Hvac Filters Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: hvac-filters

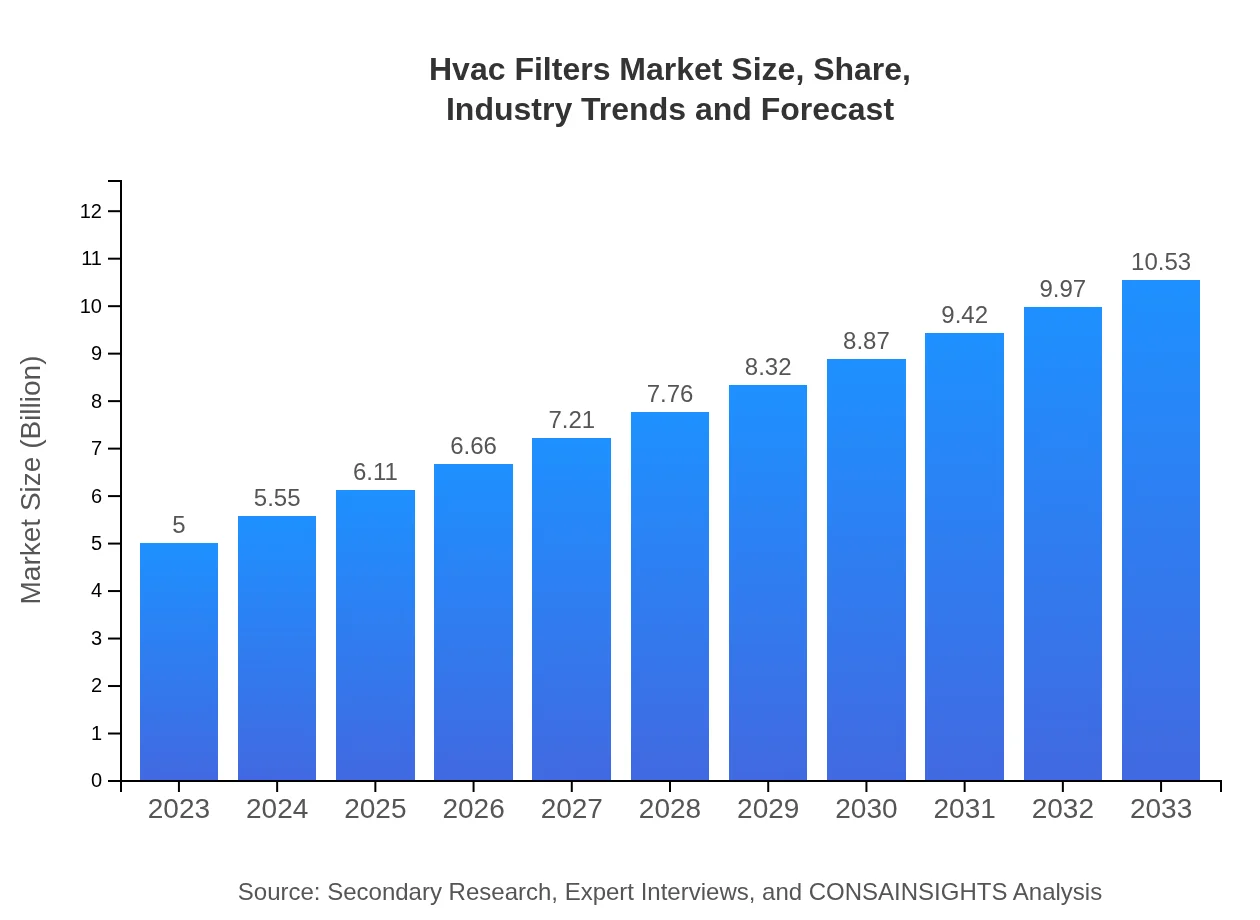

Hvac Filters Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides a comprehensive analysis of the HVAC filters market, covering market size, trends, and forecasts for the years 2023 to 2033. Insights include industry segmentation, regional performance, technology impacts, and profiles of key market players.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | MERV Filters Inc., 3M Company, Honeywell International Inc., Camfil |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Hvac Filters Market Overview

Customize Hvac Filters Market Report market research report

- ✔ Get in-depth analysis of Hvac Filters market size, growth, and forecasts.

