Silicon Photonics Market Report

First published: 17 September 2024 | Last updated: 31 January 2026 | Report Code: silicon-photonics

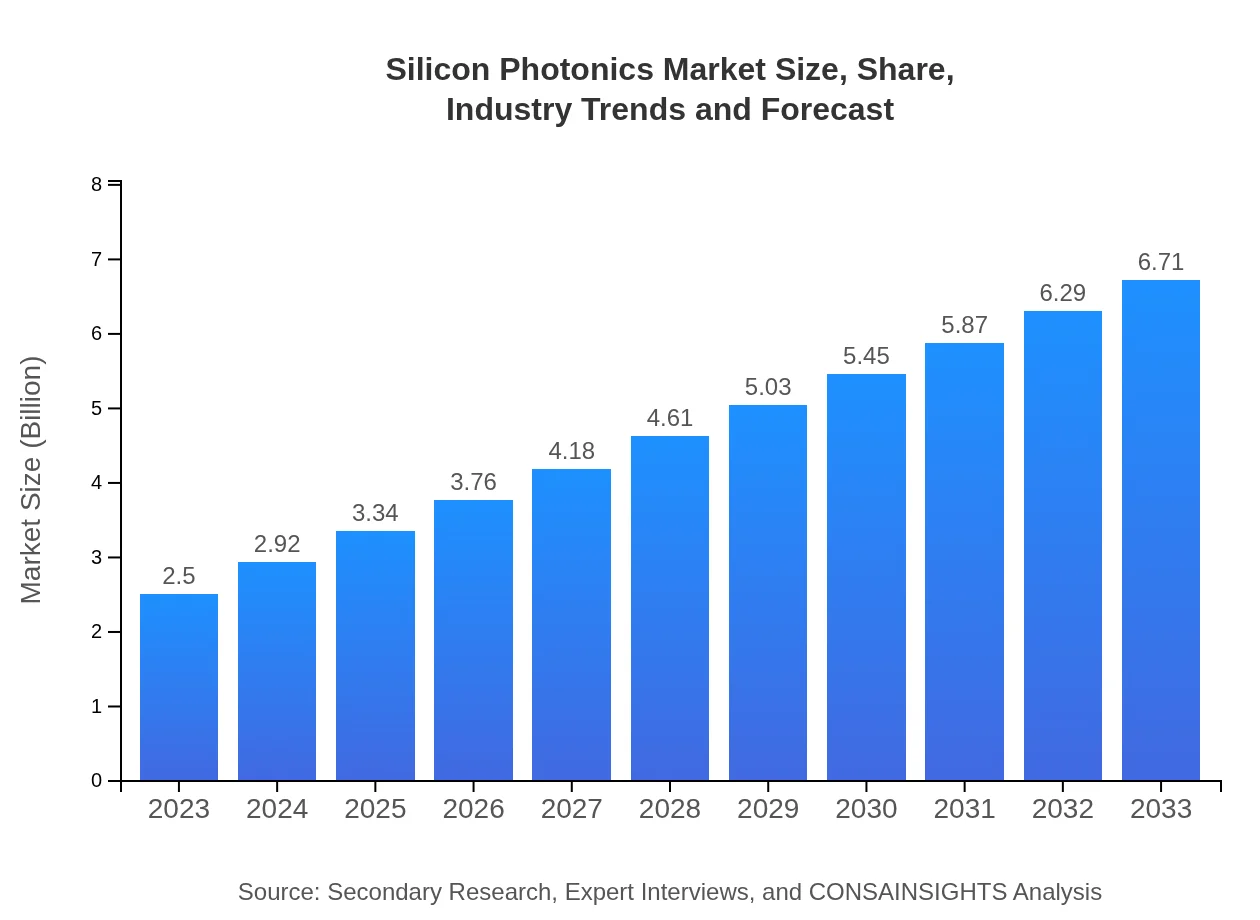

Silicon Photonics Market — USD 2.5 billion in 2023, Growing to USD 6.71B by 2033 at 10% CAGR

This report provides a comprehensive analysis of the Silicon Photonics market, detailing key trends, segmentation, and regional insights from 2023 to 2033. It includes market sizes, growth rates, and forecasts, along with profiles of leading companies in the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $2.50 Billion |

| CAGR (2023-2033) | 10% |

| 2033 Market Size | $6.71 Billion |

| Top Companies | Intel Corporation, Cisco Systems, Inc., IBM Corporation, Luxtera |

| Published Date | 17 September 2024 |

| Last Modified Date | 31 January 2026 |

Silicon Photonics Market Overview

Customize Silicon Photonics Market Report market research report

- ✔ Get in-depth analysis of Silicon Photonics market size, growth, and forecasts.

