Reports >

Life Sciences

>

Operating Room Cameras Market Report

Operating Room Cameras Market Report

First published: 08 October 2024 | Last updated: 25 May 2026 | Report Code: operating-room-cameras

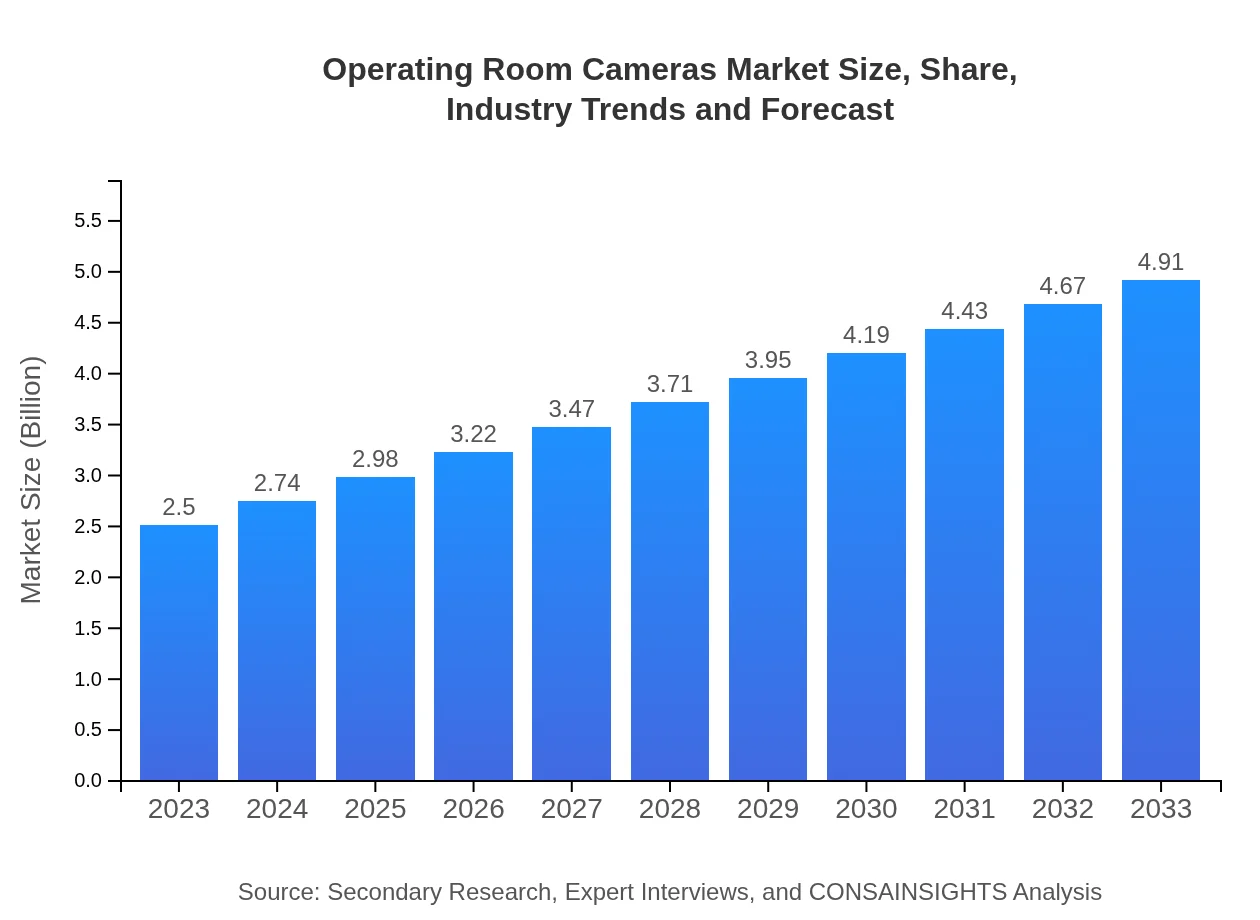

Operating Room Cameras Market — USD 2.5 billion in 2023, Growing to USD 4.91B by 2033 at 6.8% CAGR

This report provides an in-depth analysis of the Operating Room Cameras market, focusing on the current trends, market size, growth forecasts, and key players from 2023 to 2033. It offers insights into technology advancements, regional performance, and future challenges.

