Automated Plate Handlers Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: automated-plate-handlers

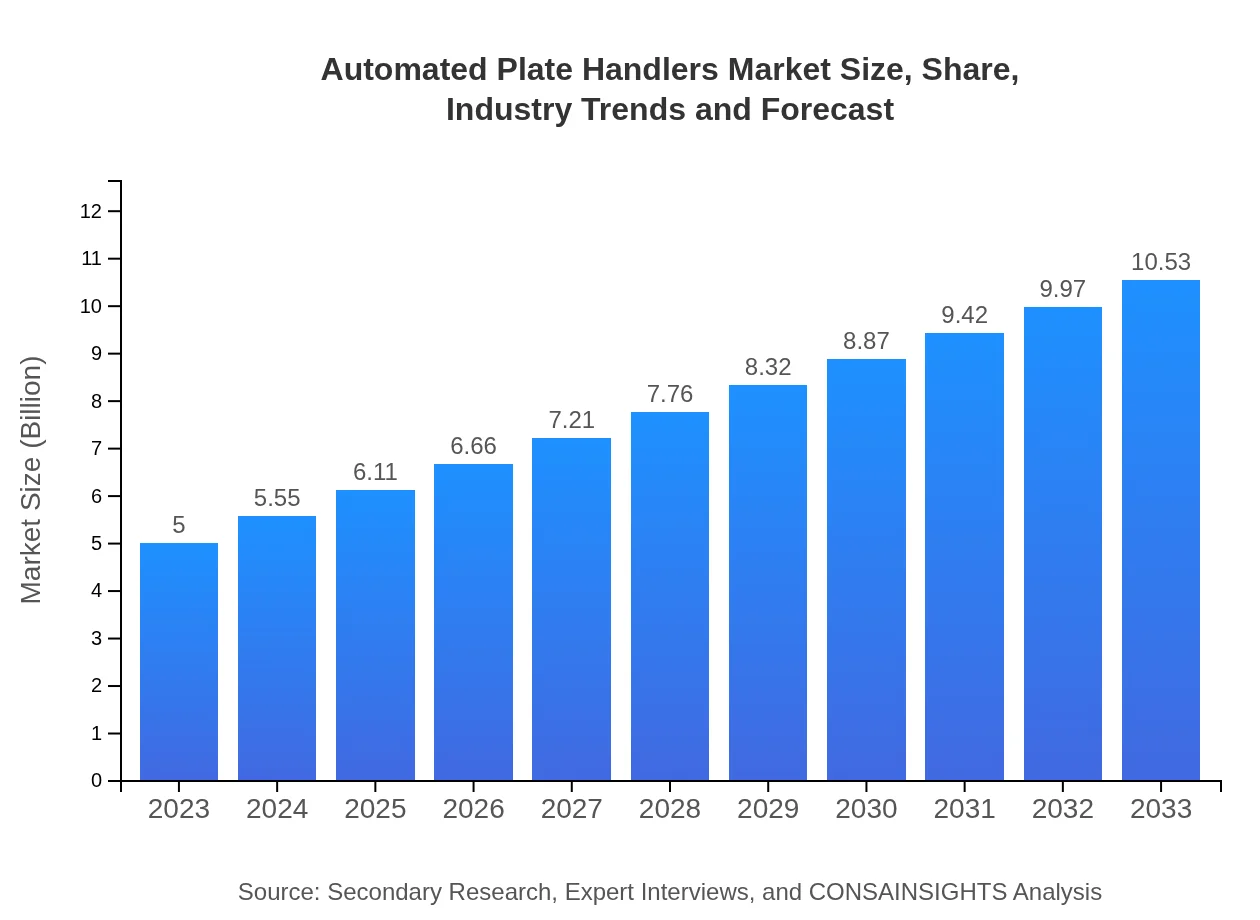

Automated Plate Handlers Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides an in-depth analysis of the Automated Plate Handlers market, covering market trends, growth forecasts for 2023 to 2033, regional insights, and key player contributions.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | KUKA AG, FANUC Corporation, Siemens AG, ABB Ltd., Yaskawa Electric Corporation |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Automated Plate Handlers Market Overview

Customize Automated Plate Handlers Market Report market research report

- ✔ Get in-depth analysis of Automated Plate Handlers market size, growth, and forecasts.

