Automatic Conveyor Market Report

First published: 08 October 2024 | Last updated: 22 January 2026 | Report Code: automatic-conveyor

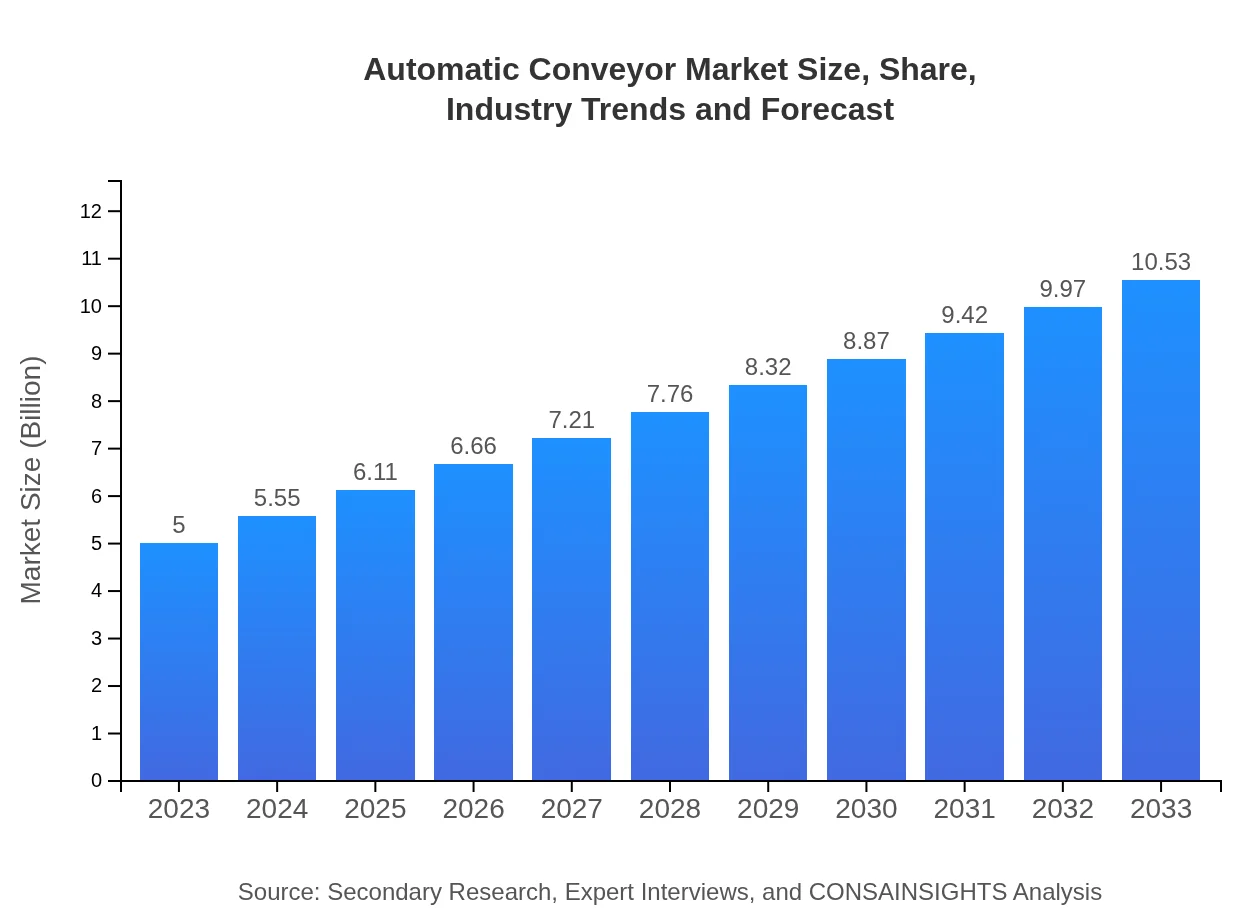

Automatic Conveyor Market — USD 5 billion in 2023, Growing to USD 10.53B by 2033 at 7.5% CAGR

This report provides an in-depth analysis of the Automatic Conveyor market, highlighting key trends, market sizes, and growth forecasts from 2023 to 2033. It offers insights into regional performance, market segmentation, and leading players in the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Honeywell Intelligrated, Siemens AG, Dematic, Schneider Electric, Fives Group |

| Published Date | 08 October 2024 |

| Last Modified Date | 22 January 2026 |

Automatic Conveyor Market Overview

Customize Automatic Conveyor Market Report market research report

- ✔ Get in-depth analysis of Automatic Conveyor market size, growth, and forecasts.

