Robotics And Automation Actuators Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: robotics-and-automation-actuators

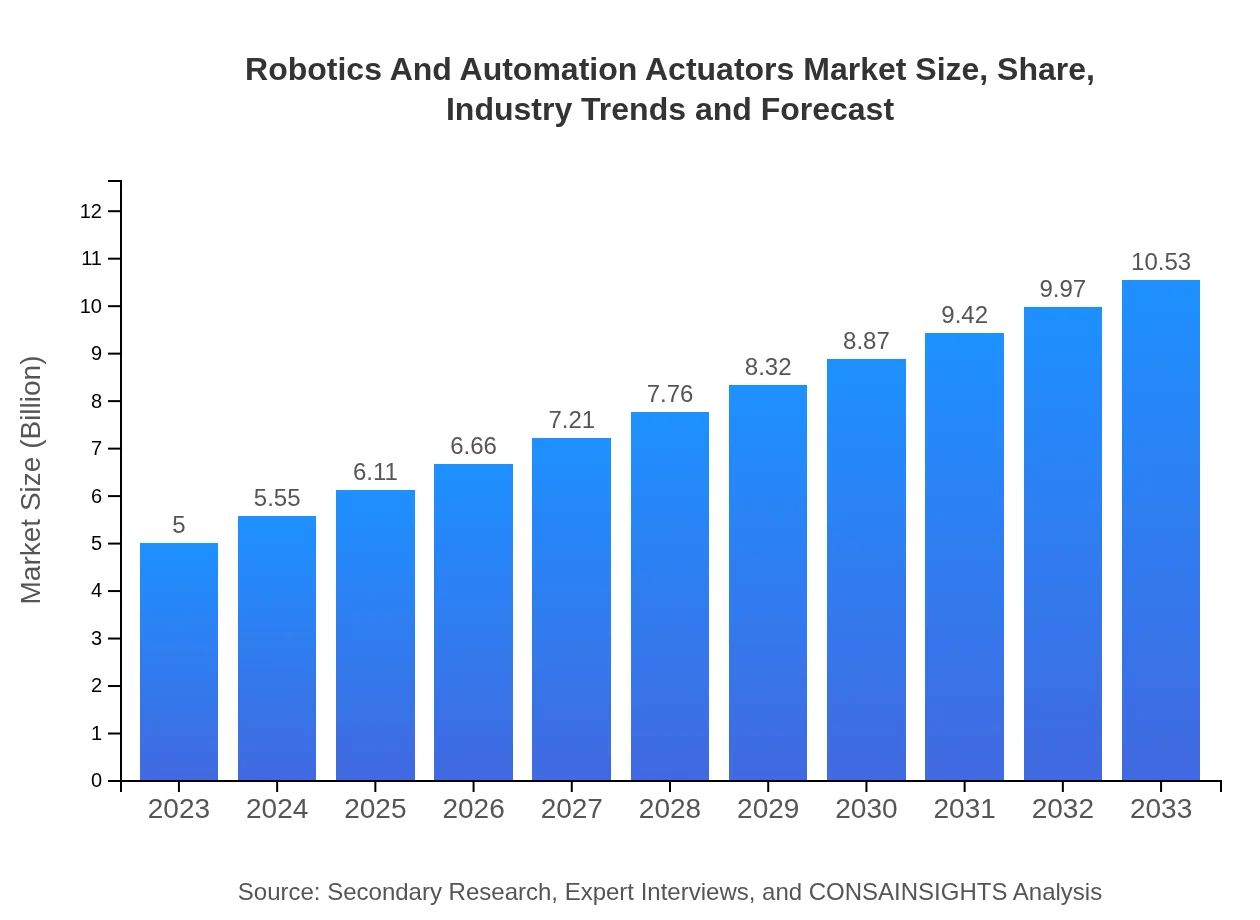

Robotics And Automation Actuators Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report covers the Robotics and Automation Actuators market from 2023 to 2033, providing insights on market size, trends, and regional analyses. The data includes comprehensive analysis, segmentation, and forecasts intended for stakeholders in the robotics and automation industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Siemens AG, FANUC Corporation, Rockwell Automation, Parker Hannifin Corporation |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Robotics And Automation Actuators Market Overview

Customize Robotics And Automation Actuators Market Report market research report

- ✔ Get in-depth analysis of Robotics And Automation Actuators market size, growth, and forecasts.

