Reports >

Life Sciences

>

Sleep Tech Devices Market Report

Sleep Tech Devices Market Report

First published: 11 October 2024 | Last updated: 28 May 2026 | Report Code: sleep-tech-devices

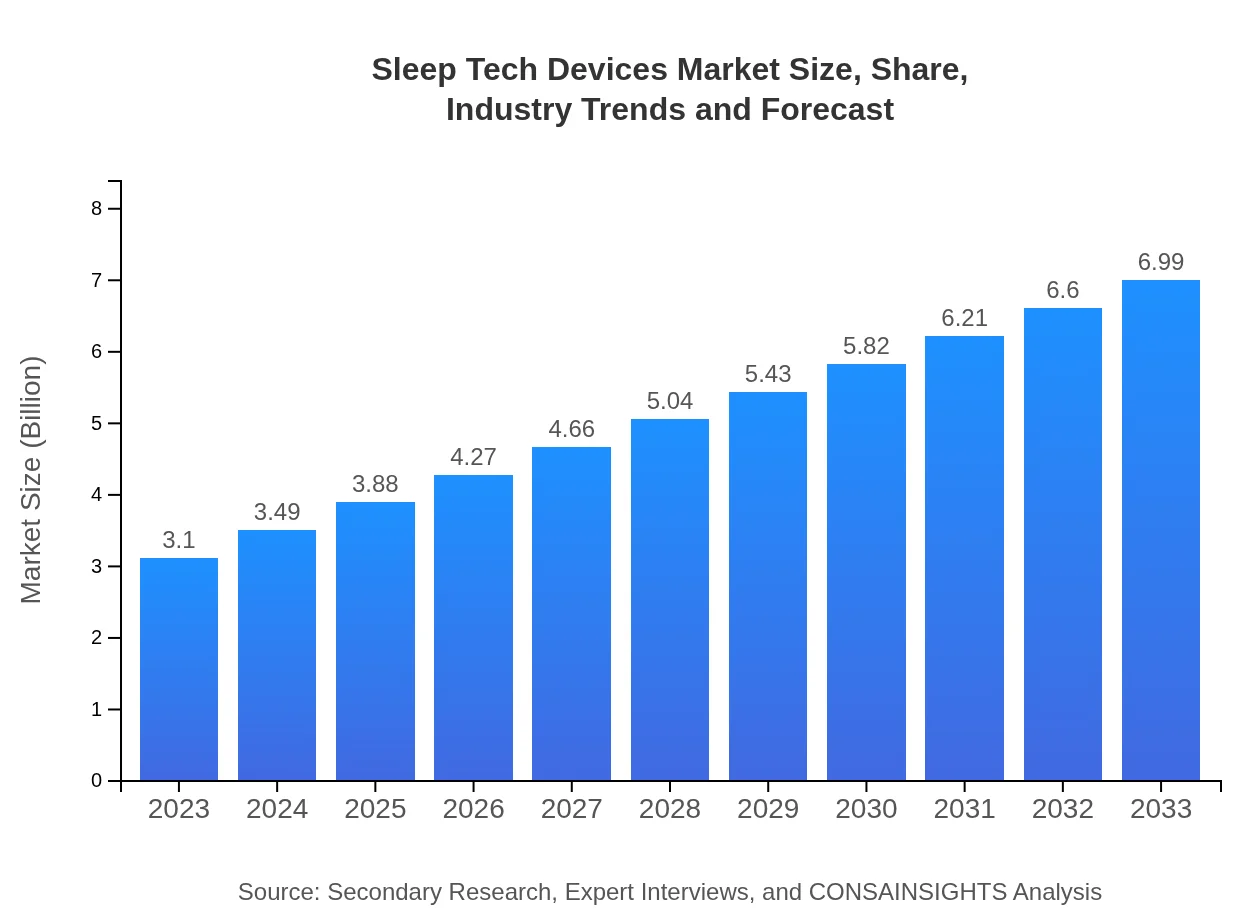

Sleep Tech Devices Market — USD $3.1 Billion in 2023, Growing to USD 6.99null by 2033 at 8.2% CAGR

This report delves deep into the Sleep Tech Devices market, providing insights into market size, growth trends, and regional analysis from 2023 to 2033. The forecast includes emerging technologies and the competitive landscape, offering stakeholders valuable information for strategic decision-making.