- ✔ Understand Silicon Photonics's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Silicon Photonics

What is the Market Size & CAGR of Silicon Photonics market in 2023?

Silicon Photonics Industry Analysis

Silicon Photonics Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Silicon Photonics Market Analysis Report by Region

Europe Silicon Photonics Market Report:

The European market is expected to grow from $0.61 billion in 2023 to $1.63 billion by 2033, fueled by increasing investments in optical communication systems and the rising importance of sustainability in technology.Asia Pacific Silicon Photonics Market Report:

In the Asia Pacific region, the Silicon Photonics market is anticipated to grow significantly, increasing from $0.53 billion in 2023 to $1.41 billion in 2033. The surge is driven by growing investments in data infrastructure and favorable government initiatives in technology adoption across countries like China, Japan, and India.North America Silicon Photonics Market Report:

North America dominates the Silicon Photonics market with a forecasted growth from $0.84 billion in 2023 to $2.26 billion in 2033. The region benefits from a strong presence of key players, robust research and development initiatives, and high demand for data-centric technologies.South America Silicon Photonics Market Report:

The South American market for Silicon Photonics is projected to expand from $0.23 billion in 2023 to $0.61 billion by 2033. Although still emerging, there is a heightened focus on developing telecommunications and data center infrastructures, which is set to enhance market growth in this region.Middle East & Africa Silicon Photonics Market Report:

The Middle East and Africa region anticipates growth from $0.30 billion in 2023 to $0.80 billion in 2033. With burgeoning interest in digital transformation across various sectors, the market is gearing up to tap into silicon photonics' potential to streamline operations and reduce costs.Tell us your focus area and get a customized research report.