- ✔ Understand Robotics And Automation Actuators's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Robotics And Automation Actuators

What is the Market Size & CAGR of Robotics And Automation Actuators market in 2023?

Robotics And Automation Actuators Industry Analysis

Robotics And Automation Actuators Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Robotics And Automation Actuators Market Analysis Report by Region

Europe Robotics And Automation Actuators Market Report:

Europe's market is projected to expand from $1.57 billion in 2023 to $3.30 billion in 2033, representing a CAGR of 7.6%. Regulatory support for automation and significant investments in robotics research are driving the market in countries like Germany and the UK.Asia Pacific Robotics And Automation Actuators Market Report:

In the Asia-Pacific region, the Robotics and Automation Actuators market is projected to grow from $0.90 billion in 2023 to $1.89 billion by 2033, reflecting a robust CAGR of 7.6%. The major drivers include rapid industrialization in countries like China and India, which are increasingly adopting automation technologies.North America Robotics And Automation Actuators Market Report:

North America leads with a market size of $1.85 billion in 2023, anticipated to reach $3.90 billion in 2033 at a CAGR of 7.6%. The presence of advanced manufacturing sectors, particularly in the USA and Canada, and significant investment in R&D are major contributing factors.South America Robotics And Automation Actuators Market Report:

The South American market is expected to see growth from $0.34 billion in 2023 to $0.71 billion by 2033, with a CAGR of 7.6%. Economic recovery and infrastructure investments are boosting automation in manufacturing and logistics across South American countries.Middle East & Africa Robotics And Automation Actuators Market Report:

The Middle East and Africa market is set to grow from $0.35 billion in 2023 to $0.73 billion by 2033, with a CAGR of 7.4%. Increased exploration of automation solutions within oil and gas sectors significantly influences this growth.Tell us your focus area and get a customized research report.