Key Takeaways

- Global market expands from $3.10 Billion in 2023 to $6.99 Billion in 2033 at an 8.2% CAGR.

- Europe is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- North America grows from $1.02 Billion to $2.30 Billion, reflecting strong demand for clinical and consumer devices.

- Wearables, monitoring sensors, and apps drive product innovation alongside integrations with AI and IoT.

- Top companies active include Fitbit, Inc., Philips Healthcare, Sleep Number Corporation, Garmin Ltd., and Oura Health Ltd.

Sleep Tech Devices Market Report — Executive Summary

Europe remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. This report examines the Sleep Tech Devices market from 2023 to 2033, charting growth from $3.10 Billion to $6.99 Billion at an 8.2% CAGR. Demand is supported by rising awareness of sleep health, wider consumer acceptance of wearables, and increased application of monitoring sensors and biofeedback technologies. Market structure spans wearables, non-wearables, software, and multiple distribution channels including online retail and direct sales. Regional dynamics vary: Europe is the largest market, while North America also posts substantial growth. Key company activity includes product innovation and partnerships between technology firms and healthcare providers, reinforcing clinical and consumer use cases. The analysis highlights segment breakdowns by user type, technology, price range, product type, and distribution, and outlines leading industry players and adoption drivers that will influence market trajectories through 2033.

Key Growth Drivers

- Growing consumer emphasis on sleep health and preventive wellness increases demand for monitoring and improvement tools.

- Integration of monitoring sensors and connected platforms enables personalized insights and continuous tracking.

- Expansion of clinical applications and collaborations between tech vendors and healthcare providers boosts credibility.

- Rising prevalence of sleep disorders and lifestyle-related sleep problems drives adoption across consumer and medical segments.

- Wider availability through online retail and direct sales channels enhances accessibility and market penetration.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $3.10 Billion |

| CAGR (2023-2033) | 8.2% |

| 2033 Market Size | $6.99 Billion |

| Top Companies | Fitbit, Inc., Philips Healthcare, Sleep Number Corporation, Garmin Ltd., Oura Health Ltd. |

| Published Date | 11 October 2024 |

| Last Modified Date | 28 May 2026 |

Sleep Tech Devices Market Overview

Customize Sleep Tech Devices Market Report market research report

- ✔ Get in-depth analysis of Sleep Tech Devices market size, growth, and forecasts.

- ✔ Understand Sleep Tech Devices's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Sleep Tech Devices

What is the Market Size & CAGR of Sleep Tech Devices Market Report market in 2023?

Sleep Tech Devices Industry Analysis

Sleep Tech Devices Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Sleep Tech Devices Market Report Market Analysis Report by Region

Europe Sleep Tech Devices Market Report:

Europe is largest regional market, rising from $1.05 Billion in 2023 to $2.36 Billion in 2033. 05 Billion in 2023 to $2.36 Billion in 2033 and is identified as the largest regional market. Growth reflects high awareness of sleep health, regulatory support for medical-grade devices, and partnerships between tech vendors and healthcare providers.Asia Pacific Sleep Tech Devices Market Report:

Asia Pacific grows from $0.58 Billion in 2023 to $1.31 Billion in 2033. Regional drivers include rising smartphone penetration, growing middle-class demand for wellness tech, and increasing availability of affordable wearable and non-wearable solutions.North America Sleep Tech Devices Market Report:

North America grows from $1.02 Billion in 2023 to $2.3 Billion in 2033. Regional expansion is driven by strong consumer adoption of wearables, health-conscious populations, clinical integration of monitoring devices, and widespread online and direct sales channels.South America Sleep Tech Devices Market Report:

Latin America grows from $0.25 Billion in 2023 to $0.55 Billion in 2033. Market progress is supported by improving access to consumer electronics, growing awareness of sleep disorders, and expanding online retail channels.Middle East & Africa Sleep Tech Devices Market Report:

Middle East and Africa grows from $0.21 Billion in 2023 to $0.46 Billion in 2033. Adoption is encouraged by urbanization, increasing healthcare investments, and expanding interest in preventive wellness technologies.Tell us your focus area and get a customized research report.