- ✔ Understand Automatic Conveyor's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Automatic Conveyor

What is the Market Size & CAGR of Automatic Conveyor market in 2023?

Automatic Conveyor Industry Analysis

Automatic Conveyor Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Automatic Conveyor Market Analysis Report by Region

Europe Automatic Conveyor Market Report:

Europe's Automatic Conveyor market will see an increase from $1.50 billion in 2023 to $3.16 billion by 2033, largely due to stringent regulations on manufacturing processes and the adoption of smart technologies.Asia Pacific Automatic Conveyor Market Report:

In the Asia-Pacific region, the Automatic Conveyor market is expected to grow from $0.98 billion in 2023 to $2.06 billion in 2033, driven by rapid industrialization and increased manufacturing activity, particularly in China and India.North America Automatic Conveyor Market Report:

The North American market is forecasted to rise from $1.76 billion in 2023 to $3.70 billion in 2033, supported by a strong emphasis on automation and efficiency across various industries, particularly transportation and warehousing.South America Automatic Conveyor Market Report:

The South American market is predicted to grow from $0.33 billion in 2023 to $0.69 billion by 2033. The expansion of the food and beverage sector is anticipated to boost the demand for automatic conveyors in the region.Middle East & Africa Automatic Conveyor Market Report:

The Middle East and Africa market, growing from $0.44 billion in 2023 to $0.92 billion in 2033, is propelled by investments in infrastructure development and a push towards automation in industrial processes.Tell us your focus area and get a customized research report.