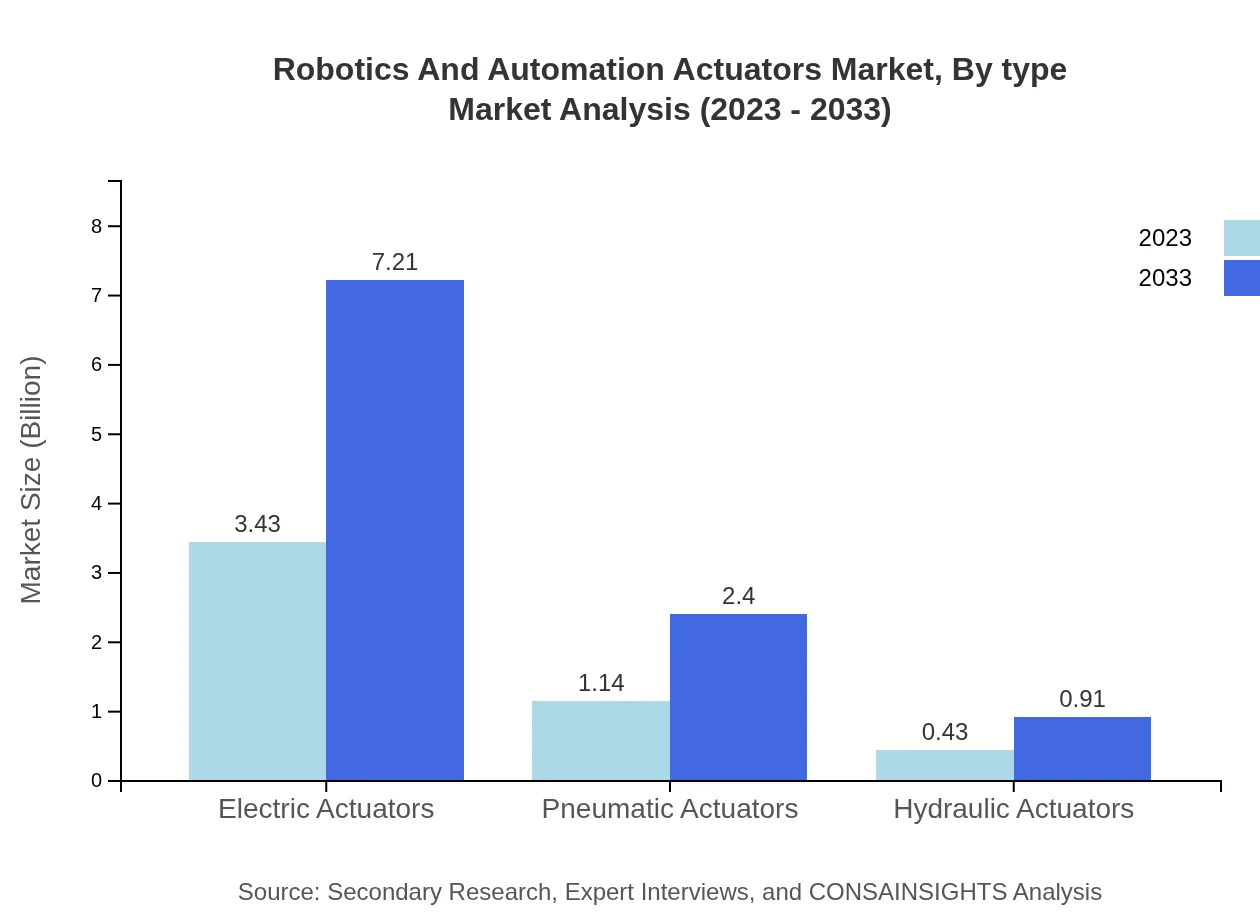

Robotics And Automation Actuators Market Analysis By Type

The market is dominated by Electric Actuators, with a market size growing from $3.43 billion in 2023 to $7.21 billion in 2033. Pneumatic Actuators follow, increasing from $1.14 billion to $2.40 billion within the same period. Hydraulic Actuators contribute with a growth from $0.43 billion to $0.91 billion, indicating diverse applications across different market segments.