Research Methodology

Sleep Tech Devices Market Analysis By Product Type

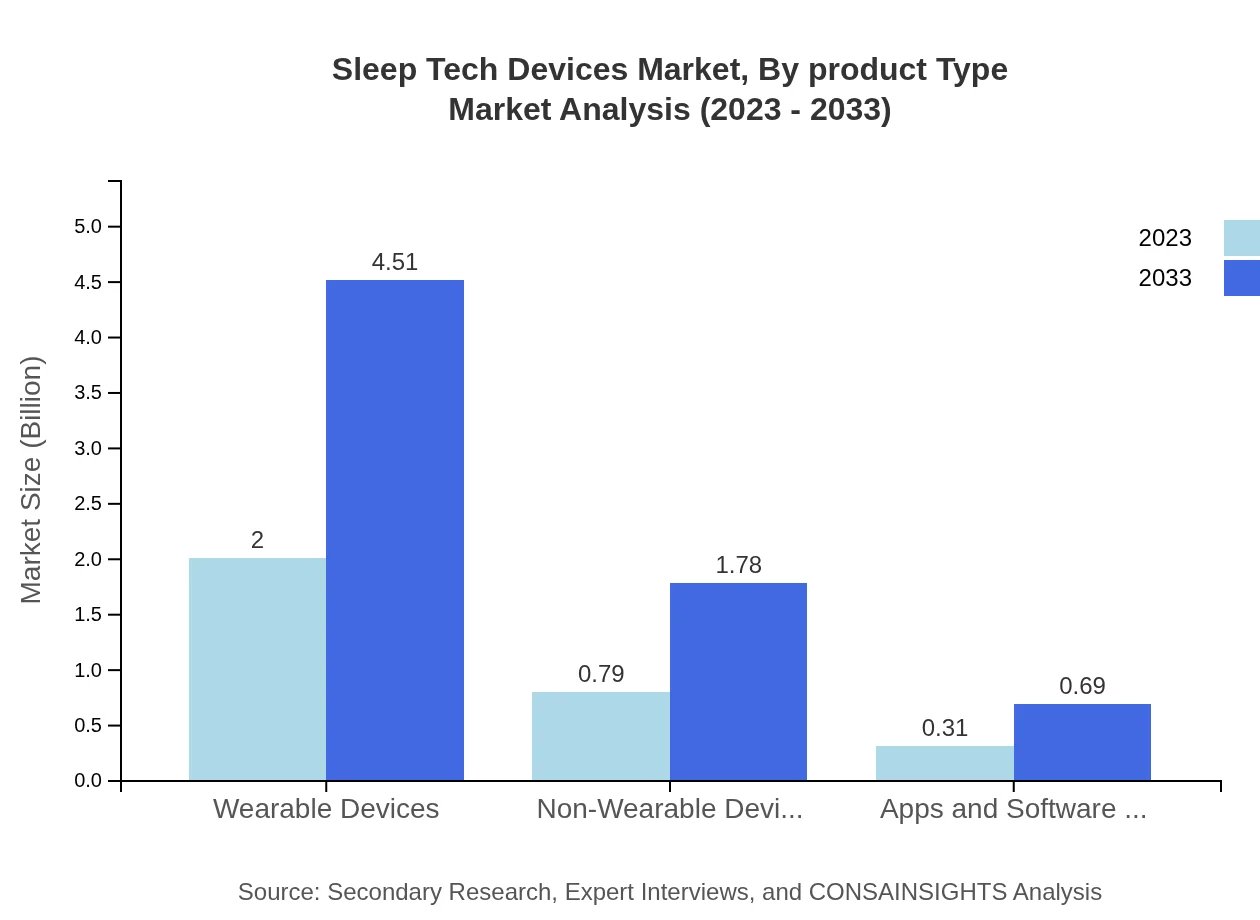

The Sleep Tech Devices market's product segmentation includes Wearable Devices ($2.00 billion in 2023, expected to reach $4.51 billion by 2033), Non-Wearable Devices ($0.79 billion in 2023, projected at $1.78 billion by 2033), and Software Applications ($0.31 billion in 2023 projected to $0.69 billion by 2033). Wearables hold significant market share due to their convenience and real-time tracking capabilities, appealing to health-conscious consumers.

