2023 to $1.27 Billion in 2033. Regional gains are driven by growing reproductive health awareness, availability of digital and urine-based kits, and increasing online purchases.Asia Pacific Pregnancy Detection Kits Market Report:

Asia Pacific grows from $0.47 Billion in 2023 to $0.79 Billion in 2033. Market progression is linked to improving access to diagnostic products, rising self-testing acceptance, and expanding e-commerce distribution.North America Pregnancy Detection Kits Market Report:

North America is largest regional market, rising from $0.9 Billion in 2023 to $1.5 Billion in 2033. Growth reflects high consumer adoption of at-home tests, established retail and online channels, and sustained manufacturer presence.South America Pregnancy Detection Kits Market Report:

Latin America grows from $0.09 Billion in 2023 to $0.15 Billion in 2033. Uptake is influenced by broader product availability and gradual increases in consumer preference for home testing solutions.Middle East & Africa Pregnancy Detection Kits Market Report:

Middle East and Africa grows from $0.28 Billion in 2023 to $0.47 Billion in 2033. Development reflects growing awareness of reproductive health and expanded access through both online and offline channels.Tell us your focus area and get a customized research report.

Research Methodology

Pregnancy Detection Kits Market Analysis By Product Type

The Pregnancy Detection Kits market is primarily categorized into urine-based kits, blood-based kits, and digital pregnancy tests. Urine-based kits account for the largest share at approximately 60.38% in 2023 and are projected to reach a similar share by 2033. Blood-based kits, though growing at about 28.81%, are less favored due to their complexity. Digital pregnancy tests are emerging as a significant segment, currently holding a 10.81% market share. By 2033, digital kits are expected to continue gaining traction, reflecting advances in technology.

Pregnancy Detection Kits Market Analysis By Distribution Channel

The distribution of Pregnancy Detection Kits is divided into online and offline sales, with online sales dominating at around 85.26% in 2023. This channel is projected to grow to 85.26% by 2033, driven by consumer preference for convenience. Offline channels, although smaller at 14.74%, are important for healthcare facilities and retail pharmacy operations. The transition towards online shopping continues to reshape the landscape of this market, pushing for retailers to enhance their online presence.