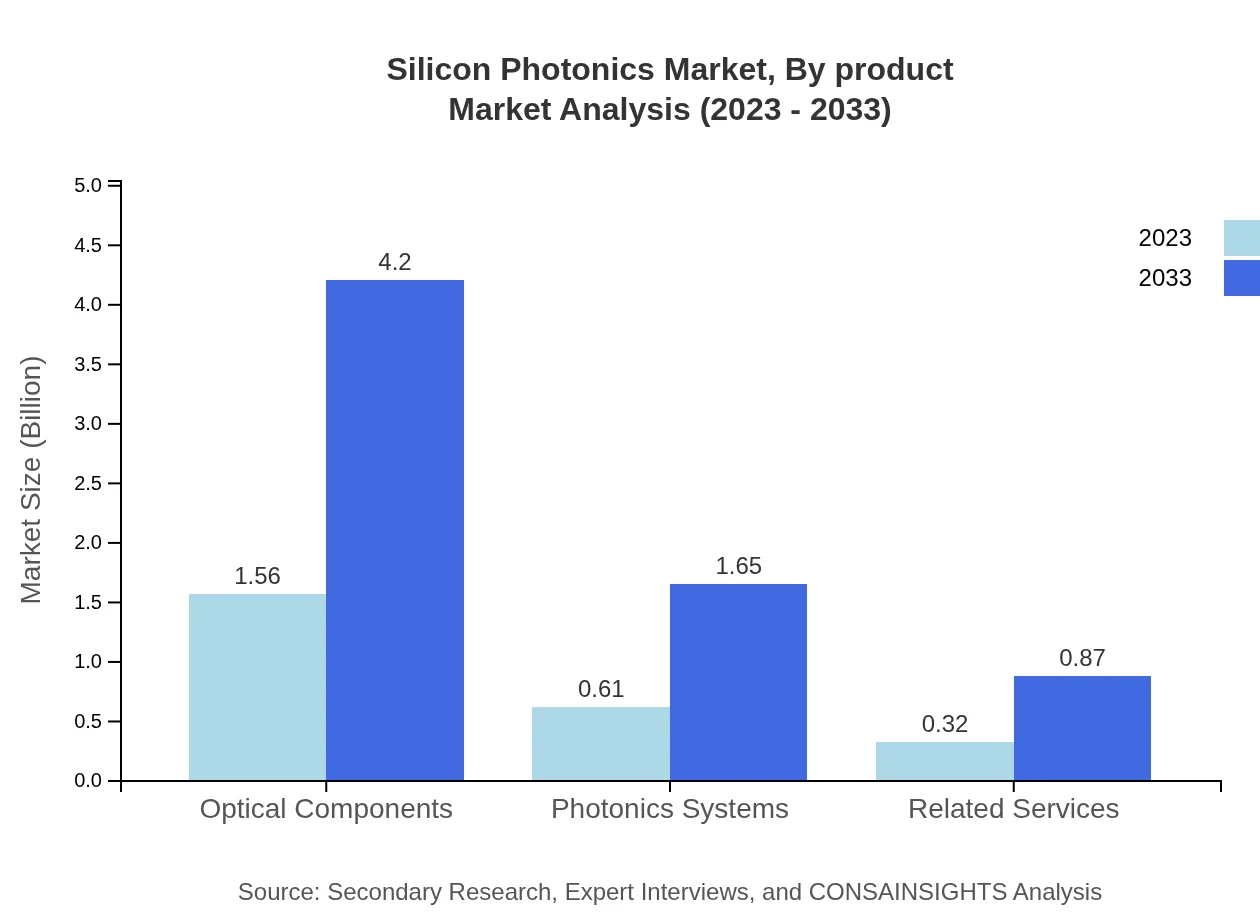

Silicon Photonics Market Analysis By Product

The Optical Components segment is the largest within the Silicon Photonics market, with a size of $1.56 billion in 2023 and projected growth to $4.20 billion by 2033. This segment holds a market share of 62.57%. Photonics Systems and Related Services follow, with sizes of $0.61 billion and $0.32 billion in 2023, respectively. By 2033, Photonics Systems is expected to reach $1.65 billion (24.51% share), while Related Services will increase to $0.87 billion (12.92% share). The performance of these segments highlights the integral role of optical technology in enhancing communication capabilities.

