Industrial Valves Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: industrial-valves

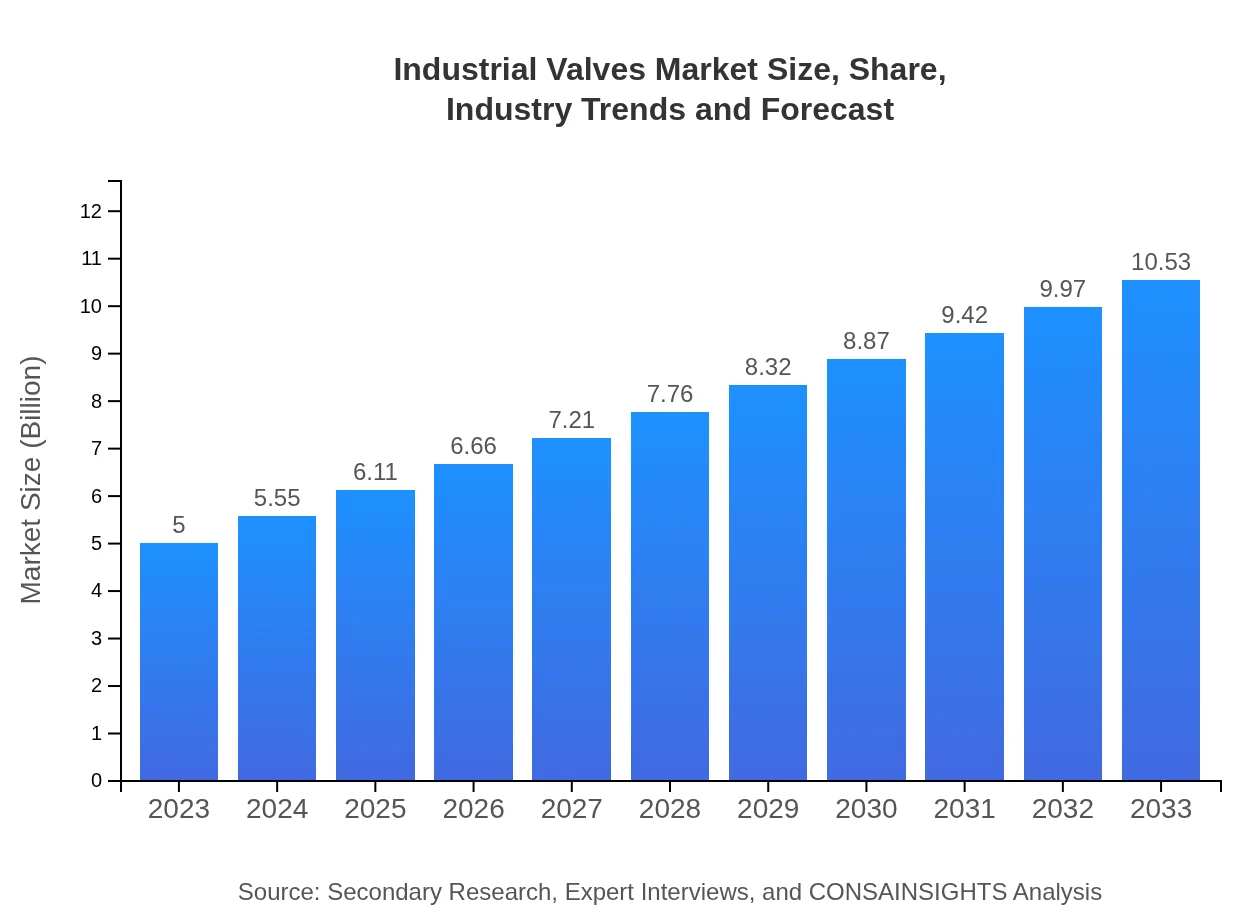

Industrial Valves Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides an in-depth analysis of the Industrial Valves market covering market size, industry trends, segmentation, regional insights, and future forecasts from 2023 to 2033, offering valuable insights for stakeholders and decision-makers.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Emerson Electric Co., Flowserve Corporation, Baker Hughes Company, Parker Hannifin Corporation, Kitz Corporation |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Industrial Valves Market Overview

Customize Industrial Valves Market Report market research report

- ✔ Get in-depth analysis of Industrial Valves market size, growth, and forecasts.