Key Takeaways

- Global market expands from $2.50 Billion in 2023 to $4.91 Billion in 2033 at a 6.8% CAGR.

- North America is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- Digital and 3D imaging adoption, along with investments in healthcare facilities, underpin demand for advanced camera systems.

- Hospitals, ambulatory surgery centers and academic institutions remain primary end-users for fixed, mobile and integrated camera solutions.

- Major vendors such as Olympus Corporation, Stryker Corporation and Karl Storz GmbH influence product innovation and market activity.

Operating Room Cameras Market Report — Executive Summary

North America remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. This report examines the Operating Room Cameras market across a ten-year outlook, noting a trajectory from $2.50 Billion in 2023 to $4.91 Billion by 2033 at a 6.8% CAGR. Growth is supported by a shift from analog to digital and 3D imaging, heightened demand for enhanced surgical visualization, and rising investments in healthcare infrastructure. North America is identified as the largest regional market, with strong expansions in Europe and Asia Pacific also documented. Product categories include fixed cameras, mobile cameras and integrated systems, used across hospitals, ambulatory surgery centers and academic institutions. Key players such as Olympus Corporation, Stryker Corporation, Karl Storz GmbH, Smith & Nephew and George M. Sharp, Inc. are active in technology upgrades and partnerships. Regulatory requirements and the ongoing trend toward minimally invasive procedures further shape procurement and product development priorities. The study combines expert interviews and secondary sources to present a validated view of market dynamics, segmentation and regional distributions.

Key Growth Drivers

- Transition from analog systems to digital and 3D imaging enhances image clarity and drives replacement cycles.

- Increased capital expenditure on healthcare infrastructure supports purchases of advanced operating room visualization equipment.

- Demand for minimally invasive procedures boosts need for precise surgical imaging and documentation solutions.

- Hospitals and specialized surgical centers upgrading equipment portfolios prioritize integrated and mobile camera systems.

- Vendor innovation and partnerships accelerate feature development and commercial availability of next-generation cameras.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $2.50 Billion |

| CAGR (2023-2033) | 6.8% |

| 2033 Market Size | $4.91 Billion |

| Top Companies | Olympus Corporation, Stryker Corporation, Karl Storz GmbH, Smith & Nephew, George M. Sharp, Inc. |

| Published Date | 08 October 2024 |

| Last Modified Date | 25 May 2026 |

Operating Room Cameras Market Overview

Customize Operating Room Cameras Market Report market research report

- ✔ Get in-depth analysis of Operating Room Cameras market size, growth, and forecasts.

- ✔ Understand Operating Room Cameras's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Operating Room Cameras

What is the Market Size & CAGR of Operating Room Cameras Market Report market in 2023?

Operating Room Cameras Industry Analysis

Operating Room Cameras Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Operating Room Cameras Market Report Market Analysis Report by Region

Europe Operating Room Cameras Market Report:

Europe grows from $0.72 Billion in 2023 to $1.41 Billion in 2033. Growth is associated with modernization of operating rooms, regulatory-driven quality standards and a shift toward digital and 3D camera technologies in surgical centers.Asia Pacific Operating Room Cameras Market Report:

Asia Pacific grows from $0.52 Billion in 2023 to $1.03 Billion in 2033. Regional gains are tied to expanding healthcare capacity, rising demand for minimally invasive surgeries and gradual uptake of digital imaging systems.North America Operating Room Cameras Market Report:

North America is largest regional market, rising from $0.85 Billion in 2023 to $1.67 Billion in 2033. This expansion aligns with regional investments in hospital infrastructure and adoption of advanced imaging solutions to support complex surgical procedures.South America Operating Room Cameras Market Report:

Latin America grows from $0.18 Billion in 2023 to $0.34 Billion in 2033. Market progression is influenced by targeted investments in medical facilities and increasing procurement of visualization equipment for surgical care.Middle East & Africa Operating Room Cameras Market Report:

Middle East and Africa grows from $0.23 Billion in 2023 to $0.46 Billion in 2033. Growth drivers include upgrades to clinical infrastructure and adoption of improved operating room imaging to support evolving surgical practices.Tell us your focus area and get a customized research report.