Pregnancy Detection Kits Market Analysis By End User

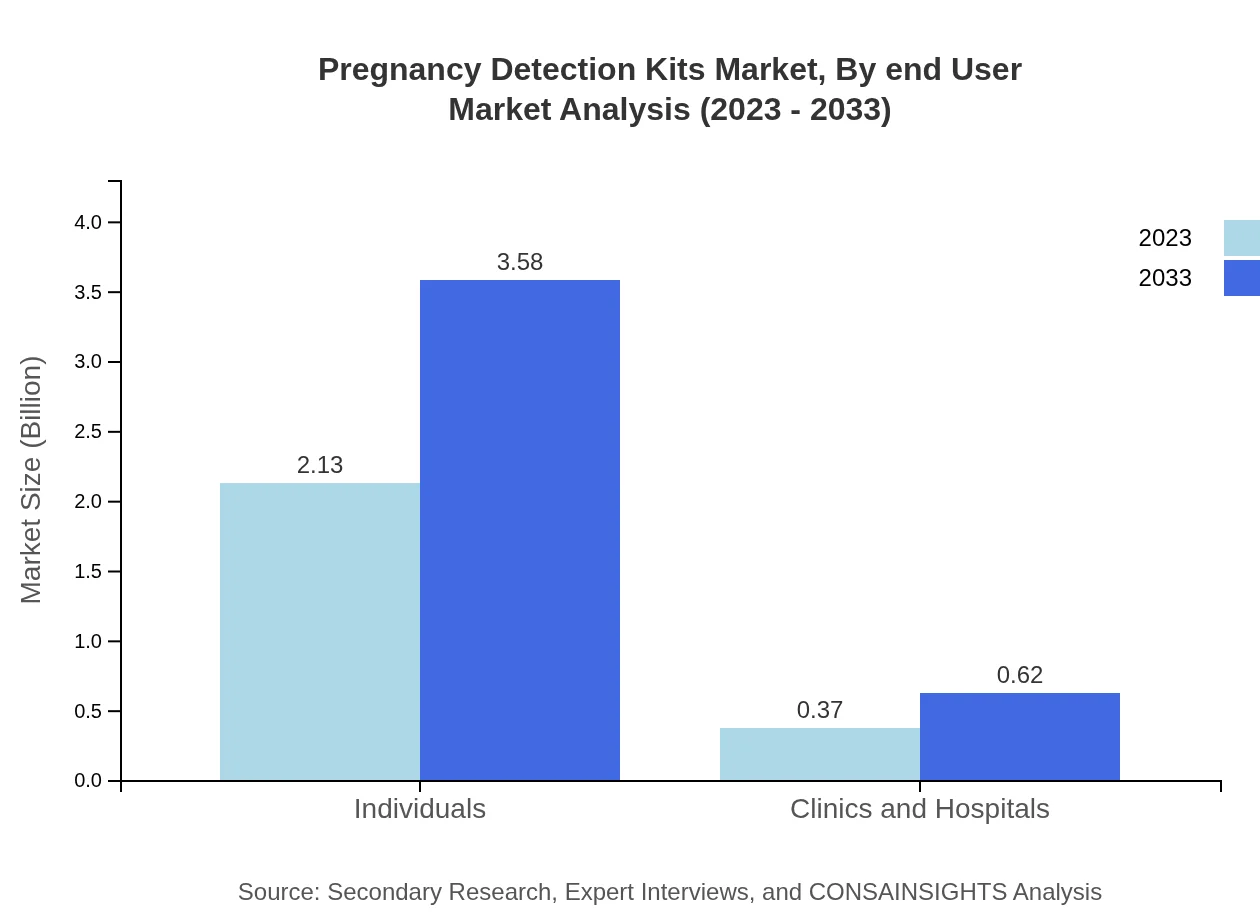

End users of Pregnancy Detection Kits include individuals, clinics, and hospitals. Individuals represent the largest share of the market at approximately 85.26% of the total market in 2023. This share is expected to remain constant as self-testing becomes more prevalent. Clinics and hospitals account for about 14.74%, reflecting their role in professional medical settings.