- ✔ Understand Automated Plate Handlers's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Automated Plate Handlers

What is the Market Size & CAGR of Automated Plate Handlers market in 2023?

Automated Plate Handlers Industry Analysis

Automated Plate Handlers Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Automated Plate Handlers Market Analysis Report by Region

Europe Automated Plate Handlers Market Report:

The European market is also witnessing robust growth, with a forecasted increase from $1.55 billion in 2023 to $3.26 billion by 2033. Stringent regulations regarding efficiency and productivity in manufacturing are pushing industries towards advanced automation solutions.Asia Pacific Automated Plate Handlers Market Report:

The Asia Pacific region is predicted to exhibit strong growth, with the market size projected to increase from $0.95 billion in 2023 to $1.99 billion by 2033. Key countries such as China and Japan are leading in the adoption of automated systems in manufacturing, significantly boosting demand for plate handling solutions.North America Automated Plate Handlers Market Report:

North America holds a substantial share of the market, anticipated to grow from $1.77 billion in 2023 to $3.73 billion by 2033. The presence of major players and advancements in automation technology in the U.S. are key contributors to this expansion.South America Automated Plate Handlers Market Report:

In South America, the market for Automated Plate Handlers is expected to grow from $0.27 billion in 2023 to $0.58 billion in 2033. Increased industrial automation and investment in logistics are pivotal factors driving this growth, although the market remains smaller compared to other regions.Middle East & Africa Automated Plate Handlers Market Report:

In the Middle East and Africa, the market is expected to rise from $0.46 billion in 2023 to $0.97 billion by 2033. Growing investments in manufacturing facilities and strategic initiatives to enhance automation are primary growth factors in this region.Tell us your focus area and get a customized research report.