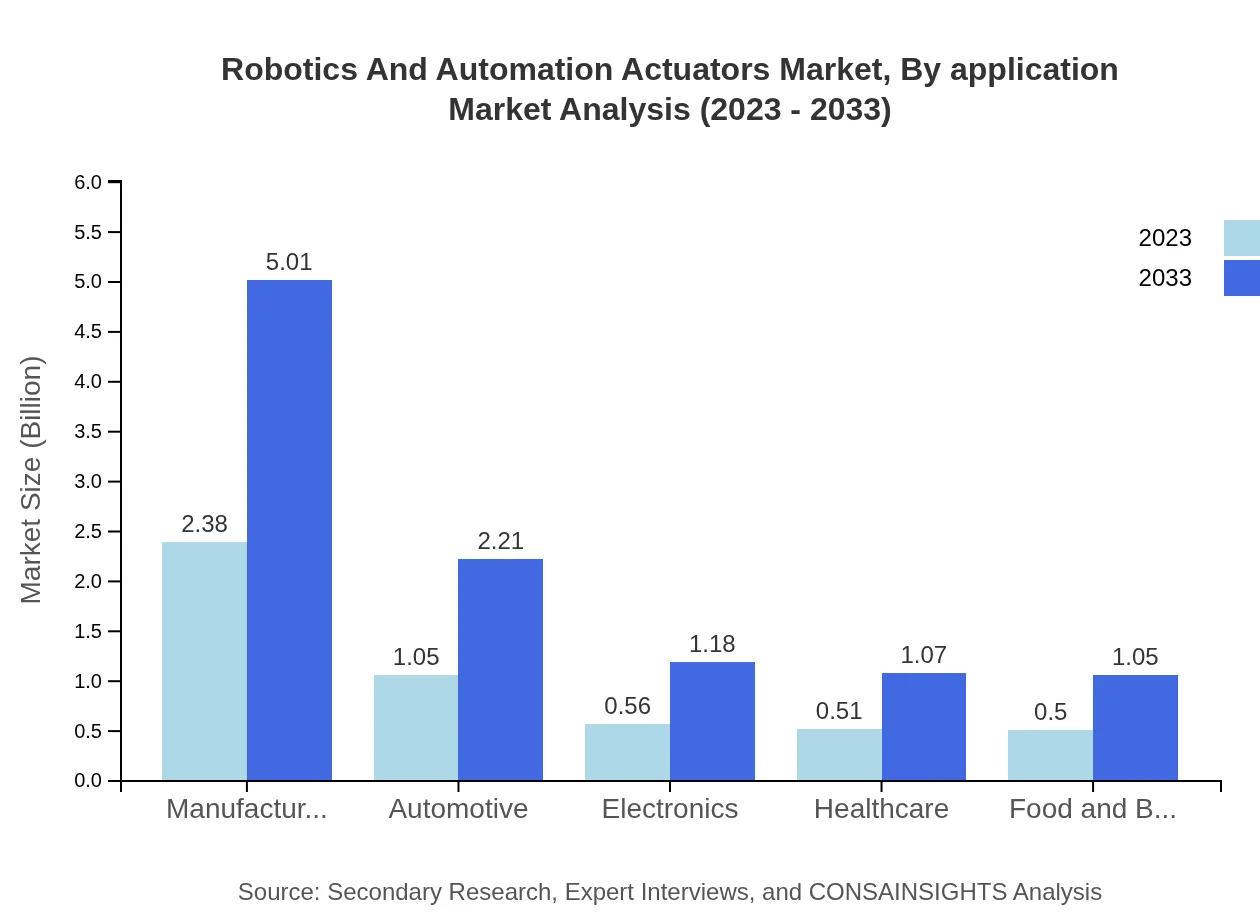

Robotics And Automation Actuators Market Analysis By Application

In terms of application, the Industrial segment leads with a market size of $2.38 billion in 2023, expected to rise to $5.01 billion by 2033. This is followed by Commercial and Residential applications at $1.05 billion (2033) and $0.56 billion (2033), respectively, showcasing the broad applicability of actuators across sectors.

