Vendor Neutral Archive Vna And Pacs Market Report

First published: 21 October 2024 | Last updated: 28 May 2026 | Report Code: vendor-neutral-archive-vna-and-pacs

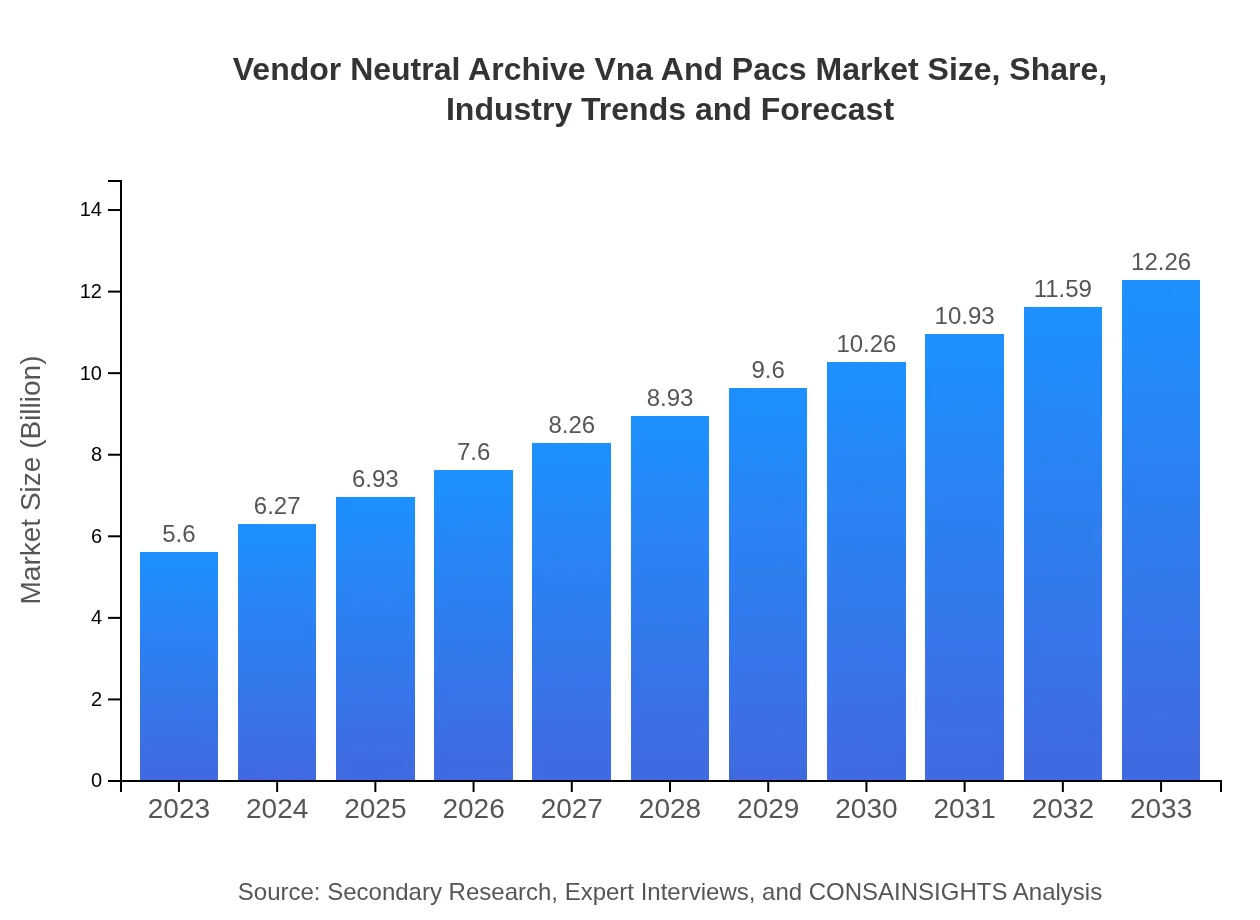

Vendor Neutral Archive Vna And Pacs Market — USD 5.6 billion in 2023, Growing to USD 12.26B by 2033 at 7.9% CAGR

This report provides an in-depth analysis of the Vendor Neutral Archive (VNA) and Picture Archiving and Communication Systems (PACS) market, covering forecasts from 2023 to 2033. Insights include market size, growth rates, technology trends, and regional explorations, aimed at empowering stakeholders with comprehensive data.