- ✔ Understand Hvac Filters's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Hvac Filters

What is the Market Size & CAGR of HVAC Filters market in 2023?

HVAC Filters Industry Analysis

HVAC Filters Market Segmentation and Scope

Tell us your focus area and get a customized research report.

HVAC Filters Market Analysis Report by Region

Europe Hvac Filters Market Report:

Europe's HVAC filters market is anticipated to grow from $1.23 billion in 2023 to $2.58 billion by 2033. The EU's aggressive climate policies and emphasis on green buildings are key contributors to this growth.Asia Pacific Hvac Filters Market Report:

In 2023, the HVAC filters market in the Asia Pacific region is valued at $0.97 billion and is projected to grow to $2.03 billion by 2033. This growth is fueled by rapid urbanization, increased construction activities, and rising pollution levels, which heighten the need for effective air filtration solutions.North America Hvac Filters Market Report:

The North American market is significantly robust, with a valuation of $1.76 billion in 2023, expected to reach $3.70 billion by 2033. The demand is propelled by strict environmental regulations and high consumer awareness regarding indoor air quality.South America Hvac Filters Market Report:

The South American HVAC filters market is valued at $0.39 billion in 2023, with expectations to rise to $0.81 billion by 2033. The region's growth is driven by increasing investments in infrastructure and growing awareness of air quality issues.Middle East & Africa Hvac Filters Market Report:

In the Middle East and Africa, the market is valued at $0.66 billion in 2023 and projected at $1.40 billion by 2033, driven by increasing investments in HVAC systems and rising temperatures leading to higher demand for air conditioning.Tell us your focus area and get a customized research report.