Sleep Tech Devices Market Analysis By Technology

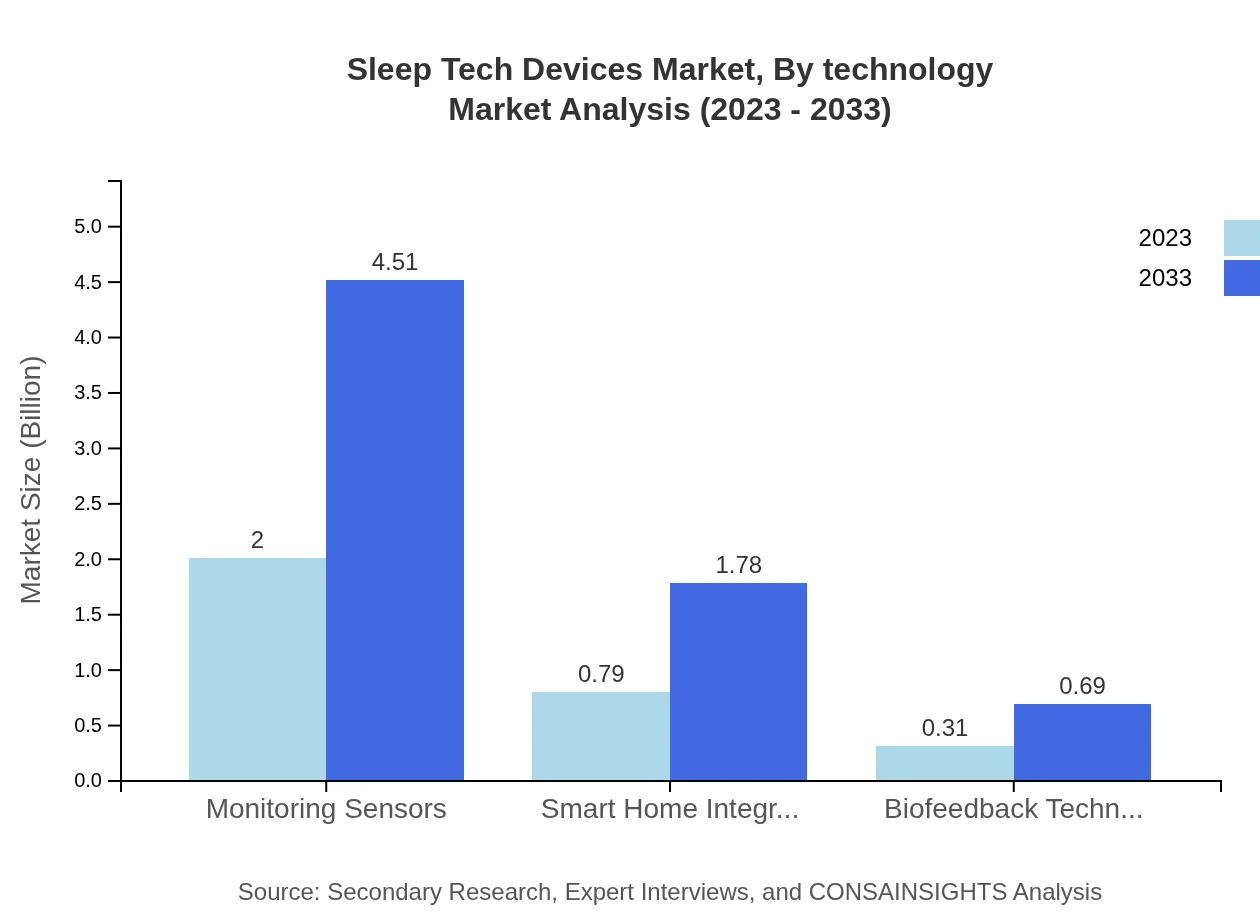

Technological advancements are at the forefront of the Sleep Tech market. Monitoring Sensors remain the largest segment at $2.00 billion in 2023 with a forecasted rise to $4.51 billion by 2033, showcasing the growing demand for accurate tracking solutions. Other technologies like Smart Home Integrations and Biofeedback Technologies are also gaining traction owing to the trend towards personalized health monitoring.