Key Takeaways

- Global market grows from $5.60 Billion in 2023 to $12.26 Billion in 2033 at a 7.9% CAGR.

- North America is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- Europe expands from $1.53 Billion in 2023 to $3.35 Billion in 2033, and Asia Pacific rises from $1.07 Billion to $2.33 Billion.

- Cloud deployment and interoperable vendor-neutral solutions are key trends enabling adoption across hospitals and diagnostic centers.

- Leading vendors include GE Healthcare, Philips Healthcare, Siemens Healthineers, Carestream Health, and McKesson Corporation.

Vendor Neutral Archive Vna And Pacs Market Report — Executive Summary

North America remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. The Vendor Neutral Archive Vna And Pacs Market Report examines a decade of growth driven by digital transformation in healthcare imaging. Rising data volumes, interoperability requirements, and a shift toward cloud-based deployments underpin expansion from $5.60 Billion in 2023 to $12.26 Billion in 2033 at a 7.9% CAGR. Key trends include migration from legacy storage to vendor-neutral archives, integration of advanced image analytics, and growing demand from hospitals, diagnostic centers, and research institutes. Regional performance varies, with North America holding the largest share based on end-period value. Major participants such as GE Healthcare, Philips Healthcare, Siemens Healthineers, Carestream Health, and McKesson Corporation are shaping market dynamics through product innovation and service offerings. The report covers segmentation by product (VNA and PACS), deployment type (cloud and on-premise), applications (medical imaging, radiology, orthopedics), and end-users, providing stakeholders with structured insight for investment and implementation decisions.

Key Growth Drivers

- Escalating medical imaging data volumes requiring scalable archive solutions

- Regulatory and interoperability mandates encouraging vendor-neutral storage adoption

- Migration to cloud deployments for reduced upfront costs and improved accessibility

- Advances in imaging analytics and integration with clinical workflows

- Rising investments by healthcare providers in IT infrastructure and data management

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.60 Billion |

| CAGR (2023-2033) | 7.9% |

| 2033 Market Size | $12.26 Billion |

| Top Companies | GE Healthcare, Philips Healthcare, Siemens Healthineers, Carestream Health, McKesson Corporation |

| Published Date | 21 October 2024 |

| Last Modified Date | 28 May 2026 |

Vendor Neutral Archive Vna And Pacs Market Overview

Customize Vendor Neutral Archive Vna And Pacs Market Report market research report

- ✔ Get in-depth analysis of Vendor Neutral Archive Vna And Pacs market size, growth, and forecasts.

- ✔ Understand Vendor Neutral Archive Vna And Pacs's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Vendor Neutral Archive Vna And Pacs

What is the Market Size & CAGR of Vendor Neutral Archive Vna And Pacs Market Report market in 2023?

Vendor Neutral Archive Vna And Pacs Industry Analysis

Vendor Neutral Archive Vna And Pacs Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Vendor Neutral Archive Vna And Pacs Market Report Market Analysis Report by Region

Europe Vendor Neutral Archive Vna And Pacs Market Report:

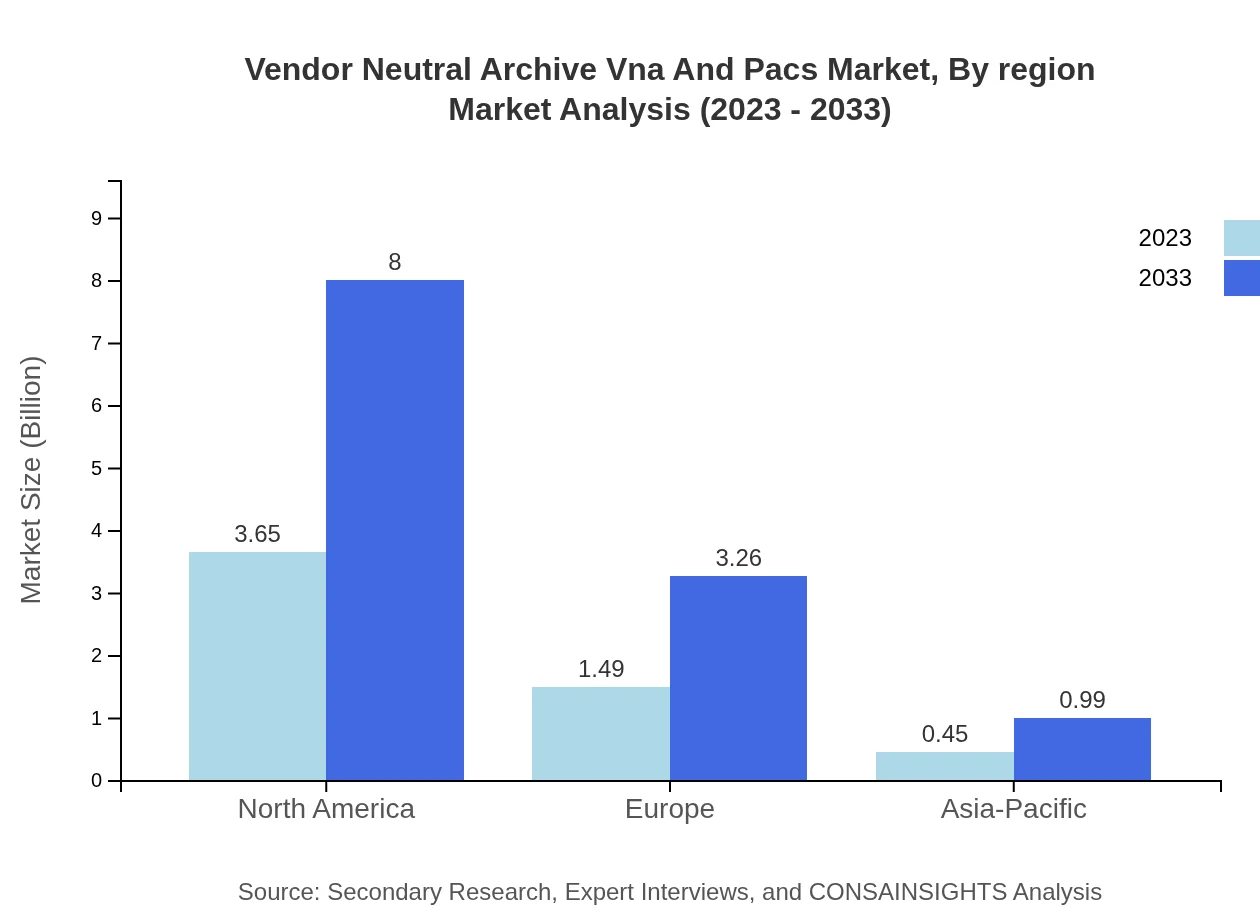

Europe grows from $1.53 Billion in 2023 to $3.35 Billion in 2033. Adoption is being supported by regulatory emphasis on data sharing, digitization of medical records, and hospitals shifting toward vendor-neutral archives for cross-provider access.Asia Pacific Vendor Neutral Archive Vna And Pacs Market Report:

Asia Pacific grows from $1.07 Billion in 2023 to $2.33 Billion in 2033. Expansion is driven by rising healthcare expenditures, increased imaging capacity, and a move to scalable cloud and archive solutions to manage growing datasets.North America Vendor Neutral Archive Vna And Pacs Market Report:

North America is largest regional market, rising from $2.1 Billion in 2023 to $4.61 Billion in 2033. This region’s trajectory reflects strong investments in healthcare IT, high imaging utilization, and early adoption of interoperable, vendor-neutral storage and cloud deployments.South America Vendor Neutral Archive Vna And Pacs Market Report:

Latin America grows from $0.34 Billion in 2023 to $0.74 Billion in 2033. Growth reflects gradual digitization of imaging workflows, investments in diagnostic infrastructure, and the need for interoperable image storage across care facilities.Middle East & Africa Vendor Neutral Archive Vna And Pacs Market Report:

Middle East and Africa grows from $0.56 Billion in 2023 to $1.23 Billion in 2033. Market drivers include expanding healthcare infrastructure, rising imaging procedures, and adoption of vendor-neutral approaches to improve data accessibility.Tell us your focus area and get a customized research report.

Research Methodology

Vendor Neutral Archive Vna And Pacs Market Analysis By Product

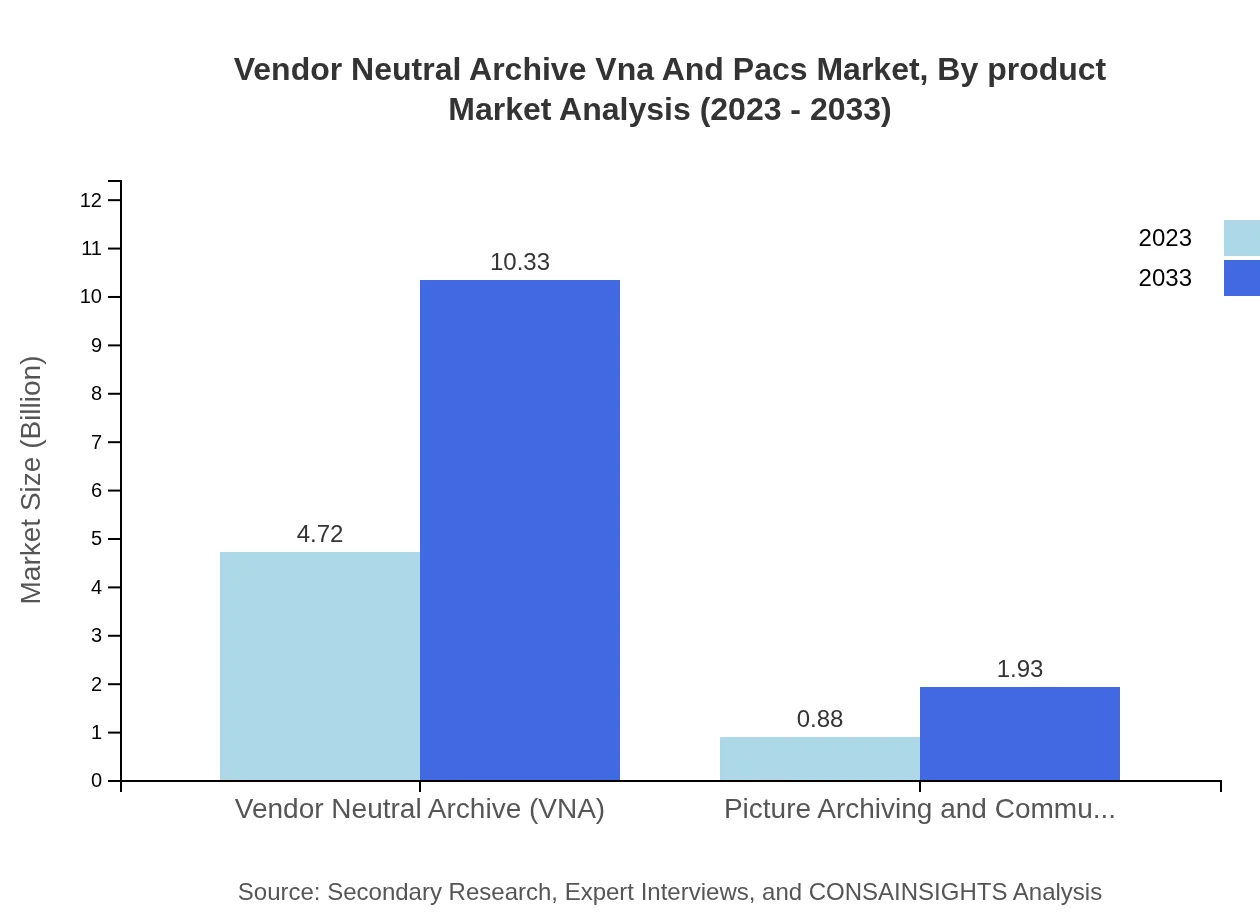

VNA products dominate the market, accounting for approximately 84.24% of the share in 2023, and are expected to drive significant growth due to their flexibility and interoperability benefits. PACS holds 15.76% of the market, reflecting its essential role in traditional imaging practices. Both product segments are crucial for comprehensive medical imaging solutions.

