Semiconductor Packaging Market Report

First published: 19 September 2024 | Last updated: 31 January 2026 | Report Code: semiconductor-packaging

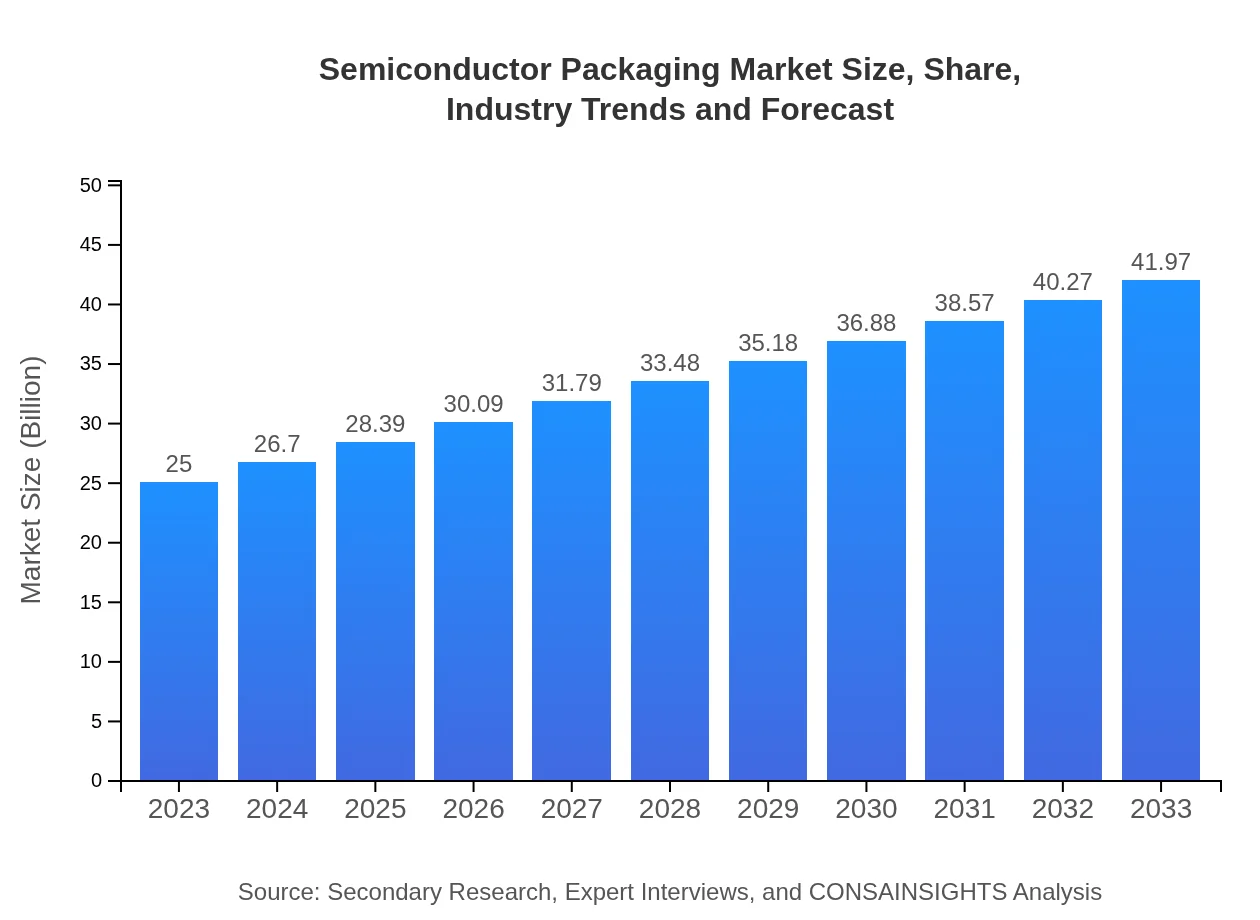

Semiconductor Packaging Market — USD 25 billion in 2023, Growing to USD 41.97B by 2033 at 5.2% CAGR

