Spunbond Nonwoven Market Report

First published: 03 October 2024 | Last updated: 02 February 2026 | Report Code: spunbond-nonwoven

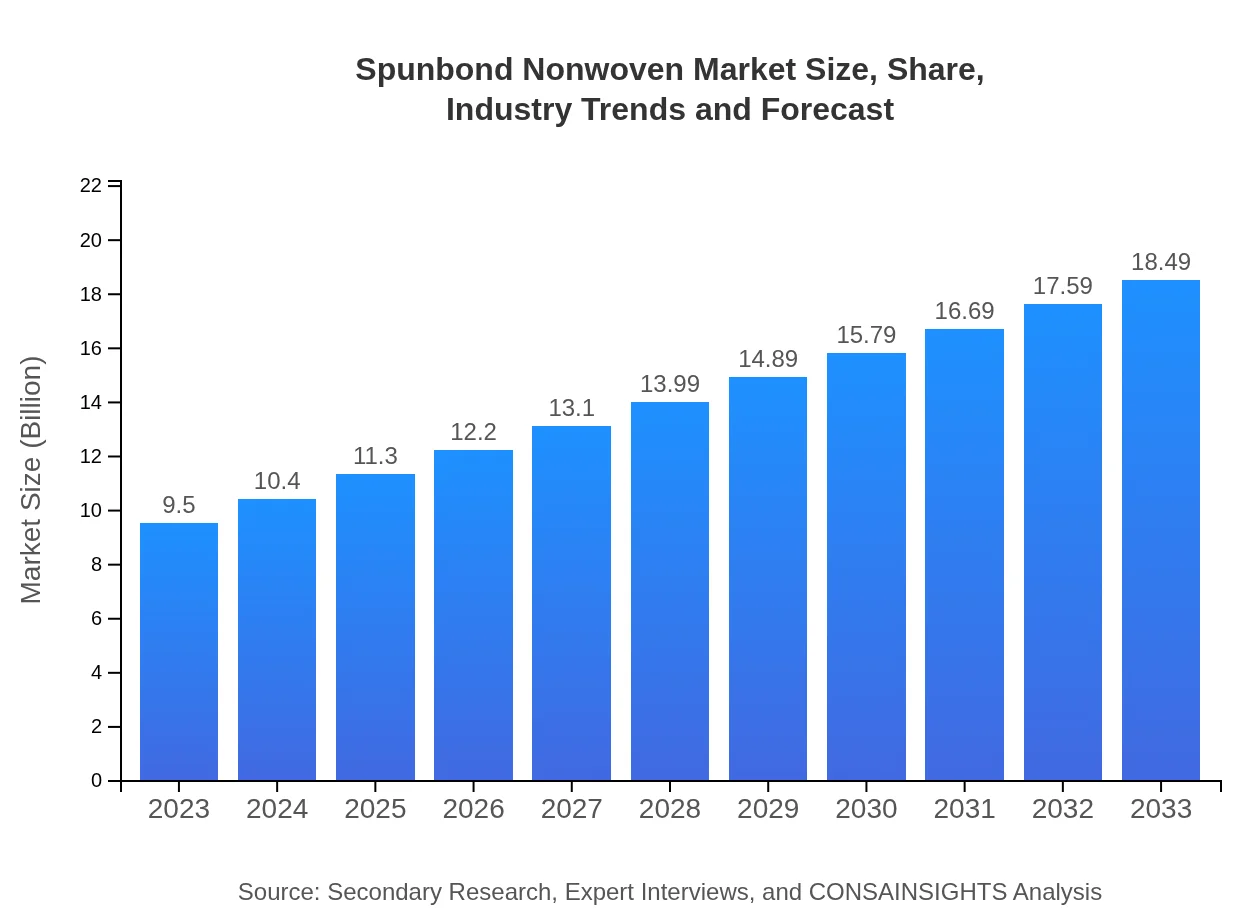

Spunbond Nonwoven Market — USD 9.5 billion in 2023, Growing to USD 18.49B by 2033 at 6.7% CAGR

This report provides a comprehensive analysis of the Spunbond Nonwoven market, including market size, trends, and forecasts from 2023 to 2033, with insights into key drivers, applications, and regional dynamics.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $9.50 Billion |

| CAGR (2023-2033) | 6.7% |

| 2033 Market Size | $18.49 Billion |

| Top Companies | Freudenberg Group, Berry Global, Inc., Lydall, Inc., Kimberly-Clark Corporation |

| Published Date | 03 October 2024 |

| Last Modified Date | 02 February 2026 |

Spunbond Nonwoven Market Overview

Customize Spunbond Nonwoven Market Report market research report

- ✔ Get in-depth analysis of Spunbond Nonwoven market size, growth, and forecasts.