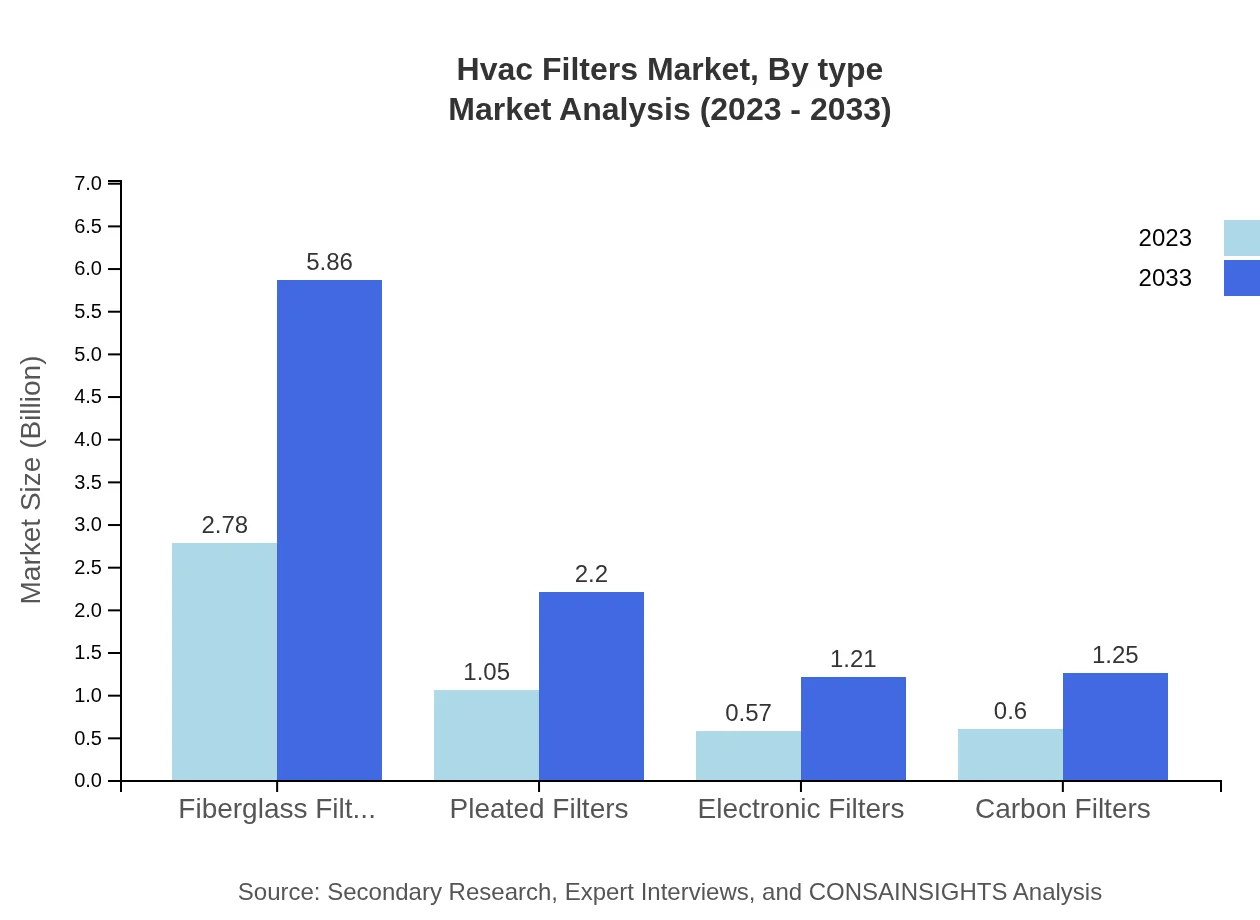

Hvac Filters Market Analysis By Type

The analysis of the HVAC filters market by type reveals distinct performance metrics across various filter categories. In 2023, fiberglass filters dominate the market with a size of $2.78 billion, projected to grow to $5.86 billion by 2033, capturing over 55% market share. Pleated filters follow with sizes of $1.05 billion in 2023 and $2.20 billion by 2033, holding a market share of approximately 20.94%. Electronic filters, although relatively smaller, show growth potential, moving from $0.57 billion to $1.21 billion. Carbon filters also exhibit growth from $0.60 billion to $1.25 billion.