- ✔ Understand Industrial Valves's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Industrial Valves

What is the Market Size & CAGR of the Industrial Valves market in 2023?

Industrial Valves Industry Analysis

Industrial Valves Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Industrial Valves Market Analysis Report by Region

Europe Industrial Valves Market Report:

The European market is valued at approximately $1.39 billion in 2023, and it is forecasted to reach $2.94 billion by 2033. With stringent regulations on water and waste management, the demand for high-quality valves in this region is expected to rise.Asia Pacific Industrial Valves Market Report:

The Asia Pacific region is expected to witness significant growth due to rapid industrialization and urbanization. In 2023, the market size is estimated at $0.95 billion, growing to approximately $2.01 billion by 2033. Key industries include energy, manufacturing, and water management, driving demand for valves.North America Industrial Valves Market Report:

North America holds a substantial share of the Industrial Valves market, with a size of $1.90 billion in 2023, projected to nearly double, reaching $3.99 billion by 2033. The booming oil and gas sector, as well as advancements in the manufacturing sector, contribute significantly to this growth.South America Industrial Valves Market Report:

In South America, the market for Industrial Valves stands at around $0.49 billion in 2023 and is expected to grow to $1.03 billion by 2033. The growth is propelled by investments in infrastructure and a growing manufacturing base.Middle East & Africa Industrial Valves Market Report:

The Middle East and Africa market is currently valued at $0.27 billion in 2023, with expectations to grow to $0.57 billion by 2033. The growth is primarily driven by the oil and gas industry and ongoing infrastructure projects.Tell us your focus area and get a customized research report.