Research Methodology

Operating Room Cameras Market Analysis By Type

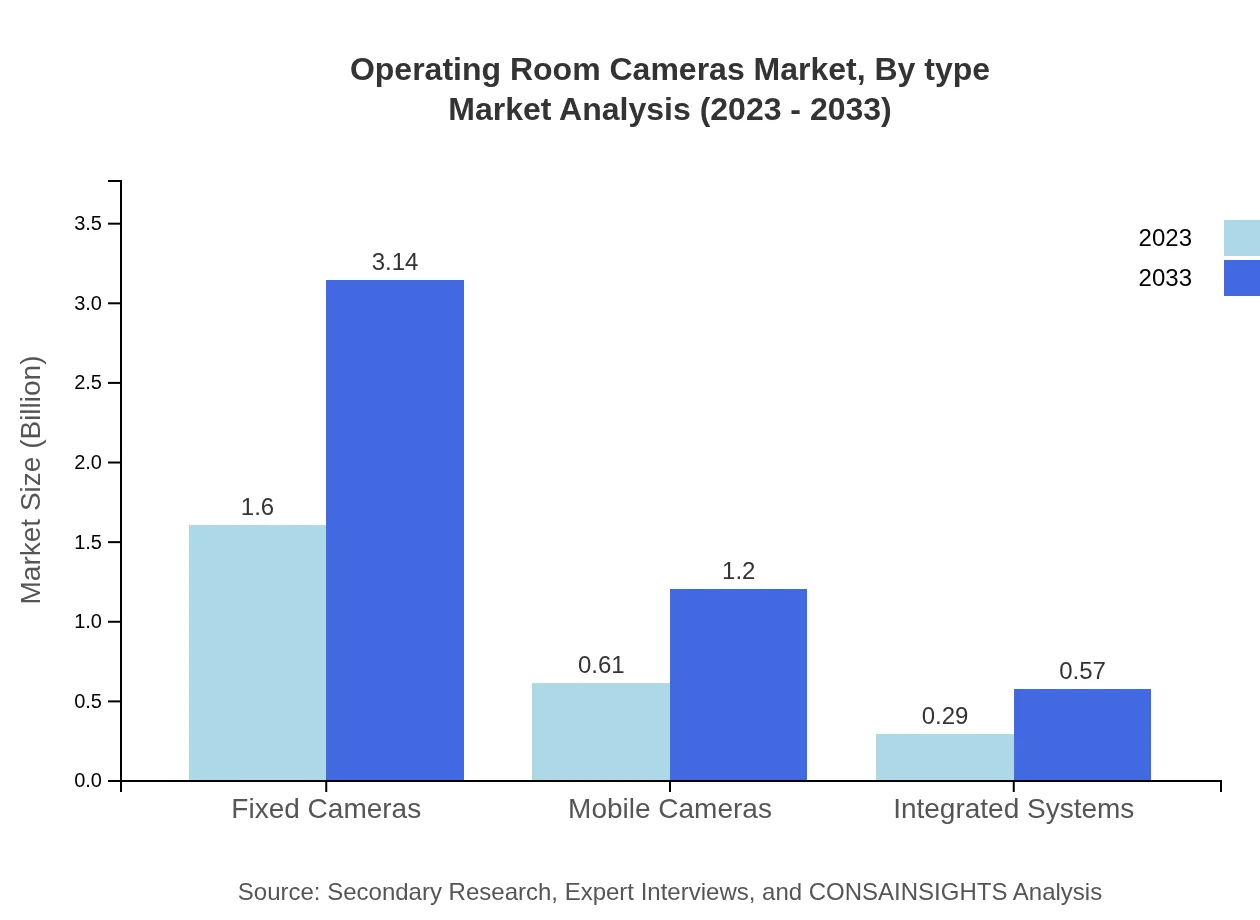

By type, the Fixed Cameras segment dominates the market, valued at $1.60 billion in 2023, with a projected growth to $3.14 billion by 2033, holding a 64% market share. Mobile Cameras, valued at $0.61 billion in 2023, are set to double to $1.20 billion by 2033, maintaining a 24.42% share. Integrated Systems follow, with a valuation of $0.29 billion in 2023, expected to grow to $0.57 billion by 2033, holding 11.58% market share.