Sleep Tech Devices Market Analysis By Users

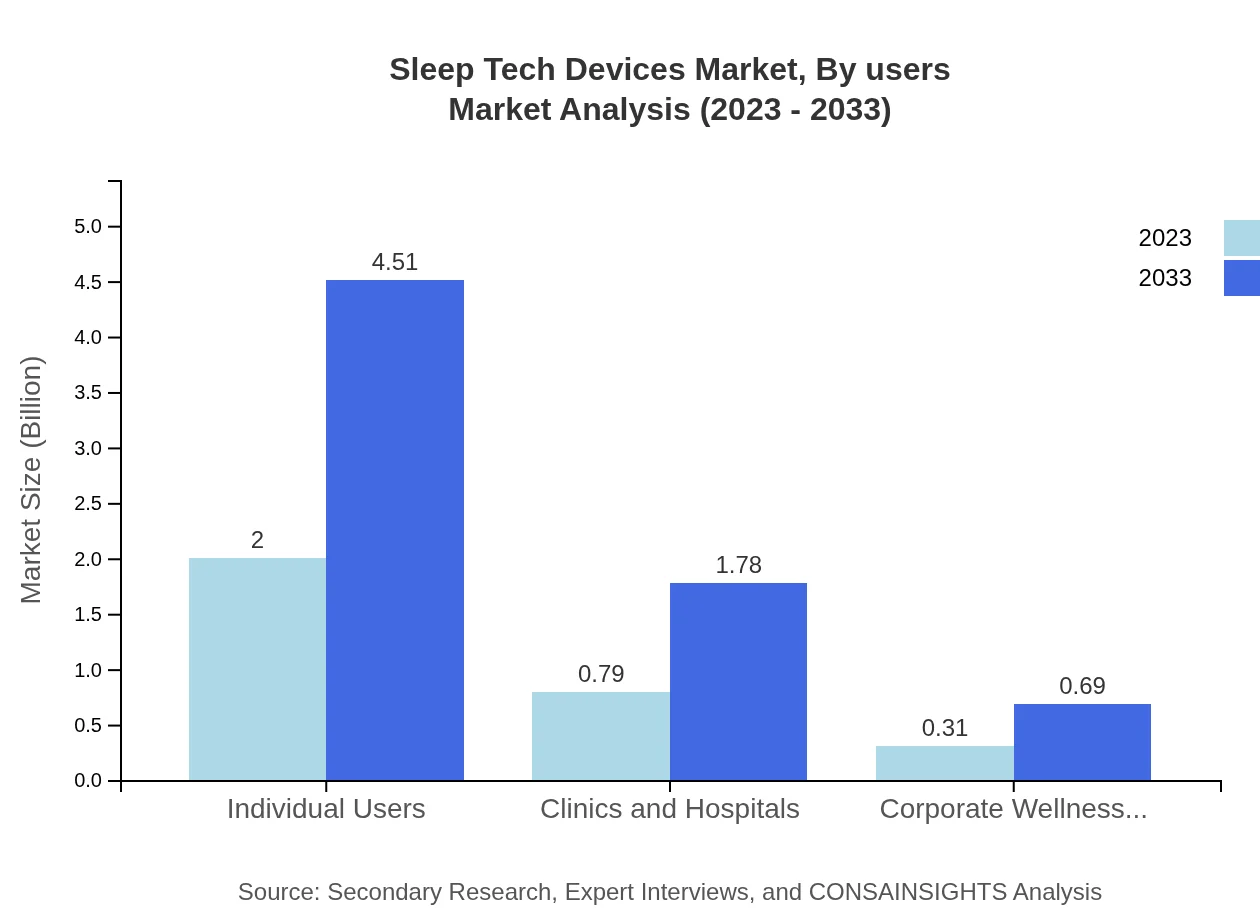

The market serves Individual Users ($2.00 billion in 2023, anticipated to reach $4.51 billion by 2033) and Clinics & Hospitals ($0.79 billion in 2023, expected to rise to $1.78 billion by 2033). Individual users dominate the market with a share of 64.6%, as consumers increasingly purchase sleep devices for personal health management, while healthcare facilities seek integrated solutions for patient care.