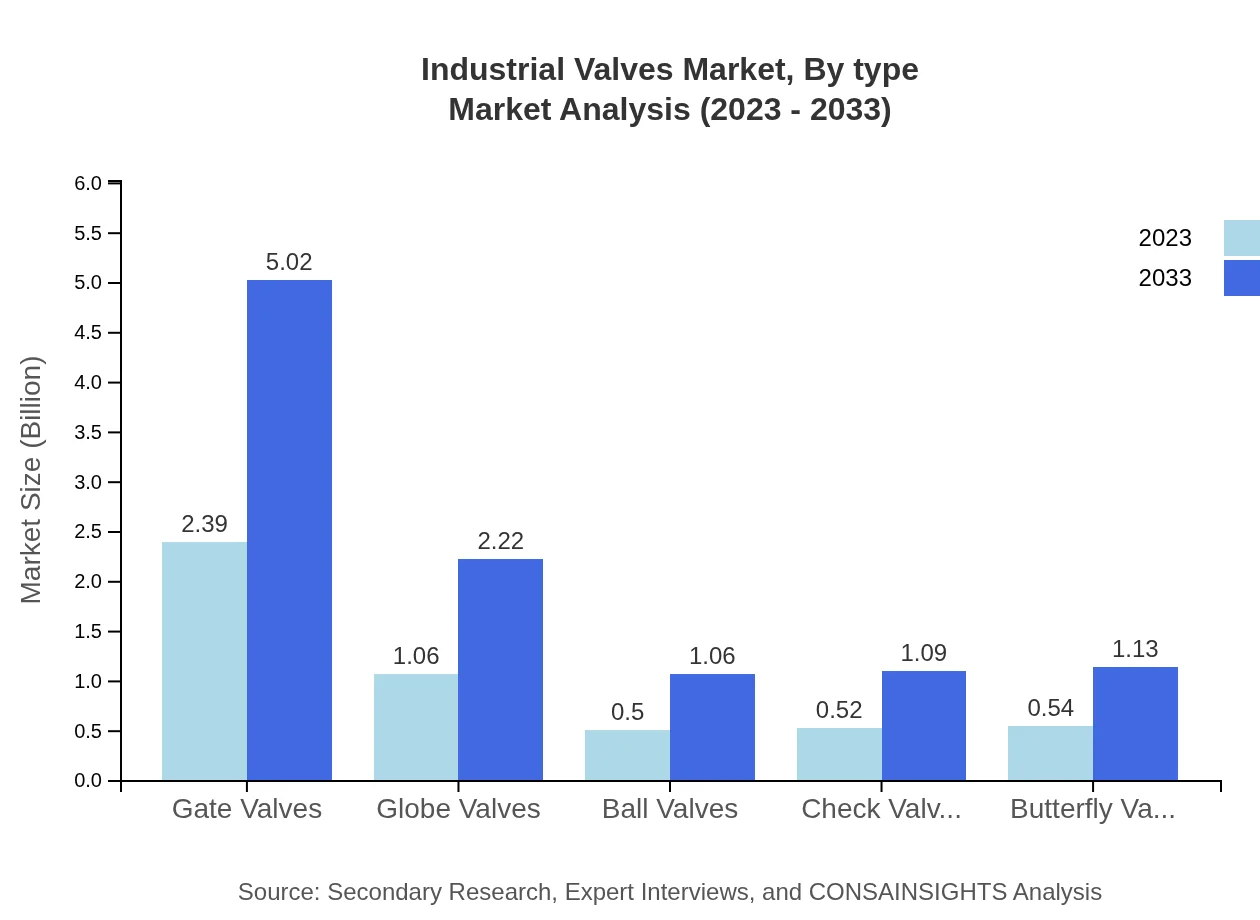

Industrial Valves Market Analysis By Type

In the market segmented by type: - Gate Valves size is projected to grow from $2.39 billion in 2023 to $5.02 billion by 2033, retaining a market share of 47.71%. - Globe Valves are expected to grow from $1.06 billion to $2.22 billion, holding 21.1% market share. - Ball Valves will increase from $0.50 billion to $1.06 billion, maintaining a 10.05% share. - Check Valves are anticipated to grow from $0.52 billion to $1.09 billion, with a 10.38% share. - Butterfly Valves will increase from $0.54 billion to $1.13 billion, holding a 10.76% share.