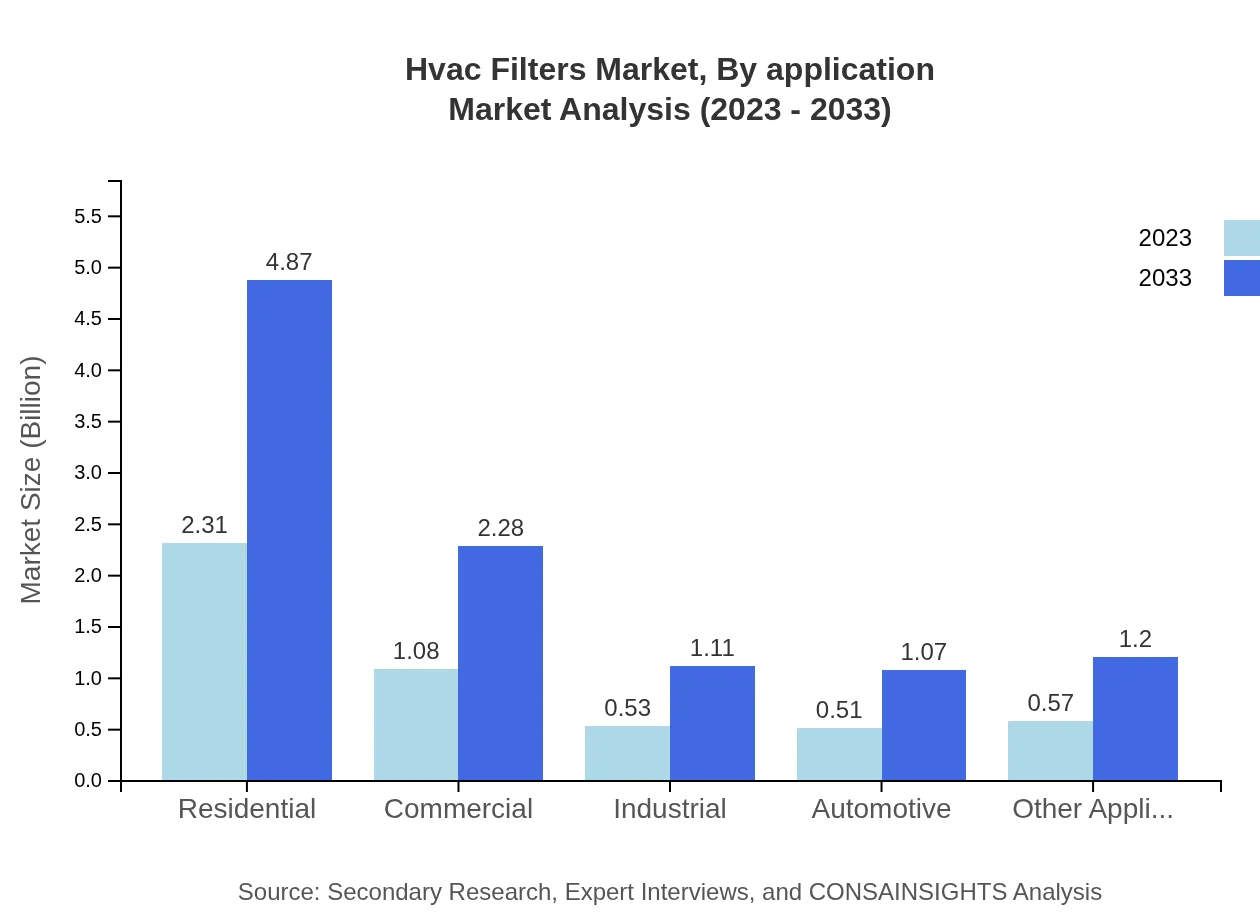

Hvac Filters Market Analysis By Application

Examining the market by application, residential buildings lead with a significant share of $2.78 billion in 2023, expected to reach $5.86 billion by 2033. Commercial buildings contribute $1.05 billion to the market in 2023, projected at $2.20 billion by 2033. Industrial applications and transportation also reflect growth, indicating diversification in air filter usage across sectors.