- ✔ Understand Spunbond Nonwoven's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Spunbond Nonwoven

What is the Market Size & CAGR of Spunbond Nonwoven market in 2023?

Spunbond Nonwoven Industry Analysis

Spunbond Nonwoven Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Spunbond Nonwoven Market Analysis Report by Region

Europe Spunbond Nonwoven Market Report:

In Europe, the market size is expected to rise from USD 3.05 billion in 2023 to USD 5.94 billion by 2033. Stringency in regulations regarding environmental impact and an increasing focus on reusable materials are key drivers contributing to growth in this region.Asia Pacific Spunbond Nonwoven Market Report:

The Asia Pacific region is projected to grow significantly with an estimated market size of USD 3.41 billion by 2033, up from USD 1.75 billion in 2023. Factors such as increasing population, expanding urbanization, and heightened demand for hygiene products drive this growth. Additionally, evolving regulatory frameworks favoring sustainable practices further bolster the market environment.North America Spunbond Nonwoven Market Report:

The North American Spunbond Nonwoven market, valued at USD 3.38 billion in 2023, is projected to reach USD 6.59 billion by 2033, reflecting robust growth driven by healthcare demands and technological advancements in manufacturing processes. The region's strong emphasis on sustainability and eco-friendly practices will further enhance market dynamics.South America Spunbond Nonwoven Market Report:

The South American market is anticipated to grow from USD 0.63 billion in 2023 to USD 1.23 billion by 2033. Growth in this region is largely fueled by rising consumer awareness regarding hygiene and the adoption of nonwoven materials in diverse applications such as agriculture and consumer goods.Middle East & Africa Spunbond Nonwoven Market Report:

The Middle East and Africa market is anticipated to grow from USD 0.68 billion in 2023 to USD 1.32 billion by 2033. Increased investments in infrastructure and heavy reliance on nonwovens in hygiene products are essential for market expansion in these regions.Tell us your focus area and get a customized research report.