This report provides a comprehensive analysis of the semiconductor packaging market from 2023 to 2033, covering market trends, size, segmentation, regional insights, technology advancements, and competitive landscape, aimed at aiding stakeholders in strategic planning.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $25.00 Billion |

| CAGR (2023-2033) | 5.2% |

| 2033 Market Size | $41.97 Billion |

| Top Companies | Intel Corporation, TSMC, ASE Technology Holding Co. |

| Published Date | 19 September 2024 |

| Last Modified Date | 31 January 2026 |

Semiconductor Packaging Market Overview

Customize Semiconductor Packaging Market Report market research report

- ✔ Get in-depth analysis of Semiconductor Packaging market size, growth, and forecasts.

- ✔ Understand Semiconductor Packaging's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Semiconductor Packaging

What is the Market Size & CAGR of Semiconductor Packaging market in 2023?

Semiconductor Packaging Industry Analysis

Semiconductor Packaging Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Semiconductor Packaging Market Analysis Report by Region

Europe Semiconductor Packaging Market Report:

Europe’s semiconductor packaging market is anticipated to grow from 7.11 billion USD in 2023 to 11.94 billion USD by 2033, supported by increased investment in research and development and the introduction of advanced packaging technologies in response to growing automaker demands.Asia Pacific Semiconductor Packaging Market Report:

The Asia Pacific region dominates the semiconductor packaging market with a valuation of 4.92 billion USD in 2023, and it is expected to reach 8.27 billion USD by 2033. Key drivers include robust consumer electronics demand, automotive industry growth, and the presence of major semiconductor manufacturers in countries like Japan and South Korea.North America Semiconductor Packaging Market Report:

North America accounts for a significant portion of the semiconductor packaging market, valued at 8.51 billion USD in 2023, expected to reach 14.29 billion USD by 2033. The region benefits from a strong presence of semiconductor companies and advancements in automotive electronics, driving demand for innovative packaging solutions.South America Semiconductor Packaging Market Report:

In South America, the semiconductor packaging market is valued at 1.91 billion USD in 2023, projected to grow to 3.20 billion USD by 2033. Growth is fuelled by increasing investments in technology and rising electronic manufacturing activities in Brazil and Argentina.Middle East & Africa Semiconductor Packaging Market Report:

The Middle East and Africa region's semiconductor packaging market is projected to increase from 2.54 billion USD in 2023 to 4.27 billion USD by 2033. Growth is influenced by rising electronics markets in South Africa and the increasing integration of technology in various sectors.Tell us your focus area and get a customized research report.