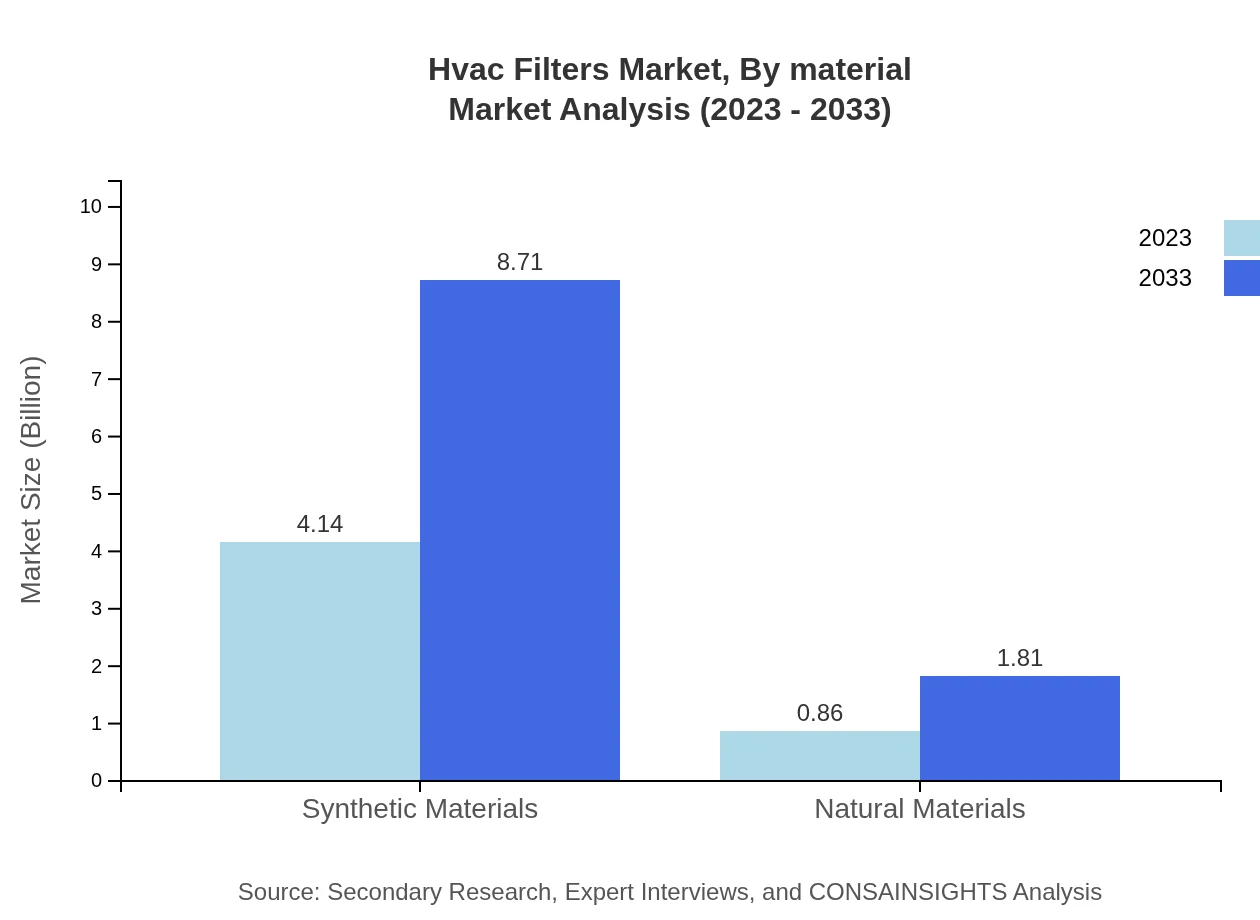

Hvac Filters Market Analysis By Material

The HVAC filters market by material shows that synthetic materials dominate with a size of $4.14 billion in 2023, expected to double by 2033. Natural materials present a smaller segment at $0.86 billion in 2023 but are expected to grow steadily, indicating a trend towards more environmentally friendly products.