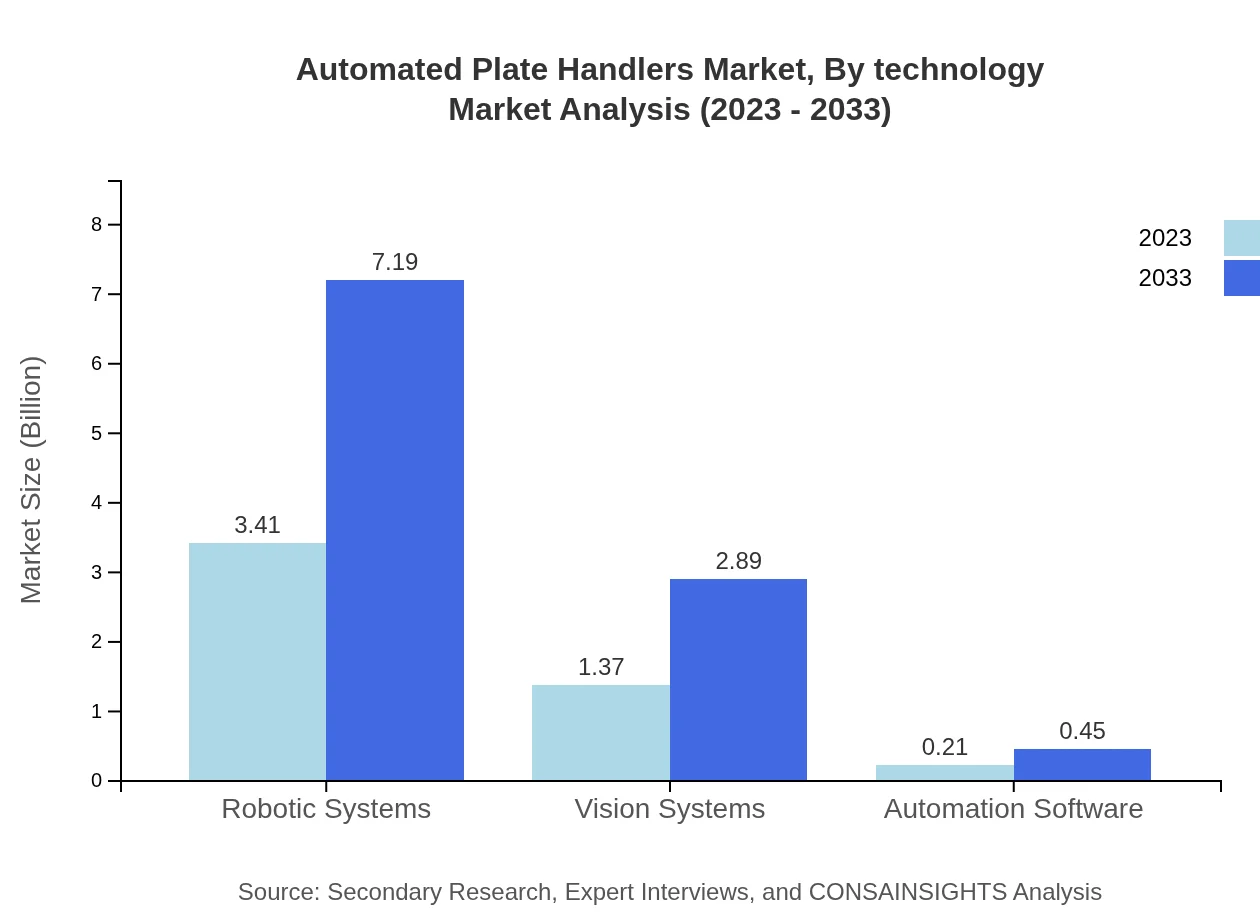

Automated Plate Handlers Market Analysis By Technology

The technology segment has varying performance levels, with Robotic Systems leading the market due to their wide application and efficiency. In 2023, the Robotic Systems segment accounted for $3.41 billion in market size, growing to $7.19 billion by 2033, capturing about 68.3% of the market share. Following this, Vision Systems and Automation Software are also experiencing growth as industries focus on enhancing accuracy and operational intelligence.