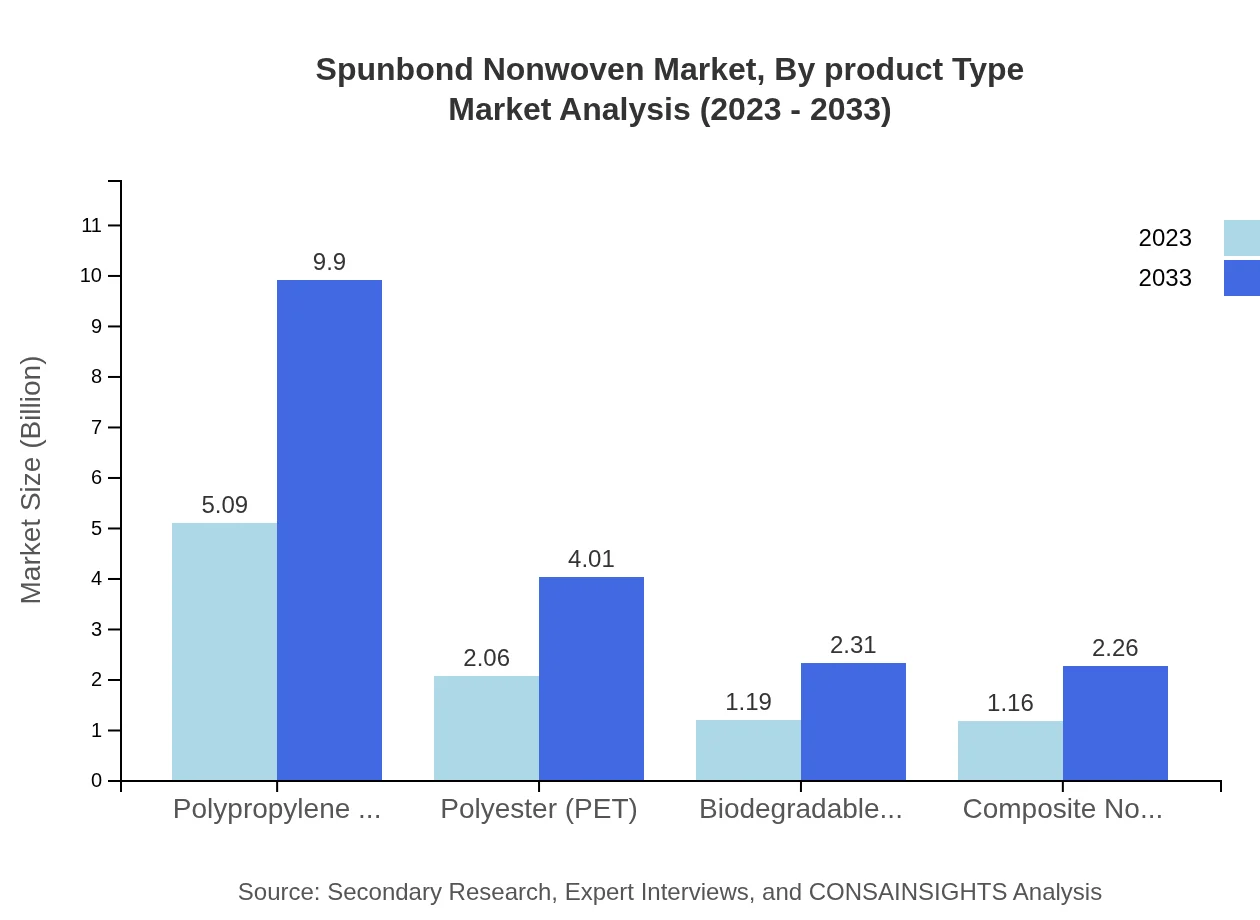

Spunbond Nonwoven Market Analysis By Product Type

The Spunbond Nonwoven market by product type is segmented into several categories including polypropylene (PP) and polyester (PET). Polypropylene remains the most significant segment, projecting a market size of USD 9.90 billion by 2033, maintaining a 53.56% market share. Polyester, critical for medical applications, is expected to reach USD 4.01 billion in the same year. Sustainable options like biodegradable nonwovens are also gaining traction, anticipated to account for 12.52% of the market share.