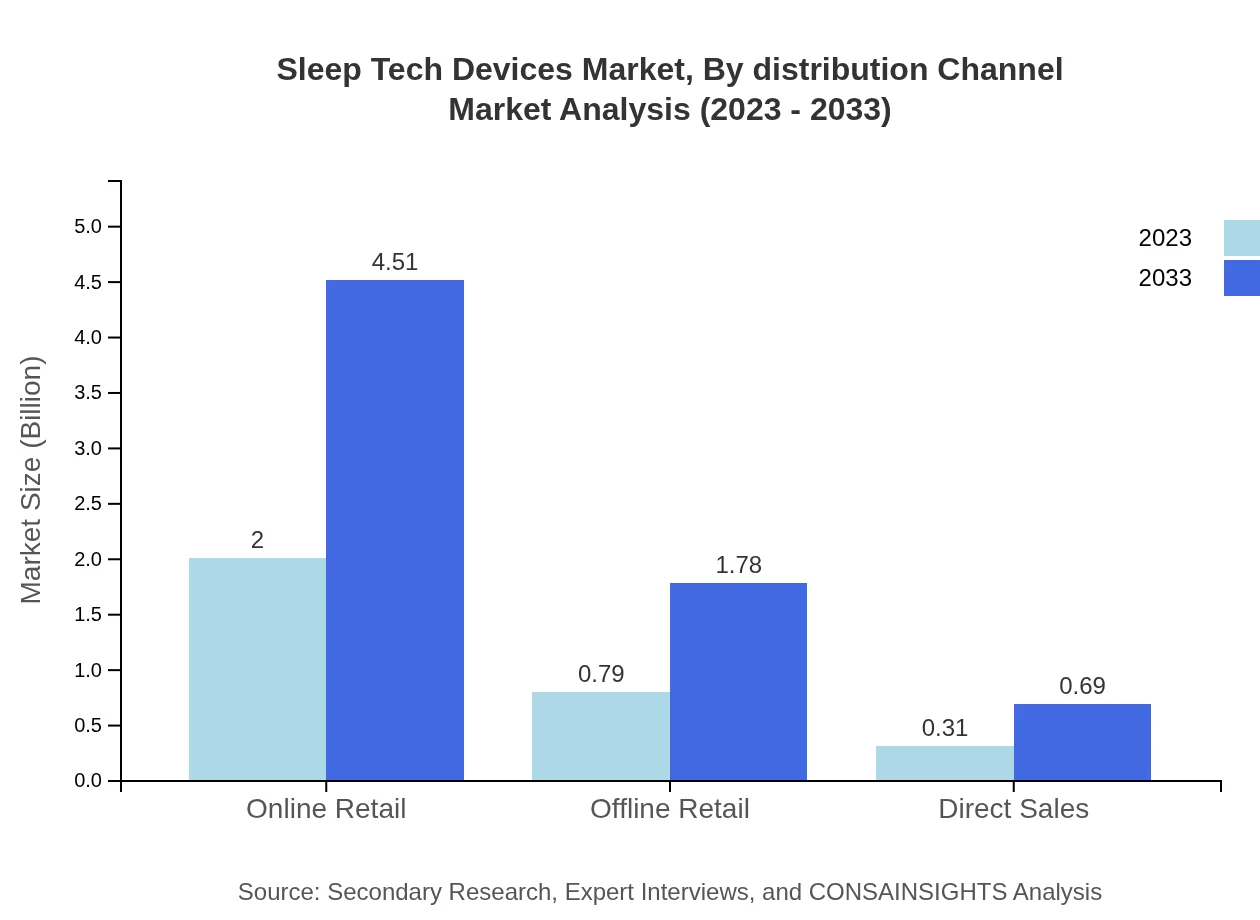

Sleep Tech Devices Market Analysis By Distribution Channel

Distribution channels encompass Online Retail ($2.00 billion in 2023, forecasted to $4.51 billion by 2033) and Offline Retail ($0.79 billion in 2023, expected to attain $1.78 billion by 2033). Online retail leads the way with a 64.6% share, supported by convenience and vast options. Offline channels continue growing as traditional retailers adapt and offer personalized selling experiences.