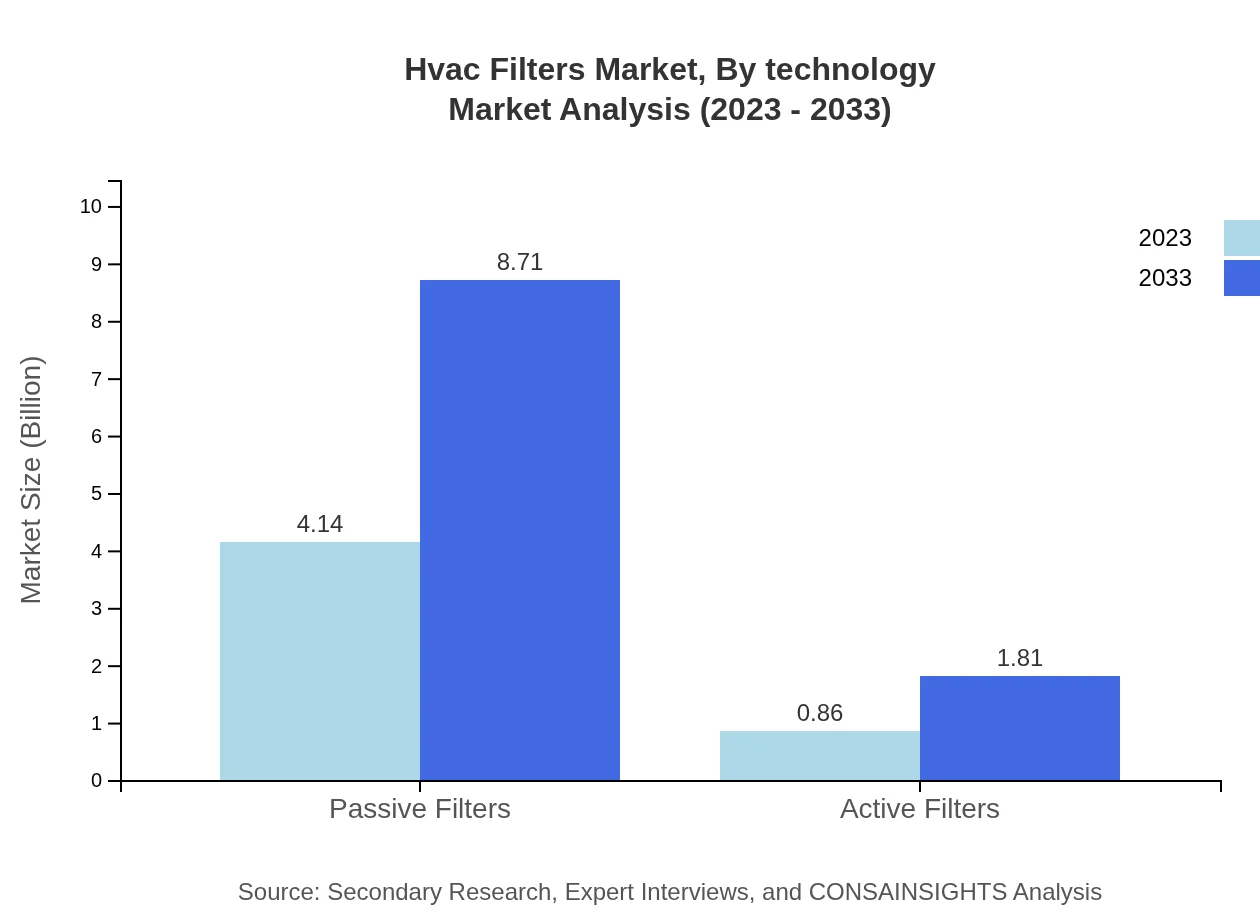

Hvac Filters Market Analysis By Technology

In terms of technology, passive filters lead the market with $4.14 billion in 2023, while active filters account for $0.86 billion, indicating a preference for traditional filtration methods in most applications. However, the demand for innovative active filtration technologies is emerging, as consumers seek efficient solutions.