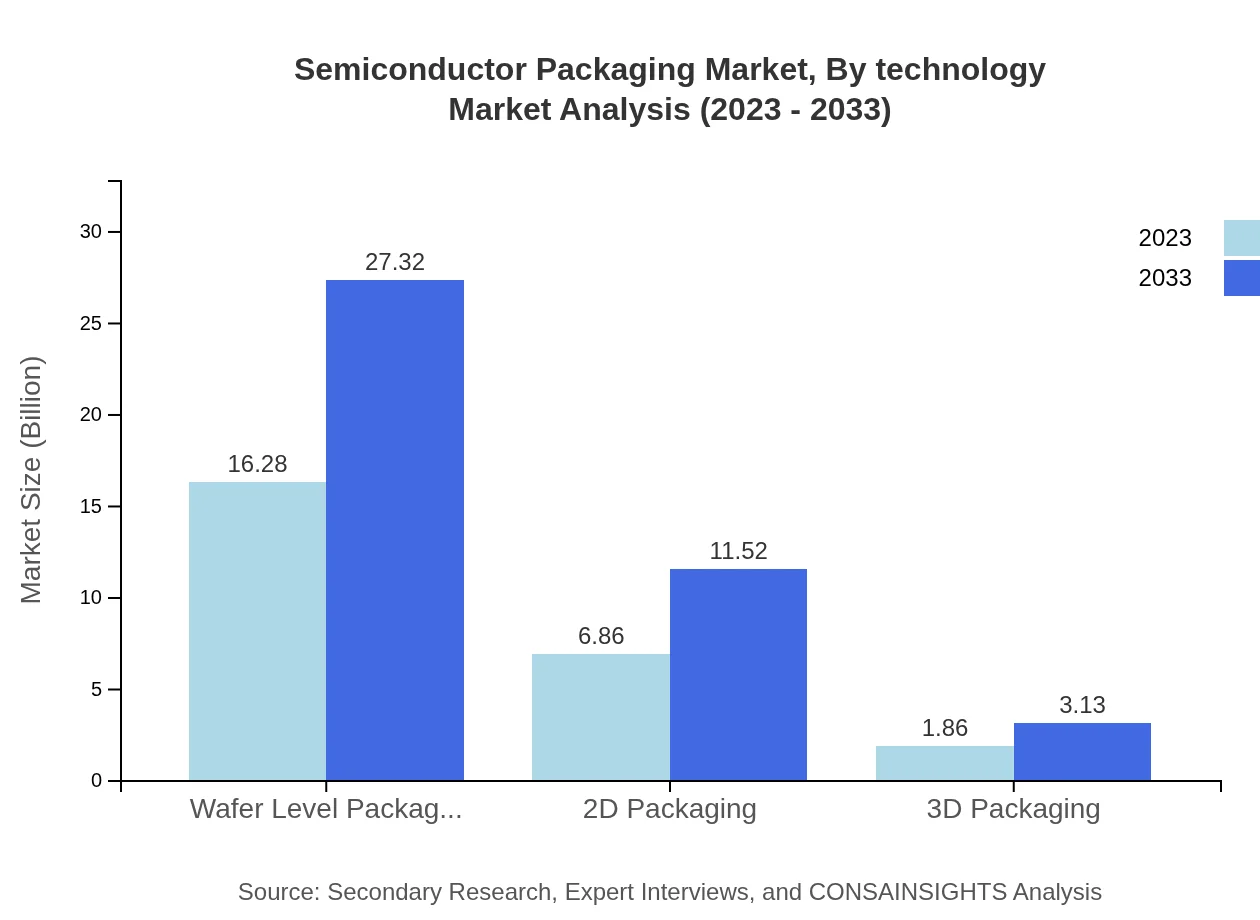

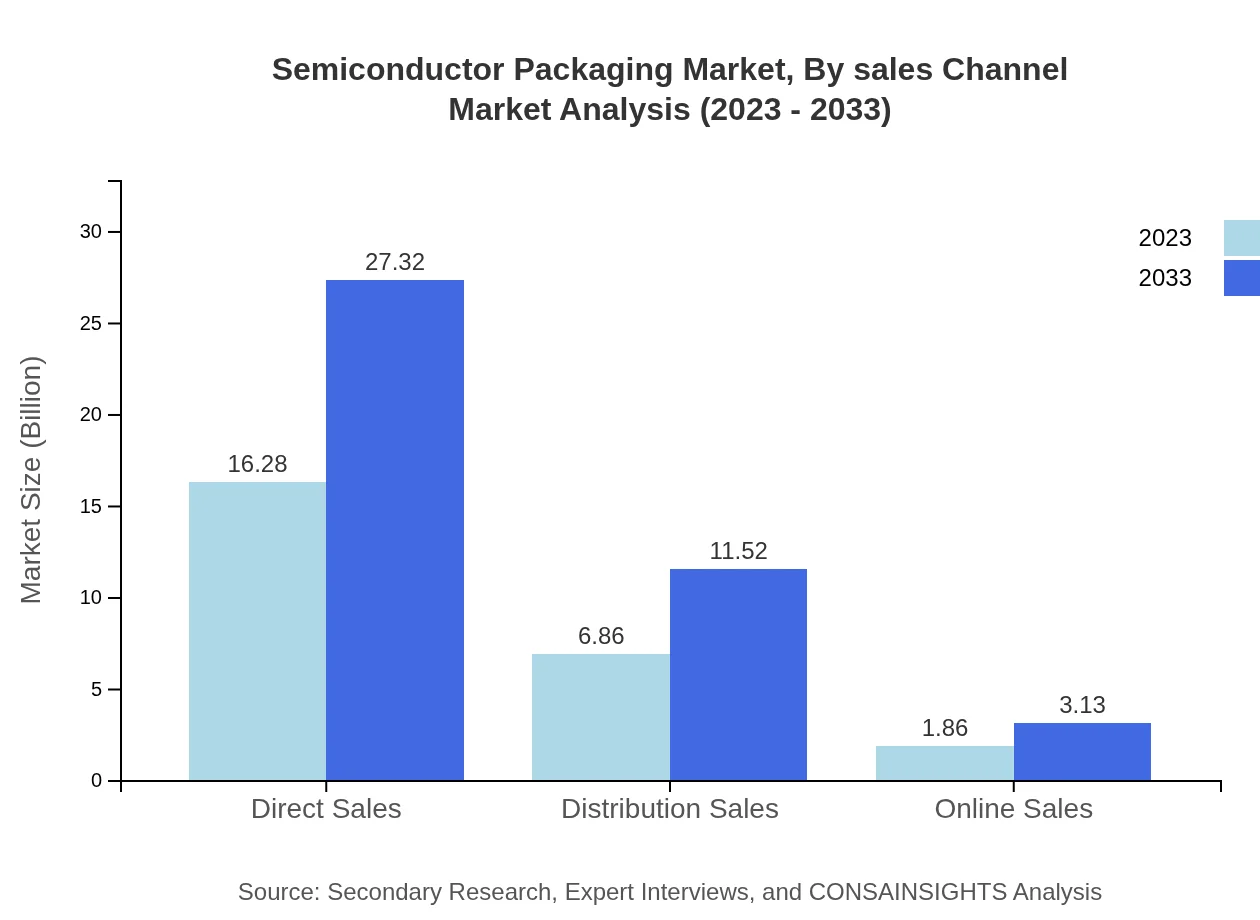

Semiconductor Packaging Market Analysis By Technology

The market is significantly driven by Wafer Level Packaging, which is valued at 16.28 billion USD in 2023 and expected to reach 27.32 billion USD by 2033. Other key technologies include 2D and 3D packaging, with 2D packaging valued at 6.86 billion USD and 3D packaging at 1.86 billion USD in 2023.