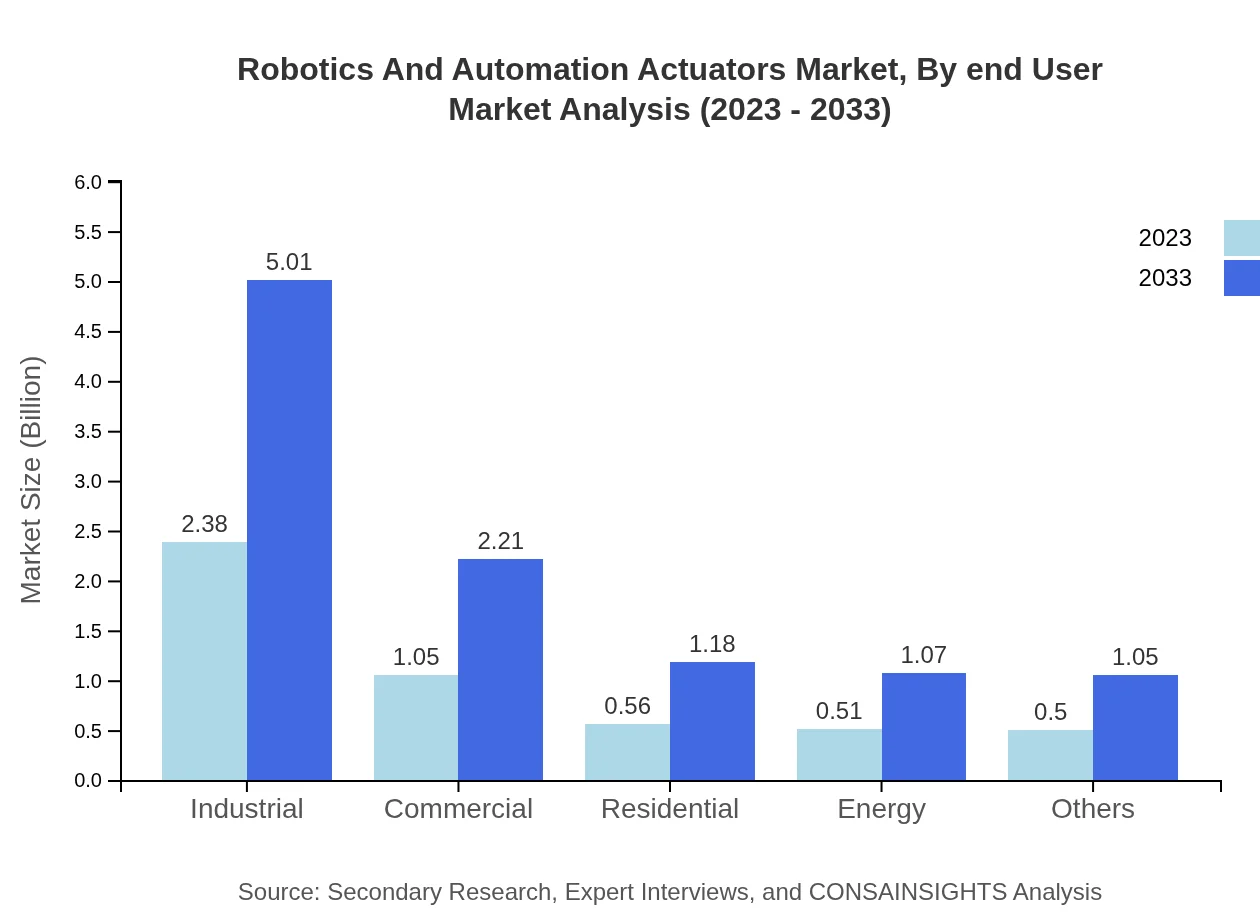

Robotics And Automation Actuators Market Analysis By End User

The Manufacturing sector heavily utilizes Robotics and Automation Actuators, accounting for a size of $2.38 billion in 2023. Other significant end-users include Automotive and Electronics sectors, highlighting the versatile usage of actuators across various industrial applications.