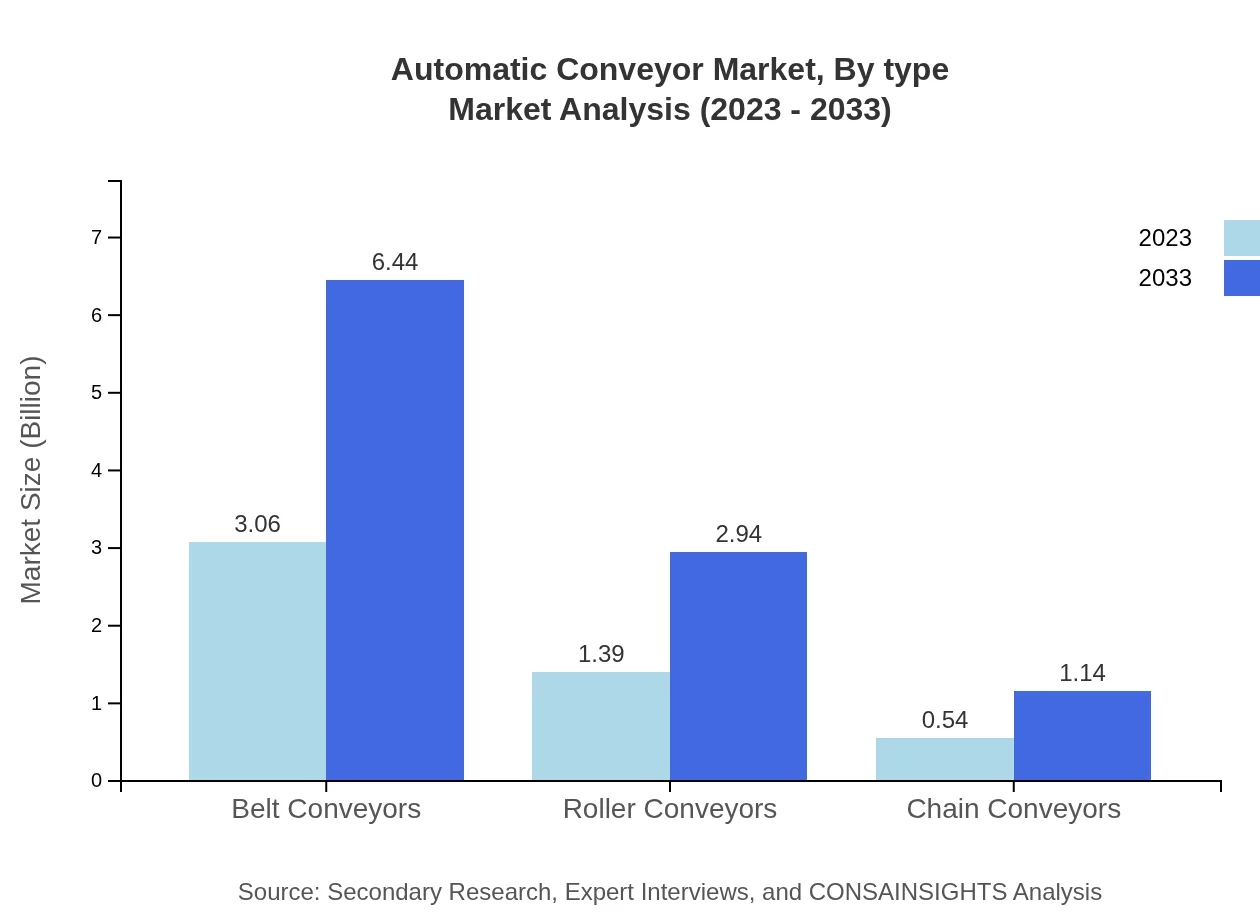

Automatic Conveyor Market Analysis By Type

The type segment indicates varying performance metrics for automatic conveyors. For instance, Belt Conveyors dominate with a projected size of $6.44 billion by 2033 from $3.06 billion in 2023, holding a market share of 61.23%. Roller Conveyors and Chain Conveyors follow with larger market sizes and shares projected to reach $2.94 billion and $1.14 billion respectively by 2033.