Operating Room Cameras Market Analysis By Technology

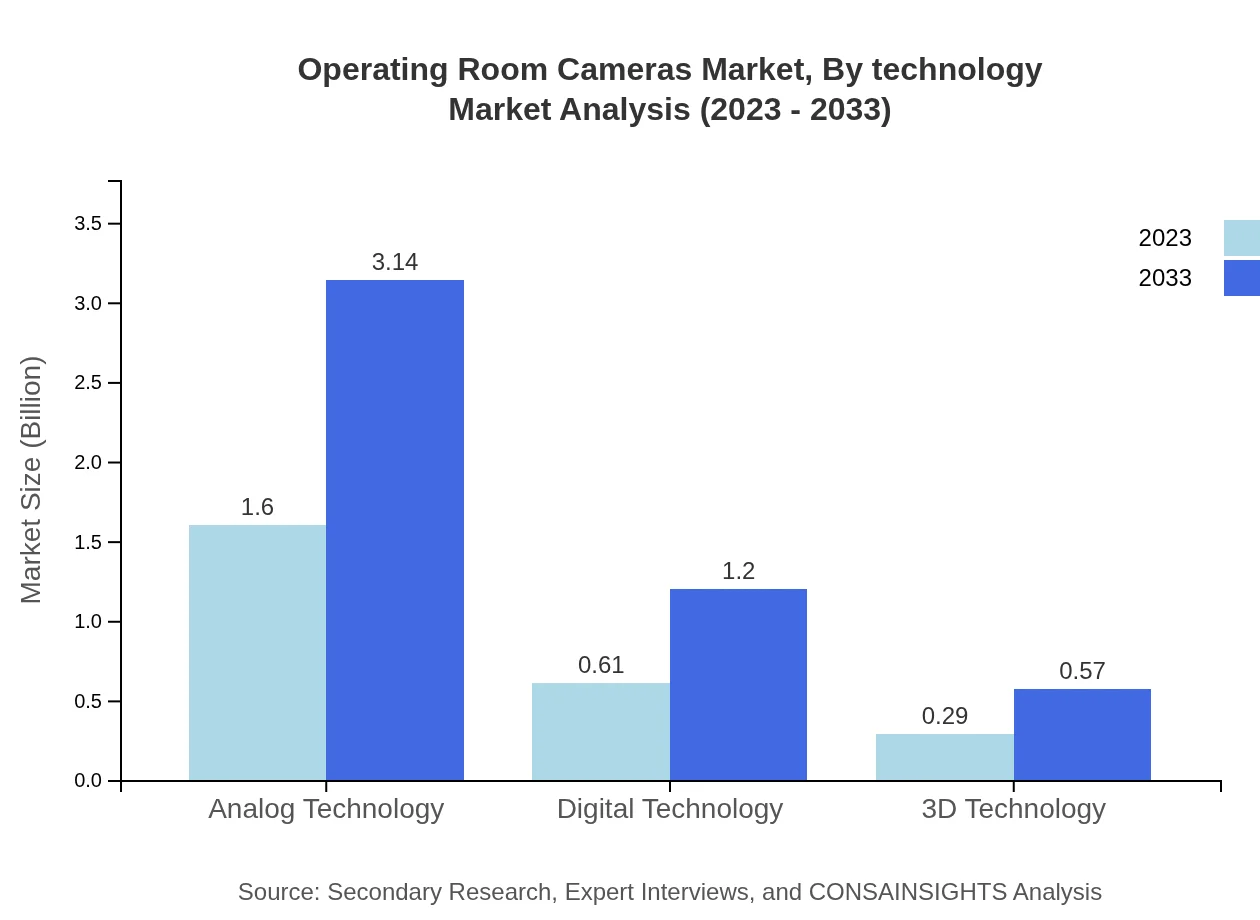

In terms of technology, Analog Technology continues to lead with a market size of $1.60 billion in 2023 and is expected to reach $3.14 billion by 2033, commanding a 64% market share. Digital Technology is growing robustly, projected from $0.61 billion to $1.20 billion, at a 24.42% share, followed by 3D Technology, forecasted to expand from $0.29 billion to $0.57 billion with an 11.58% share.