Vendor Neutral Archive Vna And Pacs Market Analysis By Application

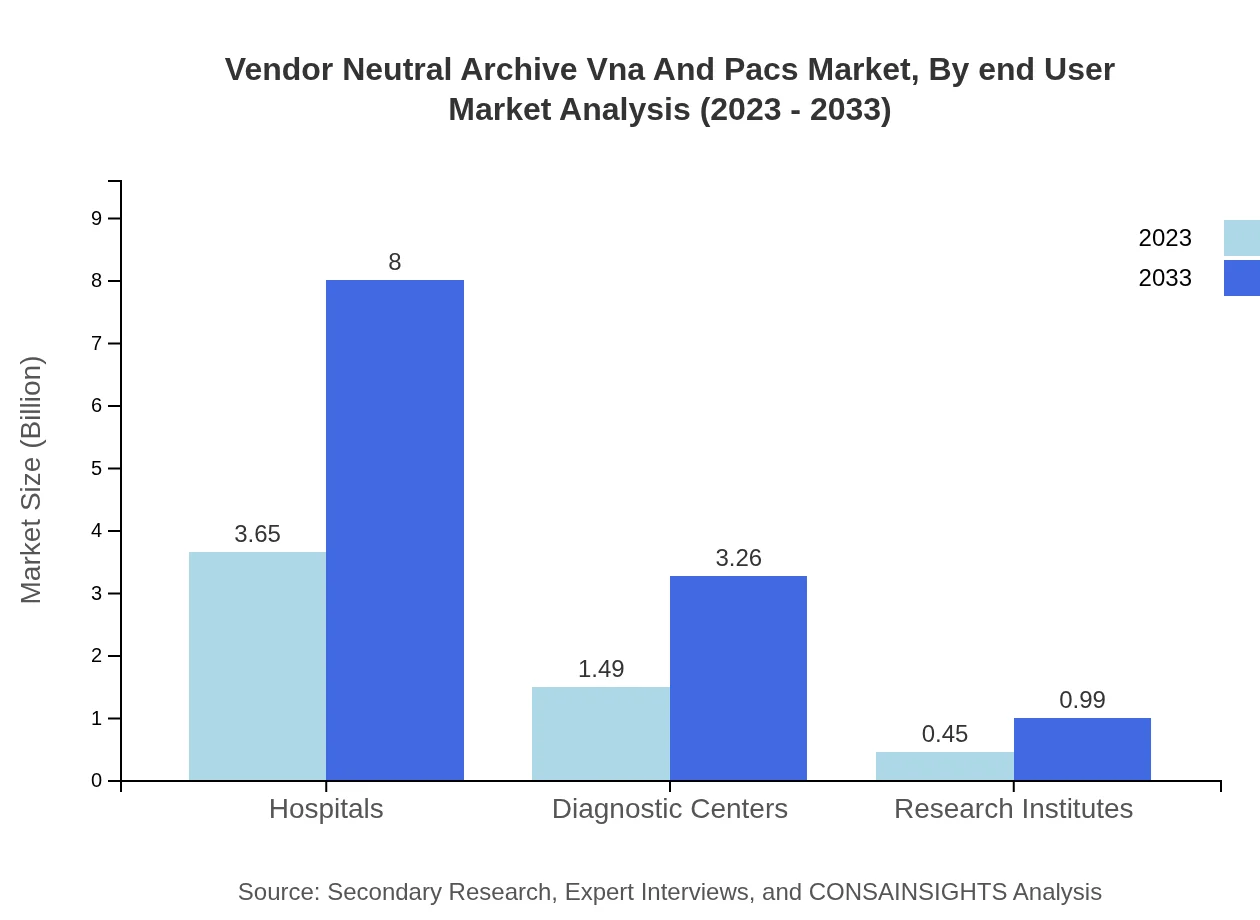

In the application segment, hospitals represent the largest end-user market, contributing to 65.26% in 2023, growing steadily as healthcare providers adopt integrated imaging systems. Diagnostic centers follow with a significant share of 26.63%, reflecting their reliance on efficient data management for patient diagnostics.