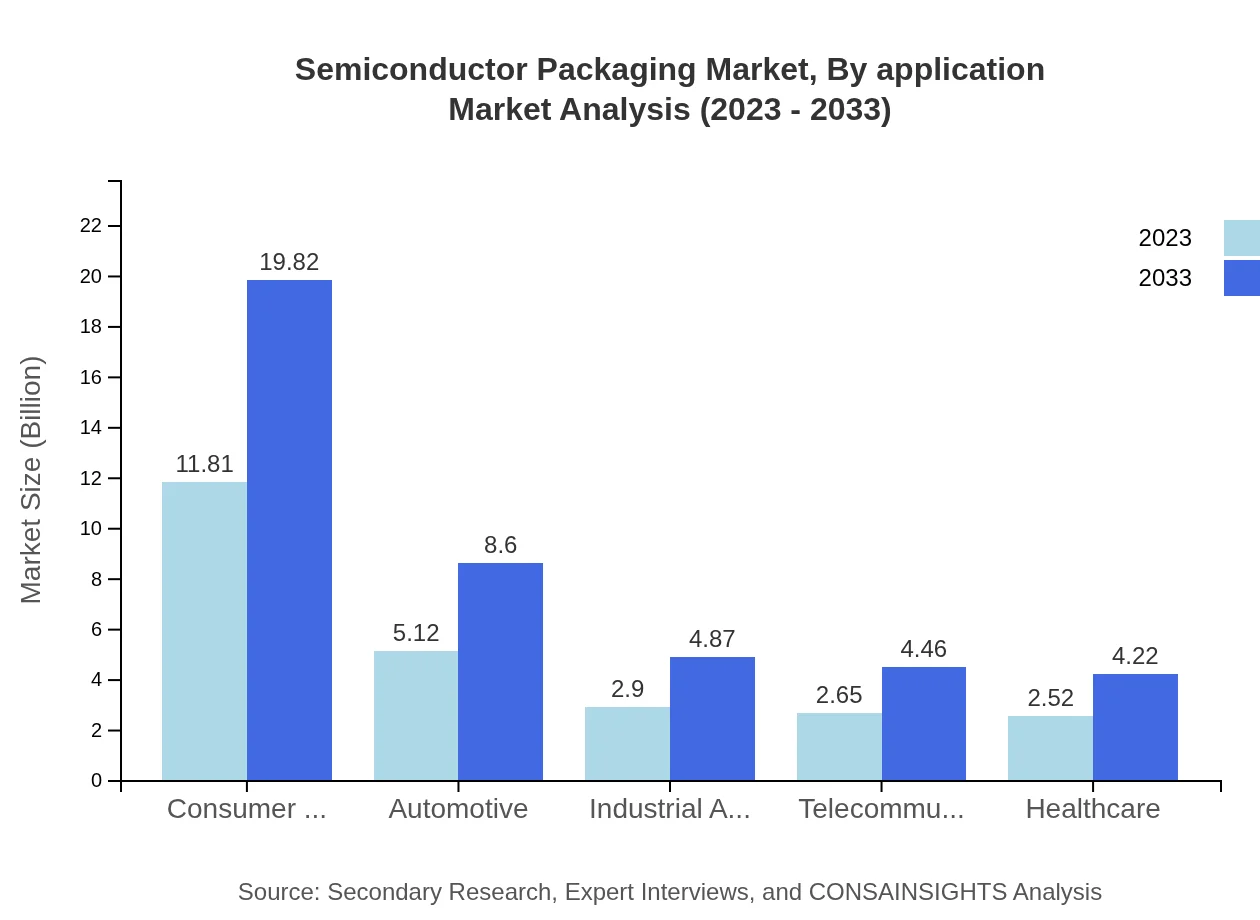

Semiconductor Packaging Market Analysis By Application

Application-wise, consumer electronics dominate the market, valued at 11.81 billion USD in 2023, with forecasts to reach 19.82 billion USD by 2033. The automotive sector also shows robust growth, projected from 5.12 billion USD to 8.60 billion USD during the forecast period.