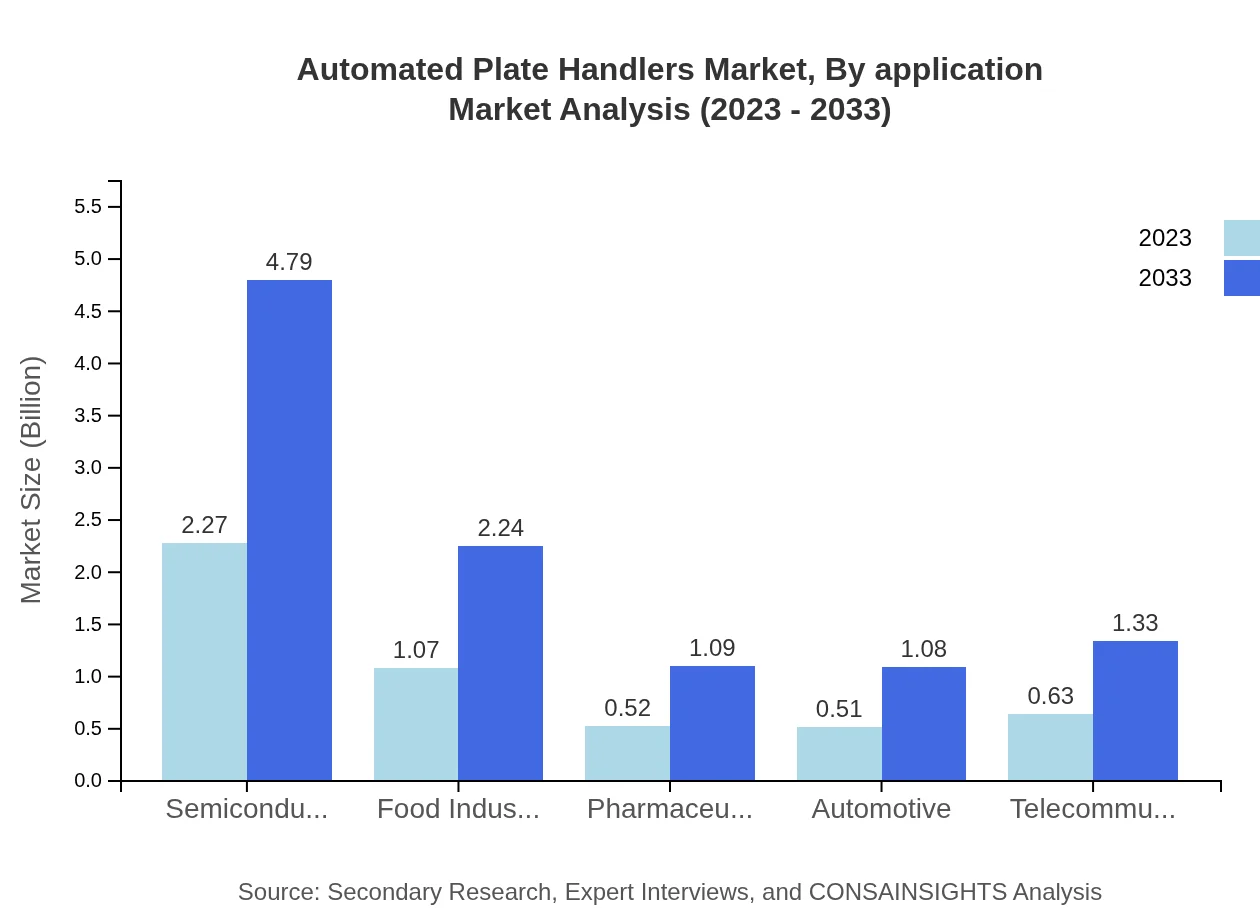

Automated Plate Handlers Market Analysis By Application

Applications in Electronics Manufacturing, Food and Beverage, and Healthcare represent significant market shares. The Electronics Manufacturers segment is largest, equating to $2.27 billion in 2023, projected to grow to $4.79 billion by 2033. The Food and Beverage segment, valued at $1.07 billion in 2023, is anticipated to reach $2.24 billion, reflecting a steady demand for automation in food processing.