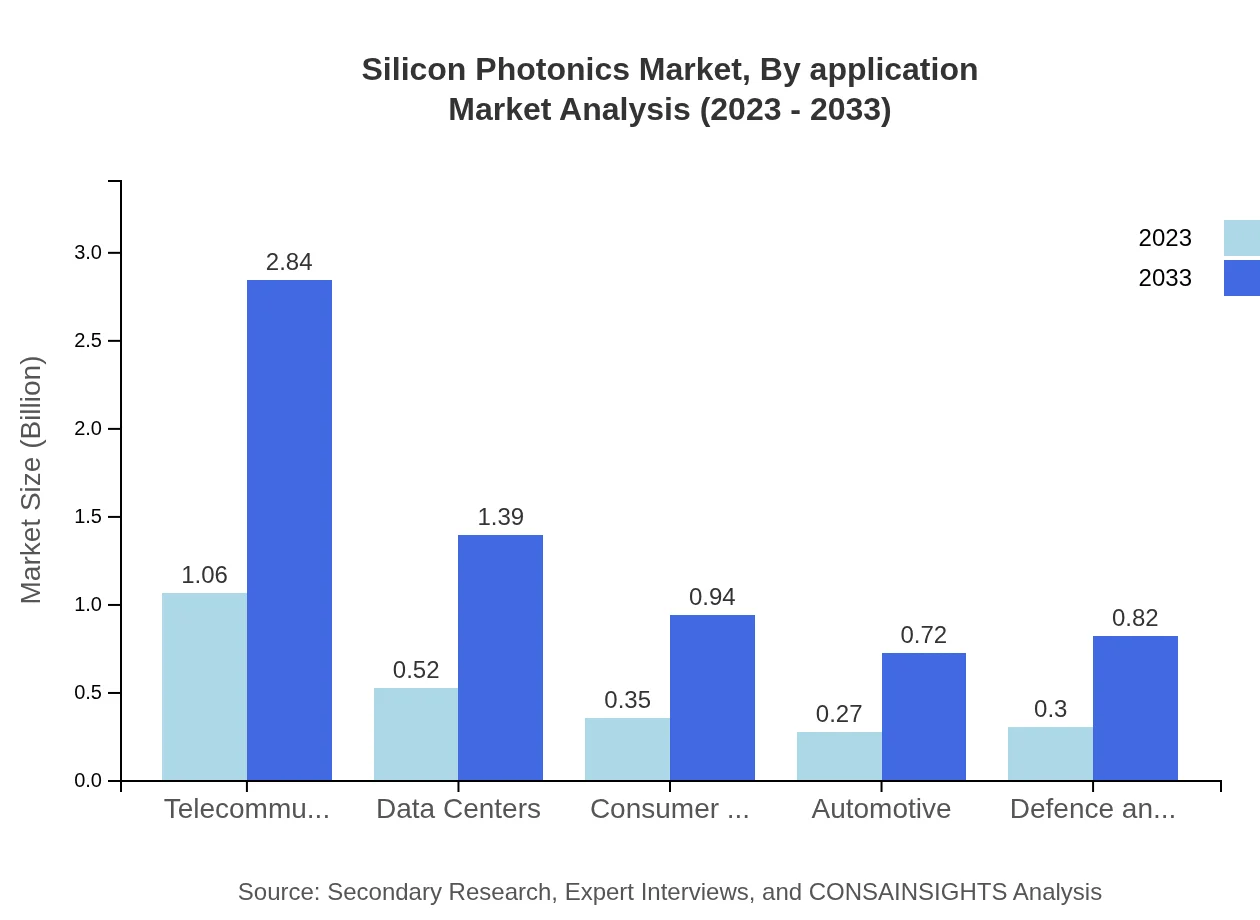

Silicon Photonics Market Analysis By Application

Telecommunications is the leading application for silicon photonics, representing a size of $1.06 billion in 2023 and projected to grow to $2.84 billion by 2033, with a 42.31% market share. Data Centers follow with $0.52 billion initially, expanding to $1.39 billion, securing a 20.77% share. Other applications include Consumer Electronics ($0.35 billion to $0.94 billion) and Automotive ($0.27 billion to $0.72 billion), which showcases the transformative nature of silicon photonics across various industries.