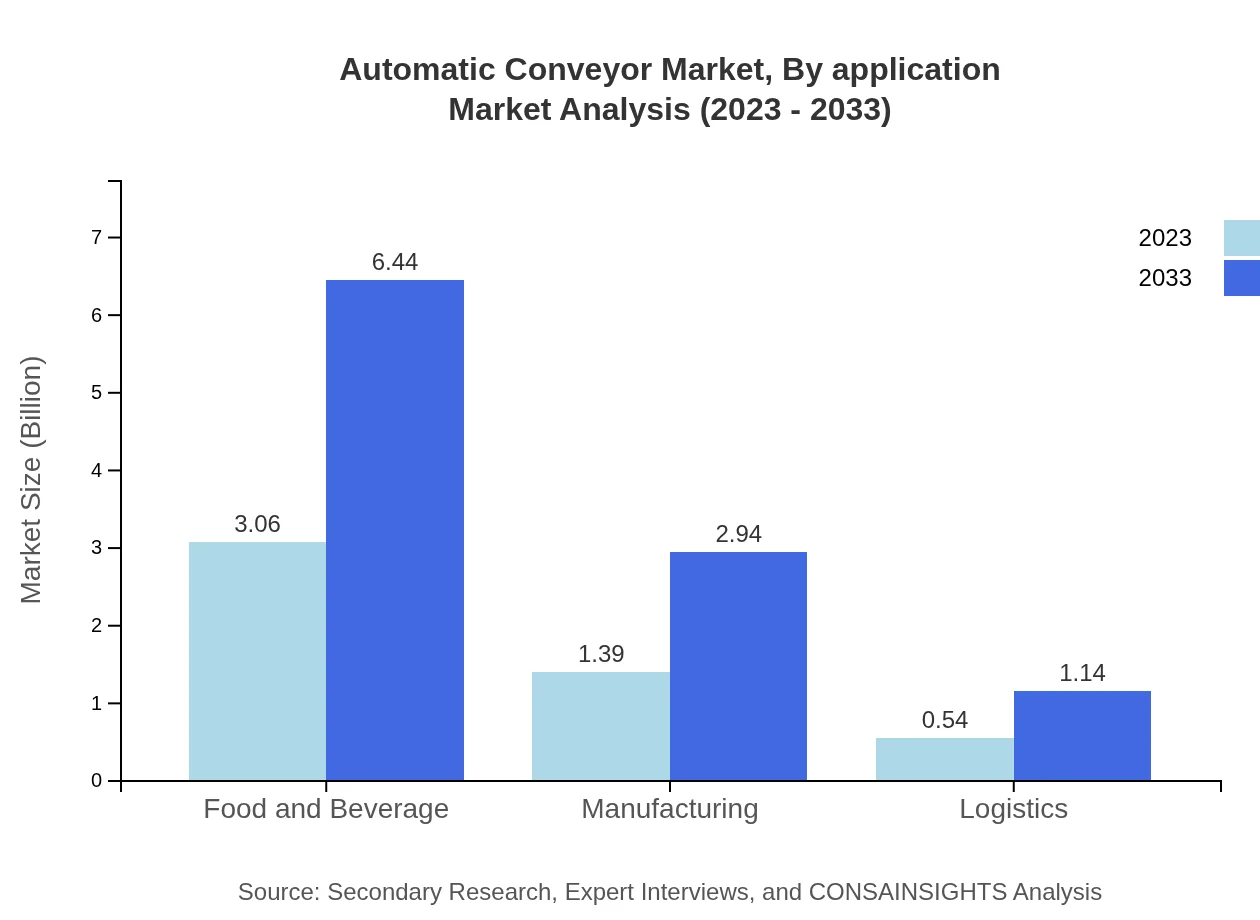

Automatic Conveyor Market Analysis By Application

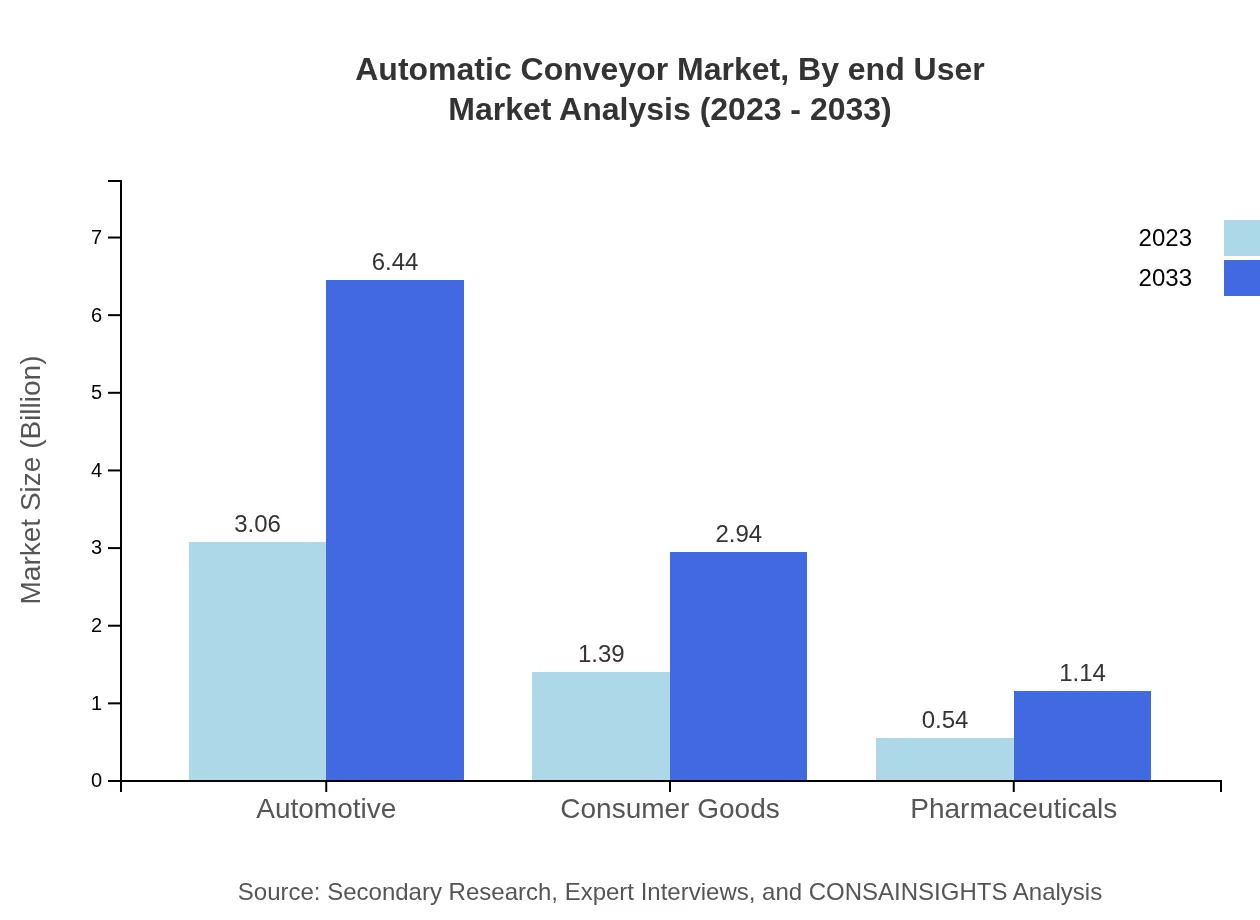

In terms of applications, Automotive and Food & Beverage sectors lead the market, with both projected to have the same size growth from $3.06 billion in 2023 to $6.44 billion in 2033, indicating their importance in the automatic conveyor landscape. The pharmaceuticals sector is also noteworthy, anticipated to grow from $0.54 billion to $1.14 billion.