Vendor Neutral Archive Vna And Pacs Market Analysis By Deployment Type

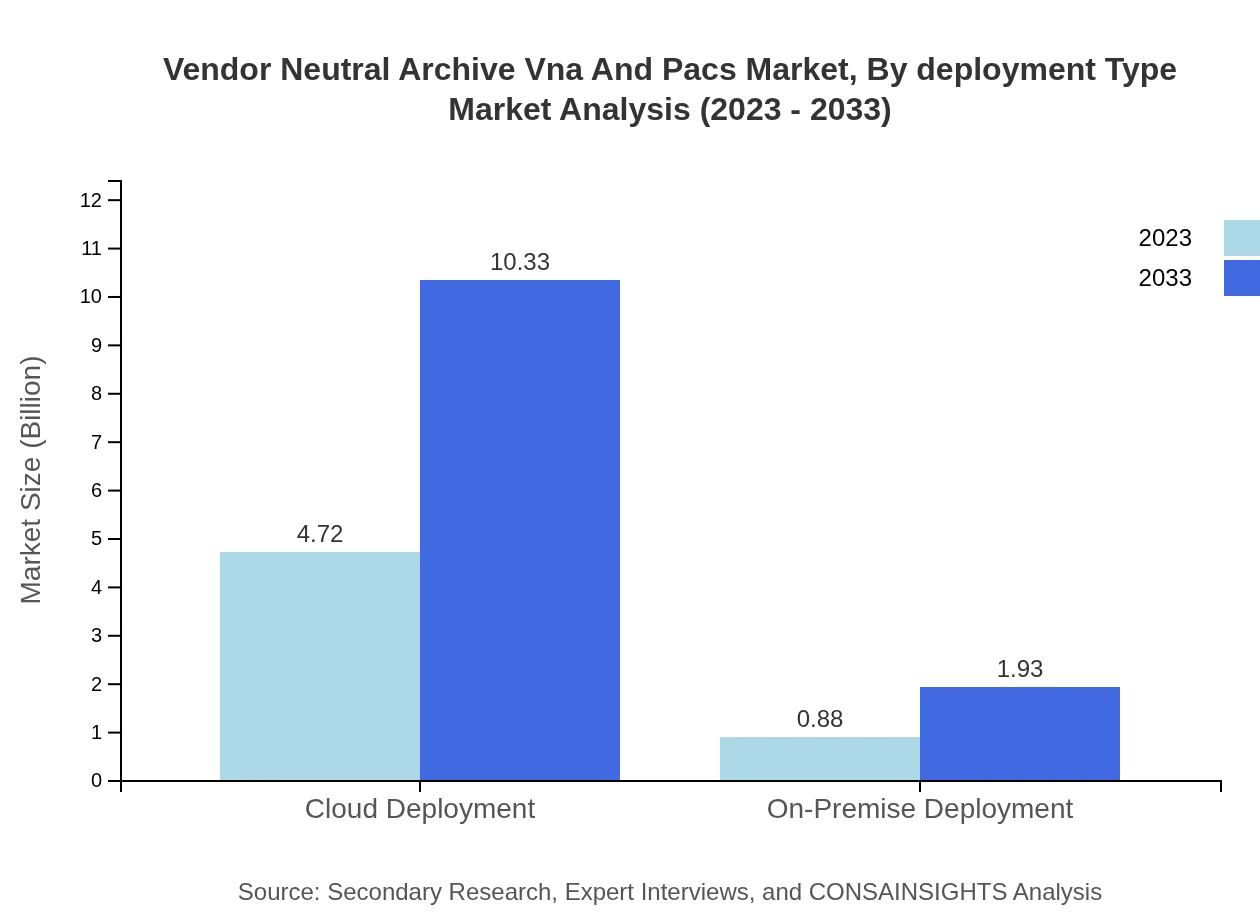

Cloud deployment is preferred due to its 84.24% share in the market, driven by its cost-effectiveness and accessibility. On-premise deployment accounts for 15.76% as some organizations prefer retaining data on-site for compliance and security reasons.

Vendor Neutral Archive Vna And Pacs Market Analysis By End User

The end-user landscape showcases a strong inclination towards hospitals, contributing significantly with a market share of 65.26% in 2023, while diagnostic centers hold 26.63%, emphasizing the need for robust imaging solutions in patient care environments.

Vendor Neutral Archive Vna And Pacs Market Analysis By Region

Regional analysis reveals North America as the largest market area with a size of $4.61 billion by 2033. Europe and Asia-Pacific are also critical regions showing robust growth due to increasing investments in health facilities and technological advancements.

Vendor Neutral Archive Vna And Pacs Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Vendor Neutral Archive Vna And Pacs Industry

GE Healthcare:

GE Healthcare is a leading player offering innovative imaging solutions that enhance workflow efficiency and patient care standards.Philips Healthcare:

Philips is known for its advanced VNA and PACS systems, focusing on personalized healthcare and improved clinical outcomes.Siemens Healthineers:

Siemens provides integrated imaging solutions with advanced analytics capabilities as part of its PACS and VNA offerings.Carestream Health:

Carestream Health specializes in imaging and healthcare IT solutions, enhancing diagnostic and operational efficiencies.McKesson Corporation:

McKesson is a prominent healthcare provider that integrates VNA solutions into its distribution and pharmacy services.We're grateful to work with incredible clients.

FAQs

What is the market size in 2023?

The market size in 2023 is $5.60 Billion as stated in the report data for the Vendor Neutral Archive Vna And Pacs market.

How big will the market be in 2033?

By 2033 the market is projected to reach $12.26 Billion according to the provided forecast figures covering the 2023 to 2033 period.

What is CAGR for the forecast period?

The compound annual growth rate (CAGR) for the 2023 to 2033 forecast period is 7.9%, based on the supplied market projections.

Is there a single fastest Growing region in the Vendor Neutral Archive Vna And Pacs Market Report market?

No single fastest-growing region is stated for the Vendor Neutral Archive Vna And Pacs Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Which product segments are included?

The report segments by product into Vendor Neutral Archive (VNA) and Picture Archiving and Communication Systems (PACS), as listed in the input data.

Who are the top companies in the market?

Top companies named in the report include GE Healthcare, Philips Healthcare, Siemens Healthineers, Carestream Health, and McKesson Corporation.

What deployment types are covered?

Deployment types included are Cloud Deployment and On-Premise Deployment, reflecting the primary models for VNA and PACS solutions.

How do applications segment the market?