Sleep Tech Devices Market Analysis By Price Range

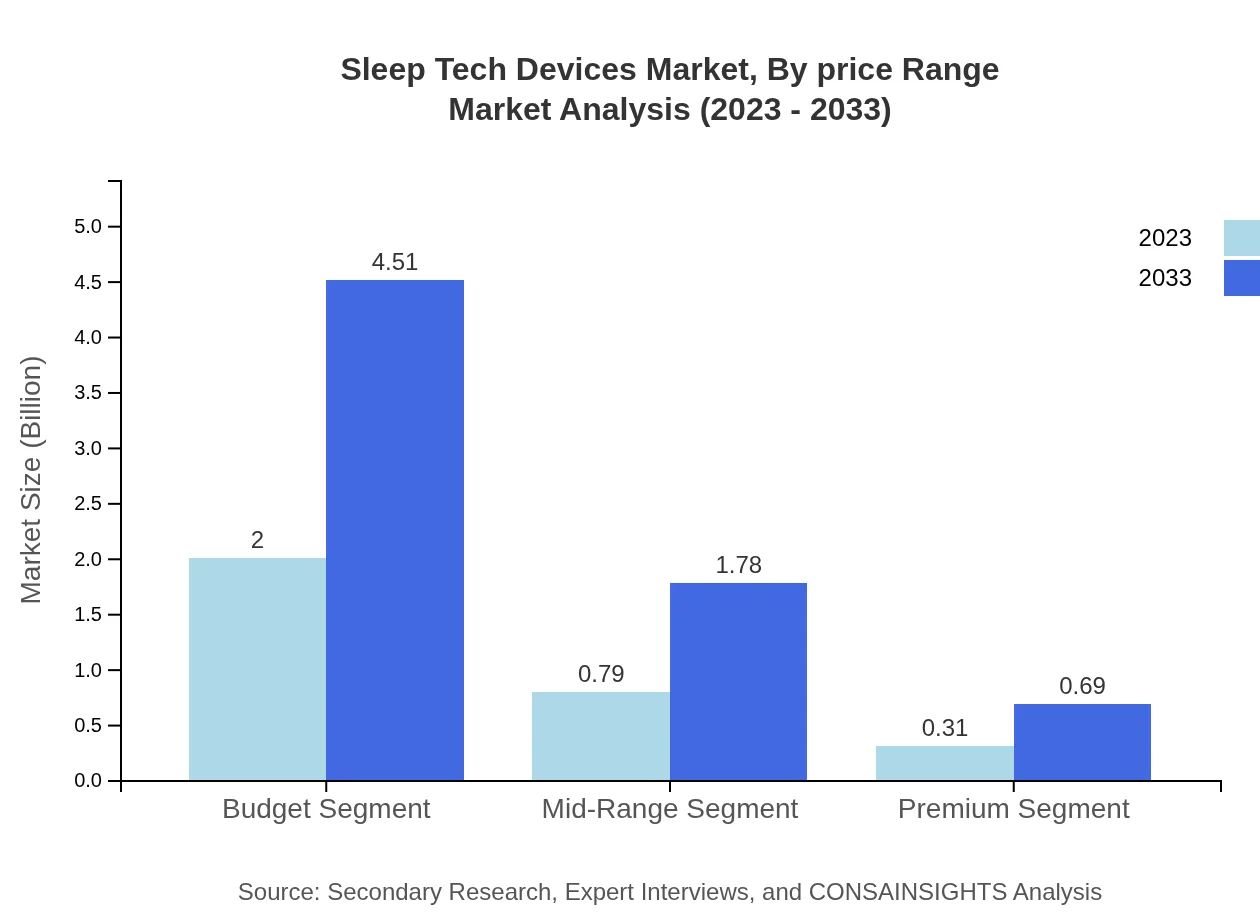

The Sleep Tech Devices segment by price includes Budget Segment ($2.00 billion in 2023 projected to $4.51 billion by 2033), Mid-Range Segment ($0.79 billion in 2023 set to rise to $1.78 billion by 2033), and Premium Segment ($0.31 billion in 2023 foreseen to reach $0.69 billion by 2033). Budget devices rule with a 64.6% share due to affordability, while premium options cater to niche markets focusing on advanced features.

Sleep Tech Devices Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Sleep Tech Devices Industry

Fitbit, Inc.:

A pioneer in wearable technology, Fitbit offers innovative sleep tracking devices that provide insights into sleep patterns and quality.Philips Healthcare:

Philips focuses on health technology and provides multiple solutions for sleep management, including smart beds and sleep therapy devices.Sleep Number Corporation:

Known for its adjustable beds, Sleep Number integrates smart technology to enhance sleep comfort, promoting overall better sleep quality.Garmin Ltd.:

Garmin develops a variety of wearables with advanced sleep tracking, emphasizing fitness and overall health monitoring.Oura Health Ltd.:

Oura produces a popular smart ring that tracks sleep patterns, delivering personalized insights for users to optimize their sleep health.We're grateful to work with incredible clients.

FAQs

What is the market size of the Sleep Tech Devices Market Report in 2023?

The market size for 2023 is $3.10 Billion as stated in the report's baseline year data and regional summaries.

How big will the Sleep Tech Devices Market Report market be in 2033?