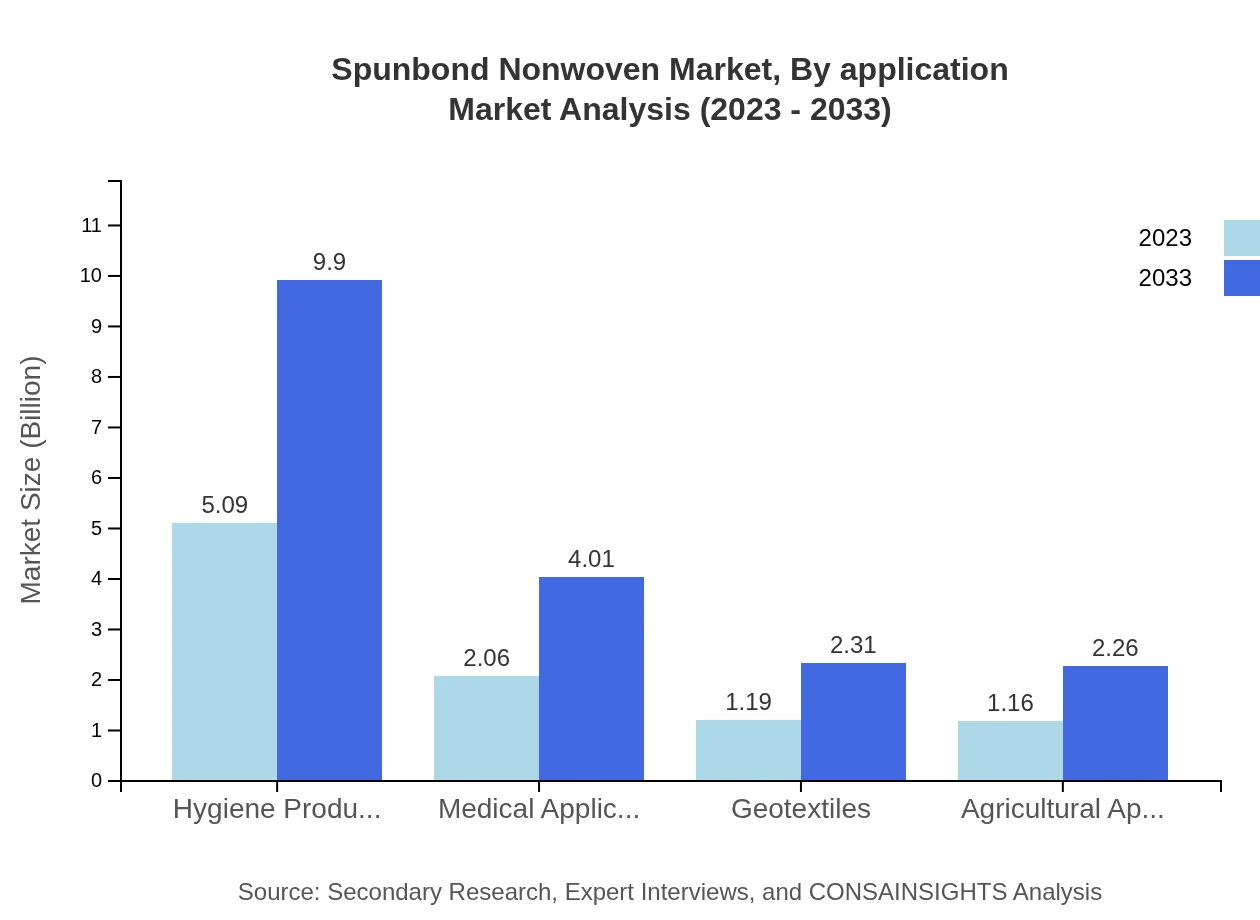

Spunbond Nonwoven Market Analysis By Application

The market for Spunbond Nonwoven segmented by application sees significant contributions from sectors like hygiene products, medical applications, and geotextiles. Hygiene products dominate with a projected size of USD 9.90 billion by 2033, while medical sectors hold a substantial share with an expected growth to USD 4.01 billion. Geotextiles, although smaller, are gaining traction, expected to achieve USD 2.31 billion demonstrating versatility in application.