Operating Room Cameras Market Analysis By Application

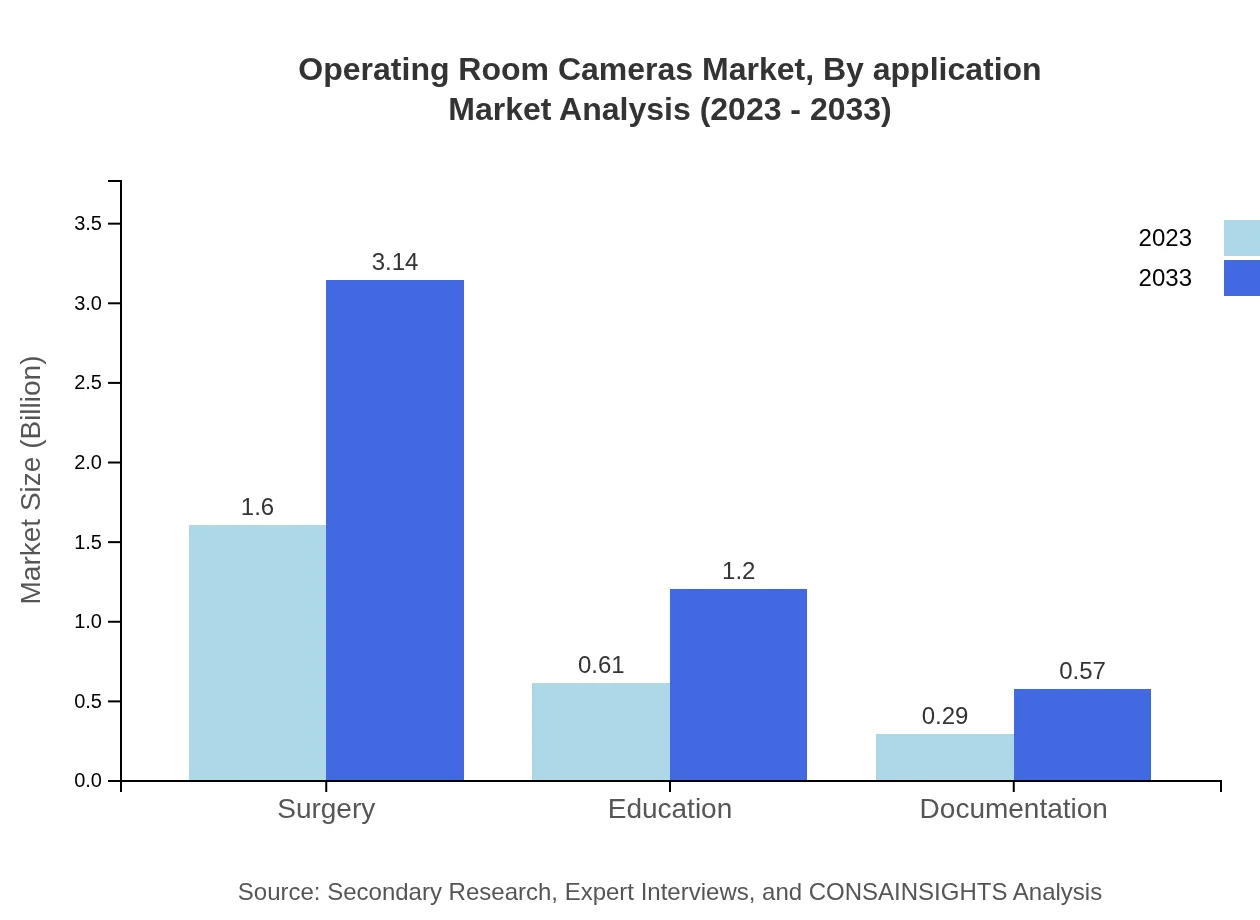

The market by application shows Surgery as a dominant segment with a valuation of $1.60 billion in 2023, and it is projected to grow to $3.14 billion with a 64% share, followed by Education at $0.61 billion growing to $1.20 billion with a share of 24.42%. Documentation needs represent a smaller segment, moving from $0.29 billion to $0.57 billion, reflecting its 11.58% share.