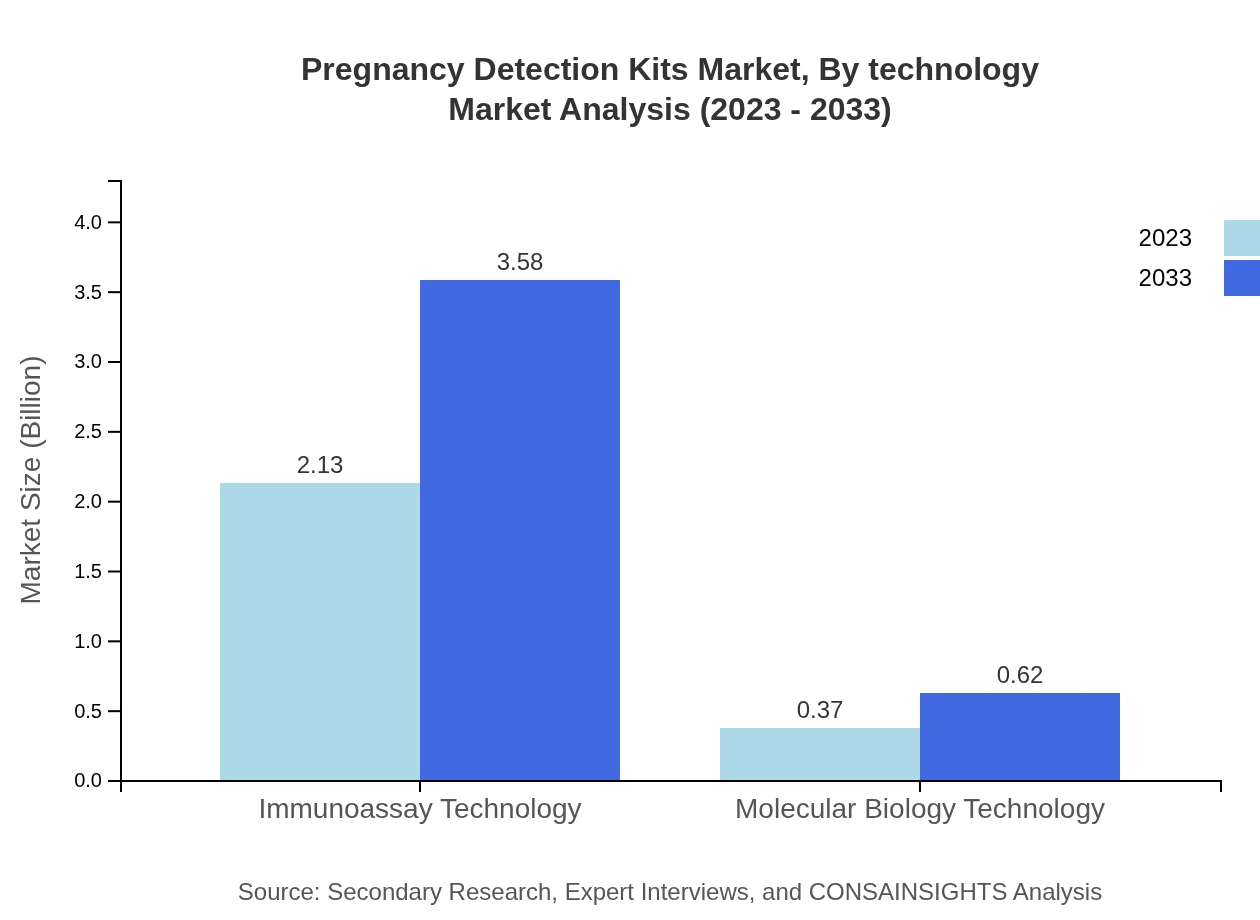

Pregnancy Detection Kits Market Analysis By Technology

The technologies employed in the Pregnancy Detection Kits market include immunoassay technology and molecular biology technology. Immunoassay technology holds the dominant share at about 85.26% due to its reliability and accuracy. Molecular biology technology represents a smaller segment at 14.74%, but it is gaining attention for its precision and effectiveness in early detection.