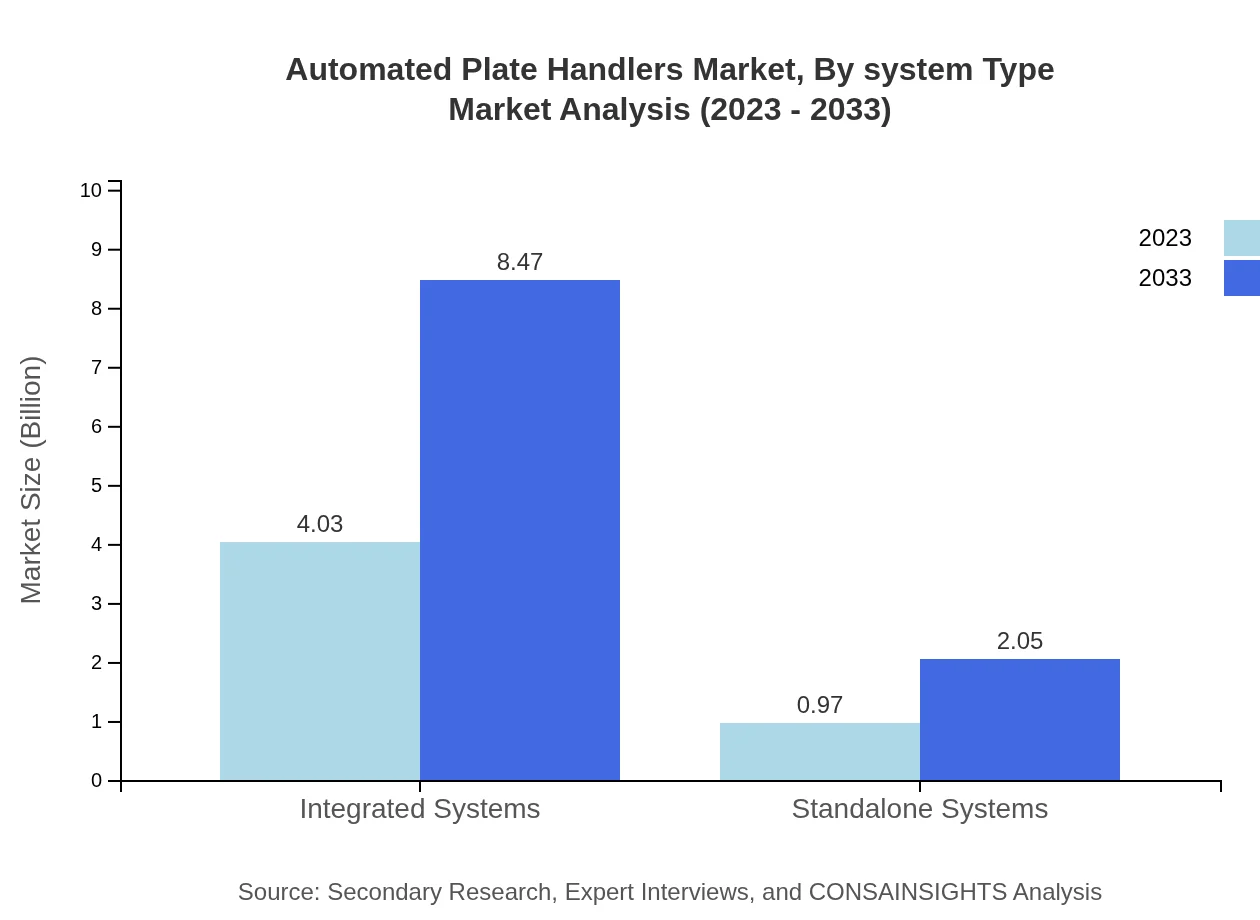

Automated Plate Handlers Market Analysis By System Type

Integrated Systems dominate the system type segment, accounting for $4.03 billion in 2023, expected to rise to $8.47 billion by 2033, driven by their effectiveness in streamlining operations. Standalone Systems, while smaller, are experiencing growth in niche applications, projected to move from $0.97 billion to $2.05 billion over the same period.