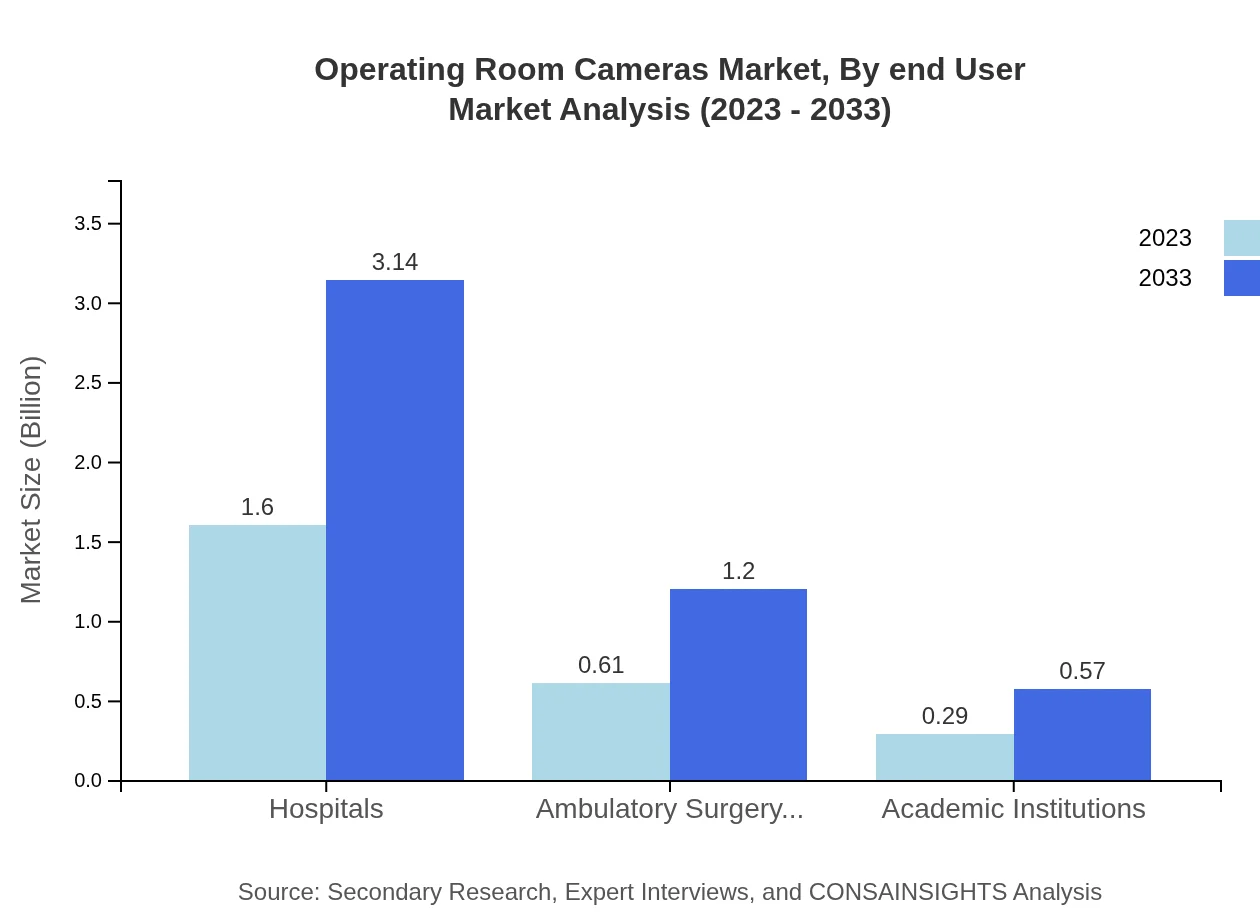

Operating Room Cameras Market Analysis By End User

Hospitals lead the end-user market, valued at $1.60 billion in 2023 and growing to $3.14 billion with a 64% share. Ambulatory Surgery Centers follow, expected to grow from $0.61 billion to $1.20 billion, holding a share of 24.42%. Academic Institutions hold a share of 11.58%, evolving from $0.29 billion to $0.57 billion during the same period.