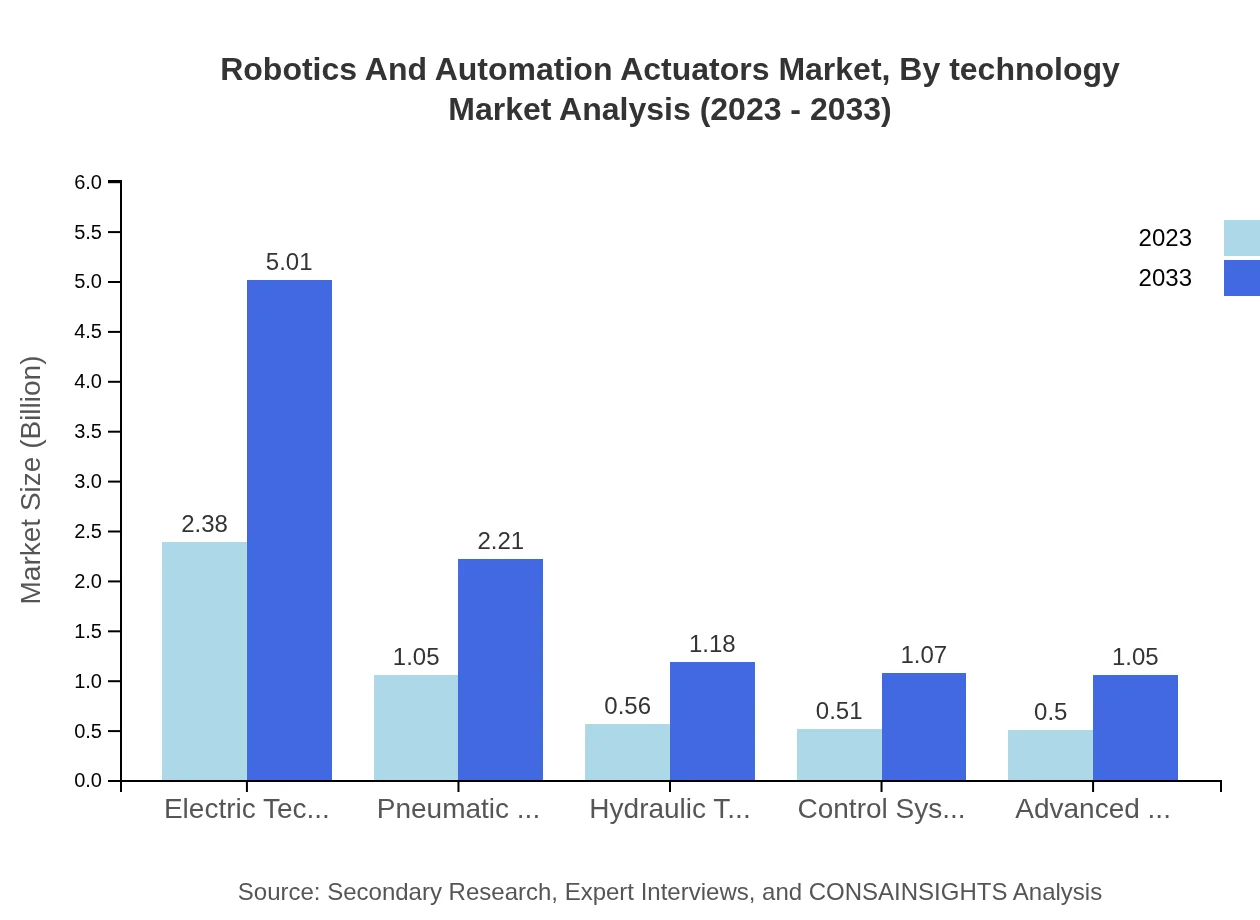

Robotics And Automation Actuators Market Analysis By Technology

The Electric Technology segment ranks highest, expected to grow from $2.38 billion in 2023 to $5.01 billion by 2033, indicating strong interest in energy-efficient solutions. Pneumatic and Hydraulic Technologies also show notable market shares, thereby suggesting a well-rounded development in actuator technology.

Robotics And Automation Actuators Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Robotics And Automation Actuators Industry

Siemens AG:

A leader in automation technology, Siemens specializes in industrial solutions that drive the efficiency of automation processes.FANUC Corporation:

Renowned for its robotics and automation solutions, FANUC leads in robotic manufacturing, including actuators for various applications.Rockwell Automation:

Rockwell focuses on industrial automation, offering state-of-the-art actuator technologies that streamline operations.Parker Hannifin Corporation:

A major player in motion and control technologies, Parker provides innovative actuator solutions for multiple sectors.We're grateful to work with incredible clients.

FAQs

What is the market size of Robotics and Automation Actuators?

The Robotics and Automation Actuators market has an estimated size of $5 billion in 2023, projected to grow at a CAGR of 7.5% towards 2033, enhancing its significance in automation and robotics.

What are the key market players or companies in the Robotics and Automation Actuators industry?

Key players in the Robotics and Automation Actuators industry include companies like Siemens AG, Parker Hannifin Corporation, Festo AG & Co. KG, and SMC Corporation, who are continuously innovating and expanding their product portfolios.

What are the primary factors driving the growth in the Robotics and Automation Actuators industry?

Factors driving growth include increasing demand for automation in various industries, advancements in robotics technology, greater efficiency and productivity requirements, and the rising need for safety and precision in manufacturing processes.

Which region is the fastest Growing in the Robotics and Automation Actuators?

The Asia Pacific region is experiencing rapid growth in the Robotics and Automation Actuators market, expected to surge from $0.90 billion in 2023 to $1.89 billion by 2033, fueled by increased industrial automation.

Does ConsaInsights provide customized market report data for the Robotics and Automation Actuators industry?

Yes, ConsaInsights offers customized market report data tailored to client-specific research needs in the Robotics and Automation Actuators industry, ensuring relevant insights and detailed information.

What deliverables can I expect from this Robotics and Automation Actuators market research project?

Deliverables include comprehensive market reports, detailed trend analyses, competitive landscape evaluations, and actionable insights on industry segments, designed to assist stakeholders in strategic planning.

What are the market trends of Robotics and Automation Actuators?

Key trends include the increasing adoption of electric actuators, innovation in automation technology, a rise in demand for smart manufacturing solutions, and a shift towards sustainable actuator designs.