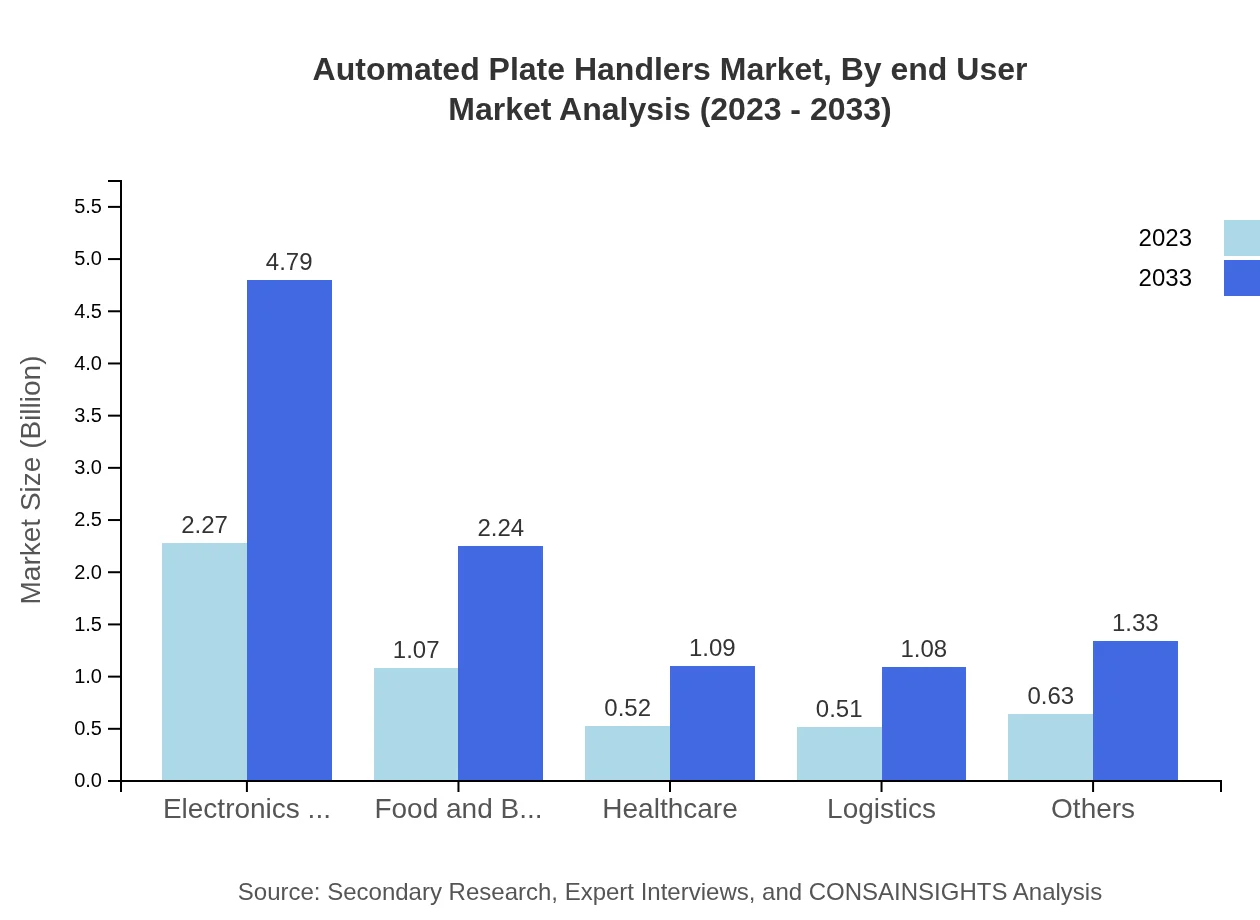

Automated Plate Handlers Market Analysis By End User

In terms of end-user industries, Electronics Manufacturing tops the chart, followed closely by Food and Beverage and Healthcare. Electronics will account for a substantial market share by comprising 45.5% in 2023 and remaining steady throughout the forecast period. The Food and Beverage sectors are witnessing increasing demand driven by automation in food processing and packaging.

Automated Plate Handlers Market Analysis By Region

Global Automated Plate Handlers Market, By Region Market Analysis (2023 - 2033)

The breakdown by region indicates varying growth rates and market preferences. North America and Europe lead with technological advancements, while the Asia Pacific region presents a rapidly expanding market due to increased industrial activities. South America and the Middle East & Africa are emerging markets, where investments in automation equipment are starting to gain traction.

Automated Plate Handlers Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Automated Plate Handlers Industry

KUKA AG:

KUKA AG is a global leader in advanced robotics and automation solutions, specializing in robotics and automation technologies to enhance production efficiency.FANUC Corporation:

FANUC Corporation provides industrial robots and automation technologies including advanced plate handling systems, known for their innovation and reliability.Siemens AG:

Siemens AG is a multinational technology company known for its automation and digitalization solutions that boost productivity across industries.ABB Ltd.:

ABB is a renowned automation technology company that focuses on enhancing productivity through innovative solutions including automated handling systems.Yaskawa Electric Corporation:

Yaskawa manufactures industrial robotics and automation systems, positioning itself as a key player in the automated plate handling market.We're grateful to work with incredible clients.

FAQs

What is the market size of automated plate handlers?

The automated plate handlers market is currently valued at approximately $5 billion, with projections indicating a compound annual growth rate (CAGR) of 7.5%. This growth is driven by increasing automation in manufacturing processes.

What are the key market players or companies in the automated plate handlers industry?

Key players in the automated plate handlers market include companies specializing in robotics, automation technology, and industrial solutions. These leaders are pivotal in fostering innovation and competition, shaping the industry's landscape and driving technological advancements.

What are the primary factors driving the growth in the automated plate handlers industry?

Growth in the automated plate handlers industry is primarily driven by the rise of automation in manufacturing, the need for operational efficiency, increased demand for precision in production, and the growing focus on reducing labor costs through automation.

Which region is the fastest Growing in the automated plate handlers market?

The fastest-growing region in the automated plate handlers market is expected to be Europe, with market growth projected from approximately $1.55 billion in 2023 to $3.26 billion by 2033, indicating significant demand for automation in various industries.

Does ConsaInsights provide customized market report data for the automated plate handlers industry?

Yes, ConsaInsights offers customized market report data for the automated plate handlers industry, allowing clients to access tailored insights and analysis that cater to their specific business needs and competitive strategies.

What deliverables can I expect from this automated plate handlers market research project?

Deliverables from the automated plate handlers market research project typically include detailed market analysis reports, forecasts, competitive landscape assessments, and insights into industry trends that inform strategic decision-making.

What are the market trends of automated plate handlers?

Current market trends for automated plate handlers include an increasing integration of advanced robotics, the adoption of AI and machine learning in automation processes, and a shift towards more sustainable practices within manufacturing and supply chain operations.