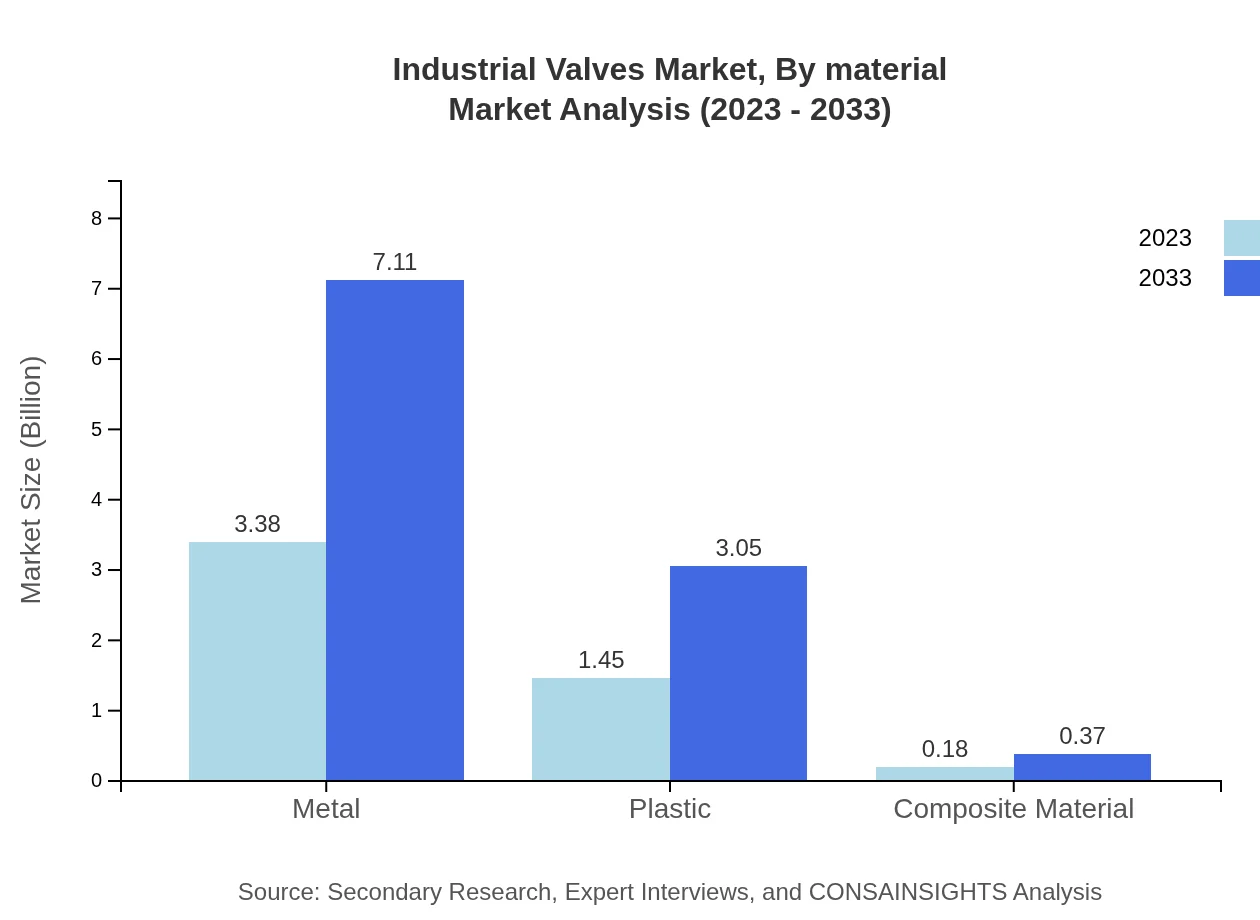

Industrial Valves Market Analysis By Material

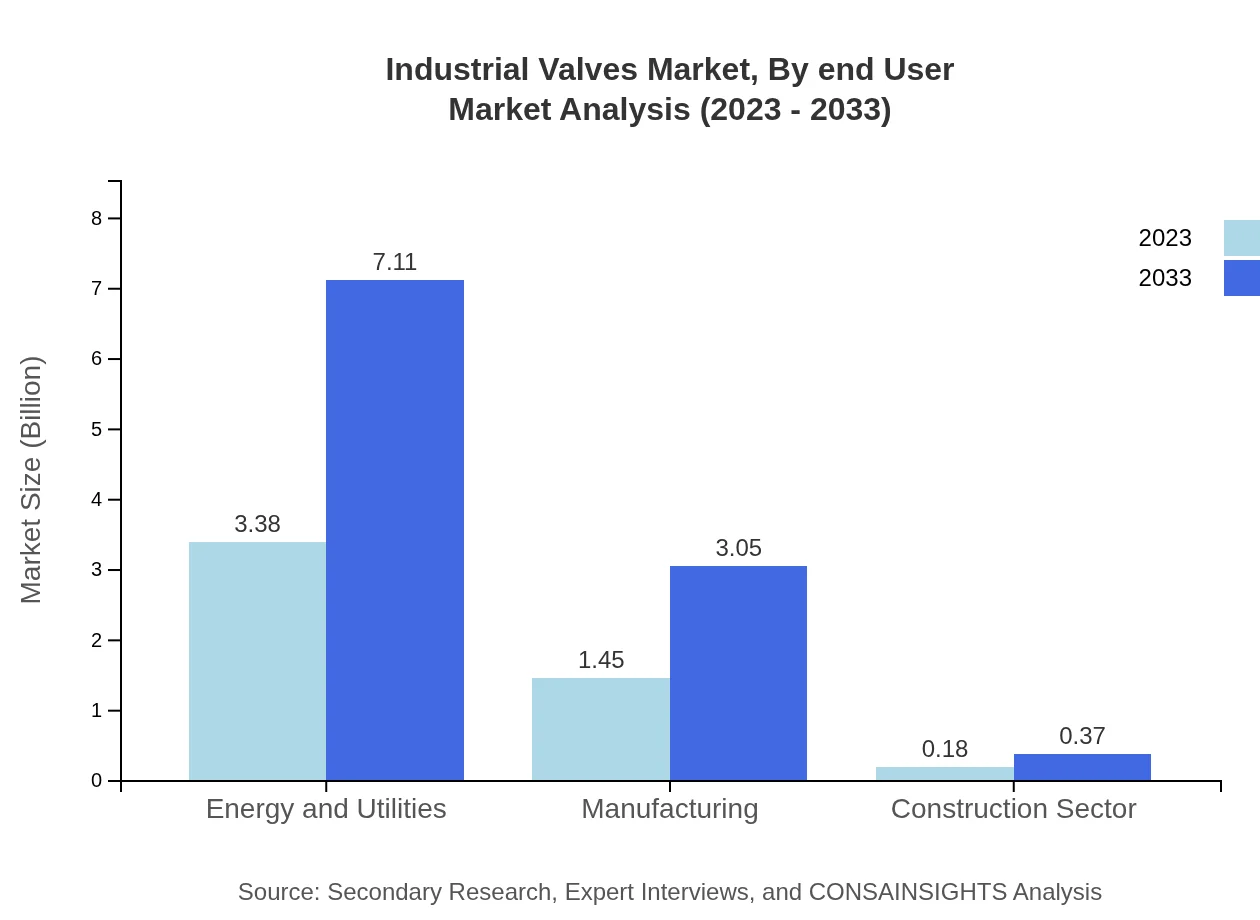

The valuation based on material: - The Metal segment is projected to grow significantly, from $3.38 billion in 2023 to $7.11 billion by 2033 with a share of 67.51%. - The Plastic segment is expected to increase from $1.45 billion to $3.05 billion, maintaining a 28.94% share. - The Composite Material segment will see growth from $0.18 billion to $0.37 billion, with 3.55% market share.