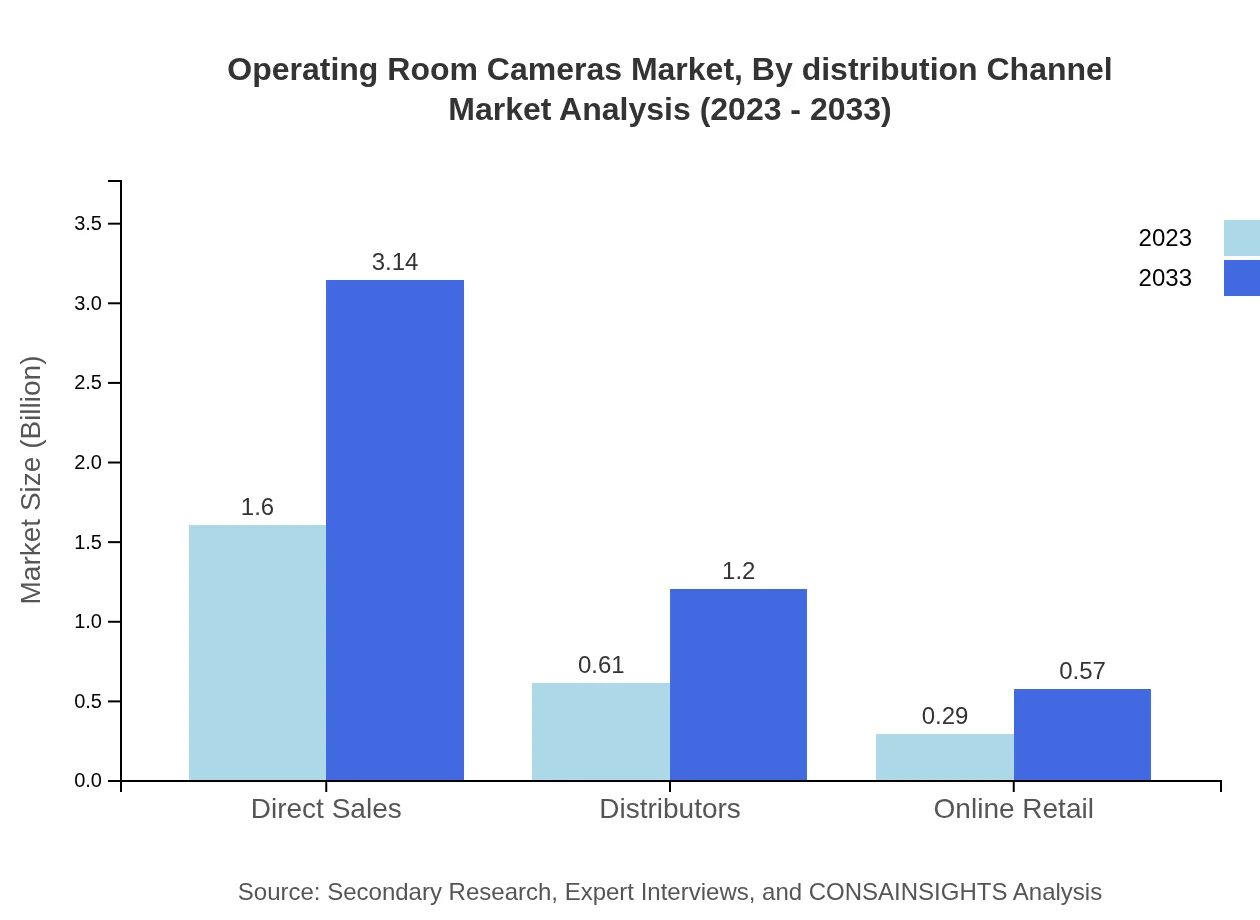

Operating Room Cameras Market Analysis By Distribution Channel

Direct Sales dominate distribution channels, with a size of $1.60 billion in 2023, projected at $3.14 billion with a consistent 64% share. Distributors are expected to grow from $0.61 billion to $1.20 billion, maintaining a 24.42% share, while Online Retail reflects a smaller segment, growing from $0.29 billion to $0.57 billion, holding 11.58% of the market.

Operating Room Cameras Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Operating Room Cameras Industry

Olympus Corporation:

Olympus is a leader in creating innovative imaging and optical technology, focusing on surgical equipment and operating room cameras that enhance visualization for better surgical outcomes.Stryker Corporation:

Known for its advanced medical devices, Stryker provides high-quality operating room cameras and solutions aimed at improving surgical prowess and patient safety.Karl Storz GmbH:

Karl Storz specializes in endoscopic instruments and equipment, offering sophisticated operating room camera systems that integrate seamlessly with surgical workflows.Smith & Nephew:

Smith & Nephew is a global medical technology company that provides innovative operating room cameras as part of its surgical portfolio, focusing on minimally invasive procedures.George M. Sharp, Inc.:

They are known for providing management and consultation services for surgical technologies including operating room cameras, enhancing surgical efficacy across facilities.We're grateful to work with incredible clients.

FAQs

What is the market size of the Operating Room Cameras market in 2023?