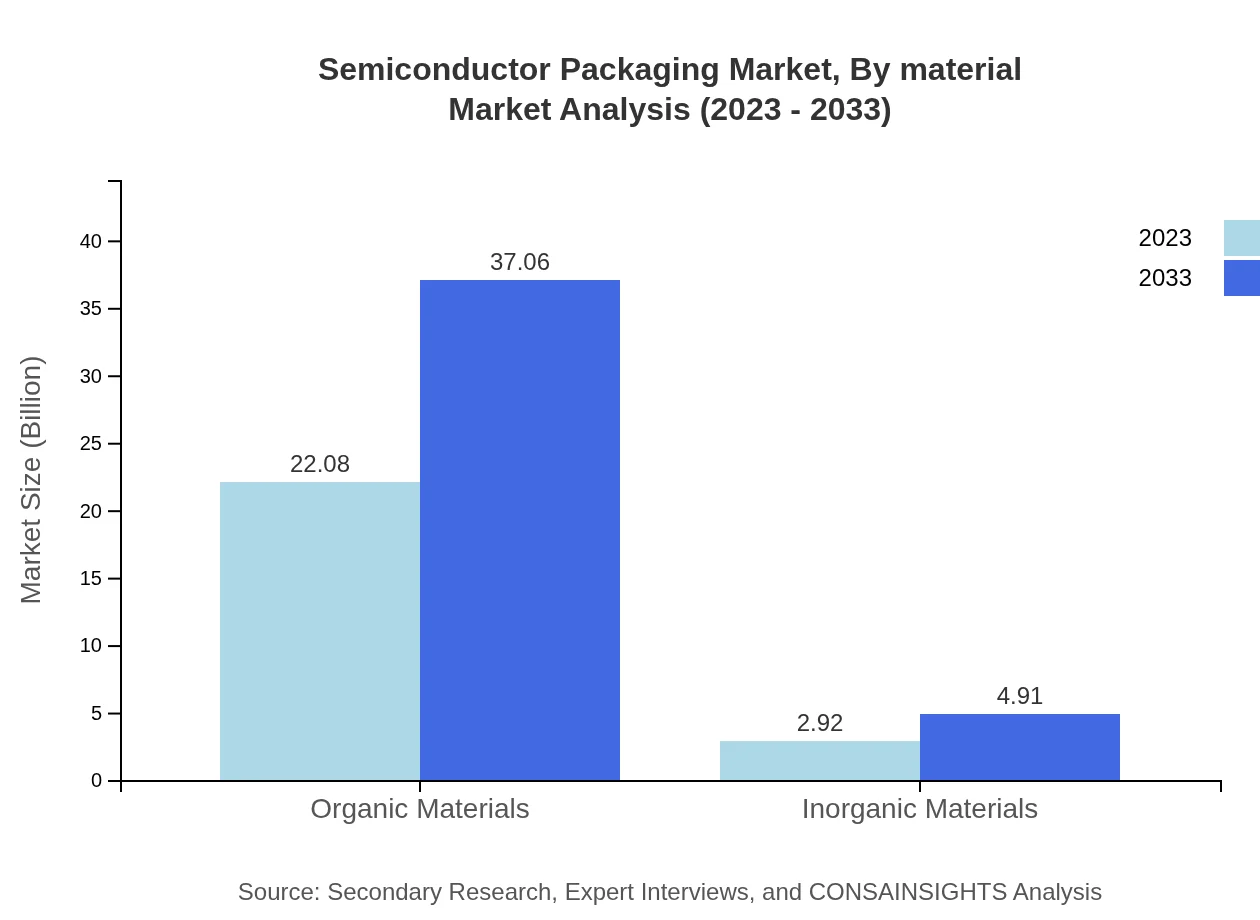

Semiconductor Packaging Market Analysis By Material

Materials used in semiconductor packaging significantly impact overall performance. Organic materials dominate with a market size of 22.08 billion USD in 2023 and expected growth to 37.06 billion USD by 2033, while inorganic materials represent a smaller segment yet show promising growth.