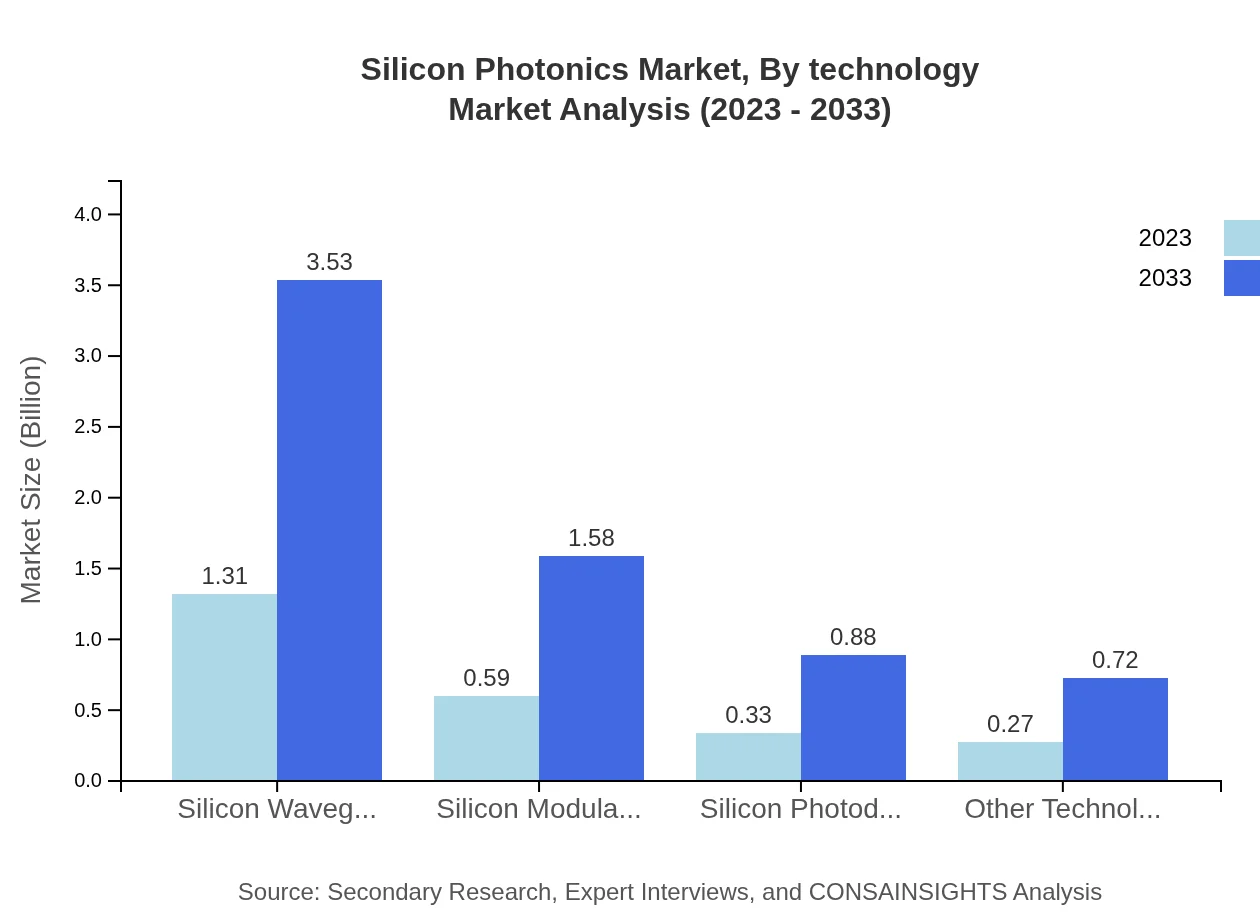

Silicon Photonics Market Analysis By Technology

In terms of technology, Silicon Waveguides exhibit prominent growth potential, escalating from $1.31 billion in 2023 to $3.53 billion by 2033, maintaining a market share of 52.6%. Other notable segments include Silicon Modulators ($0.59 billion to $1.58 billion) and Silicon Photodetectors ($0.33 billion to $0.88 billion), indicating the critical function of these technologies in the overall silicon photonics ecosystem.