The market size for 2023 is $2.50 Billion, as stated in the report's baseline year figure for global operating room camera revenues.

How big is the market expected to be in 2033?

The market is expected to reach $4.91 Billion by 2033 according to the report's forecast for the end of the projection period.

What is CAGR for the forecast period?

The reported compound annual growth rate for the 2023 to 2033 forecast period is 6.8%.

Is there a single fastest Growing region in the Operating Room Cameras Market Report market?

No single fastest-growing region is stated for the Operating Room Cameras Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Which companies are listed as top players?

Top companies named in the report include Olympus Corporation, Stryker Corporation, Karl Storz GmbH, Smith & Nephew, and George M. Sharp, Inc.

What primary trends are influencing market growth?

Key trends include migration to digital and 3D imaging, enhanced surgical visualization, and investment in minimally invasive procedure support technologies.

How are end User segments defined?

End-user segments cited are hospitals, ambulatory surgery centers and academic institutions, representing primary purchasers of operating room camera systems.

What research methods supported the report?

The study used primary interviews with industry experts, secondary company reports and publications, plus data triangulation and internal validation.

What types of camera systems are covered?

The report covers fixed cameras, mobile cameras and integrated systems as the main product type groupings analyzed.

Why are digital and 3D technologies important?

Digital and 3D technologies improve image clarity and operational efficiency, supporting surgical outcomes and encouraging adoption in operating rooms.