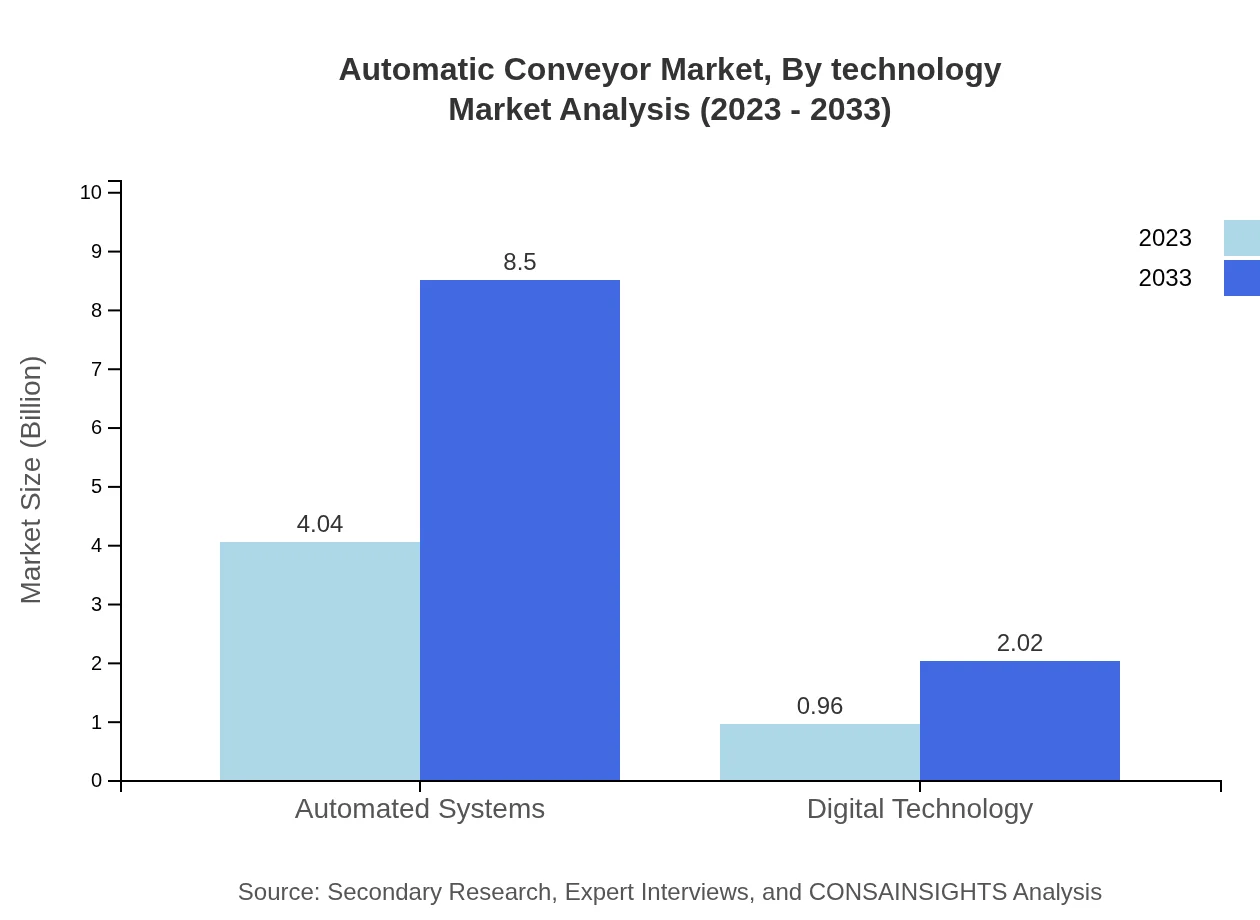

Automatic Conveyor Market Analysis By Technology

Technological advancements are profoundly impacting the Automatic Conveyor market. Automated systems are expected to maintain a significant size growth, reaching around $8.50 billion by 2033, holding 80.79% of the market share. Digital technology contributing $2.02 billion by 2033 represents 19.21% of the market share, showcasing the increasing influence of tech integration.

Automatic Conveyor Market Analysis By End User

End-user industries reveal the diverse applications of automatic conveyors. The automotive industry represents a major share, while the food and beverage industry showcases significant growth potential, reaching $6.44 billion. The pharmaceuticals sector is also growing increasingly important in the adoption of automatic conveying technology for efficient operations.

Automatic Conveyor Market Analysis By Geography

Geographical analysis delineates the market's performance across regions. North America stands out with robust growth projected, while Europe shows strong advancements in technology adoption. The Asia-Pacific market is rapidly expanding, with significant investments in manufacturing sectors, indicating a shift in global manufacturing hubs.

Automatic Conveyor Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Automatic Conveyor Industry

Honeywell Intelligrated:

A leading company in the automation and digital transformation of supply chains, specializing in advanced conveyor systems and logistics automation.Siemens AG:

A multinational corporation focused on digital industries, Siemens provides comprehensive conveyor solutions that integrate smart technology across manufacturing operations.Dematic:

A global leader in automated logistics, Dematic offers cutting-edge solutions, including intelligent conveyor systems designed for efficiency and scalability.Schneider Electric:

Known for its digital transformation services, Schneider Electric provides tailored conveyor systems aimed at improving operational efficiency and sustainability.Fives Group:

A well-established player in the automation sector known for its innovative conveyor technology that enhances productivity and operational capabilities across industries.We're grateful to work with incredible clients.

FAQs

What is the market size of automatic Conveyor?

The automatic conveyor market is valued at approximately $5 billion in 2023, with a projected compound annual growth rate (CAGR) of 7.5%, indicating significant growth potential through 2033.

What are the key market players or companies in the automatic Conveyor industry?

Key players in the automatic conveyor market include major manufacturers and suppliers that focus on innovative technologies, providing a wide range of conveyor solutions tailored to various industries, contributing significantly to market dynamics.

What are the primary factors driving the growth in the automatic Conveyor industry?

Growth is driven by increased automation in manufacturing, rising demand for efficiency in logistics, and advancements in conveyor technology, allowing industries to enhance productivity and reduce operational costs.

Which region is the fastest Growing in the automatic Conveyor?

Asia-Pacific is the fastest-growing region, with the market expected to grow from $0.98 billion in 2023 to $2.06 billion by 2033, indicating robust industrial development and expanding logistics networks.

Does ConsaInsights provide customized market report data for the automatic Conveyor industry?

Yes, ConsaInsights offers customized market report data for the automatic conveyor industry, allowing businesses to obtain specific insights tailored to their strategic needs and market positions.

What deliverables can I expect from this automatic Conveyor market research project?

Expect comprehensive reports including market size, trends, regional analysis, competitive landscape, and strategic recommendations tailored to the automatic conveyor industry for informed decision-making.

What are the market trends of automatic Conveyor?

Market trends include increasing adoption of smart conveyor systems, integration of IoT technologies, and growth of e-commerce logistics, all influencing the modernization and efficiency of conveyor operations.