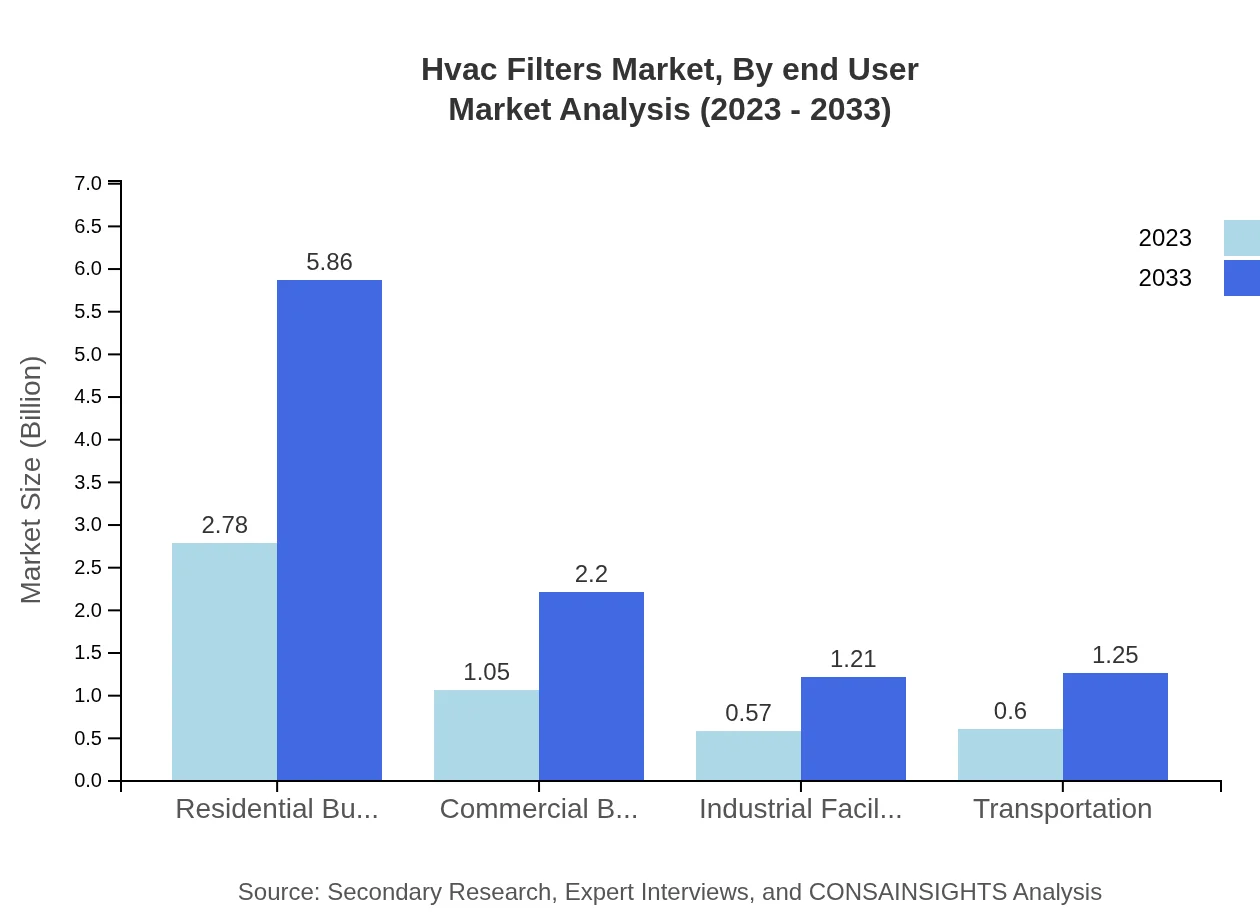

Hvac Filters Market Analysis By End User

Analyzing by end-user, residential applications account for 46.29% of the market share in 2023, while commercial applications provide approximately 21.67%. Industrial and automotive segments also contribute, reflecting the comprehensive applicability of HVAC filters across various environments.

HVAC Filters Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in HVAC Filters Industry

MERV Filters Inc.:

MERV Filters Inc. is a leading manufacturer specializing in high-efficiency air filters, focusing on innovative solutions for both residential and commercial markets.3M Company:

3M Company provides a wide range of air filtration products, employing cutting-edge technology to enhance indoor air quality and energy efficiency in HVAC systems.Honeywell International Inc.:

Honeywell is a technology and manufacturing leader that produces advanced HVAC filtration solutions compatible with various air conditioning systems.Camfil:

Camfil is renowned for its commitment to sustainability, offering premium air filters designed to improve energy efficiency and minimize environmental impact.We're grateful to work with incredible clients.

FAQs

What is the market size of HVAC filters?

The global HVAC filters market size is projected to reach $5 billion by 2033, growing at a CAGR of 7.5%. In 2023, the market was valued at $2.78 billion, highlighting strong growth potential over the next decade.

What are the key market players or companies in the HVAC filters industry?

Key players in the HVAC filters market include 3M Company, Honeywell International Inc., and Lennox International. These companies dominate through innovation, extensive distribution networks, and commitment to environmental standards.

What are the primary factors driving the growth in the HVAC filters industry?

Factors driving growth in the HVAC filters market include rising air quality concerns, increasing construction of residential and commercial buildings, and regulatory standards for air pollution and energy efficiency.

Which region is the fastest Growing in the HVAC filters market?

The Asia Pacific region is the fastest-growing market for HVAC filters, expected to rise from $0.97 billion in 2023 to $2.03 billion by 2033. This growth is fueled by urbanization and enhanced living standards.

Does ConsInsights provide customized market report data for the HVAC filters industry?

Yes, ConsInsights offers customized market report data tailored to specific needs in the HVAC filters industry. Clients can access detailed insights relevant to particular regions, segments, or competitive landscapes.

What deliverables can I expect from this HVAC filters market research project?

Deliverables include comprehensive market reports, trend analyses, competitive landscape assessments, regional insights, and segment data. These provide actionable intelligence for informed decision-making.

What are the market trends of HVAC filters?

Current market trends include increasing adoption of energy-efficient filters, growing demand for air purification solutions, and strong shifts towards eco-friendly materials in HVAC filter production.