By 2033 the market is projected to reach $6.99 Billion according to the forecast figures provided for the period 2023 to 2033.

What is CAGR for the forecast period?

The compounded annual growth rate for the forecast period 2023 to 2033 is 8.2% as reported in the market overview.

Is there a single fastest Growing region in the Sleep Tech Devices Market Report market?

No single fastest-growing region is stated for the Sleep Tech Devices Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Which companies are highlighted as key players?

Key companies listed in the report include Fitbit, Inc., Philips Healthcare, Sleep Number Corporation, Garmin Ltd., and Oura Health Ltd.

Who are the primary end users covered in segmentation?

Segmentation covers Individual Users, Clinics and Hospitals, and Corporate Wellness Programs as the main by-user categories.

What technologies are emphasized in the report?

The report emphasizes Monitoring Sensors, Smart Home Integration, and Biofeedback Technology as principal technology subsegments.

How are products categorized in the market breakdown?

Product classification includes Wearable Devices, Non-Wearable Devices, and Apps and Software Solutions across price and distribution segments.

What distribution channels are included?

Distribution channels outlined include Online Retail, Offline Retail, and Direct Sales to cover how devices reach consumers and institutions.

Why is clinical adoption important in the report?

Clinical adoption supports market credibility and broader use cases, linking device data with healthcare decision-making for diagnosis and management.