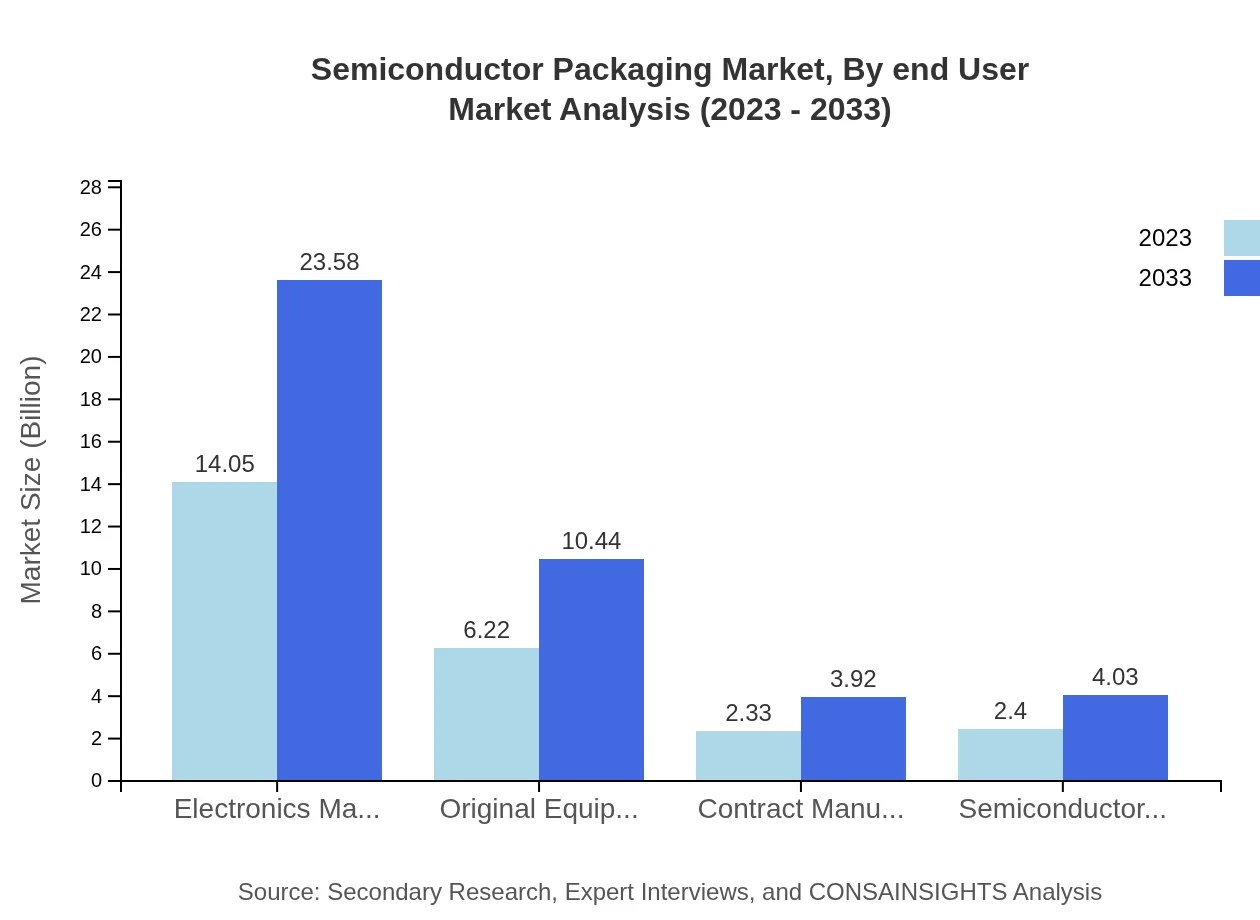

Semiconductor Packaging Market Analysis By End User

Electronics manufacturers lead the end-user segment, accounting for a market value of 14.05 billion USD in 2023, with further growth to 23.58 billion USD by 2033. The healthcare and telecommunications sectors also represent significant portions for the semiconductor packaging market.

Semiconductor Packaging Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Semiconductor Packaging Industry

Intel Corporation:

Intel is a leading semiconductor manufacturer known for its advanced packaging technologies and component innovations that empower computing and data-intensive applications.TSMC:

Taiwan Semiconductor Manufacturing Company is the world's largest dedicated independent semiconductor foundry, providing high-quality fabless manufacturing and packaging solutions.ASE Technology Holding Co.:

ASE is a global leader in semiconductor manufacturing services, specializing in packaging, testing, and AI solutions across various electronic applications.We're grateful to work with incredible clients.

FAQs

What is the market size of semiconductor Packaging?

The semiconductor packaging market is currently valued at $25 billion, with a projected growth rate (CAGR) of 5.2% expected over the next decade, indicating substantial expansion in this critical sector.

What are the key market players or companies in the semiconductor Packaging industry?

Major players in the semiconductor packaging industry include TSMC, ASE Group, Amkor Technology, and Infineon Technologies. These companies dominate through advanced technologies, extensive manufacturing capacities, and global distribution networks.

What are the primary factors driving the growth in the semiconductor Packaging industry?

Key factors driving growth in semiconductor packaging include rising demand for consumer electronics, advancements in packaging technologies, increasing integration of chips in automotive systems, and a shift towards 5G and IoT devices.

Which region is the fastest Growing in the semiconductor Packaging market?

The fastest-growing region in the semiconductor packaging market is North America, projected to grow from $8.51 billion in 2023 to $14.29 billion by 2033, followed closely by Europe and the Asia Pacific.

Does ConsaInsights provide customized market report data for the semiconductor Packaging industry?

Yes, ConsaInsights offers customized market report data tailored to specific user needs in the semiconductor packaging industry, enabling detailed insights aligned with strategic business objectives.

What deliverables can I expect from this semiconductor Packaging market research project?

Expect comprehensive deliverables, including market analysis reports, segment breakdowns, growth forecasts, competitive landscape assessments, and regional insights tailored to guide strategic decision-making.

What are the market trends of semiconductor Packaging?

Current trends include the rise of wafer-level packaging and 3D packaging technologies, increasing focus on sustainable practices, and the integration of packaging solutions for advanced applications in automotive and healthcare.