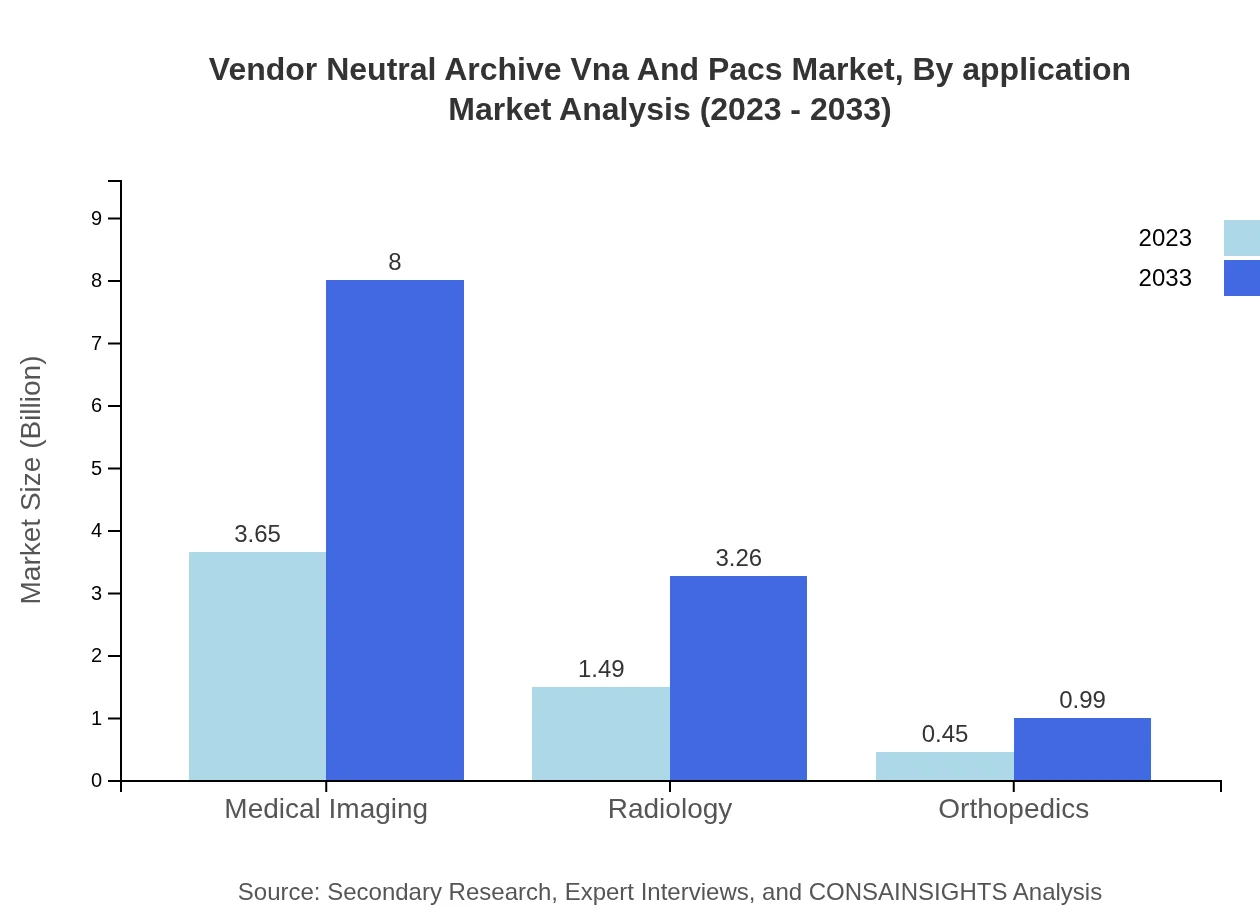

Application segments specified include Medical Imaging, Radiology, and Orthopedics, which represent core clinical use cases for VNA and PACS.

What end Users are addressed in the report?

End-user categories in the dataset are Hospitals, Diagnostic Centers, and Research Institutes as primary consumers of VNA and PACS technologies.

Why are cloud solutions influential?

Cloud solutions are influential due to scalability, lower upfront costs, and enhanced accessibility, supporting wider adoption of vendor-neutral archive strategies.