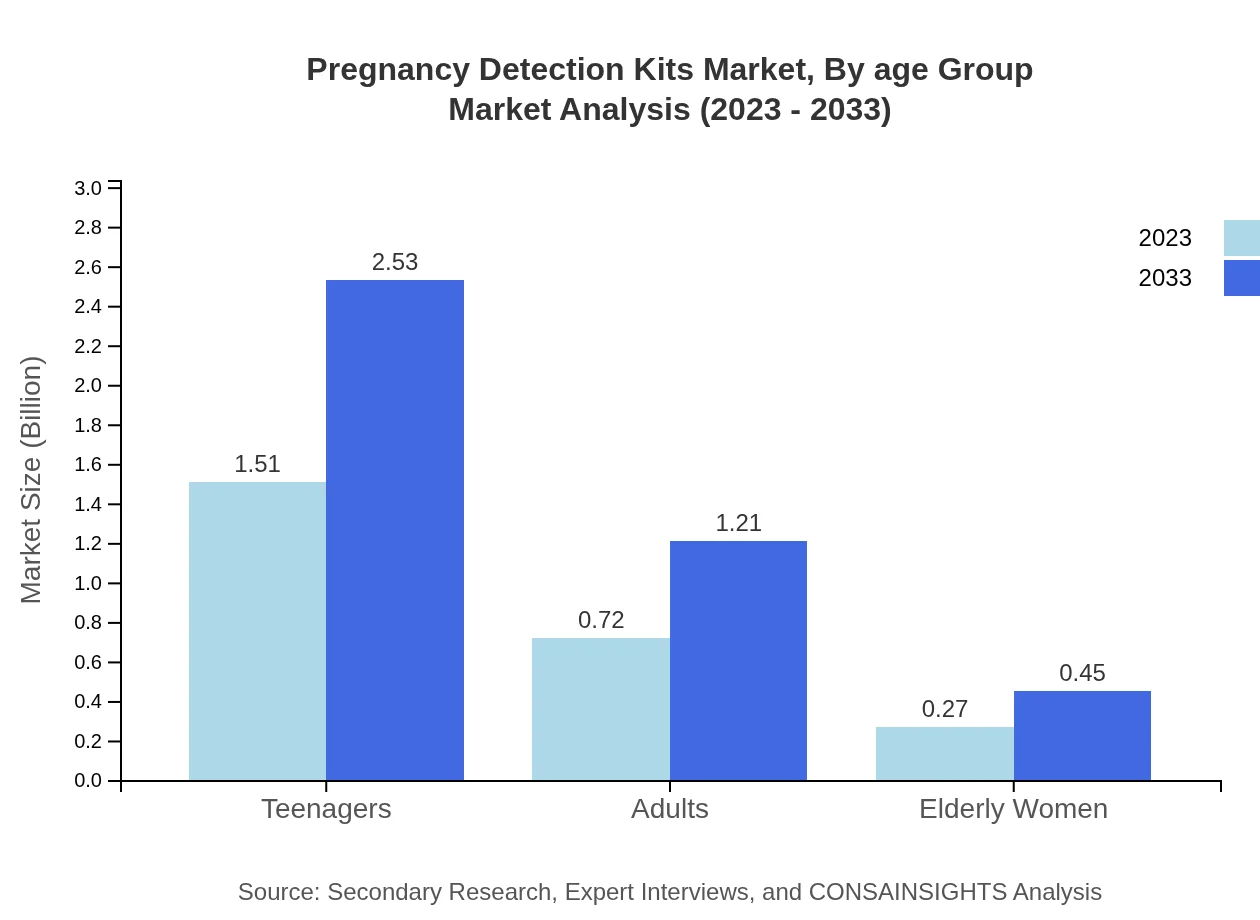

Pregnancy Detection Kits Market Analysis By Age Group

The age group segmentation includes teenagers, adults, and elderly women. Teenagers constitute a significant portion with approximately 60.38% market share due to a focus on early pregnancy awareness. Adults represent 28.81% of the market while elderly women account for 10.81%. Awareness and education on reproductive health are paramount in driving market interest across all age groups.

Pregnancy Detection Kits Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Pregnancy Detection Kits Industry

Procter & Gamble:

P&G is a leading player in the market, known for its reliable pregnancy testing brands and extensive distribution network.Church & Dwight:

The maker of the e.p.t pregnancy test, Church & Dwight has a strong presence in the retail segment and focuses on innovation in testing technology.First Response:

First Response specializes in innovative products designed for early pregnancy detection, appealing to a broad range of consumers.Clearblue:

Clearblue is recognized for its digital pregnancy tests and is a pioneer in the industry, known for its accuracy and innovation.We're grateful to work with incredible clients.

FAQs

What is the market size of the Pregnancy Detection Kits market in 2023?

The market size in 2023 is $2.50 Billion, reflecting aggregated global revenues for pregnancy detection products during that year.

How big will the market be in 2033?

By 2033 the market is projected to reach $4.20 Billion according to the provided forecast figures for the period.

What is CAGR for the forecast period?

The compound annual growth rate for 2023 to 2033 is 5.2%, representing the average annual expansion over that decade.

Is there a single fastest Growing region in the Pregnancy Detection Kits Market Report market?

No single fastest-growing region is stated for the Pregnancy Detection Kits Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Which product types are included in this market?

The market encompasses urine-based kits, blood-based kits, and digital pregnancy test kits as principal product categories.

Who are the top companies in this market?

Top companies listed include Procter & Gamble, Church & Dwight, First Response, and Clearblue, noted for broad distribution and product lines.

How are distribution channels evolving?

Distribution balances online sales and offline sales, with e-commerce expanding access and traditional retail and clinical channels remaining important.

What end User segments does the market cover?

End users include individual consumers and clinical settings such as clinics and hospitals, supporting both self-testing and professional diagnostics.