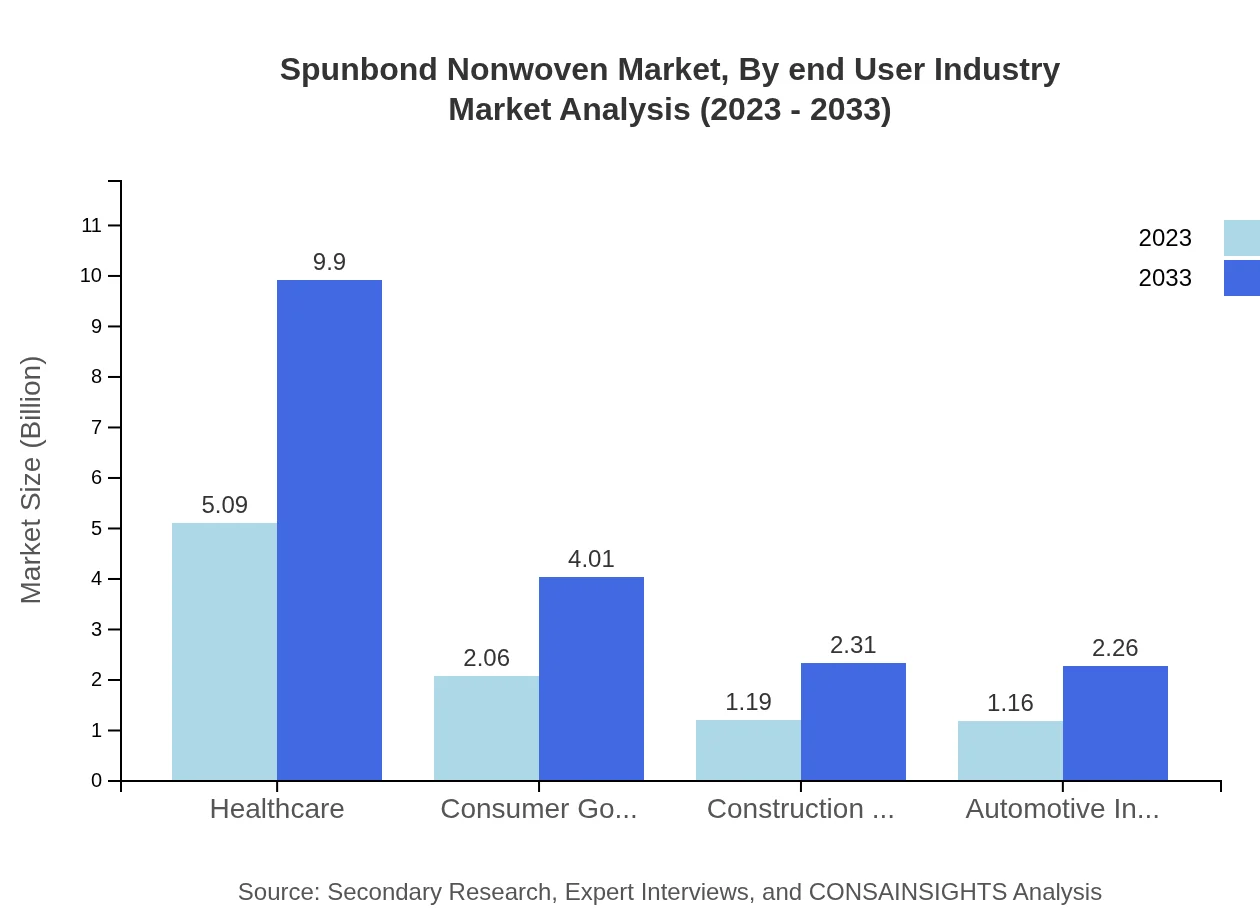

Spunbond Nonwoven Market Analysis By End User Industry

The Spunbond Nonwoven market by end-user industry comprises healthcare, consumer goods, automotive, and construction materials. Healthcare is the leading segment with an estimated value of USD 9.90 billion by 2033, accounting for 53.56% of the market share. The automotive segment, although smaller, is forecasted to grow to USD 2.26 billion, driven by demand for lightweight materials that enhance fuel efficiency.