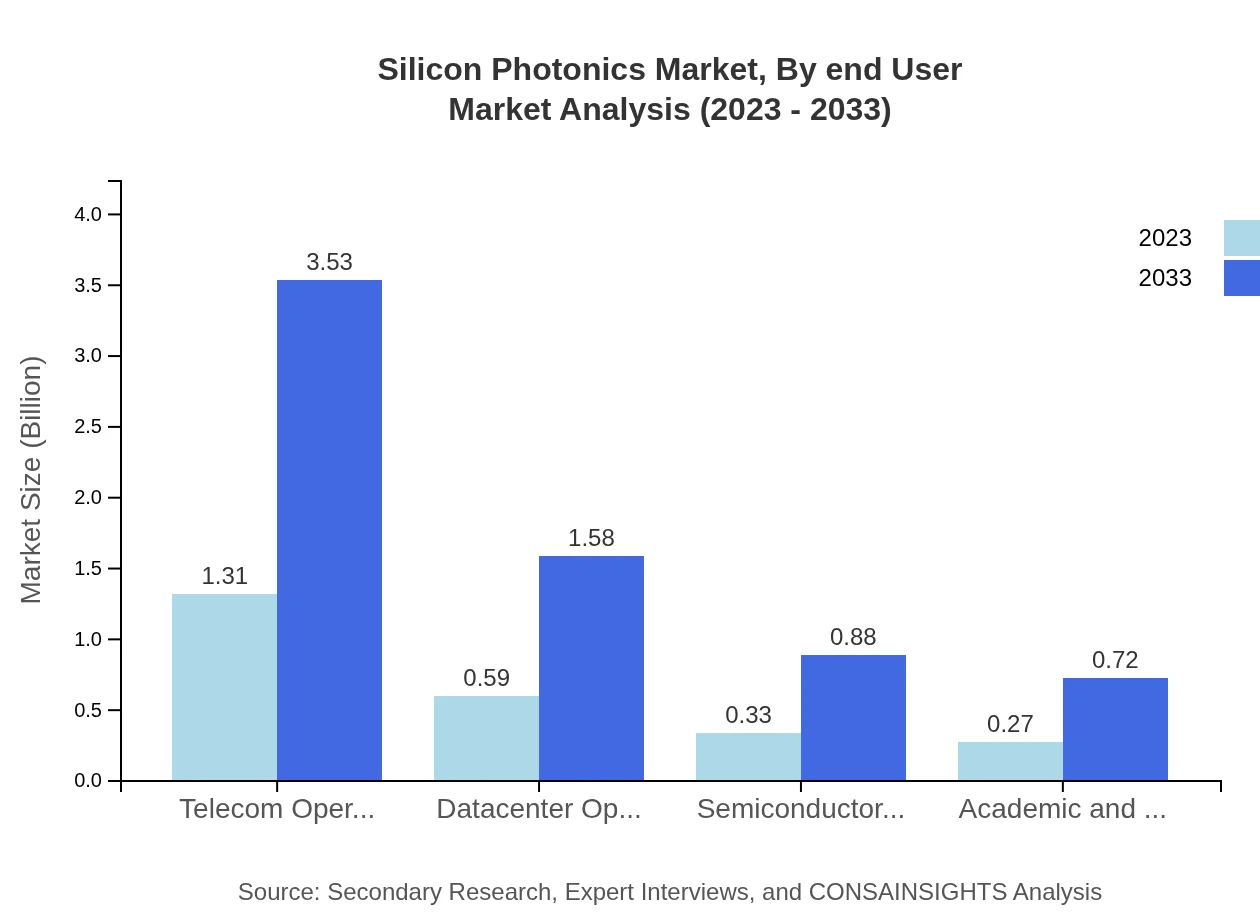

Silicon Photonics Market Analysis By End User

Key end-user industries for silicon photonics include Telecommunications, Data Centers, Consumer Electronics, and Automotive. The Telecommunications sector is valued at $1.06 billion initially, climbing to $2.84 billion by 2033, while Data Centers are projected to grow from $0.52 billion to $1.39 billion. This illustrates the critical demand and application for silicon photonics in achieving enhanced performance and efficiency in contemporary operations.

Silicon Photonics Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Silicon Photonics Industry

Intel Corporation:

A leader in silicon photonics, Intel focuses on integrating photonic technology with microprocessor systems, significantly enhancing data transfer speeds and energy efficiency.Cisco Systems, Inc.:

Cisco is a major player in networking hardware and services, leveraging silicon photonics in its solutions to improve bandwidth and connectivity for data centers and telecom networks.IBM Corporation:

IBM conducts extensive research on photonics integration, working on silicon photonics to create innovative solutions for high-performance computing and data processing systems.Luxtera:

Luxtera specializes in developing silicon photonics solutions for data centers, enhancing system performance through the integration of optical components with traditional silicon electronics.We're grateful to work with incredible clients.

FAQs

What is the market size of silicon Photonics?

The silicon-photonics market is currently valued at approximately $2.5 billion and is expected to grow at a CAGR of 10% from 2023 to 2033, indicating significant expansion driven by technological advancements and increasing demand for high-speed data transmission.

What are the key market players or companies in the silicon Photonics industry?

Key players in the silicon-photonics market include Intel, Cisco, and IBM, alongside various startups focusing on innovative optical solutions. These companies significantly impact the market by driving technological advancements and expanding product portfolios.

What are the primary factors driving the growth in the silicon Photonics industry?

Growth in the silicon-photonics industry is driven by the rising demand for high-speed data transfer, miniaturization of electronic components, and advancements in computational capacities. Additionally, the expansion of data centers and telecommunications creates significant market opportunities.

Which region is the fastest Growing in the silicon Photonics?

The fastest-growing region for silicon-photonics is North America, projected to expand from $0.84 billion in 2023 to $2.26 billion by 2033. Other growth areas include Europe and Asia-Pacific, indicating a global surge in demand for silicon-photonics technology.

Does ConsaInsights provide customized market report data for the silicon Photonics industry?

Yes, ConsaInsights offers customized market report data tailored to specific client needs in the silicon-photonics industry, allowing for detailed insights into market segments, regional trends, and competitive analyses tailored to address individual business objectives.

What deliverables can I expect from this silicon Photonics market research project?

Clients can expect comprehensive deliverables, including detailed market analysis reports, segmented data insights, trend forecasts, competitive landscape evaluations, and strategic recommendations to enhance decision-making processes within the silicon-photonics industry.

What are the market trends of silicon Photonics?

Emerging trends in the silicon-photonics market include increasing integration of optical technologies in telecommunication infrastructures, advancements in cloud computing, and the rise of AI and machine learning applications driving demand for higher data transfer rates.