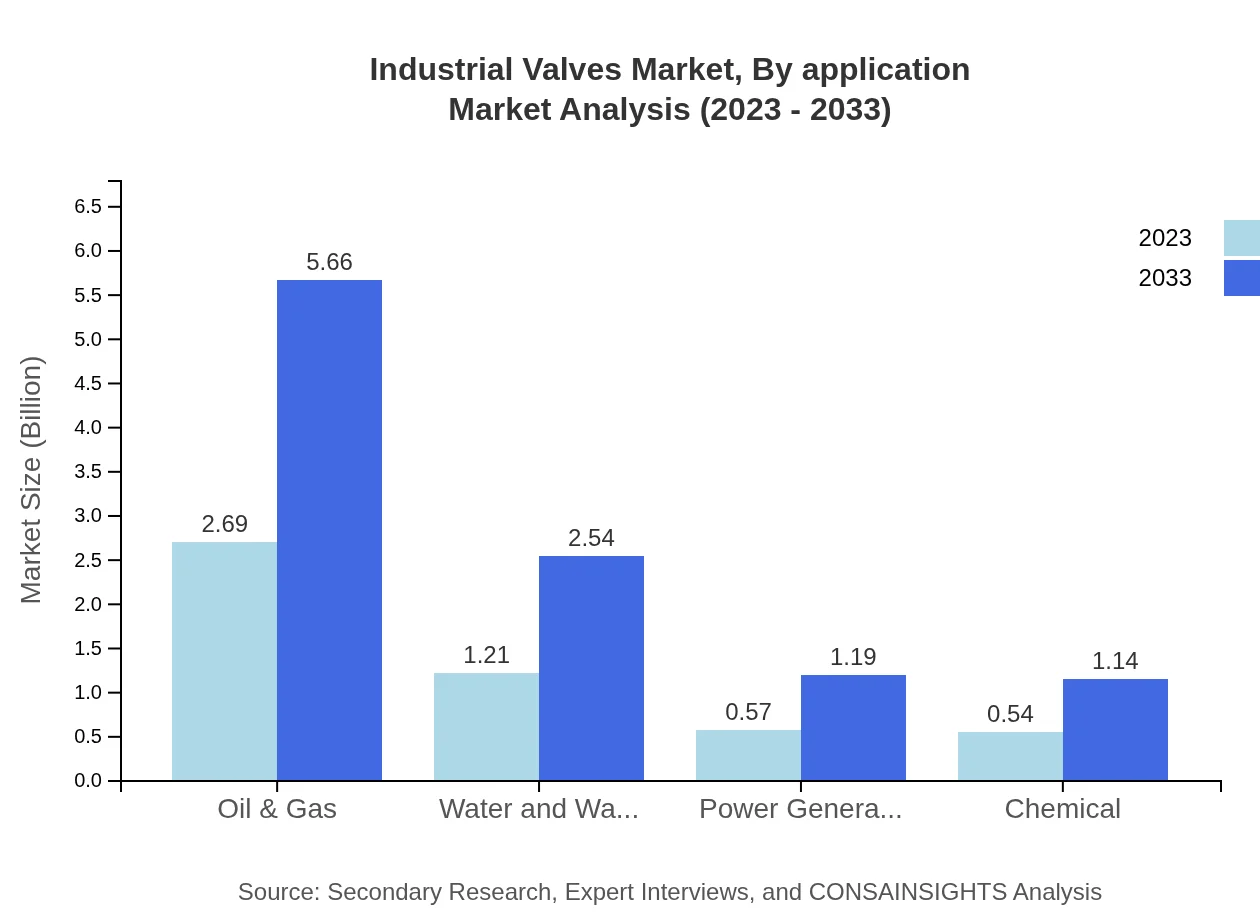

Industrial Valves Market Analysis By Application

Market performance by application: - The Energy and Utilities segment will grow from $3.38 billion to $7.11 billion, holding a significant share of 67.51%. - Manufacturing will increase its market size from $1.45 billion to $3.05 billion, accounting for 28.94%. - Other sectors like Oil & Gas, Water Management, and Power Generation are also contributing to the overall growth.

Industrial Valves Market Analysis By End User

- The Industrial end-user segment is growing, with increasing demand across manufacturing sectors. - Commercial usage of industrial valves is rising with infrastructure projects. - Residential use, while smaller, is also seeing a gradual increase, particularly in smart home technologies.