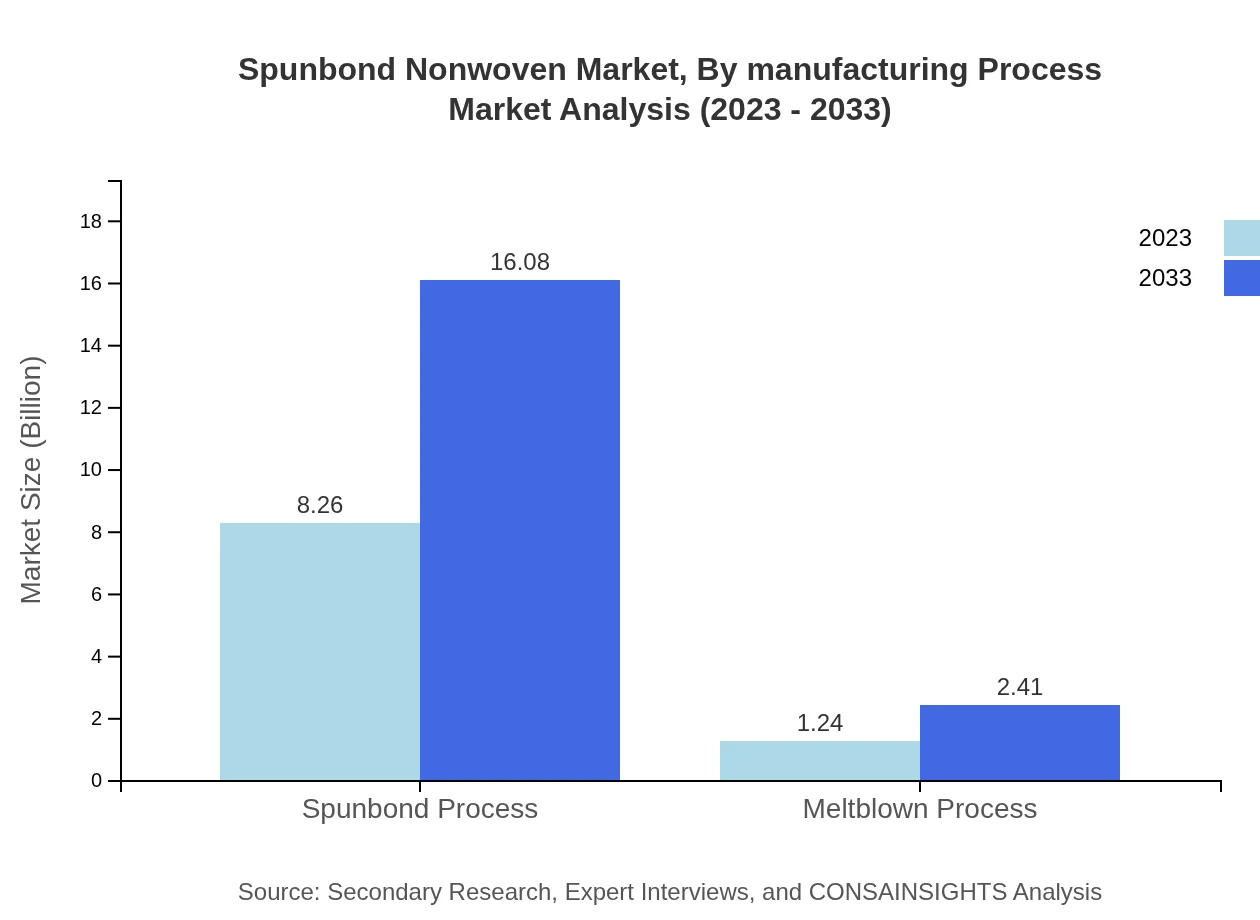

Spunbond Nonwoven Market Analysis By Manufacturing Process

The manufacturing process segment features spunbond and meltblown technologies. Spunbond dominates with an estimated market size of USD 16.08 billion by 2033, representing an impressive 86.98% of the market share. The meltblown process, significant for its applications in filtration and medical masks, is expected to reach USD 2.41 billion, representing the remaining market dynamics.

Spunbond Nonwoven Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Spunbond Nonwoven Industry

Freudenberg Group:

Freudenberg is a prominent player in the nonwoven industry, specializing in the development of high-performance nonwovens for various applications such as automotive, healthcare, and hygiene. Their innovation in lightweight and durable materials reinforces their market leadership.Berry Global, Inc.:

A key manufacturer in the global nonwoven textiles market, Berry Global specializes in producing sustainable and innovative spunbond products applicable in consumer goods, hygiene, and healthcare sectors, emphasizing their commitment to sustainability.Lydall, Inc.:

Lydall is recognized for its advanced nonwoven technologies catering mainly to filtration and insulation applications. Their diverse portfolio and strategic acquisitions have significantly strengthened their position in the market.Kimberly-Clark Corporation:

Known for its personal care and hygiene products, Kimberly-Clark utilizes spunbond technology extensively in producing efficient and high-quality nonwovens for hygiene applications worldwide.We're grateful to work with incredible clients.

FAQs

What is the market size of spunbond Nonwoven?

The global spunbond nonwoven market was valued at approximately $9.5 billion in 2023, with an expected compound annual growth rate (CAGR) of 6.7% through 2033. This growth underscores the increasing demand across diverse applications and industries.

What are the key market players or companies in this spunbond Nonwoven industry?

Key players in the spunbond nonwoven market include leading manufacturers such as Freudenberg, Berry Global, and Kimberly-Clark. These companies drive innovation and expansion within the sector, contributing to market dynamics and competition.

What are the primary factors driving the growth in the spunbond Nonwoven industry?

Factors driving growth in the spunbond nonwoven industry include rising demand for hygiene products, medical applications, and eco-friendly materials. Additionally, increased manufacturing capabilities and innovations in product technology enhance the market's appeal.

Which region is the fastest Growing in the spunbond Nonwoven?

The fastest-growing region in the spunbond nonwoven market is North America, with market size projected to grow from $3.38 billion in 2023 to $6.59 billion by 2033. Europe also shows significant growth from $3.05 billion to $5.94 billion during the same period.

Does ConsaInsights provide customized market report data for the spunbond Nonwoven industry?

Yes, ConsaInsights offers customized market report data for the spunbond nonwoven industry. This service allows clients to tailor insights and focus on specific segments, geographical areas, or market trends that are pertinent to their business needs.

What deliverables can I expect from this spunbond Nonwoven market research project?

Deliverables from the spunbond nonwoven market research project include detailed market analysis, regional and segment forecasts, competitive landscape insights, and actionable recommendations based on current industry trends and data.

What are the market trends of spunbond Nonwoven?

Key market trends in spunbond nonwoven include a surge in demand for hygiene products, innovations in biodegradable materials, and growth in medical applications. Additionally, the focus on sustainability drives diversification in product offerings and manufacturing technologies.