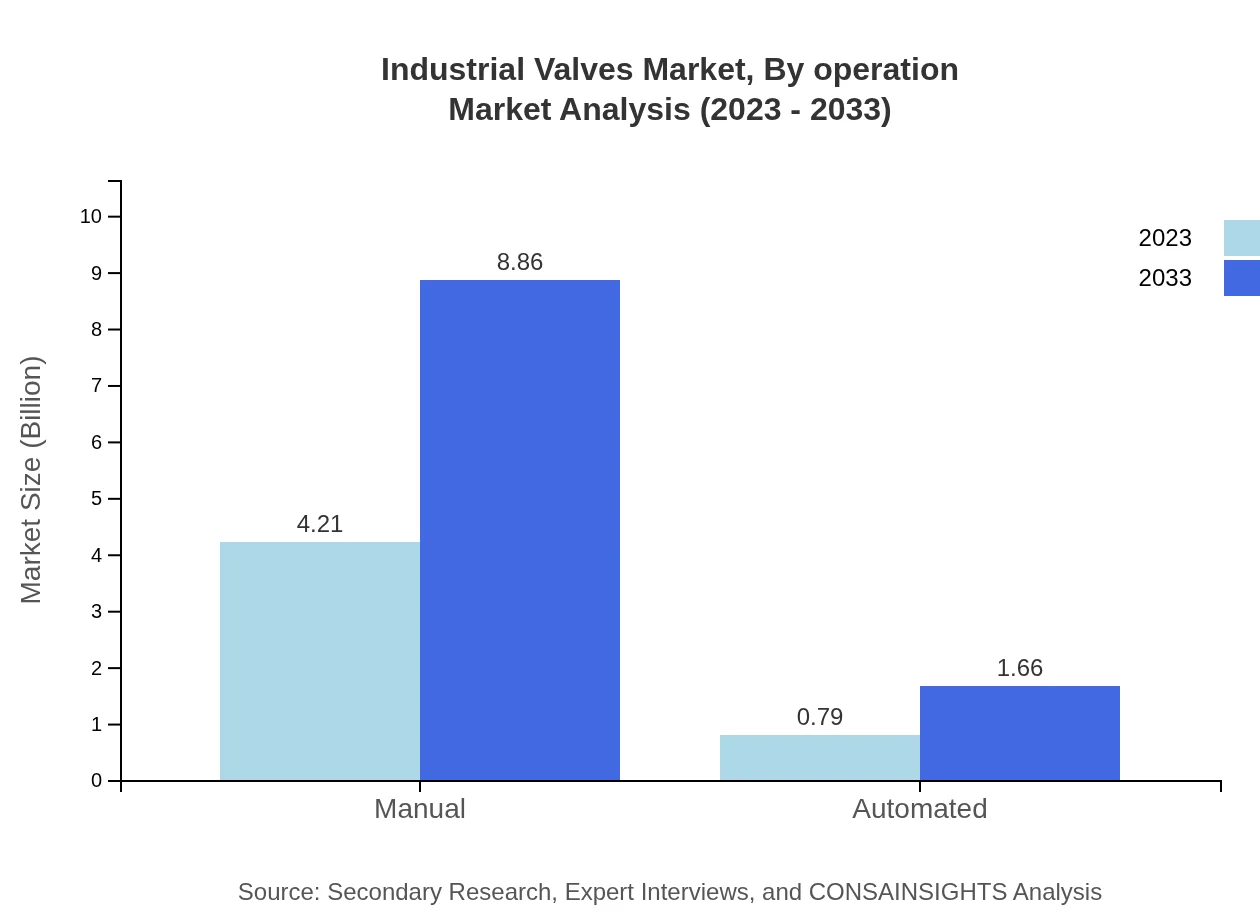

Industrial Valves Market Analysis By Operation

- The Manual valve operation segment accounts for a large share, anticipated to expand from $4.21 billion to $8.86 billion, representing 84.22% of the market. - The Automated segment is expected to grow from $0.79 billion to $1.66 billion, making up 15.78% of the market.

Industrial Valves Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Industrial Valves Industry

Emerson Electric Co.:

A global leader in automation and valves, providing innovative solutions for operational efficiency and sustainability.Flowserve Corporation:

Specializes in the manufacturing and servicing of industrial valves, pumps, and seals, focusing on high-performance and durable products.Baker Hughes Company:

A major player in the oil and gas sector, offering advanced valves that enhance efficiency and performance in critical applications.Parker Hannifin Corporation:

Provides a diverse range of high-quality valves for various applications, focusing on precision and durability.Kitz Corporation:

Global manufacturer of industrial valves committed to quality and performance, catering to various industries.We're grateful to work with incredible clients.

FAQs

What is the market size of industrial valves?

The industrial valves market is projected to grow from $5 billion in 2023 to significant levels by 2033, with a CAGR of 7.5%. This growth reflects rising demand across various industries.

What are the key market players or companies in this industrial valves industry?

Key players in the industrial valves market include leading manufacturers such as Flowserve Corporation, Emerson Electric Co., and Valmet Oyj. These companies have established strong market presence through innovation and extensive distribution networks.

What are the primary factors driving the growth in the industrial valves industry?

The growth in the industrial valves industry is driven by increasing industrialization, demand for automation, and stringent regulations for waste management. Additionally, expansion in the oil and gas sector significantly contributes to market growth.

Which region is the fastest Growing in the industrial valves market?

The Asia Pacific region is the fastest-growing market for industrial valves, expected to increase from $0.95 billion in 2023 to $2.01 billion by 2033. This growth is fueled by rapid industrial development in countries like China and India.

Does ConsaInsights provide customized market report data for the industrial valves industry?

Yes, ConsaInsights offers customized market report data for the industrial valves industry, catering to specific client needs and providing insights tailored to unique market segments and geographic areas.

What deliverables can I expect from this industrial valves market research project?

Deliverables from the industrial valves market research project include comprehensive market analysis, detailed segmentation data, competitive landscape insights, and region-specific forecasts, equipping stakeholders with essential information for strategic decision-making.

What are the market trends of industrial valves?

Current trends in the industrial valves market include a shift towards automation, innovation in valve materials, and increasing investment in sustainable technologies. As industries evolve, manufacturers are adapting their products to enhance efficiency.